K-12 Online Education Service Market: Global Expansion Fueled by AI Integration and Hybrid Learning Models

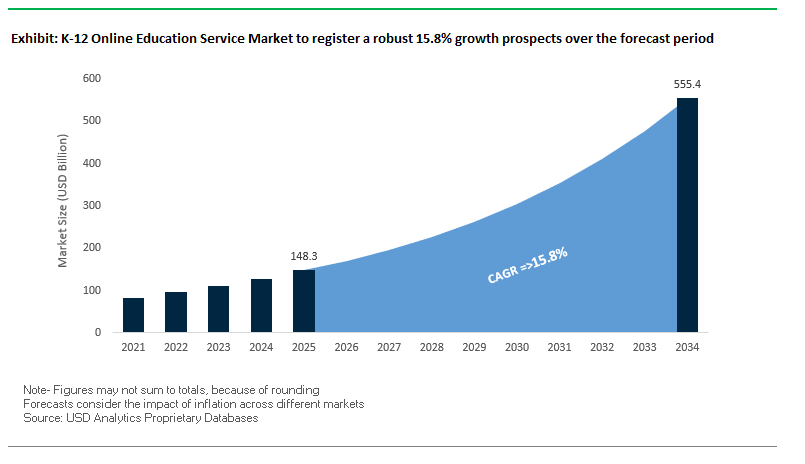

The global K-12 online learning services market is evolving from pandemic-era adoption to a permanent, revolutionary base of the learning system. The market is projected to expand from $148.3 billion in 2025 to $555.3 billion by 2034, achieving a CAGR of 15.8%. Growth within the industry is being driven by the convergence of next-generation digital infrastructure, artificial intelligence, and hybrid learning environments that combine in-classroom and online learning. For educators, the change is less about delivery and more about reframing the point of intersection between curriculum, pedagogy, and technology as it enables individualized and scalable learning.

K-12 online learning has traveled a long way from being an emergency substitute to a driving force for accessibility, inclusivity, and flexibility. With increasing investment by schools, governments, and ed-tech companies in adaptive learning platforms, virtual classrooms, and AI-based tools, the market is witnessing a wave of adoption across developed and emerging markets.

Key Insights for Education Industry Stakeholders:

- Sustained adoption: Over 65% of parents now view online learning as equally or more effective than traditional classrooms.

- Infrastructure acceleration: National programs like China’s Broadband China and the U.S. FCC’s E-Rate have expanded high-speed connectivity, enabling real-time interactive learning.

- AI-driven personalization: Tools like Oak National Academy’s “Aila” are revolutionizing lesson planning and content customization for diverse learning needs.

- Hybrid learning permanence: Platforms such as Google Classroom, Microsoft Teams, and Zoom are embedding virtual tools into regular instruction, creating a blended standard for education delivery.

Market Analysis: Recent Global Developments Driving K-12 Online Education Growth

Since 2024, the K-12 online schooling market saw growth in strategic partnerships, technology adoption, and expansion in a bid to build stronger and future-oriented education systems.

In April 2025, Oak National Academy AI solution "Aila" saw a sudden rise in adoption, with more than 20,000 teachers using it to automate lesson planning and adapt content. This reflects rising demand from teachers for AI-powered instructional design. In February 2025, the Adani Foundation partnered with GEMS Education to launch 'Adani GEMS Schools of Excellence' in India, adding top-notch physical infrastructure as well as digital learning platforms to provide greater access to affordable, world-class education.

March 2025 was a milestone in financing when K12 Techno Services raised $40 million from Kenro Capital to grow its tech-based learning solutions. June 2025 was a milestone when Zamit's global footprint expanded to 46 nations, disseminating a distinct "future readiness" model that is sensitive to the evolving needs of 21st-century students.

On the policy side, October 2024's continued implementation of India's National Education Policy 2020 reaffirmed the place of technology and digital pedagogy in creating critical thinking and imagination. This was backed by the World Bank's August 2024 report, which stressed learning ecosystems having to be robust in the aftermath of the disruption caused to over 400 million students owing to climate-driven school closures in the recent past.

These advances highlight the industry's speedy shift from supplementary to integrated, as investors pour money into solid hybrid learning infrastructures and flexible technology to address international education needs.

Trends and Opportunities in the K-12 Online Education Service Industry

AI-Powered Adaptive Learning Platforms Driving Hyper-Personalized Education

Cloud-based co-play engine integration is changing audience interaction by enabling viewers to participate in live game streams in real-time without local download or execution of the game. It utilizes remote rendering and low-latency streaming to enable real-time co-op play, decision voting on in-game decisions, and audience challenges. For the streamer, this significantly increases session retention time because interactive engagement keeps viewers online longer. Cloud scalability platforms support easily thousands of interactive viewers online at once with no performance penalty. Co-play enables premium monetization streams, where fans pay for exclusive participation rights, influence key game result drivers, or access secret in-game events. This infrastructure is applicable beyond games but is varied for live concerts, sports party viewing, and interactive storytelling, with cross-industry growth potential.

Hybrid Learning Models Cementing Their Role in Long-Term Education Policy

The use of AI-powered commentary avatars allows platforms to provide hyper-personalized game casting to everyone. AI casters are capable of adjusting tone, emphasis, and pace from real-time viewer behavior, preferences, and chat activity, providing statistical deep-dives for competitive viewers or high-level overviews for casual viewers. Advanced natural language processing and translation abilities allow streams to be watched in multiple languages at once, eliminating global language barriers. AI avatars also allow for chat moderation, highlight reel creation, and live analytics creation for viewers and creators, taking production workload off of streamers. As virtual influencer technology continues to develop, these AI casters are also a new type of brandable digital personality, allowing creators to cast themselves outside of live streams.

Micro-Credentials and Skill-Based Certifications Reshaping Early Career Readiness

Micro-credential application in K-12 is a robust growth area for EdTech companies and schools. Micro-credentials are brief, verifiable certificates in independent, work-ready skills such as coding, digital marketing, financial literacy, or data analytics skills more highly prized by employers and universities. Micro-credentials supplement traditional coursework with tangible evidence of expertise, potentially aiding admissions to universities or early hiring. Micro-credentials can be offered as independent online modules or integrated into existing curricula, enabling students to accumulate a portfolio of credentials at graduation. The rising global trend toward competency-based education and lifelong learning positions micro-credentials as a likely candidate to become an integral part of K-12 programs, bridging the gap between academic study and professional readiness.

Gamification and Scholastic Esports Driving STEM Engagement

Gamification and the integration of scholastic esports are revolutionizing curriculum planning, making classrooms interactive, skill-based learning environments. Gamified instruction uses reward mechanisms badges, leaderboards, and challenges to optimize interest in learning, which enhances retention rates and promotes healthy scholarly competition. Scholastic esports programs go beyond play, involving students in STEM-intensive fields like network engineering, game development, data analysis, and broadcast production. Global organizations like the North America Scholastic Esports Federation (NASEF) are connecting with schools directly with funding, teacher training, and industry mentorship. These programs develop critical soft skills teamwork, problem-solving, and leadership while providing transparent career paths in technology, digital media, and creative industries. As STEM recruitment becomes a national priority in nations around the globe, gamification and esports are an evidence-based engagement model to recruit and retain student interest in high-demand fields.

K-12 Online Education Service Market Share and Segmentation Insights

By Learning Model: Blended Learning Leading Post-Pandemic Market Adoption

Blended learning enjoys the largest market share of 45% through its mix of face-to-face human communication and online convenience. It is best for students who are comfortable with socialization in classrooms and employ digital media for individualized learning. Virtual schools are a close second with 35% backing from state-sponsored programs, charter school growth, and homeschooling adoption. They are best for geographically dispersed students, special needs students, and families seeking non-traditional schooling. Supplemental education segment of online tutoring, test prep, and enrichment continues to grow, driven by AI-based personalization and increased parental investment in academic support outside traditional schooling.

By Technology: LMS and Digital Content Form the Core Infrastructure of K-12 E-Learning

Learning Management Systems (LMS) lead the way with 30% market share as the underpinning structure for course organization, tracking, and integration of tools to assess. Digital content and interactive e-textbooks account for 25%, providing multimedia-enhanced materials that surpass static PDFs with the addition of quizzes, videos, and AR/VR capabilities for interactive learning. Collaboration tools like Zoom and Microsoft Teams are shifting with education-centric features like virtual whiteboards and breakout rooms. Assessment and analytics tools are gaining ground for real-time tracking of performance, allowing educators to close gaps in learning sooner. AR/VR and simulation tools while having a lower percentage are growing in STEM and experiential learning, providing virtual labs, field trips, and 3D simulations to make abstract concepts understandable and interactive.

.png)

Competitive Landscape: Key Players Shaping the K-12 Online Education Service Market

The competitive environment in K-12 online education is defined by a blend of established learning providers, edtech innovators, and global technology platforms all competing to deliver personalized, scalable, and engaging learning experiences. Key players included are Stride, Inc., Pearson plc, McGraw-Hill Education, Instructure, Inc., Coursera, Inc., BYJU'S, Unacademy, Vedantu, D2L Inc., TAL Education Group, Chegg, Inc., Microsoft Corporation, Alphabet Inc. (Google for Education), Blackboard Inc. (Anthology), Renaissance Learning, Inc., Others.

Stride, Inc. – End-to-End Virtual School Model Leader

Stride inherits two decades of experience in running K12-fueled online schools globally. Its platform marries curriculum, certified instructors, and extracurricular activities into one unified online education system. The company focuses on individualized learning pathways and career readiness programs, allowing students to follow interests while satisfying state standards. Of particular note is its commitment to military families and spouse employment programs, which has carved out a distinct niche.

Connections Academy (Pearson) – Curriculum-Driven Online Public Schooling

As a Pearson company, Connections Academy utilizes global education expertise in offering free online public school courses across several states. Its research-driven curriculum integrates live instruction with hands-on activities to maintain learner engagement. The program boasts robust parent-teacher-student interaction, with 2025 surveys reporting that 93% of parents experienced improved teacher-student relationships through its model.

Instructure, Inc. (Canvas) – Global LMS Powering Hybrid Learning

Instructure's Canvas LMS is an anchor technology platform for online and blended K-12 learning across the globe. Its cloud-first design enables seamless course management, communication, and assessment with adaptive learning and third-party tool integration. Institutions are able to customize their learning environment with the company's open integration approach, and therefore it's the solution of choice for scalable and agile digital learning infrastructure.

TAL Education Group – AI-Driven Personalized Tutoring

TAL Education is China's market leader in technology-enabled K-12 tutoring. Live tutoring, small class, and competitive academic training services are offered. AI-based feedback and adaptive question banks have enabled real-time student interaction and performance monitoring, making TAL a technology-enabled education leader.

Moodle – Open-Source LMS Democratizing Education Technology

Moodle's open-source nature offers unprecedented customization to governments, districts, and schools at zero proprietary cost. Its global user base offers constant improvement, making it highly adaptable in a variety of learning environments. Recent availability of professional hosting and integration services around Moodle marks the establishment of a robust support ecosystem helping institutions to scale online learning cost-effectively and efficiently.

India: NEP-Driven Digital Transformation and EdTech Innovation

India’s K-12 online education service market is undergoing rapid modernization under the influence of landmark government policies such as the National Education Policy (NEP) 2020 and PM SHRI Schools. These initiatives aim to seamlessly integrate digital technology into classrooms through the deployment of smart boards, online assessment systems, and virtual labs. The push for curriculum diversification introducing coding, AI, robotics, and drone technology at the school level is strengthening India’s position as a hub for future-ready education. The government’s budgetary allocations towards education also prioritize the expansion of broadband connectivity and device accessibility for rural and semi-urban schools, ensuring that digital inclusivity becomes a central pillar of the K-12 system.

The Indian EdTech ecosystem is booming, with a wave of startups and established companies delivering blended learning models that combine live online instruction with interactive self-learning modules. Platforms such as Byju’s, Vedantu, and Unacademy are leveraging AI-driven personalization to enhance student engagement and retention. Smartphone penetration exceeding 75% and affordable internet data plans have fueled the accessibility of these platforms, enabling students from diverse socioeconomic backgrounds to participate. Teacher training programs backed by government-funded centers of excellence are improving digital pedagogy, preparing educators to effectively utilize online tools in lesson delivery. The result is a highly dynamic market, blending policy support, technology adoption, and entrepreneurial innovation.

United States: Mature Infrastructure and Personalized Learning Ecosystem

The United States maintains one of the most mature K-12 online education markets, supported by advanced broadband infrastructure, widespread device availability, and high digital literacy among students and educators. School districts nationwide are integrating adaptive learning platforms and interactive whiteboards into classrooms, creating hybrid models that enhance both in-person and remote instruction. The U.S. has been a pioneer in implementing personalized learning ecosystems, where AI and machine learning algorithms track student performance in real time, allowing for tailored curriculum pathways and intervention strategies. This personalized approach is widely applied in STEM-focused programs, reinforcing the country’s long-term emphasis on preparing students for technology-driven careers.

Public-private partnerships are a defining feature of the U.S. market. Collaborations between school boards, EdTech companies, and federal agencies have led to the development of sophisticated Learning Management Systems (LMS) and cloud-based collaboration tools. Large-scale initiatives such as the ConnectED program have accelerated technology adoption, especially in underserved communities. The COVID-19 pandemic catalyzed mass adoption of online education platforms, a trend that continues to influence parental demand for flexible, at-home learning options. With the growing availability of government grants and state funding for digital infrastructure, the U.S. is well-positioned to lead in innovative K-12 education models that combine academic rigor with personalized student engagement.

China: State-Regulated EdTech Growth and Mass Digital Adoption

China’s K-12 online education sector benefits from one of the largest internet user bases in the world, with a rapidly urbanizing population that demands high-quality educational resources. The government has heavily invested in digital learning infrastructure, rolling out smart classroom projects and online curriculum standards across multiple provinces. This has been accompanied by policy-driven integration of AI-powered learning platforms and virtual tutoring services into the K-12 ecosystem. However, stringent content regulation remains a defining factor in market operations, with the government closely monitoring EdTech companies to ensure compliance with academic quality and ideological guidelines.

China’s EdTech giants such as Tencent, Alibaba, and Baidu are integrating live streaming, AI assessment tools, and gamified learning experiences into their platforms, creating highly interactive and scalable solutions. The market also exhibits strong e-commerce integration, where educational content, materials, and supplementary services are sold directly to parents via live-streaming channels. With disposable incomes rising, parents in both urban and semi-urban regions are increasingly willing to invest in after-school online learning programs to boost student performance. This combination of policy-backed infrastructure, high digital penetration, and corporate innovation positions China as a dominant force in the global K-12 online education industry.

Germany: Policy-Supported Digital Schooling and Inclusive Access

Germany’s K-12 online education services are expanding under the influence of the DigitalPakt Schule (Digital Pact for Schools), which provides federal funding to modernize school IT infrastructure. This policy aims to equip classrooms with high-speed internet, interactive displays, and secure learning platforms. The German government’s education strategy emphasizes digital inclusivity, ensuring that rural and underserved schools have equal access to technology. The integration of data privacy-compliant platforms is a key differentiator in Germany’s market, aligning with strict EU GDPR requirements.

Teacher professional development is a core focus, with state-level initiatives offering training on integrating digital tools into lesson planning. Hybrid and blended learning models are being increasingly adopted to accommodate diverse student learning needs, including support for migrant and multilingual student populations. Partnerships with EdTech providers are bringing in adaptive assessment tools, gamified learning environments, and STEM-focused digital labs. Germany’s approach blends public funding, regulatory compliance, and progressive pedagogy, positioning it as a steadily growing K-12 online education market in Europe.

Japan: High-Tech Learning Ecosystems and Cultural Adaptation

Japan’s K-12 online education market thrives on its advanced connectivity infrastructure, with near-universal internet access and rapid 5G expansion enabling seamless e-learning experiences. The government’s GIGA School Program has been a game changer, providing every student with a device and high-speed network access, thus creating a nationwide digital learning foundation. Japanese schools are incorporating AI-assisted teaching platforms that adapt to individual learning paces and styles, which aligns well with the country’s cultural emphasis on precision and academic excellence.

EdTech companies are also integrating immersive technologies such as VR-based science simulations and AR-enabled history lessons to enhance engagement. While traditional education models remain influential, there is a growing acceptance of online and blended formats, particularly for STEM enrichment and English language learning. Parental demand for flexible learning schedules is increasing, prompting schools to expand after-school online tutoring services. Japan’s fusion of technological sophistication, government support, and cultural alignment is positioning it as a leading innovator in Asia’s K-12 online education space.

K-12 Online Education Service Market Report Scope

K-12 Online Education Service Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$148.3 Billion

|

|

Market Size (2034)

|

$555.3 Billion

|

|

Market Growth Rate

|

15.8%

|

|

Segments

|

By Learning Model (Virtual Schools, Blended Learning, Supplemental Education), By Technology (Learning Management Systems (LMS), Digital Content and E-Textbooks, Assessment and Analytics Tools, Collaboration Platforms, AR/VR and Simulation Tools), By Grade Level (Elementary School (K-5), Middle School (6-8), High School (9-12)), By End User (Schools, Individual Learners, Homeschooling), By Institution Type (Public Institutions, Private Institutions)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Stride, Inc., Pearson plc, McGraw-Hill Education, Instructure, Inc., Coursera, Inc., BYJU'S, Unacademy, Vedantu, D2L Inc., TAL Education Group, Chegg, Inc., Microsoft Corporation, Alphabet Inc. (Google for Education), Blackboard Inc. (Anthology), Renaissance Learning, Inc., Others.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

K-12 Online Education Service Market Segmentation

By Learning Model

- Virtual Schools

- Blended Learning

- Supplemental Education

By Technology

- Learning Management Systems (LMS)

- Digital Content and E-Textbooks

- Assessment and Analytics Tools

- Collaboration Platforms

- AR/VR and Simulation Tools

By Grade Level

- Elementary School (K-5)

- Middle School (6-8)

- High School (9-12)

By End User

- Schools

- Individual Learners

- Homeschooling

By Institution Type

- Public Institutions

- Private Institutions

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in K-12 Online Education Service Market

- Stride Inc.

- Pearson plc

- McGraw-Hill Education

- Instructure Inc.

- Coursera Inc.

- BYJU'S

- Unacademy

- Vedantu

- D2L Inc.

- TAL Education Group

- Chegg Inc.

- Microsoft Corporation

- Alphabet Inc. (Google for Education)

- Blackboard Inc. (Anthology)

- Renaissance Learning Inc.

* List Not Exhaustive

Research Coverage

This report by USDAnalytics investigates the global K-12 Online Education Service Market, offering an in-depth exploration of breakthroughs, analysis reviews, and strategic highlights that define the sector’s rapid evolution. It examines key market dynamics, evaluates emerging technologies such as AI-powered adaptive learning platforms, and assesses hybrid learning adoption trends across multiple regions. The research provides actionable insights into policy-driven transformations, competitive strategies, and innovation-led growth opportunities shaping the future of K-12 digital learning. With its detailed coverage of market structure, technology adoption patterns, and strategic positioning of top players, this report is an essential resource for education policymakers, EdTech companies, and institutional stakeholders aiming to navigate and capitalize on this fast-growing market. Scope includes-

- Segmentation:

- By Learning Model: Virtual Schools, Blended Learning, Supplemental Education

- By Technology: Learning Management Systems (LMS), Digital Content and E-Textbooks, Assessment and Analytics Tools, Collaboration Platforms, AR/VR and Simulation Tools

- By Grade Level: Elementary School (K-5), Middle School (6-8), High School (9-12)

- By End User: Schools, Individual Learners, Homeschooling

- By Institution Type: Public Institutions, Private Institutions

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Historic Data & Forecasts: Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies: Analysis/profiles of 15+ companies.

Methodology

The research methodology integrates a robust combination of primary and secondary research to ensure accurate and actionable insights. Primary research involved interviews and surveys with industry experts, education policymakers, EdTech innovators, and K-12 institution administrators across key markets. Secondary research included an exhaustive review of government reports, academic publications, corporate disclosures, and regulatory updates to track technological adoption trends and policy impacts. Advanced analytical tools were employed to assess market segmentation, forecast growth trajectories, and map competitive landscapes. This data-driven approach ensures a comprehensive understanding of market trends, competitive positioning, and emerging opportunities within the K-12 online education ecosystem.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.