Intumescent Coatings Market Size, Passive Fire Protection Demand, and Infrastructure Safety Outlook

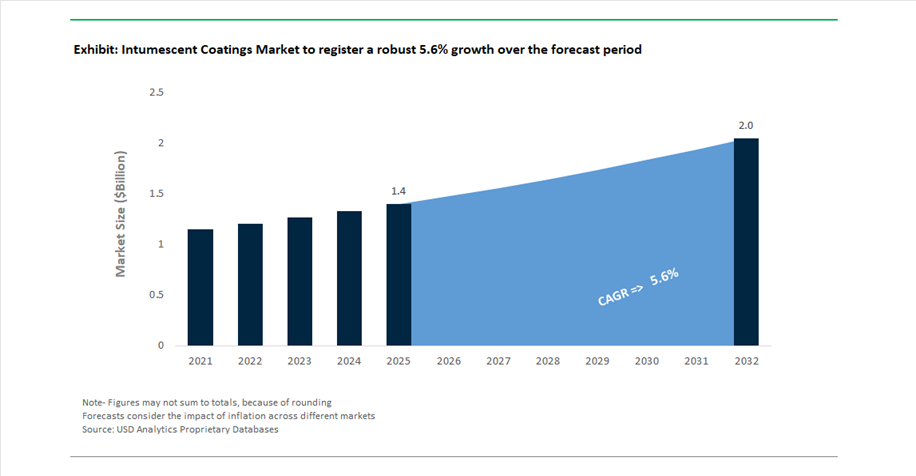

The global intumescent coatings market was valued at $1.4 billion in 2025 and is projected to reach $2.1 billion by 2032, growing at a CAGR of 5.6%. This growth is being driven by rising demand for passive fire protection (PFP) coatings, fire-resistant coatings, epoxy intumescent coatings, and water-based intumescent systems across commercial construction, oil & gas, infrastructure, marine, and industrial facilities. As fire safety regulations become increasingly stringent worldwide, intumescent coatings are emerging as a critical solution for protecting structural steel and load-bearing assets from fire-induced failure.

A major growth driver is the increasing adoption of hydrocarbon and cellulosic fire protection systems, particularly in high-rise buildings, tunnels, offshore platforms, and energy infrastructure. Intumescent coatings expand when exposed to high temperatures, forming an insulating char layer that delays structural collapse, making them essential for compliance with fire safety standards and building codes. Additionally, the rise of modular construction and prefabricated steel structures is accelerating demand for coatings that can be applied efficiently in off-site controlled environments, improving quality and reducing project timelines.

Sustainability and performance optimization are also influencing market evolution. The shift toward low-VOC, water-based intumescent coatings with faster drying times is addressing environmental concerns while improving application efficiency. Emerging applications in electric vehicle battery systems, data centers, and semiconductor facilities are further expanding the scope of intumescent coatings beyond traditional construction and energy sectors.

Digital PFP Services, and Advanced Fire Protection Technologies Transforming Market Dynamics

The intumescent coatings industry is undergoing rapid transformation driven by consolidation, digitalization, and high-performance product innovation. A pivotal development occurred in February 2026, when AkzoNobel and Axalta announced a mega-merger, uniting AkzoNobel’s Chartek (hydrocarbon) and Interchar (cellulosic) product lines with Axalta’s industrial infrastructure coatings portfolio. This consolidation creates a dominant global force in the passive fire protection (PFP) market, enhancing capabilities across energy, infrastructure, and industrial segments.

Strategic realignment toward high-growth regions and applications is evident among leading players. Hempel A/S, following record profits of €168 million in 2025, officially launched its “Accelerate to Win” strategy in January 2026, prioritizing intumescent coatings for marine newbuilds and infrastructure projects in Asia and the Middle East. This is supported by its March 2025 expansion initiative, backed by CVC Funds, to scale its Hempafire product range in North America, intensifying competition with established players such as Sherwin-Williams and PPG Industries.

Digitalization is emerging as a critical differentiator in PFP services. In December 2025, PPG Industries introduced the PFP Digital Support Suite, enabling real-time dry film thickness (DFT) calculations and compliance tracking for complex steel structures. This innovation reflects a broader industry shift toward data-driven fire protection engineering, improving accuracy and reducing over-application costs. Similarly, Sherwin-Williams advanced its FIRETEX M90/02 system in June 2025, optimizing it for off-site application, which aligns with the growing adoption of modular construction techniques.

Product innovation continues to push performance boundaries in extreme environments. Jotun’s Jotachar 1709XT, launched in November 2025, is engineered for hydrocarbon fire and explosion scenarios, offering improved workability in high-temperature desert conditions, making it highly suitable for Middle Eastern energy projects. Meanwhile, AkzoNobel’s July 2025 launch of a water-based intumescent coating with 30% faster drying time addresses a critical bottleneck in commercial high-rise construction, where project timelines are tightly constrained.

The market is also witnessing increased scrutiny and regulatory focus. The September 2025 legal dispute involving Sherwin-Williams and Carboline over performance claims has triggered a broader verification audit of fire-resistance certifications, emphasizing the importance of validated performance data and compliance transparency in procurement decisions.

Emerging applications are further diversifying market opportunities. Jotun reported strong growth in intumescent powder coatings for EV battery enclosures in China, leveraging fire-resistant properties to mitigate thermal runaway risks, with new investments in Malaysia to scale production. Additionally, PPG’s STEELGUARD 951, introduced in September 2024, provides up to three hours of fire protection for critical infrastructure such as data centers and semiconductor facilities, combining aesthetic finish with fire safety performance.

Clear Intumescent Coatings Enabling Exposed Cross-Laminated Timber in High-Rise Construction

The rapid adoption of cross-laminated timber in mid- and high-rise buildings is reshaping the intumescent coatings market, particularly through demand for transparent fire-protection systems that preserve architectural aesthetics. Unlike traditional fireproofing methods such as gypsum encapsulation, clear intumescent coatings allow exposed timber surfaces while delivering required fire resistance ratings. These coatings are engineered to significantly reduce the natural charring rate of timber, lowering it by up to 36% under controlled heat flux conditions, thereby preserving structural load-bearing capacity during early fire stages. Performance optimization is achieved through precise dry film thickness control, typically ranging between 0.18 mm and 0.40 mm, balancing visual clarity with expansion efficiency during fire exposure. This is particularly critical in premium architectural projects where design intent prioritizes visible wood grain. Adoption is accelerating, with over half of mass timber buildings exceeding 10 stories now specifying clear intumescent systems to meet stringent fire standards such as ASTM E119 and EN 13381-7. However, for higher heat flux environments, opaque intumescent coatings still dominate due to their superior thermal shielding capability. The convergence of sustainability-driven construction and fire safety requirements is positioning clear intumescent coatings as a key enabling technology in modern timber architecture.

Hydrocarbon Jet Fire-Rated Intumescent Coatings Becoming Standard for Offshore Platforms

Offshore oil and gas infrastructure is increasingly transitioning to jet fire-rated intumescent coatings to address the severe risks associated with high-pressure hydrocarbon releases. Unlike conventional pool fires, jet fires involve rapid temperature escalation up to approximately 1,100°C combined with high-velocity erosive forces, necessitating advanced coating systems capable of maintaining structural protection under extreme conditions. Modern epoxy intumescent coatings are engineered to withstand heat flux levels up to 350 kW/m² while maintaining adhesion strength exceeding 5 MPa, ensuring that the protective char layer remains intact even under intense mechanical scouring. A critical performance requirement is maintaining structural steel temperatures below 400°C, significantly lower than traditional thresholds, to preserve load-bearing capacity in offshore environments. Additionally, advancements in formulation technology now allow for high-build applications of 8 to 10 mm in a single pass, improving application efficiency and durability. These coatings also provide resistance to environmental stressors such as salt spray, vibration, and impact, making them suitable for harsh marine conditions. These factors are driving widespread adoption of jet fire-rated intumescent coatings as a standard safety solution in offshore energy infrastructure.

US FRA Fire Safety Regulations Driving Retrofit Demand for Intumescent Coatings in Rail Systems

The strengthening of fire safety regulations in the rail sector is creating a significant opportunity for intumescent coatings, particularly in passenger rail and transit systems. Updated compliance requirements mandate enhanced fire resistance and smoke emission control for structural components in rolling stock. To meet these standards, rail operators are increasingly adopting intumescent coatings as a cost-effective retrofit solution for existing fleets, avoiding the need for full structural replacement. Modern formulations are designed to achieve low-smoke, zero-halogen performance, maintaining optical smoke density below critical thresholds during fire exposure. These coatings also offer weight advantages, delivering approximately 40% reduction compared to traditional insulation materials, which is particularly important for high-speed rail applications where energy efficiency is a priority. Additionally, intumescent systems provide structural fire protection durations ranging from 30 to 60 minutes, ensuring passenger safety during evacuation scenarios. As compliance deadlines approach, retrofit demand is expected to accelerate, positioning intumescent coatings as a key solution in rail safety modernization efforts.

China MOHURD Mandate Driving Demand for Fireproof Coatings in Steel Residential High-Rises

China’s regulatory push toward steel-framed construction in urban residential developments is creating a substantial growth opportunity for intumescent coatings. New standards mandate fire resistance ratings of up to three hours for primary structural components in buildings exceeding 54 meters in height, significantly increasing the requirement for high-performance fireproof coatings. This is particularly relevant as steel construction gains momentum in densely populated urban areas, where prefabrication and rapid construction techniques are being prioritized. The integration of digital monitoring systems during construction is further enhancing compliance requirements, with coating thickness tracked in real time to ensure adherence to specified tolerances. This level of precision is driving demand for advanced ultra-thin film intumescent coatings that maximize usable interior space while meeting fire safety standards. Additionally, localization requirements are favoring manufacturers capable of meeting domestic certification standards, creating opportunities for both local and international suppliers. These regulatory and construction trends are positioning China as a major growth market for intumescent coatings in high-rise residential applications.

Intumescent Coatings Market Share 2025: Cellulosic Fire Protection and Certified Applicators Lead Growth

Application Insights: Cellulosic Fire Protection Dominates Building Fire Safety Standards

The cellulosic fire protection segment leads the intumescent coatings market with a 52% market share in 2025, driven by its widespread use in commercial and institutional construction projects. Designed to follow the standard temperature-time curve (ASTM E119/UL 263), these coatings are essential for structures where wood, paper, and textile-based materials act as primary fire loads, including offices, schools, hospitals, and stadiums. A major growth driver is the increasing adoption of thin-film intumescent coatings, typically applied at 0.5–3mm dry film thickness, which provide both fire resistance and enhanced aesthetics for exposed structural steel. Compared to traditional cementitious fireproofing and board systems, thin-film coatings offer faster application, reduced weight, and superior design flexibility, making them highly attractive for modern architectural projects. As building codes tighten globally, cellulosic fire protection will continue to dominate the intumescent coatings market.

Sales Channel Insights: Certified Applicator Networks Drive Compliance and Performance Assurance

The certified applicator networks segment holds the largest 55% share in the intumescent coatings market in 2025, reflecting the critical importance of application quality, regulatory compliance, and performance guarantees. Leading manufacturers such as PPG, AkzoNobel, Sherwin-Williams, and Jotun only provide warranties when coatings are applied by trained and certified professionals, ensuring precise control over dry film thickness (DFT), environmental conditions, and surface preparation standards. These applicators also deliver comprehensive documentation and traceability, including records of temperature, humidity, and coating thickness measurements, which are mandatory for building code approvals and insurance certifications. This level of accountability is crucial in fire protection systems where failure is not an option. As safety regulations and liability requirements become more stringent, certified applicator networks will remain the dominant sales channel in the global intumescent coatings market.

Intumescent Coatings Market Competitive Landscape Shaped by PFP Regulations and Hydrocarbon Fire Innovation

The global intumescent coatings market is intensely competitive, driven by stringent passive fire protection regulations, hydrocarbon fire resistance requirements, and the transition to low-VOC, water-based formulations. Leading players are scaling advanced fire-retardant chemistries, expanding manufacturing capacity, and targeting modular construction and offshore infrastructure protection.

AkzoNobel strengthens fire protection leadership through Smart-Expansion intumescent technologies

AkzoNobel N.V. is reinforcing its leadership in the global intumescent coatings market through its International® brand and a strategic focus on value-driven sustainability. The announced 2026 all-stock merger with Axalta is set to create a coatings powerhouse with expanded R&D capabilities in advanced fire-retardant polymers. The company reported an 80 basis-point improvement in Q1 2026 profitability, reflecting operational efficiency within its Performance Coatings segment. Its Interchar® and Chartek® product lines now incorporate Smart-Expansion technology, optimizing char-layer thickness for up to 120-minute fire resistance in structural steel applications. With operations spanning more than 150 countries, AkzoNobel leverages its “Paint the Future” ecosystem to deliver high-performance intumescent coatings across industrial and architectural sectors. This combination of innovation, scale, and sustainability positions it as a benchmark in passive fire protection coatings.

PPG accelerates intumescent coatings growth with advanced manufacturing and safety compliance focus

PPG Industries, Inc. is expanding its footprint in the intumescent coatings industry through a $300 million investment in advanced manufacturing infrastructure through 2026. The development of a highly automated Tennessee facility supports increasing demand for commercial steel fire protection coatings. PPG’s flagship PPG PITT-CHAR® NX and PPG STEELGUARD® lines have been enhanced for superior durability against chemical exposure, targeting petrochemical and aerospace applications. Its 2025 initiative promoting accurate fire testing and adherence to UL-listed standards underscores its leadership in safety compliance and regulatory alignment. Sustainability remains a key pillar, with 41% of 2024 sales from sustainably advantaged products and a growing shift toward waterborne intumescent formulations. This integrated approach strengthens PPG’s position in high-performance passive fire protection systems.

Sherwin-Williams advances modular-ready intumescent coatings with high-build fire protection systems

Sherwin-Williams Company continues to dominate the intumescent coatings market through its vertically integrated model and rapid product commercialization strategy. The 2025 global expansion of its Core Product Offering standardizes high-performance fire protection coatings across international markets, enhancing supply consistency. Its FIRETEX® FX7002 success has accelerated the development of high-build intumescent coatings that reduce application layers while achieving 90-minute fire ratings. Operating in over 120 countries, Sherwin-Williams leverages its Valspar acquisition to maintain strong penetration in contractor and OEM channels. The company is also pioneering factory-applied intumescent coatings tailored for off-site modular construction, improving curing speed and transport durability. This innovation aligns with evolving construction trends and strengthens its competitive edge in structural fire protection coatings.

Jotun targets hydrocarbon fire protection with localized R&D and extreme-condition coatings

Jotun Group is a key player in the intumescent coatings market, specializing in extreme-environment protection for offshore and industrial assets. The company achieved record operating revenue of NOK 11,376 million in early 2025, reflecting strong demand in its Performance Coatings segment. Its expansion strategy includes new manufacturing facilities in Algeria and enhanced distribution networks across Africa and Southeast Asia. The launch of Jotachar 1709 XT addresses hydrocarbon fire scenarios, including jet fires and thermal shock, reinforcing its leadership in oil and gas fire protection coatings. Jotun’s global R&D network supports product localization, ensuring optimal coating performance under varying climatic conditions. This focus on extreme durability and regional adaptability positions Jotun as a critical supplier in high-risk industrial fire protection.

Hempel drives sustainable intumescent coatings growth with record financial performance and climate targets

Hempel A/S is strengthening its presence in the intumescent coatings industry through strong financial growth and aggressive sustainability targets. The company reported €2.165 billion in revenue in 2025, alongside record free cash flow and an EBITDA margin of 18.2%. Its Hempafire Extreme product line is engineered for infrastructure fire protection across Europe and Asia-Pacific, targeting high-growth construction markets. Hempel has achieved a 70% reduction in Scope 1 and 2 emissions since 2019, with a goal of reaching 90% by 2026, aligning with global decarbonization initiatives. Strategic leadership transition plans announced in 2026 aim to drive the next phase of its “Double Impact” growth strategy. This combination of financial strength, product innovation, and sustainability focus reinforces Hempel’s competitive positioning in passive fire protection coatings.

RPM scales industrial fireproofing solutions through Asia-Pacific expansion and smart coating R&D

RPM International Inc. is leveraging its Performance Coatings Group, including Carboline and Tremco, to expand its leadership in industrial intumescent coatings. The acquisition of a Malaysia-based manufacturing facility in 2026 strengthens its ability to serve high-growth Asia-Pacific markets. RPM reported $583.2 million in operating cash flow in H1 2026, providing financial flexibility for continued M&A and innovation investments. Its $100 million MAP 2025 cost optimization program is reallocating resources toward advanced “smart coating” R&D initiatives. The Performance Coatings Group generated $533.8 million in Q2 2026 sales, reflecting steady demand for fireproofing solutions in oil and gas infrastructure. This strategic focus on scalability, innovation, and regional expansion positions RPM as a strong competitor in the global intumescent coatings market.

United States Intumescent Coatings Market: Shale Expansion and Battery Safety Driving Fire Protection Demand

The United States intumescent coatings market is experiencing significant expansion, driven by robust investments in shale gas exploration and the rapid growth of energy storage systems. The modernization of Gulf Coast refineries and upstream oil & gas infrastructure is fueling demand for thick-film epoxy intumescent coatings capable of withstanding high-intensity jet fires. These coatings are critical for ensuring structural integrity in high-risk hydrocarbon environments, positioning the U.S. as a leader in advanced passive fire protection solutions.

Technological innovation is reshaping the market, with the introduction of “smart” intumescent coatings embedded with fiber-optic sensors that enable real-time monitoring of steel structures under thermal stress. The shift toward PFAS-free formulations, driven by stringent environmental regulations, is accelerating the adoption of sustainable fire protection coatings. Additionally, the rapid expansion of the “Battery Belt” is driving large-scale deployment of fire-retardant coatings in lithium-ion battery enclosures to prevent thermal propagation. Investments in modular fabrication hubs are further enhancing efficiency by enabling factory-applied coatings with superior uniformity, reinforcing the U.S. market’s leadership in high-performance intumescent coating technologies.

China Intumescent Coatings Market: National Safety Codes and Mega-Urbanization Driving Volume Growth

China remains the global leader in the intumescent coatings market, supported by strict fire safety regulations and rapid urbanization. The implementation of updated national standards for fire-resistant materials is significantly raising compliance requirements, driving the adoption of advanced intumescent coatings across construction and industrial sectors. Government initiatives focused on safety in high-density urban clusters and chemical industrial parks are further boosting demand for high-performance fire protection coatings.

Technological advancements are enhancing product performance, with innovations such as graphene-enhanced char-forming coatings providing improved thermal insulation and durability in extreme conditions. The expansion of smart city projects is creating strong demand for waterborne intumescent coatings in high-rise buildings, ensuring fire safety while maintaining environmental compliance. Strategic investments by global and domestic manufacturers in water-based coating production are also strengthening supply chains. Additionally, the adoption of advanced intumescent coatings in marine applications, particularly in large crude carriers, highlights China’s growing influence in global fire protection coating technologies.

Germany Intumescent Coatings Market: Hydrogen Infrastructure and Sustainable Fire Protection Innovation

Germany serves as the European hub for sustainable intumescent coatings, driven by stringent regulatory frameworks and strong investments in hydrogen infrastructure. The country is leading the development of advanced fire protection coatings that are compatible with hydrogen environments, ensuring durability and safety under high-pressure conditions. These coatings are essential for supporting Europe’s energy transition and the expansion of hydrogen networks.

Sustainability remains a key focus, with innovations such as bio-based and de-coatable intumescent coatings enabling circular economy practices and reducing environmental impact. Technological advancements, including UV-LED curing systems, are improving energy efficiency in coating applications. Regulatory requirements mandating migration-tested coatings for industrial use are further shaping market dynamics. Additionally, the integration of radiative cooling technologies into intumescent coatings is enhancing energy efficiency in industrial facilities. These developments position Germany as a leader in environmentally responsible and technologically advanced fire protection coatings.

India Intumescent Coatings Market: Smart Cities Expansion and Industrial Growth Accelerating Adoption

India is emerging as one of the fastest-growing markets for intumescent coatings, driven by large-scale infrastructure development and government-led initiatives. Programs such as the National Infrastructure Pipeline and Smart Cities Mission are significantly increasing demand for fire-retardant coatings in commercial buildings, transportation hubs, and industrial facilities. These coatings are essential for enhancing fire safety in high-occupancy structures and critical infrastructure.

The market is also benefiting from regulatory reforms, including mandatory quality standards that ensure product reliability and eliminate sub-standard imports. Strategic expansions by global coating companies are improving local production capabilities and reducing supply chain lead times. The rapid growth of the manufacturing sector is further driving demand for epoxy-based passive fire protection coatings in automotive and heavy machinery applications. Additionally, the adoption of thin-film intumescent coatings in metro rail projects and green-certified buildings highlights the increasing focus on sustainability and safety in India’s construction sector.

Saudi Arabia Intumescent Coatings Market: Vision 2030 Megaprojects and Hydrocarbon Infrastructure

Saudi Arabia is a key market for intumescent coatings in the Middle East, driven by extensive investments in oil & gas infrastructure and large-scale development projects under Vision 2030. The expansion of gas processing facilities and petrochemical complexes is significantly increasing demand for high-performance fire protection coatings capable of withstanding extreme thermal conditions.

Regulatory frameworks mandating certified fire protection systems are shaping market growth, ensuring compliance with international safety standards. Technological advancements, including robotic coating application systems, are improving efficiency and consistency in large-scale projects. The adoption of low-VOC and eco-friendly coatings is also gaining momentum, supported by sustainability initiatives aimed at reducing environmental impact. Additionally, the use of intumescent coatings in desalination plants and infrastructure projects highlights their critical role in protecting assets from both fire and corrosion, reinforcing Saudi Arabia’s position as a major market for industrial fire protection coatings.

United Kingdom Intumescent Coatings Market: Regulatory Compliance and Building Safety Transformation

The United Kingdom intumescent coatings market is undergoing a significant transformation, driven by stringent building safety regulations and increased emphasis on fire protection in high-risk environments. The implementation of comprehensive safety laws has introduced mandatory certification requirements for fire protection coatings, raising industry standards and ensuring greater accountability in construction and infrastructure projects.

Technological innovation is supporting compliance with these regulations, with the development of solvent-free and waterborne intumescent coatings that meet strict VOC limits while maintaining high fire resistance performance. Market consolidation is streamlining service delivery, enabling integrated solutions that cover specification, application, and certification. Additionally, advancements such as intumescent fabric wraps are expanding application areas, particularly in protecting critical infrastructure such as data cables in high-heat environments. The growing demand for advanced fire protection solutions in offshore and industrial sectors further reinforces the UK’s role as a key market for intumescent coatings.

Intumescent Coatings Market Report Scope

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.4 Billion

|

|

Market Size (2032)

|

$2.1 Billion

|

|

Market Growth Rate

|

5.6%

|

|

Segments

|

By Technology (Water-borne Coatings, Solvent-borne Coatings, Epoxy-based Coatings, Hybrid Formulations), By Product (Thin-film Intumescent Coatings, Thick-film Intumescent Coatings), By Application (Cellulosic Fire Protection, Hydrocarbon Fire Protection, Jet Fire Protection), By Substrate (Structural Steel and Cast Iron, Timber, Concrete, Composites and Plastics, Cables and Electrical Raceways), By Resin Type (Acrylic, Epoxy, Vinyl Ester, Alkyd, Specialty Resins), By End-Use Industry (Building and Construction, Oil and Gas, Industrial Facilities, Automotive and Transportation, Aerospace and Defense), By Fire Rating Duration (Up to 60 Minutes, 90 Minutes, 120 Minutes, Beyond 120 Minutes), By Sales Channel (Direct Sales, Specialty Industrial Distributors, Certified Applicator Networks)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Sherwin-Williams Company, AkzoNobel N.V., PPG Industries, Inc., Jotun A/S, Hempel A/S, Sika AG, RPM International Inc., 3M Company, Kansai Paint Co., Ltd., Nippon Paint Holdings Co., Ltd., Teknos Group, Promat International, Isolatek International, Nullifire, Rudolf Hensel GmbH,

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Intumescent Coatings Market Segmentation

By Technology

- Water-borne Coatings

- Solvent-borne Coatings

- Epoxy-based Coatings

- Hybrid Formulations

By Product

- Thin-film Intumescent Coatings

- Thick-film Intumescent Coatings

By Application

- Cellulosic Fire Protection

- Hydrocarbon Fire Protection

- Jet Fire Protection

By Substrate

- Structural Steel and Cast Iron

- Timber

- Concrete

- Composites and Plastics

- Cables and Electrical Raceways

By Resin Type

- Acrylic

- Epoxy

- Vinyl Ester

- Alkyd

- Specialty Resins

By End-Use Industry

- Building and Construction

- Oil and Gas

- Industrial Facilities

- Automotive and Transportation

- Aerospace and Defense

By Fire Rating Duration

- Up to 60 Minutes

- 90 Minutes

- 120 Minutes

- Beyond 120 Minutes

By Sales Channel

- Direct Sales

- Specialty Industrial Distributors

- Certified Applicator Networks

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Intumescent Coatings Market

- The Sherwin-Williams Company

- AkzoNobel N.V.

- PPG Industries, Inc.

- Jotun A/S

- Hempel A/S

- Sika AG

- RPM International Inc.

- 3M Company

- Kansai Paint Co., Ltd.

- Nippon Paint Holdings Co., Ltd.

- Teknos Group

- Promat International

- Isolatek International

- Nullifire

- Rudolf Hensel GmbH

*- List not Exhaustive