Japan Water Treatment Chemicals Market: Growth Forecast and Value Analysis

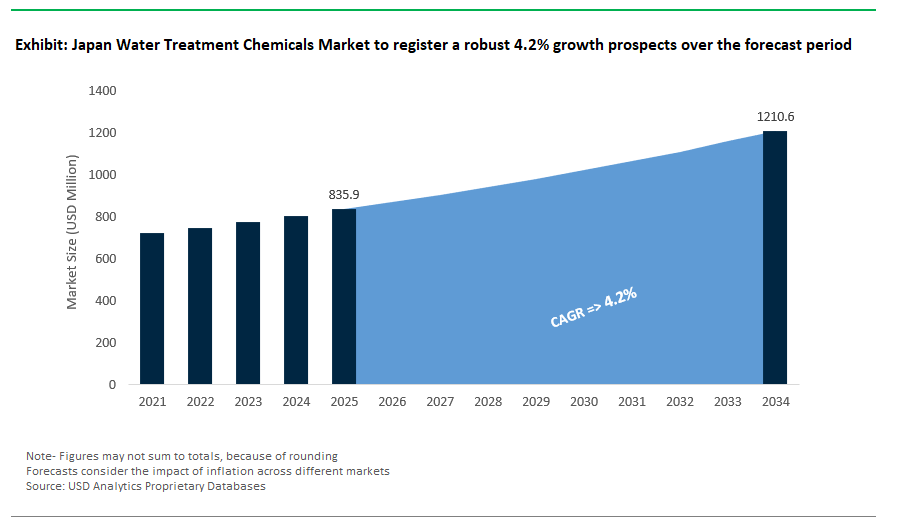

Japan Water Treatment Chemicals Market Size is estimated at $835.9 Million in 2025 and is forecast to register an annual growth rate (CAGR) of 4.2% to reach $1210.5 Million by 2034.

Japan’s water treatment chemicals market is distinguished by its precision-driven approach, emphasis on ultra-clean water standards, and robust infrastructure designed for resilience in the face of natural disasters. This market reflects an advanced synergy of regulatory compliance, precision chemical formulations, and infrastructure resilience, making it a global benchmark for performance and innovation in water treatment.

The country’s globally dominant electronics and semiconductor sectors demand ultrapure water, pushing treatment systems to achieve <0.1 ppb total organic carbon (TOC) using advanced UV/185 nm oxidation combined with membrane degasification, in compliance with SEMI F63 standards. Boron, a critical impurity in chip fabrication, is reduced to below 0.01 ppb using highly selective ion exchange resins under alkaline conditions (pH >10.5), following JIS K 0102 protocols. The stringent requirements for UPW in Japan's semiconductor industry are among the highest globally, driving continuous innovation in this segment.

On the municipal front, water utilities employ low-dose chlorine dioxide disinfection to eliminate coliforms while cutting trihalomethanes (THMs) by over 70%, in accordance with Japanese Water Works Association Standards, which supports the use of chlorine dioxide for effective disinfection with minimized DBP formation. Japan is also a leader in biosolids valorization, leveraging anaerobic digestion coupled with combined heat and power (CHP) systems to recover 60–80% of the energy embedded in municipal sludge, as promoted by the Japan Sewage Works Association. This approach aligns with national circular economy goals and reduces the environmental footprint of wastewater treatment plants.

Earthquake preparedness plays a pivotal role in treatment chemical deployment, with the Ministry of Land, Infrastructure, Transport and Tourism (MLIT) endorsing polymer-based flocculants for sediment stabilization in reservoirs at doses ranging from 0.5 to 2.0 mg/L an essential measure in landslide-prone regions. This proactive approach ensures water supply resilience even during natural calamities.

Looking ahead, the Japanese market is characterized by a growing municipal preference for integrated smart-sensor systems and highly adaptive filtration techniques, particularly for micro-pollutants. Innovations from leading corporations like Mitsubishi Chemical (next-generation polymer resins for toxic element removal), Hitachi (advanced nanofiltration devices), and Kubota Corporation (ceramic membrane systems for reduced maintenance) are driving progress. The emphasis on resource sustainability and stricter environmental directives further propels the adoption of chemical-free or reduced-chemical physical water treatment solutions, such as membrane filtration and advanced UV disinfection, to minimize residual sludge and align with greener industrial processes.

Market Trend: Japan Accelerates Green Chemistry & Digital Precision in Ultra-Pure Water Treatment

Japan’s water treatment chemicals market is rapidly evolving to meet the twin imperatives of extreme purity requirements and environmental compliance, especially in high-tech sectors such as semiconductors and pharmaceuticals. Following Japan’s 2024 PFAS Action Plan banning long-chain fluorinated compounds in industrial effluents, the market is witnessing swift adoption of PFAS-free and bio-based alternatives. Kurita’s Kuriverter® IK-110, a plant-derived antiscalant deployed at TSMC’s new Kumamoto fab, exemplifies this shift delivering 50% TOC reductions and full compliance with sub-ppb UPW thresholds. Meanwhile, enzymatic membrane cleaners like Tosoh’s EcoClean™ are replacing harsh chemical agents in pharma facilities, doubling membrane lifespan while aligning with PMDA purity norms. Digitalization is further reshaping the sector: Mitsubishi Chemical’s AquaAI system integrates predictive analytics to dynamically adjust corrosion inhibitor dosing in industrial cooling towers, reducing overuse by 20%. With over 30% of Japan’s municipal plants requiring corrosion-free upgrades (per METI), and semiconductors demanding <0.1 ppb purity levels, Japan is setting a new global benchmark for ultra-clean, digitally optimized, and green water treatment solutions.

Market Opportunity: Hydrogen & Battery Sectors Create Multibillion-Yen Niche for High-Purity Water Chemistry

Japan’s clean energy revolution anchored in green hydrogen and lithium-ion battery circularity is catalyzing a new ¥350 billion+ market for advanced water treatment chemicals. The Green Innovation Fund’s ¥2 trillion allocation is fast-tracking deployment of HyPure UPW systems from Organo, which blend ion exchange and EDR to produce <0.05 µS/cm feedwater for PEM electrolyzers in partnerships with Kawasaki Heavy Industries. Simultaneously, the EV battery recycling wave is generating demand for lithium-specific coagulants like Sumitomo Metal Mining’s LiPure, which enables 90% water reuse and lithium recovery from acidic leachate streams. With Panasonic’s Osaka facility monetizing cobalt recovery at ¥8,000/kg, chemical suppliers capable of supporting closed-loop water and resource recovery are gaining a competitive edge. Even beyond energy, data center growth is driving adoption of eco-safe biocides like Toray’s CoolGuard™ for Legionella control in NTT’s urban campuses. Backed by carbon credit incentives (e.g., Mitsui’s ZLD plant in Fukuoka earns ¥500/ton CO₂ saved), the synergy between water purification, resource valorization, and emissions reduction positions Japan as a prime innovation hub for next-gen water chemistries.

Competitive Landscape Analysis- Japan Water Treatment Chemicals Market

The Japanese water treatment chemicals market is marked by strong domestic leadership, high technical barriers, and a procurement environment that emphasizes value. Unlike cost-sensitive markets, Japan prioritizes reliability, certification, and long-term partnerships. These factors have led to an ecosystem dominated by local companies while foreign players operate in narrow strategic niches. This situation creates a market structure driven more by technology management, regulatory compliance, and vertical integration than by price competition.

Domestic leaders like Kurita Water Industries, Organo Corporation, and Toray Industries hold about 70% of the market. These companies benefit from long-standing ties, especially through Japan’s keiretsu and industrial groupings. Such relationships result in technological lock-in, where end users seldom change suppliers because of strict internal testing and the high costs of switching. The average contract lasts 7 to 10 years, which raises entry barriers for new challengers. Additionally, many of these firms cover the entire water treatment value chain, from chemical formulation to system installation and maintenance, allowing them to significantly control product performance and integration.

One key feature of the Japanese competitive landscape is premium pricing linked to certification. Products that meet the Japan Industrial Standards (JIS) command a 25% to 30% price premium, which local buyers accept due to the perceived quality, safety, and environmental standards. However, obtaining and maintaining JIS compliance involves high initial costs typically between ¥50 million and ¥100 million per product making it hard for smaller or foreign companies to enter the market. This certification creates a barrier that keeps even high-growth areas like ultrapure water (UPW) for semiconductors limited to a few suppliers who can operate on a large scale.

Vertical integration and government-supported R&D further strengthen incumbents. For example, Toray uses METI-funded projects to improve membrane chemistry, while Kurita's acquisition approach aligns with its smart manufacturing philosophy. This alignment with Japan’s industrial policy and innovation grants enables a sustained edge in high-value sectors such as electronics, automotive, and precision manufacturing.

While foreign firms like Ecolab and BASF have a presence, their impact is limited and highly adapted. Their growth strategies depend on local formulation centers, joint projects (such as those with Toyota), and niche markets like data center cooling or electronics. However, public contracts, particularly in municipal or infrastructure projects, heavily favor domestic vendors, further restricting opportunities for international entrants.

On the fringes, a small but notable segment of innovators holds about 5% market share and is starting to challenge the status quo. Backed by venture capital and institutional funding, companies like Aquatech Innovation and GreenChem Japan target underserved SME manufacturers and align with Society 5.0 goals Japan’s smart city initiative. Their emphasis on IoT, nanobubbles, and plant-based formulations positions them as potential disruptors, especially as sustainability standards tighten and legacy systems age.

Japan Water Treatment Chemicals Market– Segmentation Insights (2025–2034)

By Type of Chemical: Corrosion Inhibitors Lead, Membrane Cleaners Grow Fastest

In the Japan water treatment chemicals market, corrosion and scale inhibitors represent the largest share at 30.2% in 2025, largely due to the country’s aging industrial infrastructure and the need for rigorous equipment maintenance across sectors such as power generation, manufacturing, and petrochemicals. These chemicals play a vital role in preventing scaling and corrosion in boilers, pipelines, and heat exchangers, thereby enhancing equipment lifespan and efficiency. Japan’s strict industrial maintenance codes and safety compliance requirements also contribute to the consistent demand for these inhibitors.

In contrast, membrane cleaning chemicals are projected to grow at the fastest CAGR of 5.6% between 2025 and 2034, propelled by increasing deployment of RO (Reverse Osmosis) and NF (Nanofiltration) systems, particularly in high-tech manufacturing clusters. Sectors such as semiconductors, pharmaceuticals, and ultrapure water (UPW) production demand high-performance chemical treatments to ensure membrane longevity and optimal water quality. The growing trend of decentralised water treatment and water reuse solutions in urban areas is also expanding the footprint of membrane-based purification technologies, further boosting demand for chemical cleaners tailored to scale, biofouling, and particulate buildup. This shift underscores Japan’s move toward precision-driven water treatment approaches, balancing traditional system preservation with cutting-edge purification.

.png)

By End-User Industry: Municipal Segment Dominates, Manufacturing Accelerates

From an end-user perspective, the municipal sector holds the largest share at 39.7% in 2025, driven by Japan’s advanced drinking water infrastructure and highly regulated wastewater management frameworks. The country’s strong focus on public health, compliance with national water quality standards, and emphasis on wastewater recycling (especially in urban areas like Tokyo and Osaka) have solidified municipal water treatment as the backbone of chemical demand. Chlorine-based disinfectants, coagulants, and pH adjusters remain central to these operations.

However, the manufacturing sector is emerging as the fastest-growing end-user, expanding at a CAGR of 6.3% through 2034, fueled by rising investments in semiconductor fabs, precision electronics, and biopharmaceutical production facilities. These industries require ultrapure water and closed-loop systems that rely heavily on specialty chemicals, including membrane cleaning agents, biocides, and corrosion inhibitors. Additionally, the use of geothermal energy in Japan’s power sector supports consistent demand for scale inhibitors, while oil & gas and chemical sectors continue to support chemical-intensive water treatment in cooling and steam generation. This dual-market dynamic municipal volume leadership and industrial value acceleration defines the strategic outlook for water treatment chemical suppliers in Japan.

Japan Water Treatment Chemicals Market Report Scope

Japan Water Treatment Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$835.9 Million

|

|

Market Size (2034)

|

$1210.5 Million

|

|

Market Growth Rate

|

4.2%

|

|

Segments

|

By Type of Chemical (Coagulants and Flocculants, Corrosion and Scale Inhibitors, Biocides and Disinfectants, pH Adjusters and Softeners, Oxygen Scavengers, Defoamers and Antifoaming Agents, Membrane Cleaning Chemicals, H2S Scavengers, Other Specialty Chemicals), By Application (Municipal Water Treatment, Industrial Water Treatment, Commercial Water Treatment), By End-User Industry (Municipal, Power Generation, Oil and Gas, Chemical and Petrochemical, Manufacturing), By Form of Chemical (Liquid, Powder/Solid), By Distribution Channel (Direct Sales, Distributors/Channel Partners

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Kurita Water Industries Ltd., Toray Industries, Inc., Mitsubishi Chemical Corporation (and Mitsubishi Chemical Cleansui), Hitachi Ltd., Kubota Corporation, METAWATER Co., Ltd., Suido Kiko Kaisha, LTD., Taki Chemical Co., Ltd., MT AquaPolymer, Inc., Sanyo Chemical Industries, Ltd., Ecolab Inc. (U.S.), Solenis LLC (U.S.), BASF SE (Germany), Kemira Oyj (Finland), SNF Floerger (France), Veolia Water Technologies (France), The Dow Chemical Company (U.S.),

|

Japan Water Treatment Chemicals Market Segmentation

By Type of Chemical

- Coagulants and Flocculants

- Corrosion and Scale Inhibitors

- Biocides and Disinfectants

- pH Adjusters and Softeners

- Oxygen Scavengers

- Defoamers and Antifoaming Agents

- Membrane Cleaning Chemicals

- H2S Scavengers

- Other Specialty Chemicals

By Application

- Municipal Water Treatment

- Drinking Water Treatment

- Municipal Wastewater Treatment

- Industrial Water Treatment

- Cooling Water Treatment

- Boiler Water Treatment

- Process Water Treatment

- Industrial Wastewater Treatment

- Water Reuse and Recycling

- Industrial Desalination

- Sludge Treatment

- Commercial Water Treatment

By End-User Industry

- Municipal

- Power Generation

- Oil and Gas

- Chemical and Petrochemical

- Manufacturing

- Food and Beverage

- Pulp and Paper

- Textile

- Mining and Metallurgy

- Pharmaceutical

- Automotive

- Electronics and Semiconductors

- Other Industrial Manufacturing

By Form of Chemical

By Distribution Channel

- Direct Sales

- Distributors/Channel Partners

Top Companies in Japan Water Treatment Chemicals Market

- Kurita Water Industries Ltd.

- Toray Industries, Inc.

- Mitsubishi Chemical Corporation (and Mitsubishi Chemical Cleansui)

- Hitachi Ltd.

- Kubota Corporation

- METAWATER Co., Ltd.

- SuidKikKaisha, LTD.

- Taki Chemical Co., Ltd.

- MT AquaPolymer, Inc.

- SanyChemical Industries, Ltd.

- Ecolab Inc. (U.S.)

- Solenis LLC (U.S.)

- BASF SE (Germany)

- Kemira Oyj (Finland)

- SNF Floerger (France)

- Veolia Water Technologies (France)

- The Dow Chemical Company (U.S.)

* List Not Exhaustive

Research Coverage

The Japan Water Treatment Chemicals Market Report by USDAnalytics delivers an in-depth examination of the country’s high-performance water treatment ecosystem, shaped by stringent regulatory compliance, precision-driven ultrapure water (UPW) standards, and sustainability mandates. The report focuses on the integration of advanced chemical formulations with smart digital dosing platforms and PFAS-free chemistries, alongside the shift toward bio-based solutions in alignment with Japan’s 2024 PFAS Action Plan and circular economy objectives.

Scope Includes:

- By Type of Chemical: Corrosion and Scale Inhibitors, Coagulants & Flocculants, Biocides, pH Adjusters, Membrane Cleaning Agents, Oxygen Scavengers, Defoamers, Specialty Chemicals

- By Application: Municipal Water Treatment (Drinking, Wastewater), Industrial Water Treatment (Cooling, Boiler, Process, Water Reuse), Commercial Water Treatment

- By End User: Municipal Utilities, Electronics & Semiconductors, Chemical & Petrochemical, Automotive, Pharmaceuticals, Food & Beverage, Power Generation

- By Form: Liquid and Powder/Solid

- By Distribution Channel: Direct Sales, Distributors/Channel Partners

- Geographic Focus: Comprehensive coverage of industrial hubs like Kanto (Tokyo), Kansai (Osaka), Kyushu (Fukuoka), and Kumamoto for semiconductor manufacturing, municipal water plants, and zero-liquid discharge facilities.

- Study Period: Historic: 2021–2024; Forecast: 2025–2034

- Leading Players: Kurita Water Industries, Toray Industries, Mitsubishi Chemical Corporation, Ecolab, BASF SE, Kemira Oyj, Solenis LLC, SNF Floerger, Veolia Water Technologies.

Methodology

The study follows a structured, multi-step research methodology, ensuring accuracy and actionable insights:

- Primary Research: Interviews with executives from major water chemical firms (e.g., Kurita, Toray), plant operators, and procurement managers in sectors like electronics, municipal utilities, and green hydrogen facilities. Consultations with Japanese regulators (MLIT, METI) and industry associations such as the Japan Sewage Works Association.

- Secondary Research: Analysis of government policies (PFAS Action Plan 2024, Green Innovation Fund, Water Works Standards), corporate sustainability disclosures, METI statistical yearbooks, JIS standards, and industrial journals.

- Market Modeling: Utilization of bottom-up segmental analysis validated with trade data, capex trends, and UPW plant deployments. AI-powered forecasting models incorporated semiconductor fab expansions, EV battery recycling initiatives, and municipal upgrade projects.

- Validation Framework: Cross-checks through case studies such as Kurita’s Kuriverter® IK-110 deployment for semiconductor fabs and municipal trials for PFAS-free chemistries. Benchmarking aligned with REACH compliance, ISO standards, and Japanese Industrial Standards (JIS).

Deliverables

- Complete Market Research Report (PDF, Excel): data tables, market charts, and visual insights.

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis

- Recent Developments & News Tracker

- Executive summary and key takeaway slides for boardroom presentations

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements