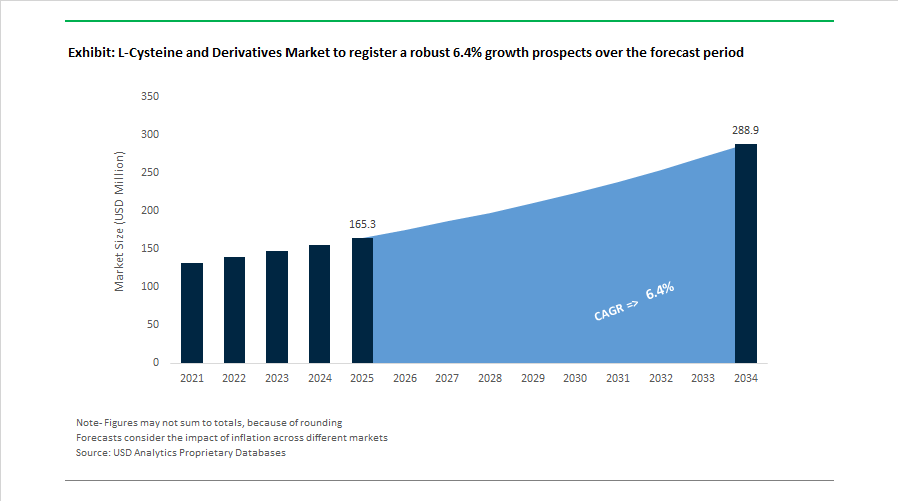

L-Cysteine and Derivatives Market to Reach $288.9 Million by 2034 Driven by Biopharma Demand and Fermentation Innovation

The L-Cysteine and Derivatives Market is projected to expand from $165.3 Million in 2025 to $288.9 Million by 2034, registering a CAGR of 6.4%. Market expansion is being driven by rising demand for pharmaceutical-grade amino acids, fermentation-based clean-label food ingredients, and specialty derivatives used in respiratory drugs and monoclonal antibody production. The competitive landscape is increasingly defined by biotechnology integration, AI-driven fermentation control, and supply chain localization for high-purity sulfur-containing amino acids.

In January 2025, Wacker Chemie AG inaugurated a new AI-controlled fermentation facility in Burghausen, Germany, effectively doubling its food-grade L-cysteine capacity. The plant integrates real-time microbial growth monitoring to optimize yield and reduce carbon intensity per kilogram produced. This follows Wacker’s 2024 rollout of AI-enabled quality control systems across its global biotech network, enabling impurity detection at levels required for semiconductor and pharmaceutical applications. These digital fermentation systems are setting new benchmarks for production efficiency and traceability in amino acid manufacturing.

Pharmaceutical applications remain a primary growth engine. In 2024, Exela Pharma Sciences received expanded FDA recognition for ELCYS (cysteine hydrochloride injection), reinforcing its use in Total Parenteral Nutrition for neonatal and pediatric patients with severe liver conditions. The move elevated injectable L-cysteine to a standard-of-care component in critical care nutrition. In late 2024 through 2025, Evonik scaled commercialization of cQrex KC, a peptide derivative of L-cystine designed to overcome solubility constraints at neutral pH. This innovation enhances amino acid delivery efficiency in bioreactors producing monoclonal antibodies and advanced biologics. Further strengthening the peptide ecosystem, Ajinomoto Bio-Pharma Services partnered with Olon S.p.A. in October 2025 to expand large-scale peptide and antibody-drug conjugate manufacturing using sulfur-containing amino acids.

Strategic portfolio optimization is reshaping industry structure. In April 2025, Ajinomoto Co., Inc. divested its Ajinomoto Althea CDMO stake to concentrate on high-value amino acids, reinforcing its pharmaceutical and medical food positioning. Nippon Fine Chemical announced in November 2025 that its Specialty Amino Acids operations will transition to 100% renewable energy by 2030 under its VISION 2030 roadmap, aligning L-cysteine production with ESG benchmarks demanded by multinational pharmaceutical buyers.

Nutraceutical and functional food applications are expanding rapidly. In May 2024, Plexus Worldwide introduced IronWoman, incorporating L-cysteine derivatives to enhance iron absorption in women-focused supplements. CJ Bio showcased its WellNrich and AMINATURE portfolios in October 2025, highlighting fermentation-derived, non-animal L-cysteine for muscle health and “beauty-from-within” formulations. In parallel, CJ CheilJedang formalized its CJ Food & Nutrition Tech division in 2024, leveraging L-cysteine-driven Maillard reaction chemistry to develop clean-label vegan meat flavor systems for the alternative protein market.

Respiratory therapeutics represent another accelerating segment. In 2025, Wuhan Grand Hoyo expanded its Carbocisteine production line to address rising demand for mucolytic APIs across aging populations in Asia and Europe. Carbocisteine, derived from L-cysteine, is increasingly prescribed for chronic bronchitis and other obstructive pulmonary conditions.

Strategic Trends and High-Conviction Opportunities Reshaping the L-Cysteine and Its Derivatives Market

Trend: Mandatory Shift to Fermentation-Derived L-Cysteine for Pharmaceutical-Grade Purity and Compliance

The L-cysteine and its derivatives market is undergoing a structural transformation as pharmaceutical, nutraceutical, and clinical nutrition buyers move decisively away from animal-derived cysteine sources toward fermentation-based production. This shift is driven by heightened regulatory scrutiny, biosecurity risk mitigation, and traceability requirements across global drug and excipient supply chains. In October 2025, the European Food Safety Authority issued a definitive scientific opinion confirming the safety of L-cysteine and L-cysteine hydrochloride produced via electrochemical reduction of L-cystine sourced from genetically modified E. coli fermentation. This regulatory clarification effectively establishes fermentation-derived L-cysteine as the reference standard for pharmaceutical and feed-grade applications in Europe, removing long-standing ambiguity around non-animal production pathways.

In response, leading amino acid manufacturers such as Wacker Chemie AG and Ajinomoto have accelerated capital deployment into microbial fermentation capacity. These investments are strategically positioned to support upcoming zero-animal procurement mandates adopted by European pharmaceutical majors for 2026 onward. Beyond regulatory compliance, fermentation-based cysteine offers superior batch-to-batch consistency, sulfur source control, and resilience against supply disruptions linked to keratin extraction, particularly in China. Demand is further amplified by Kosher, Halal, and vegan certification requirements, where fermentation-derived L-cysteine is the only scalable option that satisfies ethical, religious, and pharmaceutical-grade purity standards simultaneously.

Trend: Pharmaceutical Repositioning of N-Acetyl-L-Cysteine Across Respiratory and Neuropsychiatric Indications

N-Acetyl-L-Cysteine is transitioning from a narrow-use antidote and mucolytic into a strategically important therapeutic adjunct across multiple chronic disease categories. Its continued inclusion on the 24th Model List of Essential Medicines by the World Health Organization in September 2025 has reinforced its role in national drug procurement programs, particularly in emerging markets where cost-effective antioxidant therapies are prioritized. This status ensures sustained baseline demand for pharmaceutical-grade NAC formulations, including injectables and oral solids.

Clinical momentum is expanding NAC’s addressable market well beyond acute care. Meta-analyses published in early 2025 highlight its efficacy in modulating glutamatergic signaling and systemic inflammation, with evidence supporting its role as an adjunct therapy in treatment-resistant depression and bipolar disorder. Parallel respiratory studies published between 2024 and 2025 in Archivos de Bronconeumología demonstrate statistically significant reductions in exacerbation frequency among COPD and chronic bronchitis patients, with reported odds ratios exceeding three versus placebo. These findings are repositioning NAC as a long-term disease management molecule rather than a short-term symptomatic intervention, structurally increasing demand for high-purity, pharma-compliant NAC supply.

Opportunity: Expansion of Cysteine-Derived Chelation Therapies in Environmental and Preventive Health

Rising awareness of heavy metal exposure in water, soil, and food systems is opening a durable growth avenue for cysteine-derived chelators beyond hospital-based toxicology. Succimer (DMSA), a cysteine derivative, remains the frontline oral therapy for pediatric lead poisoning, with recent field evaluations by Médecins Sans Frontières demonstrating average blood lead reductions of approximately 75% following oral treatment courses. This efficacy profile positions DMSA as a scalable alternative to intravenous EDTA, particularly in low-resource settings.

Governments across the Middle East and Southeast Asia are increasingly funding public health research into L-cysteine-enriched supplements and medical foods aimed at mitigating oxidative stress caused by chronic arsenic, mercury, and chromium exposure. These initiatives support the emergence of a preventive health segment within the cysteine market, where long-term supplementation and population-level interventions drive recurring demand rather than episodic clinical use.

Opportunity: Critical Processing and Flavor-Formation Role in Plant-Based Meat Analogues

The rapid scale-up of plant-based meat production is creating a high-value, non-pharmaceutical demand pocket for L-cysteine derivatives. One of the primary technical challenges in meat analogues remains replicating the fibrous texture and mouthfeel of animal muscle. L-cysteine hydrochloride has emerged as a preferred processing aid in high-moisture extrusion systems, where its reducing properties enable controlled manipulation of disulfide bonds in wheat gluten and pea protein matrices. Patent activity during 2024 and 2025 increasingly references cysteine-assisted extrusion to improve protein alignment, elasticity, and shear-induced fiber formation.

Beyond texture, L-cysteine plays a strategic role in clean-label flavor development. As a sulfur-containing amino acid, it acts as a precursor in Maillard reactions, generating characteristic savory notes associated with cooked meat when reacted with reducing sugars. This dual functionality allows plant-based manufacturers to replace artificial flavor systems with functional amino acid inputs, aligning with clean-label positioning while improving sensory authenticity. As alternative protein producers scale globally, this application is expected to materially contribute to incremental demand for food-grade and specialty cysteine derivatives.

L-Cysteine and Derivatives Market Share and Segmentation Insights

L-Cysteine Leads the Market Through Multifunctional Applications Across Food, Pharma, and Personal Care

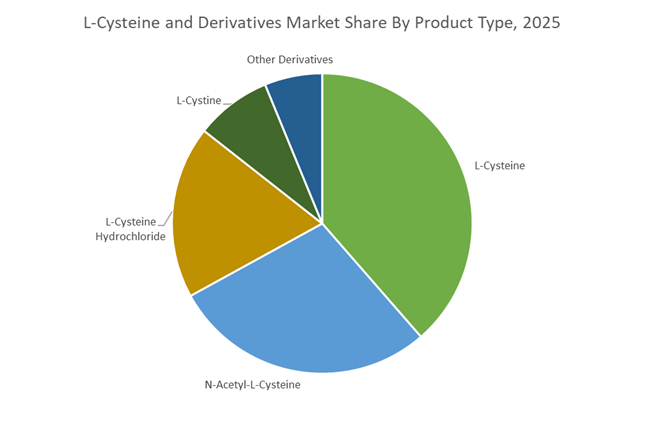

L-Cysteine accounted for 38.60% of the L-Cysteine and Derivatives Market share in 2025, making it the most widely used product type within the amino acid derivatives sector. L-cysteine functions as a core precursor for several downstream derivatives, including N-acetyl-L-cysteine, L-cysteine hydrochloride, and L-cystine, giving it a central role in multiple industrial value chains. The amino acid is widely applied as a dough conditioning agent in bakery products, a flavor precursor in savory food formulations, a reducing agent in cosmetic formulations, and a pharmaceutical intermediate used in mucolytic drugs and antioxidant therapies. Its broad functional versatility supports high production volumes across global food and pharmaceutical industries. In 2025, one of the most significant growth drivers is the clean label reformulation trend in bakery products, where manufacturers increasingly replace synthetic dough conditioners such as azodicarbonamide with naturally derived processing aids. L-cysteine fits well within clean label product development strategies, allowing industrial food manufacturers to maintain dough elasticity and processing efficiency while responding to consumer demand for recognizable and naturally derived ingredients.

Food Processing and Bakery Industry Drives the Largest Consumption of L-Cysteine Derivatives

Food processing and bakery accounted for 42.80% of the L-Cysteine and Derivatives Market share in 2025, establishing it as the largest end-user industry for cysteine-based ingredients. L-cysteine is widely used in industrial baking operations as a dough conditioner and reducing agent, where it improves dough extensibility, reduces mixing time, and enhances machinability during automated production processes. Large-scale bakeries rely on L-cysteine to maintain consistent dough rheology and uniform product quality in high-volume manufacturing of bread, buns, rolls, pastries, and pizza bases. The ingredient enables efficient processing in continuous production lines where dough must be shaped, proofed, and baked at high throughput while maintaining uniform texture and structure. In 2025, global bakery consumption continues to expand alongside urbanization, convenience food demand, and the growing popularity of Western-style baked goods in emerging markets across Asia and Latin America. Despite the growing interest in artisanal bakery products, industrial bakery production remains dominant, sustaining strong demand for functional ingredients like L-cysteine that support scalable and standardized food manufacturing operations.

Competitive Landscape in L-Cysteine and Derivatives Market

Wacker Chemie Leads Fermentation-Based Vegan L-Cysteine Production

Wacker Chemie AG remains the pioneer of fermentation-based L-Cysteine production and is widely recognized as a global benchmark for non-animal-derived amino acids. The company markets its products under the FERMOPURE® brand, delivering plant-based L-Cysteine suitable for vegan food formulations and pharmaceutical-grade applications requiring high purity. In early 2025, Wacker commissioned a new fermentation facility in Burghausen that doubled its food-grade production capacity, and by March 2026 the site began operating AI-controlled fermentation reactors to optimize yield and production efficiency. The company is targeting the clean-label bakery segment in North America and Europe, where L-Cysteine is used as a dough conditioner to improve elasticity, texture, and shelf stability. Wacker is also pursuing a sustainability roadmap targeting a 50% reduction in greenhouse gas emissions by 2030, supported by its bio-based production infrastructure in León, Spain.

Ajinomoto Strengthens Pharmaceutical-Grade Amino Acid Leadership

Ajinomoto Co., Inc. maintains a dominant position in the amino acid technology sector, particularly in high-purity L-Cysteine derivatives used in clinical nutrition and biopharmaceutical manufacturing. Following the integration of Ajinomoto Genexine, the company expanded its global cell culture media portfolio, incorporating L-Cysteine as a key nutrient component for large-scale biologics production. Ajinomoto supplies ultra-pure L-Cysteine for Total Parenteral Nutrition formulations including ELCYS cysteine hydrochloride injection, which has received increased regulatory focus for neonatal medical care. In 2025, the company collaborated with healthcare brands to introduce IronWoman, a dietary supplement combining cysteine with probiotic L-Plantarum and vitamin C to enhance iron absorption in women. Ajinomoto’s strategic pivot toward bioprocessing, pharmaceutical intermediates, and clinical nutrition reflects a deliberate shift away from commodity food-grade cysteine toward higher-margin medical and biotechnology markets.

CJ CheilJedang Expands Fermentation-Based Amino Acid Portfolio

CJ CheilJedang’s CJ Bio division is among the largest global producers of fermentation-derived amino acids, historically serving the animal nutrition industry while increasingly expanding into human nutrition and specialty ingredients. In February 2026, the company signed a major technology licensing agreement with Star Lake Eppen in China to export proprietary microbial strain technology for amino acid production, securing long-term royalty streams while strengthening influence in the Chinese market. CJ manufactures high-volume L-Cysteine derivatives used as flavor precursors in Maillard reaction systems that create meat-like savory profiles for plant-based proteins and processed foods. During late 2025 the company divested its CJ Feed & Care segment to redirect capital toward Green Bio operations and high-purity amino acid products. Recent clinical research on its BiomeNrich™ platform highlights the role of amino acid derivatives such as cysteine in improving gut microbiome balance and livestock productivity.

Evonik Industries Develops Advanced Cysteine Derivatives for Bioprocessing

Evonik Industries focuses on high-value biotechnology applications for L-Cysteine derivatives through its Elective Bio segment. The company markets cQrex® AC, a cystine peptide derivative designed to address stability, oxidation, and solubility limitations associated with conventional L-Cysteine in cell culture media. In 2025 and 2026, Evonik received recognition as a leading bioprocessing supplier for its non-animal-derived amino acid portfolio supporting biopharmaceutical production. The company is building a Global Competence Network for Cell Culture Solutions that integrates research and development capabilities across Asia, Europe, and the Americas. Evonik’s financial outlook for 2026 targets adjusted EBITDA between €1.7 billion and €2.0 billion while implementing a dynamic dividend strategy to maintain capital flexibility. Its focus on advanced amino acid peptides positions the company strongly in biologics manufacturing and next-generation bioprocessing platforms.

Hebei Huayang Biological Technology Strengthens Global NAC Supply

Hebei Huayang Biological Technology represents a critical component of the global L-Cysteine supply chain, particularly in the large-scale production of N-acetyl-L-cysteine and cysteine hydrochloride. Operating from its major production base in Hengshui, Hebei, the company supplies high-volume cysteine derivatives to dietary supplement manufacturers and pharmaceutical distributors worldwide. Its product portfolio includes food-grade and pharmaceutical-grade materials certified under international standards such as USP, EP, and AJI. In 2025 and 2026, Hebei Huayang released extensive 36-month stability data for its NAC batches conforming to AJI92 standards, enabling a three-year retest period that strengthens product reliability for pharmaceutical distribution channels. The company is also enhancing international compliance systems to ensure supply chain traceability and regulatory alignment for exports to North America and Europe, where scrutiny over amino acid sourcing and manufacturing transparency continues to increase.

South Korea L-Cysteine and Derivatives Market: Fermentation-Led Scale-Up and Clean-Label Leadership

South Korea has emerged as a global reference point for fermentation-based L-cysteine production, driven by the strategic repositioning of CJ CheilJedang toward a total-solutions nutrition and biotechnology model. The full operational rollout of CJ Food & Nutrition Technology in 2025 has accelerated the scaling of the Aminature® vegan L-cysteine platform, which relies entirely on non-animal microbial fermentation. This transition directly addresses rising global demand for clean-label, allergen-free, and ethically sourced amino acids ahead of 2026 regulatory and customer audits. Overseas revenue now accounts for nearly half of CJ CheilJedang’s sales, supported by fermentation assets across China, Indonesia, and Brazil, with a new Hungary-based European facility scheduled for commissioning by 2026 to localize derivative supply for EU food and pharma customers.

Operational sustainability is reinforcing competitiveness. CJ’s verified bio-innovation process now recycles over 90% of fermentation byproducts into organic fertilizers, aligning with tightening ESG screening criteria across global food, nutraceutical, and specialty ingredient buyers. Parallel investments in applied nutrition science are expanding addressable end uses. R&D into cysteine–iron bioavailability synergies has intensified following successful launches such as IronWoman, while strong growth in K-Food exports has structurally lifted domestic demand for fermentation-derived flavor enhancers and dough conditioners. In this context, L-cysteine functions as a critical functional ingredient enabling consistent flavor profiles and shelf stability across international retail markets.

Japan L-Cysteine and Derivatives Market: Biopharma Integration and IP-Led Differentiation

Japan’s L-cysteine market is increasingly anchored in high-value biopharmaceutical and advanced food applications, underpinned by proprietary fermentation know-how. Ajinomoto Co., Inc. deepened its biopharma footprint in October 2025 through a licensing agreement with Astellas Pharma Inc., integrating advanced development and manufacturing platforms that utilize ultra-high-purity L-cysteine derivatives in cell culture media. This momentum continued with a November 2025 collaboration with Forge Biologics, where cysteine-enriched supplements are being used to raise productivity in AAV-based gene therapy pipelines entering 2026 clinical stages.

Beyond biopharma, Ajinomoto is reinforcing leadership in fermentation-enabled flavor systems. The June 2025 launch of the Palate Perfect™ platform introduced L-cysteine-based fermentation solutions that replace traditional tomato powder inputs in large-scale food processing, improving cost stability and sensory consistency. At the same time, Ajinomoto’s defensive patent actions across Japan and China in late 2025 highlight the strategic value of its amino acid synthesis IP as competition intensifies. Complementary innovation is emerging in pharmaceuticals, where IFF Pharma Solutions showcased low-nitrite METHOCEL™ systems that leverage cysteine’s antioxidant behavior to mitigate nitrosamine risks in next-generation drug formulations.

United States L-Cysteine and Derivatives Market: Clinical Nutrition and Bio-Manufacturing Pull

In the United States, regulatory scrutiny and bio-manufacturing incentives are shaping demand for pharmaceutical-grade L-cysteine and derivatives. The FDA’s ongoing infant formula nutrient review process, initiated in 2025, has elevated the importance of semi-essential amino acids in neonatal care. This has reinforced clinical reliance on cysteine hydrochloride injections such as ELCYS for newborn total parenteral nutrition, positioning L-cysteine as a compliance-critical input for hospital pharmacies and sterile injectables producers.

Industrial applications are also broadening. Federal bio-manufacturing tax credits scheduled for 2026 are encouraging domestic scale-up of L-cysteine derivatives as PFAS-free surfactants and specialty cleaning agents for semiconductor fabrication and advanced manufacturing. Food safety regulation is another demand lever. The FDA’s January 2025 draft guidance on sanitation for low-moisture foods has accelerated adoption of fermentation-derived cysteine dough conditioners, which offer improved microbial stability versus legacy animal-based sources. Strategic investments are reinforcing the biotech interface, exemplified by Ajinomoto’s June 2025 investment in Somite Therapeutics Inc., where AI-optimized iPS cell differentiation relies on tightly controlled cysteine concentrations.

Germany L-Cysteine and Derivatives Market: Circular Chemistry and Bioprocess Performance

Germany’s L-cysteine market is evolving under circular economy mandates and bioprocess performance requirements. The National Circular Economy Strategy finalized in mid-2025 requires chemical producers to recover and reuse sulfur-bearing compounds, directly impacting amino acid synthesis economics. Evonik is aligning with this framework by integrating recovery pathways for cysteine precursors while expanding high-performance derivatives for life sciences.

Product innovation is tightly coupled to biomanufacturing productivity. Evonik’s 2025 expansion of the cQrex® portfolio with cQrex KC addresses solubility limitations of conventional L-cystine, enabling higher antibody titers in neutral-pH cell culture systems expected to dominate 2026 biologics capacity additions. From a financial perspective, Evonik’s Capital Markets Day outlined a path to €1 billion in additional EBITDA by 2027, with cysteine-based peptides positioned as margin-accretive custom solutions within Nutrition & Care. Parallel integration of green hydrogen into amination precursor production is targeting a 25% reduction in amino acid supply chain emissions by 2027, strengthening supplier qualification for climate-screened pharmaceutical buyers.

L-Cysteine and Derivatives Market: Country-Level Strategic Snapshot

L-Cysteine and Derivatives Market County Level Snapshot

|

Country

|

Strategic Focus Area

|

Primary Demand Driver

|

Structural Impact

|

|

South Korea

|

Fermentation scale and vegan sourcing

|

Clean-label food and nutrition

|

Global volume leadership with ESG alignment

|

|

Japan

|

Biopharma media and IP protection

|

Gene therapy and specialty foods

|

High-margin, technology-protected supply

|

|

United States

|

Clinical nutrition and bio-manufacturing

|

TPN, semiconductors, food safety

|

Regulation-driven quality demand

|

|

Germany

|

Circular chemistry and bioprocess efficiency

|

Biologics and healthcare

|

Premium derivatives with sustainability credentials

|

L-Cysteine and Derivatives Market Report Scope

L-Cysteine and Derivatives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$165.3 Million

|

|

Market Size (2034)

|

$288.9 Million

|

|

Market Growth Rate

|

6.4%

|

|

Segments

|

By Product Type (L-Cysteine, L-Cystine, N-Acetyl-L-Cysteine, L-Cysteine Hydrochloride, Other Derivatives), By Production Method (Microbial Fermentation, Enzymatic Synthesis, Chemical Synthesis), By Grade (Pharmaceutical Grade, Food Grade, Cosmetic Grade, Industrial Grade), By Application (Food and Beverage, Pharmaceuticals, Cosmetics and Personal Care, Dietary Supplements, Animal Feed), By End-User Industry (Pharmaceutical and Biotechnology, Food Processing and Bakery, Nutraceuticals, Personal Care, Animal Nutrition)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

CJ CheilJedang Corporation, Ajinomoto Co., Inc., Evonik Industries AG, Kyowa Hakko Bio Co., Ltd., Grand Hoyo Co., Ltd., Wacker Chemie AG, Hebei Huayang Biological Technology Co., Ltd., Nippon Rika Co., Ltd., Ningbo Zhenhai Haide Amino Acid Co., Ltd., Exela Pharma Sciences, LLC, Donboo Amino Acid Co., Ltd., Zhejiang Pangtong Chemical Co., Ltd., Asahi Kasei Corporation, Merck KGaA

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

L-Cysteine and Derivatives Market Segmentation

By Product Type

- L-Cysteine

- L-Cystine

- N-Acetyl-L-Cysteine

- L-Cysteine Hydrochloride

- Other Derivatives

By Production Method

- Microbial Fermentation

- Enzymatic Synthesis

- Chemical Synthesis

By Grade

- Pharmaceutical Grade

- Food Grade

- Cosmetic Grade

- Industrial Grade

By Application

- Food and Beverage

- Pharmaceuticals

- Cosmetics and Personal Care

- Dietary Supplements

- Animal Feed

By End-User Industry

- Pharmaceutical and Biotechnology

- Food Processing and Bakery

- Nutraceuticals

- Personal Care

- Animal Nutrition

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the L-Cysteine and Derivatives Industry

- CJ CheilJedang Corporation

- Ajinomoto Co., Inc.

- Evonik Industries AG

- Kyowa Hakko Bio Co., Ltd.

- Grand Hoyo Co., Ltd.

- Wacker Chemie AG

- Hebei Huayang Biological Technology Co., Ltd.

- Nippon Rika Co., Ltd.

- Ningbo Zhenhai Haide Amino Acid Co., Ltd.

- Exela Pharma Sciences, LLC

- Donboo Amino Acid Co., Ltd.

- Zhejiang Pangtong Chemical Co., Ltd.

- Asahi Kasei Corporation

- Merck KGaA

*- List not Exhaustive