Laboratory Chemicals Market to Reach $77.3 Billion by 2034 as Life Sciences, Biologics and Semiconductor R&D Accelerate

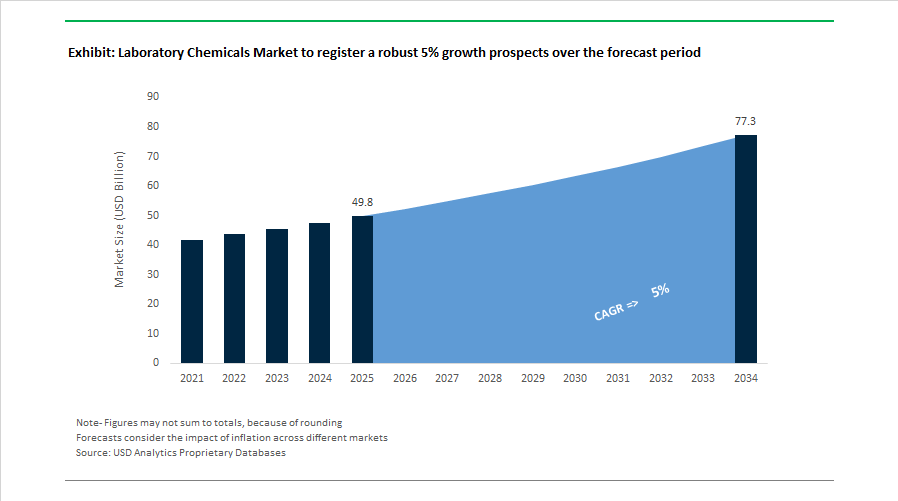

The Laboratory Chemicals Market is projected to grow from $49.8 billion in 2025 to $77.3 billion by 2034, expanding at a CAGR of 5%. Market momentum is being driven by next-generation biologics research, semiconductor materials testing, climate-neutral manufacturing mandates, and increasing automation in research laboratories. Demand is particularly strong for high-purity reagents, chromatography media, analytical standards, molecular biology chemicals, and downstream purification solutions supporting antibody and cell therapy production.

Structural transformation began in October 2024 when Honeywell announced plans to spin off its Advanced Materials business, which includes globally recognized laboratory chemical brands Hydranal® and Fluka®. The spin-off, expected to conclude by early 2026, will create a pure-play specialty chemicals company with approximately $3.8 billion in annual revenue, sharpening focus on analytical reagents and titration chemistries. In parallel, November 2024 saw Avantor open its Bridgewater Innovation Center in New Jersey, a facility dedicated to advanced chemicals and single-use technologies for cell and gene therapy manufacturing. By February 2026, Avantor launched its “Revival” program and relaunched the VWR brand, strengthening digital procurement capabilities for academic and biotech laboratories following a challenging 2025 demand cycle.

Biopharmaceutical innovation is a central growth pillar. In January 2025, Merck KGaA completed the acquisition of HUB Organoids Holding B.V., integrating organoid-specific reagents into its Next-Gen Biology platform for high-throughput drug discovery. In the same month, Merck partnered with Opentrons Labworks to automate biological assays through robotic workstations, enhancing reproducibility and scaling laboratory chemical consumption in automated environments. In October 2025, Merck signed a deal to acquire JSR Life Sciences’ chromatography business, significantly expanding its Protein A purification capabilities for monoclonal antibody production. Further strengthening its manufacturing footprint, Merck inaugurated a €150 million climate-neutral facility in Cork, Ireland in September 2025 dedicated to filters and purification chemicals used in downstream bioprocessing.

Instrumentation-driven reagent demand is also rising. In May 2025, Agilent Technologies launched the InfinityLab Pro iQ Series LC-mass detection platform, engineered for high-resolution impurity profiling in oligonucleotides and peptide therapeutics. During Q3 2025, Agilent reported a rebound in its Chemical and Advanced Materials segment, supported by semiconductor investments that increased uptake of GC, GCMS platforms and ultra-high-purity laboratory solvents. Thermo Fisher Scientific reported full-year 2025 revenue of $44.56 billion in January 2026, a 4% increase year-on-year, with growth tied to life sciences research recovery and registry-based real-world evidence platforms utilizing specialty lab reagents for GLP-1 obesity therapies.

Asia-Pacific is emerging as a key demand center. In January 2025, Shanghai Bid Pharmaceutical acquired Combi-Blocks for $215 million, integrating a vast catalog of laboratory building blocks into its drug discovery and CRO ecosystem. India’s R&D expenditure reached approximately $10 billion in late 2024, expanding at 15% annually, catalyzing domestic growth in molecular biology reagents and analytical chemicals. This regional expansion is reinforcing supply chain localization and driving competition among global laboratory chemical providers.

Strategic Trends and High-Impact Opportunities Transforming the Laboratory Chemicals Market

Trend: Fab-Grade Ultra-High Purity Chemicals Redefine Semiconductor R&D Supply Chains

The laboratory chemicals market is undergoing a decisive upgrade cycle driven by the semiconductor industry’s transition toward sub-3nm logic nodes and Gate-All-Around transistor architectures. Research laboratories supporting advanced chip design are no longer able to rely on conventional analytical- or reagent-grade chemicals. Instead, they are increasingly specifying fab-grade acids, bases, and etchants that approach parts-per-quadrillion impurity thresholds to replicate production-level conditions during early-stage experimentation. This shift is structurally altering supplier qualification criteria, favoring manufacturers with semiconductor-grade purification capabilities, contamination analytics, and traceability systems.

Strategic investments underline the commercial urgency of this trend. In late 2025, BASF Electronic Materials announced plans for a new electronic-grade ammonium hydroxide facility in Ludwigshafen, following its April 2025 investment in high-purity sulfuric acid production designed specifically for Europe’s expanding chip R&D ecosystem. In parallel, Sumitomo Chemical expanded its Iksan Research Laboratory in South Korea in May 2025, adding cleanrooms and process verification lines aimed at ultra-high-purity functional chemicals. These investments align with the move by TSMC toward volume production of 2nm technology in Q4 2025, which is pushing laboratory suppliers to deliver contamination-controlled inputs that reduce yield risks during AI chip prototyping. As a result, laboratory chemicals are increasingly treated as strategic enablers of semiconductor innovation rather than consumable inputs.

Trend: Portfolio Rationalization Accelerates the Shift Toward Integrated Life Science Solutions

Another defining trend in the laboratory chemicals market is the deliberate consolidation of supplier portfolios around high-margin, high-growth life science applications. Leading vendors are actively divesting low-value commodity chemicals and reallocating capital toward bioprocessing, genomics, and advanced cell and gene therapy workflows. This repositioning reflects customer demand for integrated solutions that combine reagents, consumables, instruments, and data infrastructure into a single procurement ecosystem.

In October 2025, Merck KGaA strengthened its downstream bioprocessing footprint by acquiring the chromatography business of JSR Life Sciences, adding Protein A resin technologies critical for monoclonal antibody purification. Similarly, Thermo Fisher Scientific announced the acquisition of Clario Holdings in late 2025 for approximately USD 650 million, integrating clinical trial data platforms into its Laboratory Products and Biopharma Services segment. Financial disclosures from 2024 to 2025 show that such integrated offerings allow suppliers to command pricing premiums of 20 to 30% over standard reagent-grade products. This trend signals a structural move away from transactional reagent sales toward long-term, data-enabled partnerships with pharmaceutical and biotechnology clients.

Opportunity: Lyophilized Reagents and Cartridge-Based Formats Unlock Decentralized Diagnostics

The rapid expansion of point-of-care and decentralized testing models is creating a high-growth opportunity for ready-to-use laboratory chemicals. Lyophilized reagents, pre-aliquoted master mixes, and integrated cartridges are becoming essential as diagnostics move closer to patients, pharmacies, and field settings where cold-chain infrastructure and skilled technicians are limited. These formats reduce handling variability, improve assay reproducibility, and shorten time to result, directly addressing operational bottlenecks in decentralized healthcare delivery.

Research published in RSC Advances in November 2025 demonstrated disposable microfluidic cartridges capable of detecting SARS-CoV-2 antibodies in whole blood within three minutes, integrating sample preparation and reagent mixing into a single passive chip. Industry data from 2025 further indicates a decisive shift toward freeze-dried PCR master mixes, which can be stored and transported at ambient temperatures without performance degradation. This cartridge-based economy benefits suppliers by embedding reagents into proprietary platforms, ensuring recurring demand while enabling smaller clinical labs and retail pharmacies to adopt molecular diagnostics with minimal infrastructure investment.

Opportunity: Bio-Based Solvents Gain Momentum Under Green Lab and Regulatory Mandates

Sustainability-driven procurement is emerging as a durable growth lever for laboratory chemical suppliers, particularly in solvents and process chemicals. Regulatory frameworks such as EU REACH and India’s CMSR, combined with institutional sustainability commitments, are accelerating the replacement of hazardous solvents with bio-derived alternatives. In May 2025, India proposed its National Green Chemistry Mission, signaling long-term policy support for bio-based solvent development and adoption across academic and industrial laboratories.

At the institutional level, Green Lab certification programs such as LEAF and My Green Lab are increasingly influencing purchasing decisions. Universities including the University of Cologne are hosting forums in early 2026 focused on replacing high-risk solvents like dichloromethane with safer options such as 2-methyltetrahydrofuran. Bio-based solvents like cyclopentyl methyl ether are gaining traction due to improved oxidative stability and reduced peroxide formation, offering laboratories a combined safety and efficiency advantage. For suppliers, this shift creates opportunities to align laboratory chemical portfolios with ESG objectives while capturing premium demand from sustainability-driven buyers.

Laboratory Chemicals Market Share and Segmentation Insights

Reagents Lead the Laboratory Chemicals Market Through Critical Role in Analytical and Research Applications

Reagents represented 42.80% of the Laboratory Chemicals Market share in 2025, making them the most widely consumed product category across global laboratory operations. Reagents serve as the fundamental chemicals used in analytical testing, scientific research, diagnostic procedures, and quality control laboratories, supporting a wide range of laboratory techniques including titration, chromatography, spectroscopy, molecular biology assays, and biochemical analysis. Their broad applicability across scientific disciplines ensures consistent demand from pharmaceutical laboratories, academic research institutions, clinical laboratories, and environmental testing facilities. Laboratory reagents are formulated to precise specifications, often requiring high levels of purity, stability, and traceability to ensure accurate experimental results and regulatory compliance. In 2025, technological advances in analytical instrumentation and high-sensitivity testing platforms have increased demand for ultra-high-purity reagents with documented impurity profiles. These specialized reagents are essential in applications such as pharmaceutical quality control, trace environmental contaminant detection, and advanced molecular biology research, where even parts-per-billion impurities can significantly affect analytical outcomes.

Pharmaceutical and Biotechnology Companies Drive the Largest Demand for Laboratory Chemicals

Pharmaceutical and biotechnology companies accounted for 42.80% of the Laboratory Chemicals Market share in 2025, establishing them as the largest end-user group in the industry. These companies rely heavily on laboratory chemicals throughout the entire drug development pipeline, including drug discovery research, analytical testing, formulation development, process optimization, and regulatory quality control. Laboratory chemicals such as analytical reagents, solvents, buffer solutions, catalysts, and reference standards are required in large volumes to support routine testing and research activities in pharmaceutical laboratories. Strict regulatory requirements in pharmaceutical manufacturing also demand high-purity laboratory chemicals with documented quality specifications, traceability, and compliance with international pharmacopeia standards. In 2025, the rapid expansion of biopharmaceutical development, biologics manufacturing, and advanced cell and gene therapies has further increased demand for specialized laboratory chemicals. Research and production of biologics require cell culture media, growth factors, buffer systems, and biochemical reagents, expanding the range of laboratory chemicals used in pharmaceutical and biotechnology laboratories and reinforcing the sector’s leading position in global market consumption.

Competitive Landscape in the Laboratory Chemicals Market

The Laboratory Chemicals Market is highly competitive, driven by global leaders focusing on high-purity reagents, AI-integrated laboratory instrumentation, chromatography chemicals, diagnostic reagents, and automated laboratory workflows. Major companies are strengthening their positions through strategic acquisitions, digital laboratory platforms, automation technologies, sustainable chemical manufacturing, and expanded biopharmaceutical reagent portfolios.

Thermo Fisher Scientific Accelerates AI-Driven Laboratory Chemical Innovation and Biopharma Services

Thermo Fisher Scientific maintains a dominant position in the global laboratory chemicals market by integrating its extensive reagent portfolio with AI-enabled scientific instrumentation and global research distribution networks. In January 2026, the company announced a strategic collaboration with NVIDIA to integrate artificial intelligence into laboratory instrumentation, enabling predictive analysis of chemical interactions and real-time reagent monitoring. Its Laboratory Products and Biopharma Services segment generated $23.98 billion in 2025, supported by a $422 million year-over-year expansion in its research and safety market channel. In early 2026, Thermo Fisher launched new chromogenic culture media for rapid detection of drug-resistant Candida auris, strengthening its clinical microbiology chemical portfolio. A 2025 restructuring initiative generated approximately $500 million in cost savings, while the $3.1 billion acquisition of Clario Holdings further expands its specialty reagents and pharmaceutical clinical research capabilities.

Merck KGaA Strengthens High-Purity Chemical Portfolio Through Structural Transformation and Chromatography Expansion

Merck KGaA, through its Life Science division MilliporeSigma, is reshaping its strategy in the laboratory chemicals industry to support next-generation therapeutic research and biopharmaceutical manufacturing. Effective January 1, 2026, the company reorganized its Life Science business into Process Solutions, Advanced Solutions, and Discovery Solutions, with the Discovery Solutions unit operating as a digital-first platform for laboratory chemical procurement and biological reagents.

In October 2025, Merck signed an agreement to acquire JSR Life Sciences’ chromatography business, significantly expanding its portfolio of Protein A resins and downstream purification chemicals used in monoclonal antibody production. Infrastructure investments include a €150 million climate-neutral filtration facility in Ireland and a €290 million biosafety testing center in Maryland. Additionally, Merck introduced the AAW™ automated workstation in 2025 and secured a 20-year renewable power agreement to support green chemical production in Asia.

Danaher Integrates AI Diagnostics and Advanced Life Sciences Chemistry Through Strategic Acquisitions

Danaher Corporation is strengthening its presence in the life sciences and laboratory chemicals market by combining precision diagnostics, analytical reagents, and advanced instrumentation under the Danaher Business System (DBS) operational model. In February 2026, Danaher announced a definitive agreement to acquire Masimo Corporation for approximately $9.9 billion, integrating advanced sensor technologies and AI-enabled monitoring with its diagnostics platform, which includes chemical analysis solutions from brands such as Beckman Coulter. The company also established a precision medicine partnership with AstraZeneca in May 2025 to develop AI-powered diagnostic platforms and companion diagnostic reagents for pharmaceutical research. To accelerate digital transformation, Danaher appointed its first Chief Technology and AI Officer in late 2025 to oversee predictive analytics integration in laboratory workflows and chemical manufacturing processes. In 2025, the company reported high-single-digit core revenue growth in its diagnostics segment, driven by increasing demand for laboratory testing reagents.

Agilent Technologies Expands Analytical Chemistry Leadership with Digital Pathology and Lab Consumables

Agilent Technologies is strengthening its competitive position in the analytical laboratory chemicals market by focusing on high-purity solvents, chromatography consumables, and diagnostic reagents supporting mass spectrometry and analytical testing. The company reported $1.80 billion in revenue for the first quarter of fiscal 2026, representing 7% year-over-year growth, supported by the Agilent CrossLab Group (ACG) which achieved 9% revenue growth due to strong demand for laboratory consumables and services.

To enhance operational efficiency, Agilent launched a 2025 restructuring program expected to reduce annual costs by $75 million to $80 million, enabling greater R&D investment in life sciences and applied markets. In January 2026, the company introduced the Agilent S540MD Slide Scanner System, integrating high-resolution digital pathology imaging with chemical staining reagents to accelerate clinical diagnostics workflows. Agilent also launched the Instrument Trade-In Impact Award in 2026, encouraging laboratories to adopt chemically efficient analytical instruments that reduce solvent consumption and laboratory waste.

Waters Corporation Drives Chromatography Chemical Demand Through LC-MS Innovation and Strategic Expansion

Waters Corporation continues to expand its influence in the chromatography chemicals and bioseparation reagents market, benefiting from a global laboratory instrument replacement cycle and strong demand for advanced LC-MS analytical technologies. The company reported 12% growth in its Chemistry segment for both Q4 and the full year 2025, outperforming instrument sales and highlighting the strength of recurring revenue from chromatography columns and bioanalytical reagents. In February 2026, Waters completed a transformative combination with BD’s Biosciences & Diagnostic Solutions business, a move expected to add approximately $3 billion in revenue for 2026.

The company also introduced next-generation Microflow LC Columns featuring MaxPeak Premier Technology, designed to deliver higher analytical sensitivity while reducing solvent and sample consumption, aligning with green laboratory initiatives. Additionally, Waters recorded 13% constant currency growth in Asia during 2025, driven by expanding pharmaceutical R&D, biotechnology innovation, and industrial chemical testing across the region.

United States Laboratory Chemicals Market: Domestic Capacity Reinforcement and Portfolio Specialization

The United States laboratory chemicals market is undergoing a structural reset focused on domestic capacity, supply chain resilience, and specialization in high-purity applications. Thermo Fisher Scientific’s $2 billion U.S. manufacturing and R&D investment program for 2025–2028 represents one of the largest recent commitments to laboratory chemicals and instrumentation localization. The opening of the Mebane, North Carolina facility under a $192.5 million HHS and Department of Defense contract has materially strengthened national preparedness by securing automated production of 40 million pipette tips per week. This move directly addresses vulnerabilities exposed during pandemic-era shortages and supports sustained growth in diagnostics, biopharma research, and academic laboratories.

Portfolio optimization is equally reshaping competitive dynamics. Honeywell’s planned spin-off of its Advanced Materials business by early 2026 will position the Hydranal™ Karl Fischer reagents franchise as part of a focused, high-growth specialty chemicals entity aligned with electronic materials and sustainability trends. Parallel investments by Agilent Technologies and AbbVie underline the pull from biopharma and API synthesis, where chromatography reagents, analytical standards, and ultra-high-purity chemicals are mission critical. Innovation is increasingly sustainability-led, as demonstrated by Avantor’s biodegradable detergent development, signaling a shift away from legacy solvent-intensive lab cleaning systems ahead of tighter ESG procurement screening.

India Laboratory Chemicals Market: Regulatory Tightening and Manufacturing Scale-Up

India’s laboratory chemicals market is being reshaped by a combination of fiscal support, regulatory enforcement, and capacity expansion aimed at reducing import dependence. The ₹1,61,965 crore allocation to the Ministry of Chemicals and Fertilizers in the FY 2025–26 Union Budget has created a strong investment signal for specialty and laboratory-grade chemicals. This policy backdrop is complemented by Thermo Fisher Scientific’s commitment at Bioconclave 2025 to establish advanced bioprocess design and customer experience centers in Genome Valley, Hyderabad, embedding global laboratory workflows into India’s life sciences ecosystem.

Domestic consolidation and quality enforcement are accelerating. Sudarshan Chemical’s acquisition of Heubach Group has created a globally integrated platform for pigments and laboratory colorants, while new large-scale assets such as Shivtek Spechemi Industries’ Gujarat facility are scaling specialty output toward 250,000 MTPA by 2027. Critically, the February 2025 rollout of BIS Quality Control Orders covering more than 150 chemical products is raising compliance thresholds for laboratory reagents, benefiting organized manufacturers with validated quality systems and disadvantaging low-cost importers.

China Laboratory Chemicals Market: Electronic-Grade Pivot and Sustainability Alignment

China’s laboratory chemicals sector is increasingly aligned with electronic materials, fine chemicals, and environmental compliance under central industrial policy. The MIIT’s 2025–2026 stabilization plan, targeting 5% annual added-value growth, explicitly prioritizes advanced laboratory reagents for semiconductors, electronics, and high-end manufacturing. This policy direction is visible in the rapid expansion of ultra-high-purity solvent production above 99.9% purity for semiconductor cleaning, supporting the next phase of “Made in China 2025” in 5G and AI infrastructure.

Sustainability and process control are becoming competitive differentiators. BASF’s transition of its Nanjing intermediate and amine portfolio to 100% renewable electricity has reduced the carbon footprint of laboratory reagents supplied across Asia, aligning with multinational customer Scope 3 reduction targets. Environmental compliance capabilities are also being exported, as illustrated by Mitsubishi Chemical Group deploying advanced wastewater treatment technology from Japan into Chinese clusters to meet 2026 discharge standards. These moves collectively signal a shift from volume-led reagent supply to performance- and compliance-driven laboratory chemical production.

Germany and European Union Laboratory Chemicals Market: Regulatory Complexity and Digital Commercialization

The European laboratory chemicals landscape is being reshaped by regulatory tightening and organizational realignment. The ongoing REACH overhaul for 2025–2026, including stricter PFAS assessment frameworks and the addition of DMAC and NEP to Annex XVII restrictions, is forcing laboratories and suppliers to reformulate mixtures and validate safer alternatives before the December 2026 transition deadline. This environment favors suppliers with deep toxicological expertise, substitution pipelines, and regulatory support capabilities.

Strategic restructuring by Merck KGaA illustrates how suppliers are adapting. From January 2026, its Life Science business will operate through Process Solutions, Advanced Solutions, and a digital-first Discovery Solutions unit designed to streamline procurement of laboratory reagents and consumables. With capital expenditure stabilizing at €1.8–€1.9 billion through 2026, the focus is shifting from asset build-out to digital access, compliance readiness, and portfolio depth in biology and chemistry catalog products across the EU.

Laboratory Chemicals Market: Country-Level Strategic Summary

Laboratory Chemicals Market County Level Snapshot

|

Region

|

Strategic Priority

|

Key Structural Shift

|

Market Implication

|

|

United States

|

Supply chain resilience and biopharma pull

|

Large-scale domestic manufacturing and divestitures

|

Higher security of supply for critical lab consumables

|

|

India

|

Import substitution and quality enforcement

|

Budget support, QCOs, and capacity additions

|

Rapid formalization of laboratory chemicals supply

|

|

China

|

Electronic-grade chemicals and sustainability

|

Ultra-high-purity reagents and green operations

|

Performance-driven laboratory reagent demand

|

|

Germany & EU

|

Regulatory tightening and digital access

|

REACH reform and sector reorganization

|

Premium for compliant, digitally accessible suppliers

|

Laboratory Chemicals Market Report Scope

Laboratory Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$49.8 Billion

|

|

Market Size (2034)

|

$77.3 Billion

|

|

Market Growth Rate

|

5%

|

|

Segments

|

By Product Type (Reagents, Solvents, Standards and Reference Materials, Catalysts and Building Blocks, Buffer Solutions, Cell Culture Media), By Grade (ACS Grade, Reagent Grade, USP and EP Grade, Electronic Grade, Chromatography Grade), By Application (Research and Development, Quality Control and Quality Assurance, Clinical Diagnostics, Drug Discovery and Development, Forensic Testing, Environmental Testing), By End-User (Pharmaceutical and Biotechnology Companies, Academic and Government Research Institutes, Healthcare and Diagnostic Centers, Food and Beverage Industry, Environmental and Forensic Laboratories, Industrial Manufacturing)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Thermo Fisher Scientific Inc., Merck KGaA, Avantor, Inc., Agilent Technologies, Inc., Waters Corporation, Shimadzu Corporation, Honeywell International Inc., Revvity, Inc., Bio-Rad Laboratories, Inc., Danaher Corporation, GFS Chemicals, Inc., Mitsubishi Chemical Group, AppliChem GmbH, Lonza Group AG, Spectrum Chemical Mfg. Corp.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Laboratory Chemicals Market Segmentation

By Product Type

- Reagents

- Solvents

- Standards and Reference Materials

- Catalysts and Building Blocks

- Buffer Solutions

- Cell Culture Media

By Grade

- ACS Grade

- Reagent Grade

- USP and EP Grade

- Electronic Grade

- Chromatography Grade

By Application

- Research and Development

- Quality Control and Quality Assurance

- Clinical Diagnostics

- Drug Discovery and Development

- Forensic Testing

- Environmental Testing

By End-User

- Pharmaceutical and Biotechnology Companies

- Academic and Government Research Institutes

- Healthcare and Diagnostic Centers

- Food and Beverage Industry

- Environmental and Forensic Laboratories

- Industrial Manufacturing

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Laboratory Chemicals Industry

- Thermo Fisher Scientific Inc.

- Merck KGaA

- Avantor, Inc.

- Agilent Technologies, Inc.

- Waters Corporation

- Shimadzu Corporation

- Honeywell International Inc.

- Revvity, Inc.

- Bio-Rad Laboratories, Inc.

- Danaher Corporation

- GFS Chemicals, Inc.

- Mitsubishi Chemical Group

- AppliChem GmbH

- Lonza Group AG

- Spectrum Chemical Mfg. Corp.

*- List not Exhaustive