Interior Architectural Coatings Market Size, Premiumization Trends, and Sustainable Interior Paint Demand Outlook

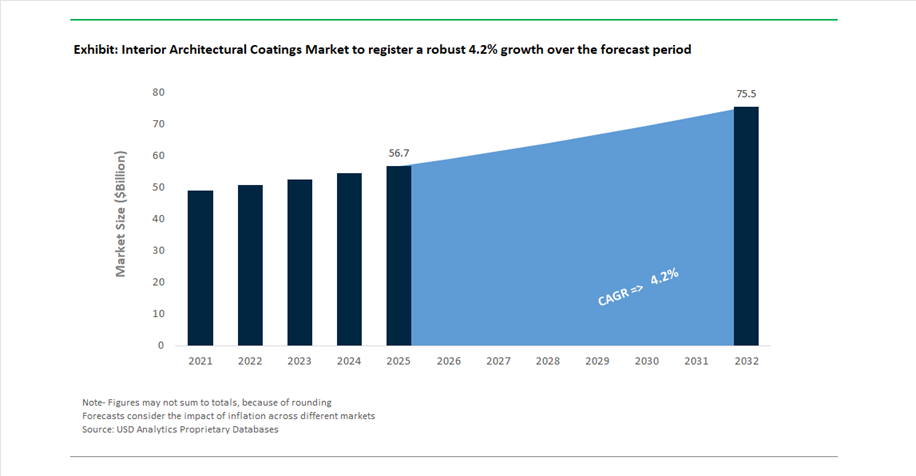

The global interior architectural coatings market was valued at $56.7 billion in 2025 and is projected to reach $75.6 billion by 2032, expanding at a CAGR of 4.2%. Growth is being driven by rising demand for low-VOC interior paints, zero-VOC coatings, high-durability interior coatings, and eco-friendly architectural coatings across residential, commercial, and institutional construction. Increasing emphasis on indoor air quality (IAQ), wellness-focused interiors, and sustainable building materials is transforming product innovation and procurement strategies in this market.

A key structural shift is the transition from traditional decorative paints to high-performance interior coatings that offer scuff resistance, stain resistance, antimicrobial properties, and air-purifying capabilities. The demand for premium emulsions and one-coat coverage paints is accelerating, particularly among professional contractors seeking efficiency and reduced labor costs. Additionally, the rise of urbanization, renovation cycles, and smart home trends is boosting consumption of advanced decorative coatings in both developed and emerging markets.

Sustainability remains central to market evolution. Regulatory pressures and green building certifications are pushing manufacturers to develop bio-based paints, plant-derived resins, and ultra-low odor formulations. Technologies such as infrared-reflective pigments and air-cleaning additives are gaining traction, especially in office spaces, schools, and healthcare facilities.

Pro-Segment Shift, and Eco-Innovation Redefining Competitive Dynamics

The interior architectural coatings industry is undergoing significant transformation driven by consolidation, portfolio realignment, and sustainability-focused innovation. In February 2026, AkzoNobel and Axalta announced a landmark all-stock merger, combining AkzoNobel’s Dulux decorative coatings leadership with Axalta’s industrial and building product expertise. This creates a ~$17 billion global coatings entity, significantly consolidating the premium interior coatings segment and strengthening global distribution and product development capabilities.

A major trend shaping the market is the shift toward the professional contractor (Pro) segment, as DIY demand softens in mature markets. Sherwin-Williams, in March 2025, launched its Pro-Series High-Performance interior coatings, emphasizing one-coat coverage, ultra-low odor, and durability, specifically targeting professional applicators. Supporting this trend, Masco (Behr) reported in February 2025 that Pro segment sales continued to grow, even as overall DIY retail sales declined, prompting increased R&D investment in contractor-grade interior finishes. Similarly, PPG Industries introduced ANTI-SCUF Zero VOC interior coatings in July 2025, engineered for high-traffic commercial environments such as offices and schools, where durability and maintenance reduction are critical.

Sustainability-driven product innovation is rapidly gaining momentum. In November 2025, Behr launched BEHR PREMIUM PLUS® ECOMIX™, a plant-based, zero-VOC interior paint meeting the USDA BioPreferred Program’s renewable material threshold while maintaining Greenguard Gold certification. AkzoNobel further advanced this trend with its September 2025 “Color of the Year” launch, featuring coatings designed for wellness-focused interiors, incorporating low-emission and air-purifying technologies. Additionally, the March 2024 strategic alliance between Evonik and Nippon Paint is accelerating the development of bio-based interior coatings, combining advanced additives with large-scale distribution networks, particularly in China.

Strategic portfolio realignment is also reshaping competitive positioning. PPG Industries’ October 2024 divestment of its North American architectural coatings business marks a decisive pivot toward high-performance industrial coatings, while Sherwin-Williams’ October 2025 acquisition of BASF’s Brazilian paints business (Suvinil) strengthens its dominance in South America’s interior decorative coatings market.

Emerging markets continue to play a critical role in growth. Asian Paints’ January 2024 expansion in India, with a new automated manufacturing facility, supports rising demand for premium decorative emulsions and integrated home décor services, reflecting the increasing convergence of coatings, design, and lifestyle solutions.

Interior Architectural Coatings Market Share 2025: Wall Paint Dominance and Specialty Retail Leadership

Product Type Insights: Interior Wall Paints Lead with High Volume Demand and Advanced Features

The interior wall paints segment dominates the interior architectural coatings market with a substantial 58% market share in 2025, driven by its extensive application across residential, commercial, and institutional interiors. Wall paints cover the largest surface area in buildings, making them the most frequently used coating type, with repainting cycles typically ranging from 3 to 7 years, ensuring consistent replacement demand. The segment is further strengthened by continuous product innovation, including washable, scuff-resistant, stain-blocking, and low-VOC formulations that enhance durability and indoor air quality. Premium features such as antimicrobial coatings and air-purifying paints are gaining traction, particularly in healthcare facilities, schools, and high-traffic commercial spaces. As consumers and contractors increasingly prioritize both aesthetics and performance, interior wall paints will continue to dominate the global interior architectural coatings market.

Sales Channel Insights: Specialty Paint Stores Lead with Expertise and Contractor Loyalty

The specialty paint stores segment holds the largest 45% share in the interior architectural coatings market in 2025, driven by its ability to offer expert guidance, precise color matching, and premium product availability. These stores provide advanced tinting systems, brand-exclusive formulations, and technical advice, which are highly valued by both DIY consumers and professional painters seeking high-quality finishes. A key competitive advantage lies in their strong relationships with contractors, supported by loyalty programs, bulk purchase discounts, job tracking tools, and dedicated account management services. This personalized approach ensures repeat business and long-term customer retention, even in the face of price competition from big-box retailers. Additionally, specialty stores often stock high-performance and eco-friendly coatings, catering to evolving market preferences. As demand for customized solutions and professional-grade coatings grows, specialty paint stores will remain the leading sales channel in the interior architectural coatings market.

Interior Architectural Coatings Market Competitive Landscape: Digital Color Innovation, Sustainable Formulations, and Pro-Contractor Dominance

The interior architectural coatings market is highly competitive, driven by digital color technologies, low-VOC sustainable paints, and the rapid shift toward professional contractor networks. Leading players are leveraging AI-enabled color platforms, green building compliance, and premium functional coatings to capture growth in residential renovation and commercial interior segments.

Sherwin-Williams drives pro-contractor dominance with AI color forecasting and omnichannel sales growth

The Sherwin-Williams Company is reinforcing its leadership in interior architectural coatings through digital commerce and professional contractor integration. The company generated $340 million in online sales in 2025, with algorithm-driven upselling increasing average order value by 22% compared to physical stores. Its 2026 Colormix Forecast: Anthology Volume Two introduces 48 curated shades, including Modern Lavender (SW 9688), shifting toward emotion-driven color frameworks. A 7% price increase in 2026 helped offset TiO₂ and resin supply volatility while supporting EPS guidance of $11.50 to $11.90. Its network of 5,000+ stores remains a key differentiator, enabling "Just-in-Time" delivery and industrial-grade durability solutions for high-traffic commercial interiors. This integrated digital and physical ecosystem secures Sherwin-Williams’ dominance in the professional coatings segment.

AkzoNobel accelerates sustainable architectural coatings with AR-enabled color tools and mega-merger strategy

AkzoNobel N.V. is advancing its position in interior architectural coatings through sustainability and digital innovation. The company’s "Rhythm of Blues" 2026 Color of the Year series, supported by an augmented reality calculator, has reduced over-ordering by 30% across 1.2 million users. Its planned $25 billion merger with Axalta is set to create the world’s largest performance and sustainable coatings entity. Strategic divestments, including Pakistan and India operations, are sharpening its focus on high-margin European and North American green building markets. AkzoNobel has also achieved 100% reusable waste across key European plants, aligning with its goal to reduce value chain emissions by 50% from 2018 levels. This combination of digital tools and sustainability leadership strengthens its competitive positioning.

Nippon Paint scales self-cleaning interior coatings and pro-painter networks across Asia-Pacific

Nippon Paint Holdings is leveraging its strong Asia-Pacific presence to expand in the interior architectural coatings market. The company reported ¥1,774.2 billion in revenue with 17.5% gross profit growth in early 2026, driven by its NIPSEA regional ecosystem. Its FASTAR technology introduces hydrogel-based self-cleaning interior coatings that resist household pollutants, addressing growing demand for low-maintenance surfaces. Nippon Paint is shifting toward a ROIC-focused "Asset Assembly" strategy, targeting bolt-on acquisitions in ASEAN and North America. The company is also prioritizing "Do-It-For-Me" (DIFM) service networks, capturing the rapid expansion of professional painter services over DIY trends. This strategy enhances its scalability and market penetration.

Asian Paints strengthens premium interior coatings with health-focused formulations and design-led innovation

Asian Paints Limited is solidifying its leadership in the interior coatings market through premiumization and functional innovation. Its 2026 Color of the Year, Moonlit Silk (7809), reflects a shift toward calming, wellness-driven interior aesthetics. The Royale Health Shield range continues to gain traction, offering anti-bacterial and dust-resistant properties that improve indoor air quality. The company’s "IRL" design philosophy emphasizes tactile finishes such as lime plaster and concrete textures, aligning with evolving consumer preferences. Asian Paints dominates the Indian subcontinent through its integrated Home Solutions network, combining waterproofing and decorative coatings. This strong distribution and innovation pipeline supports its leadership in high-growth residential markets.

Behr (Masco) captures DIY leadership with one-coat performance and AI-driven color visualization

Masco Corporation’s Behr Paint Company is a key player in the DIY architectural coatings segment, driven by product performance and digital integration. Its BEHR® 2026 Commercial Color Forecast features 50 curated shades under the "Elemental Harmony" theme, guided by a newly formed Designer Council. The BEHR DYNASTY® and MARQUEE® lines set industry benchmarks with a one-coat hide guarantee covering up to 400 sq. ft. per gallon. The company leverages ColorSmart by BEHR® AI visualization tools to reduce product return rates below 2%, enhancing customer satisfaction. Its strong retail partnership with Home Depot ensures widespread accessibility for consumers. This focus on convenience and performance strengthens Behr’s competitive edge in the DIY segment.

Pittsburgh Paints emerges as a focused North American leader with zero-VOC contractor-grade solutions

Pittsburgh Paints Co., backed by American Industrial Partners, has emerged as a specialized leader in interior architectural coatings following its $550 million acquisition from PPG. The company operates over 15,000 points of sale, targeting both residential and commercial markets across North America. Its "Pure Play" architectural strategy emphasizes high-volume contractor networks and zero-VOC coatings aligned with tightening environmental regulations. The rebranding of legacy products into the Pittsburgh Paints™ portfolio supports a cohesive market identity. The company is positioned to capitalize on the 5.7% growth in renovation of post-1970 housing stock. This focused approach enhances its competitiveness in the regional architectural coatings landscape.

United States Interior Architectural Coatings Market: Indoor Air Quality Innovation and Healthy Building Demand

The United States interior architectural coatings market is undergoing a structural shift toward healthier and environmentally compliant solutions, driven by increasing awareness around indoor air quality (IAQ) and regulatory tightening. The introduction of stricter VOC limits under federal environmental policies has accelerated the transition toward ultra-low-VOC interior paints, particularly in matte finishes. These regulatory developments are pushing manufacturers to innovate in eco-friendly architectural coatings that align with stringent air quality standards.

Technological advancements are further reshaping the market landscape. The development of formaldehyde-scavenging coatings is enabling active neutralization of indoor pollutants, significantly improving residential air quality. Additionally, the launch of PFAS-free stain-resistant coatings using advanced acrylic-silane hybrids is addressing growing concerns over harmful chemicals while maintaining durability. Infrastructure investments under “Healthy Building” initiatives are boosting demand for insulative interior coatings that enhance energy efficiency. The increasing adoption of antimicrobial coatings in office spaces and commercial buildings is also contributing to market growth, as organizations prioritize hygiene and occupant safety in post-pandemic environments.

China Interior Architectural Coatings Market: Waterborne Transition and Smart City Expansion

China continues to lead the global interior architectural coatings market, driven by strong regulatory enforcement and rapid urbanization. Government mandates requiring the use of 100% waterborne coatings in new public infrastructure projects are significantly accelerating the shift toward environmentally friendly paint systems. These initiatives are aligned with broader decarbonization goals under national development plans, ensuring large-scale adoption of low-emission coatings across residential and commercial sectors.

Technological innovation is also playing a crucial role in market expansion. The commercialization of graphene-enhanced coatings is improving coverage efficiency and reducing material consumption, while rapid-drying and odorless paints are supporting fast-paced urban housing developments. The expansion of social housing projects is creating sustained demand for high-performance interior coatings that enable quick occupancy cycles. Additionally, the adoption of negative-ion coatings in high-density residential spaces is addressing health concerns such as sick building syndrome. The presence of global and domestic manufacturers investing in bio-based coating production further strengthens China’s leadership in sustainable interior coatings.

India Interior Architectural Coatings Market: Smart Cities and Premiumization Driving Growth

India is witnessing one of the fastest growth rates in the interior architectural coatings market, fueled by urbanization and the premiumization of residential and commercial spaces. Government initiatives such as the Smart Cities Mission and large-scale housing programs are creating a substantial pipeline for high-performance interior coatings. These projects are driving demand for durable, self-cleaning, and aesthetically advanced coatings in public infrastructure and residential developments.

Product innovation is a key growth driver, with the introduction of antiviral and antifungal coatings gaining traction in metropolitan areas. Strategic investments by global and domestic players are enhancing supply chain efficiency, particularly through localized production and digital platforms for customized color solutions. The adoption of augmented reality-based visualization tools is further influencing consumer preferences toward premium finishes and personalized interior designs. Regulatory measures ensuring product quality are eliminating sub-standard imports, strengthening the organized market segment. These factors collectively position India as a major growth engine in the global interior architectural coatings market.

Germany Interior Architectural Coatings Market: Bio-Based Innovation and Circular Economy Leadership

Germany serves as the innovation hub for sustainable interior architectural coatings in Europe, driven by strict REACH compliance and ambitious environmental targets. The market is characterized by a strong focus on bio-based materials and circular economy principles. The commercialization of de-coatable coatings is enabling complete recyclability of substrates during renovation, aligning with sustainability goals and reducing construction waste.

Technological advancements are further enhancing market growth. The adoption of UV-LED curing technologies is reducing energy consumption in coating applications, while the development of carbon-negative coatings is supporting green building certifications. Regulatory frameworks are also driving innovation, with stricter limits on chemical migration encouraging the use of safer resin systems. High demand for mineral-based paints in heritage building renovations highlights Germany’s commitment to balancing sustainability with architectural preservation. These innovations position Germany as a leader in environmentally responsible interior coating solutions.

United Arab Emirates Interior Architectural Coatings Market: Premium Finishes and Green Building Codes

The United Arab Emirates represents a high-value market for interior architectural coatings, driven by rapid urban development and a thriving hospitality sector. Large-scale tourism and real estate projects are significantly increasing demand for premium interior finishes, particularly in luxury hotels and commercial spaces. These coatings are designed to withstand high traffic while maintaining aesthetic appeal and durability.

Regulatory frameworks are shaping the market, with strict VOC limits and environmental standards encouraging the adoption of eco-friendly coatings. Technological innovations such as heat-reflective interior coatings are improving energy efficiency in high-rise buildings, reducing cooling costs in extreme climates. Investments in smart manufacturing facilities are also enhancing local production capabilities for advanced coating systems. Additionally, the use of low-odor, rapid-occupancy coatings is supporting fast-paced refurbishment projects, particularly in retail and hospitality sectors. These factors position the UAE as a key market for high-performance interior coatings in the Middle East.

Vietnam Interior Architectural Coatings Market: FDI-Driven Growth and Residential Expansion

Vietnam is emerging as a dynamic market for interior architectural coatings, supported by strong foreign direct investment and rapid residential development. The construction of new apartment complexes and urban infrastructure is creating sustained demand for mid-range and premium interior coatings. These developments are driving the adoption of advanced paint systems that offer durability, aesthetic appeal, and environmental compliance.

Technological integration is enhancing market efficiency, with digital platforms enabling direct procurement of customized coatings from manufacturers. Regulatory measures are also encouraging modernization, particularly through stricter emission standards for coating applications. Product innovation tailored to local climatic conditions, such as humidity-resistant coatings, is addressing challenges related to mold and peeling. Additionally, the expansion of luxury resort projects is increasing demand for high-performance coatings in the hospitality sector. These factors collectively position Vietnam as a rapidly growing market within the global interior architectural coatings industry.

Interior Architectural Coatings Market Report Scope

|

Parameter

|

Details

|

|

Market Size (2025)

|

$56.7 Billion

|

|

Market Size (2032)

|

$75.6 Billion

|

|

Market Growth Rate

|

4.2%

|

|

Segments

|

By Technology (Water-borne Coatings, Solvent-borne Coatings, Radiation-Cured, Powder Coatings), By Resin Type (Acrylic, Alkyd, Vinyl Acetate Ethylene, Polyurethane, Epoxy, Bio-based), By Product Type (Interior Wall Paints, Primers and Undercoats, Sealers and Fillers, Stains and Varnishes, Ceiling Paints, Floor Coatings), By End-Use Sector (Residential, Non-Residential, Institutional), By Application Method (Roller and Brush, Spray Applied, Automated), By Performance (Low, Anti-Microbial, Scrub and Stain Resistant, Smart, Decorative), By Gloss (Flat, Eggshell and Satin, Semi-Gloss, High-Gloss), By Sales Channel (Specialty Paint Stores, Home Improvement, E-commerce, B2B)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Sherwin-Williams Company, PPG Industries, Inc., AkzoNobel N.V., Nippon Paint Holdings Co., Ltd., Asian Paints Limited, Kansai Paint Co., Ltd., Benjamin Moore & Co., Masco Corporation, Jotun A/S, RPM International Inc., Berger Paints India Limited, Axalta Coating Systems Ltd., Hempel A/S, Tikkurila Oyj, Dunn-Edwards Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Interior Architectural Coatings Market Segmentation

By Technology

- Water-borne Coatings

- Solvent-borne Coatings

- Radiation-Cured

- Powder Coatings

By Resin Type

- Acrylic

- Alkyd

- Vinyl Acetate Ethylene

- Polyurethane

- Epoxy

- Bio-based

By Product Type

- Interior Wall Paints

- Primers and Undercoats

- Sealers and Fillers

- Stains and Varnishes

- Ceiling Paints

- Floor Coatings

By End-Use Sector

- Residential

- Non-Residential

- Institutional

By Application Method

- Roller and Brush

- Spray Applied

- Automated

By Performance

- Low

- Anti-Microbial

- Scrub and Stain Resistant

- Smart

- Decorative

By Gloss

- Flat

- Eggshell and Satin

- Semi-Gloss

- High-Gloss

By Sales Channel

- Specialty Paint Stores

- Home Improvement

- E-commerce

- B2B

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Interior Architectural Coatings Market

- The Sherwin-Williams Company

- PPG Industries, Inc.

- AkzoNobel N.V.

- Nippon Paint Holdings Co., Ltd.

- Asian Paints Limited

- Kansai Paint Co., Ltd.

- Benjamin Moore & Co.

- Masco Corporation

- Jotun A/S

- RPM International Inc.

- Berger Paints India Limited

- Axalta Coating Systems Ltd.

- Hempel A/S

- Tikkurila Oyj

- Dunn-Edwards Corporation

*- List not Exhaustive