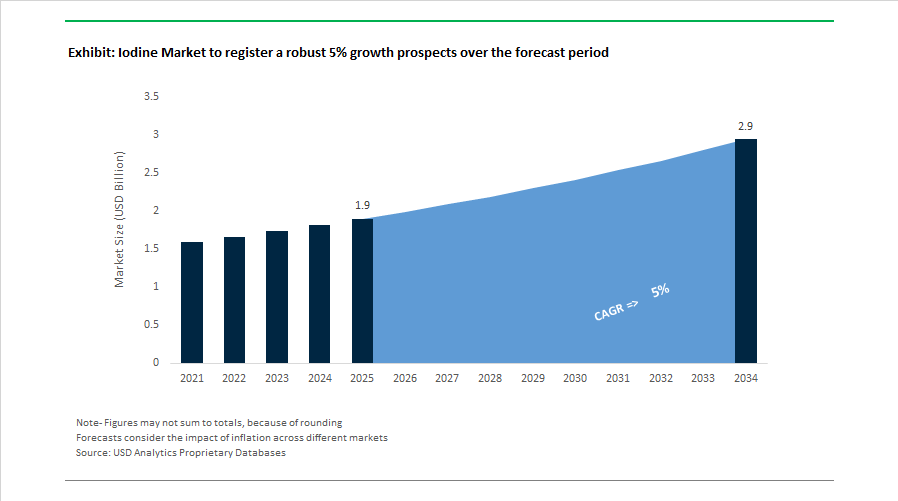

Iodine Market to Reach $2.9 Billion by 2034 at 5% CAGR as Medical Imaging and Brine Extraction Capacity Expand

The Iodine Market is projected to grow from $1.9 billion in 2025 to $2.9 billion by 2034, registering a CAGR of 5%. Market expansion is being driven by rising demand for iodine-based contrast media, increasing brine-extraction capacity in North and South America, and infrastructure investments that secure long-term supply stability. The industry is simultaneously strengthening circular recovery systems and integrating AI-enabled production optimization to reduce marginal costs.

Supply-side modernization gained momentum beginning in 2023. In June 2023, REMONDIS inaugurated a specialized plant to recover iodine from hazardous waste flue gas, reaching full commercial capacity by early 2024 and reinforcing circular economy supply streams. In 2024, GE Healthcare announced a significant expansion of its iodine-based contrast agent production following global shortages, committing multi-million-dollar investments to stabilize hospital supply chains. In December 2024, Abbott Laboratories introduced a targeted iodine supplement line for maternal health, addressing persistent iodine deficiency concerns in prenatal care. During late 2024 and into 2025, Omron Healthcare initiated a $15.7 million investment in Tamil Nadu, India, strengthening regional medical infrastructure and indirectly supporting demand for iodine-based antiseptics and imaging reagents.

Capacity acceleration intensified throughout 2025. In January 2025, Merck KGaA launched a novel iodine-based contrast agent engineered to enhance radiological clarity while minimizing adverse reactions in sensitive patients. In mid-2025, Iofina began construction of its largest iodine extraction plant in the Permian Basin, designed to process approximately 50,000 barrels of brine per day and deliver up to 220 metric tonnes annually. In Q3 2025, Iofina’s IO#11 plant in Oklahoma became fully operational using proprietary IOsorb® brine extraction technology. In Q3 2025, SQM announced that its Atacama Desert seawater pipeline project surpassed 80% completion, a critical step toward unlocking additional caliche-based iodine production by mid-2026. During the same period, SQM implemented executive leadership restructuring to streamline its global iodine strategy as part of its broader $2.7 billion CAPEX program, including the expansion of its María Elena operation expected to add 1,500 tonnes of new capacity.

Operational optimization and record output characterized early 2026. In 2025, IOCHEM Corporation deployed AI-enabled monitoring systems across its brine extraction assets, improving flow control and reducing downtime for high-purity iodine production. In January 2026, Iofina reported record crystalline iodine production of 743.2 metric tonnes for 2025, reflecting a 17% year-on-year increase supported by the successful performance of its IO#10 facility and projecting revenues exceeding $65 million. These coordinated investments in extraction technology, infrastructure, and medical-grade product innovation are reshaping global iodine supply dynamics while reinforcing the sector’s role in diagnostics, nutrition, and advanced industrial applications.

Iodine Market Trends and Opportunities

Strategic Capacity Scaling and Brine-to-Crystalline Extraction Modernization

The global iodine market continues to be structurally concentrated, with Chile and Japan collectively controlling the majority of primary supply through caliche ore mining and iodine-rich brine extraction. The sharp price escalation seen in early 2025, when iodine prices crossed USD 70 per kilogram, has acted as a catalyst for aggressive capacity expansion and extraction efficiency upgrades rather than greenfield discoveries. Producers are prioritizing technologies that can economically convert marginal brine and ore reserves into crystalline iodine at scale, thereby stabilizing long-term supply.

In November 2025, SQM significantly reinforced this strategy by updating its capital expenditure roadmap to USD 2.7 billion for the 2025–2027 period. A central pillar of this investment is the completion of its seawater pipeline and the expansion of the Maria Elena production complex in northern Chile. These assets are critical to SQM’s stated objective of increasing annual iodine capacity by approximately 1,000 to 1,500 metric tonnes, positioning the company to respond rapidly to demand spikes from medical imaging and electronics while preserving cost leadership.

North America is simultaneously emerging as a structurally relevant secondary supply base. In Q3 2025, Iofina plc reported record crystalline iodine output of 215.8 metric tonnes, representing a 32% year-on-year increase. This growth was directly enabled by the commissioning of its IO#11 plant in Oklahoma, which applies proprietary WET® IOsorb® technology to recover iodine from produced water streams in oil and gas operations. This model not only diversifies geographic supply but also embeds iodine recovery into existing energy infrastructure, reducing marginal production costs and improving ESG credentials.

Japan is reinforcing its role as a premium-grade supplier rather than competing on volume. In September 2025, Japanese exporters reported a 0.7% month-on-month price increase, driven by investments in environmentally optimized brine recovery systems. These upgrades are strategically targeted at European pharmaceutical buyers who depend on Japan’s consistently high-purity iodine grades for complex synthesis pathways, making Japan a supply-side anchor despite limited resource expansion.

Multi-Million-Dollar Infrastructure Investments for Iodinated Contrast Media

The accelerating global adoption of CT and advanced X-ray diagnostics is transforming iodinated contrast media from a niche pharmaceutical category into a high-throughput industrial manufacturing segment. Procedure volumes are projected to double over the coming decade, forcing imaging companies to secure iodine supply and scale fill-finish capacity with the same rigor applied to essential injectable drugs.

In January 2025, GE HealthCare announced a USD 138 million investment to expand its Carrigtohill facility in Ireland. Once operational in 2027, the site will add capacity for approximately 25 million additional doses of iodinated contrast media annually, with a clear focus on cardiovascular and oncology diagnostics where iodine-based agents remain indispensable. This expansion signals a structural shift toward long-term iodine offtake contracts and tighter supplier qualification.

Asia-Pacific demand dynamics are reinforcing this trend. In March 2025, South Korea’s Taejoon Pharm expanded its iodinated contrast media production capacity by 15% to address rising demand driven by aging demographics across North Asia. This expansion underscores the growing regionalization of contrast media supply chains and the increasing strategic value of reliable iodine sourcing in Asia.

R&D intensity and sustainability are becoming differentiators within this segment. Guerbet continues to allocate roughly 9% of annual revenue, exceeding EUR 840 million in 2024, toward research and development across its global centers. Recent initiatives have shifted toward eco-design, including a 40% plastic reduction program for iodine-based contrast packaging launched in late 2024. For decision makers, this signals that iodine demand growth is increasingly tied to innovation-led healthcare infrastructure rather than commodity volume alone.

High-Purity Iodine Precursors for Perovskite Solar Cells

Perovskite solar cells are rapidly moving from laboratory-scale breakthroughs to pilot and pre-commercial manufacturing, creating a high-value demand pocket for ultra-high-purity iodine derivatives such as methylammonium iodide and formamidinium iodide. These compounds are central to perovskite absorber layers and require impurity levels below 10 parts per billion to avoid charge recombination losses.

In 2025, perovskite cell efficiencies reached 25.55, outperforming conventional silicon modules that typically operate in the 16 to 22% range. This performance leap is accelerating industrial interest. At SNEC 2025, BOE showcased flexible perovskite applications including dimmable glass roofing systems that rely on iodine-based absorbers for tunable light transmission, highlighting commercial pathways beyond utility-scale solar.

By mid-2025, more than 20 companies in China and several in Europe had announced plans to scale perovskite pilot lines toward gigawatt-per-year capacity. These expansions are directly translating into demand for electronic-grade iodine with tightly controlled metallic and organic impurity profiles. Unlike indium and other scarce thin-film materials, iodine offers relative abundance and cost stability, positioning it as a strategic backbone of next-generation photovoltaic supply chains.

Iodine-Based Biocides as Regulatory-Compliant Oxidizers

Tightening environmental regulations across Europe and the United Kingdom are creating a structural opening for iodine-based biocides as alternatives to chlorine-intensive and PFAS-linked water treatment chemistries. Iodine’s ability to act as an effective oxidizer while degrading into benign iodide ions is increasingly aligned with regulatory and ESG priorities.

The UK Biocidal Products Regulation Amendment of 2024, which fully applies to new applications from October 2025, favors substances with cleaner degradation profiles. This regulatory shift is accelerating the adoption of iodophors in cooling towers, food processing water systems, and agricultural applications where the formation of carcinogenic trihalomethanes from chlorine is under scrutiny.

Maritime regulations are amplifying this opportunity. Global ballast water treatment mandates are driving interest in iodine-releasing resin systems that provide effective pathogen neutralization in high-volume seawater environments. These systems avoid the corrosive impacts of high-dose chlorine, reducing onboard maintenance costs by an estimated 12 to 15% while meeting international discharge standards. For ship operators and port authorities, iodine-based solutions offer a compelling balance between compliance, lifecycle cost reduction, and environmental stewardship.

Iodine Market Share and Segmentation Insights

Underground Brines Dominate Iodine Production Through Scalable Extraction and Stable Supply Chains

Underground brines represented 58.60% of the Iodine Market share in 2025, making them the largest and most reliable source of iodine production globally. Major iodine extraction operations are concentrated in Japan, the United States, and Chile, where iodine-rich subterranean brine reservoirs allow producers to extract iodine through controlled pumping, oxidation, and adsorption recovery processes. Compared with solid ore sources, brine extraction offers lower production costs, consistent iodine purity, and scalable output, enabling producers to meet the growing global demand for iodine used in pharmaceuticals, nutrition products, and imaging agents. Brine operations also benefit from co-production of natural gas, bromine, and other minerals, improving overall project economics and resource utilization. In 2025, brine-based iodine production continues to dominate global supply, while Chilean caliche ore operations remain the second-largest source, supported by process optimization technologies. Producers in Chile increasingly deploy advanced adsorption and solvent extraction systems that enhance iodide recovery from caliche leach solutions, helping maintain stable iodine output despite declining ore grades.

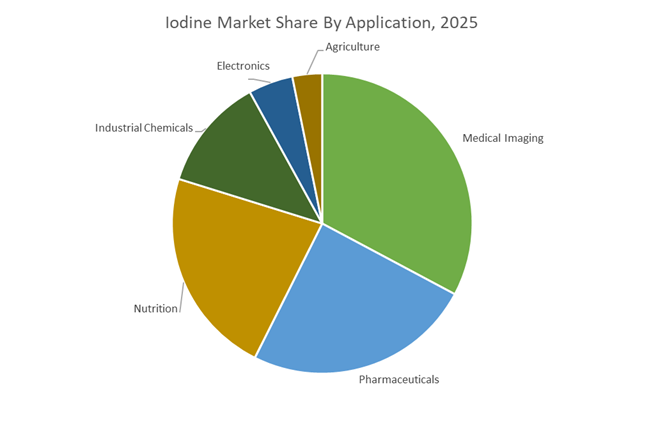

Medical Imaging Sector Drives the Largest Consumption of Iodine

Medical imaging accounted for 32.80% of the Iodine Market share in 2025, positioning it as the largest end-use application for iodine compounds. Iodine plays a critical role in iodinated contrast media used in X-ray imaging and computed tomography (CT) scans, where its high atomic number provides strong radiopacity that enhances visualization of internal organs, blood vessels, and tissues. Contrast-enhanced imaging procedures are widely used in cardiology diagnostics, oncology screening, neurological imaging, and vascular disease evaluation, driving sustained demand for pharmaceutical-grade iodine. The increasing prevalence of chronic diseases, aging populations, and expanding access to advanced diagnostic imaging technologies continues to support growth in contrast media consumption worldwide. In 2025, pharmaceutical manufacturers are advancing next-generation iodinated contrast agents, including iso-osmolar and dimeric formulations designed to improve patient safety, particularly for individuals with renal impairment or cardiovascular conditions. Research into targeted diagnostic imaging agents that use iodine-based compounds for specific disease detection is also expanding, creating high-value product segments within the global iodine market.

Competitive Landscape in Iodine Market

Sociedad Química y Minera de Chile Consolidates Leadership with Green Iodine Strategy

Sociedad Química y Minera de Chile remains the global leader in iodine production, controlling approximately 30 to 35% of global supply through extensive caliche reserves in the Atacama Desert. On March 1, 2026, the company reported a strong financial turnaround, generating $588.1 million in net income for 2025, with its Iodine and Plant Nutrition division contributing 42% of total gross profit. SQM has secured multi-year feedstock agreements with major pharmaceutical intermediaries, including GE HealthCare, ensuring premium pricing stability for medical-grade iodine used in diagnostic imaging. Production capacity targets exceed 16,000 metric tons per year as of early 2026, supported by renewable energy integration into extraction and refining processes. AI-enabled water monitoring systems are being deployed to reduce consumption in the arid Atacama region while lowering carbon intensity, reinforcing SQM’s positioning in sustainable iodine supply.

Iofina PLC Expands Circular Brine-Based Iodine Recovery

Iofina PLC differentiates itself through secondary extraction of iodine from oil and gas brine streams in the United States. In January 2026, the company confirmed full operational status of its eighth and ninth IOsorb plants in Oklahoma’s Anadarko Basin, with a tenth facility scheduled for commissioning by late 2026. Iofina reported a 31% increase in iodine derivative sales in May 2025, reaching $16.9 million, driven by demand for specialty iodides and halogen-based biocides. Its proprietary WET IOsorb technology isolates iodine from waste brine, positioning the company as a leader in environmentally efficient and circular production models. Participation in SOCMA Show 2026 highlights its expanding portfolio for pharmaceutical and fine chemical markets, reinforcing its standing as a key North American supplier of iodine derivatives.

ISE Chemicals Strengthens Medical-Grade Iodine Supply Chain

ISE Chemicals Corporation, a subsidiary of AGC Inc., is Japan’s premier iodine producer, extracting iodine from domestic natural gas brines and maintaining diversified operations through its US subsidiary, Woodward Iodine. The company’s 2026 strategic focus centers on medical-grade dominance, targeting high-purity iodine for contrast media production serving European and North American radiology markets. In addition to elemental iodine, ISE manufactures povidone-iodine and related antiseptic derivatives widely used in surgical and wound-care applications. Investments in advanced ion-exchange resin systems are improving recovery efficiency from low-concentration brine sources, strengthening supply security. Geographic diversification across APAC and North America enhances resilience against regional disruptions in iodine feedstock availability.

Iochem Corporation Advances High-Purity and Closed-Loop Recovery

Iochem Corporation, based in Vici, Oklahoma, is the largest producer of medical-grade iodine in North America, manufacturing approximately 1,200 metric tons annually with purity levels exceeding 99.8%. The company is expanding brine extraction infrastructure in northwestern Oklahoma, utilizing more than 16 deep production wells to secure consistent feedstock supply. AI-enabled monitoring systems implemented during 2025 improved operational uptime and cost efficiency, contributing to enhanced profitability. Iochem’s strategic alignment with closed-loop iodine recycling services allows recovery of iodine from spent contrast agents and industrial catalysts, reducing waste and supporting sustainability objectives. This integrated model positions the company strongly in high-margin pharmaceutical and specialty chemical applications.

Algorta Norte Enhances Cost Efficiency in Chilean Caliche Production

Algorta Norte operates as a competitive Chilean iodine producer, focusing on cost-efficient extraction from caliche ore to challenge larger incumbents. In 2026, the company is investing in infrastructure upgrades and modernization of blow-out extraction techniques to stabilize supply and mitigate price volatility in the Chilean iodine sector. Production expansion plans are aimed at lowering supply costs while maintaining consistent quality for industrial-grade iodine used in biocides, animal nutrition additives, and nylon catalysts. Algorta Norte is transitioning its Atacama operations toward renewable energy integration and advanced purification technologies to meet tightening environmental regulations and rising demand for lower-carbon chemical intermediates. This cost-optimization strategy supports its position as a stable bulk supplier within the global iodine value chain.

Chile Iodine Market: Water Security, Capacity Scaling, and Energy-Efficient Extraction

Chile remains the structural anchor of the global iodine supply chain, with 2025–2026 developments centered on water security, capacity expansion, and energy management. Sociedad Química y Minera de Chile is finalizing a $450 million seawater pipeline to the Nueva Victoria operation, scheduled for completion by mid-2026. The pipeline will deliver a stable 900 liters per second, materially reducing dependence on continental groundwater and stabilizing output across climatic cycles. Capacity growth is advancing on two fronts. Late-2025 confirmations include brownfield projects adding 1,500 metric tons of iodine and greenfield developments expected to contribute a further 2,500 metric tons using advanced solar evaporation, reinforcing Chile’s long-cycle production resilience.

Operational efficiency and sustainability credentials are becoming competitive differentiators. In January 2025, Nueva Victoria became the world’s first iodine production site to achieve ISO 50001:2018 certification, signaling a shift toward energy-optimized Green Iodine. Regional integration is deepening as Atacama producers, including Albemarle, deploy thermo-evaporators such as the La Negra III expansion to recycle mother liquor, cutting freshwater consumption by roughly 30% per metric ton of technical-grade output. Regulatory clarity is also improving market access. In August 2025, the Chilean Ministry of Health initiated revisions to Decree 977/96 to strengthen traceability and GMP for iodine-based stabilizers in food-contact materials, setting clearer compliance pathways for the 2026 market.

United States Iodine Market: Brine-Based Scale-Up and Medical Demand Pull

The United States iodine market is expanding through brine extraction scale-up and sustained healthcare demand. In December 2025, Iofina PLC partnered with Western Midstream Partners to construct a new IOsorb plant in the Permian Basin. Designed to process 50,000 barrels of brine per day, this will be Iofina’s largest facility and is targeted for commissioning in the third quarter of 2026. Earlier momentum was established in July 2025 with the successful start-up of the IO11 plant in Oklahoma, adding approximately 100 metric tons of crystalline iodine annually via proprietary air-stripping technology.

End-market dynamics continue to favor high-purity output. Realized prices for crystalline iodine peaked in the first half of 2025, reflecting robust demand for USP-grade material used in X-ray contrast media and pharmaceutical synthesis. This demand is reinforced by multi-year offtake alignment. GE Healthcare maintains an active partnership through 2025–2026 to support incremental patient doses annually, supplied by a specialized production line in Cork that relies on Chilean raw materials, underscoring transatlantic supply integration anchored by U.S. downstream consumption.

Japan Iodine Market: Supply Resilience and Renewable Materials R&D

Japan’s iodine industry is prioritizing supply resilience and forward-looking materials research. Following early-summer typhoon disruptions in 2025, refiners in Chiba Prefecture invested in weather-proof refining clusters to safeguard production of 99.7% purity iodine crystals, improving continuity in a region exposed to climate volatility. These investments are protecting export reliability at a time of persistent global supply tightness.

R&D is extending iodine’s relevance beyond traditional uses. INPEX Corporation and other Kanto-region producers are advancing research into iodine-based salts for perovskite solar cells, positioning iodine as a critical input for the renewable energy transition from 2026 onward. Export economics reflect this strategic value. By September 2025, Japanese iodine export prices rebounded amid sustained deficits and rising procurement from emerging healthcare markets in India and Southeast Asia, reinforcing Japan’s role as a premium-grade supplier.

India Iodine Market: Pharmaceutical Growth and Radiopharmaceutical Readiness

India’s iodine market is demand-led, anchored by pharmaceuticals and emerging nuclear medicine capabilities. The domestic pharmaceutical sector projects a sustained increase in iodine consumption during 2025–2026 for antiseptics and contrast agents used in diagnostic imaging, reflecting expanding healthcare access and imaging intensity. Policy frameworks are shaping production efficiency. The launch of the Carbon Credit Trading Scheme in mid-2026 will bind major chemical processors in Gujarat and Maharashtra to emissions targets, incentivizing adoption of low-energy iodine recovery and purification processes.

Strategic capability is also advancing in medical isotopes. Construction progress by China National Nuclear Corporation on a medical isotope test reactor is on track to enable production of Iodine-131 and Iodine-125 by 2027, with 2026 serving as a critical year for domestic regulatory alignment and supply chain readiness in radiopharmaceuticals. This positions India to localize isotope availability while scaling downstream iodine derivatives for clinical use.

Iodine Industry: Country-Level Strategic Snapshot

Iodine Market County Level Snapshot

|

Region

|

Primary Strategic Driver

|

Key Application Focus

|

Structural Direction

|

|

Chile

|

Water security and capacity scaling

|

Technical and food-contact iodine

|

Energy-efficient, traceable Green Iodine

|

|

United States

|

Brine-based expansion and healthcare demand

|

USP-grade iodine, contrast media

|

Domestic scale-up with integrated offtake

|

|

Japan

|

Climate resilience and advanced materials R&D

|

High-purity exports, solar materials

|

Premium supply with future-facing applications

|

|

India

|

Pharmaceutical growth and isotope readiness

|

Antiseptics, diagnostics, radiopharma

|

Demand-led expansion with carbon compliance

|

Iodine Market Report Scope

Iodine Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.9 Billion

|

|

Market Size (2034)

|

$2.9 Billion

|

|

Market Growth Rate

|

5%

|

|

Segments

|

By Source (Underground Brines, Caliche Ore, Marine Biomass, Recycling and Recovery), By Form (Elemental Iodine, Inorganic Iodides, Organic Iodine Compounds, Iodophors), By Grade (Pharmaceutical Grade, Reagent Grade, Industrial Grade, Food and Feed Grade), By Application (Medical Imaging, Pharmaceuticals, Nutrition, Industrial Chemicals, Electronics, Agriculture)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sociedad Química y Minera de Chile S.A., Iochem Corporation, Iofina PLC, ISE Chemicals Corporation, Kanto Natural Gas Development Co., Ltd., Cosayach Compañía de Salitre y Yodo, Algorta Norte S.A., GODO SHIGEN Co., Ltd., INPEX Corporation, Nippoh Chemicals Co., Ltd., Toyota Tsusho Corporation, Adani Pharmachem Pvt. Ltd., Infinium Pharmachem Pvt. Ltd., Calibre Chemicals Pvt. Ltd., Siegfried Holding AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Iodine Market Segmentation

By Source

- Underground Brines

- Caliche Ore

- Marine Biomass

- Recycling and Recovery

By Form

- Elemental Iodine

- Inorganic Iodides

- Organic Iodine Compounds

- Iodophors

By Grade

- Pharmaceutical Grade

- Reagent Grade

- Industrial Grade

- Food and Feed Grade

By Application

- Medical Imaging

- Pharmaceuticals

- Nutrition

- Industrial Chemicals

- Electronics

- Agriculture

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Iodine Industry

- Sociedad Química y Minera de Chile S.A.

- Iochem Corporation

- Iofina PLC

- ISE Chemicals Corporation

- Kanto Natural Gas Development Co., Ltd.

- Cosayach Compañía de Salitre y Yodo

- Algorta Norte S.A.

- GODO SHIGEN Co., Ltd.

- INPEX Corporation

- Nippoh Chemicals Co., Ltd.

- Toyota Tsusho Corporation

- Adani Pharmachem Pvt. Ltd.

- Infinium Pharmachem Pvt. Ltd.

- Calibre Chemicals Pvt. Ltd.

- Siegfried Holding AG

*- List not Exhaustive