Latex Saturated Paper Market Valuation 2025–2034: Specialty Paper Saturation Technologies Driving $4.7 Billion Outlook at 3.6% CAGR

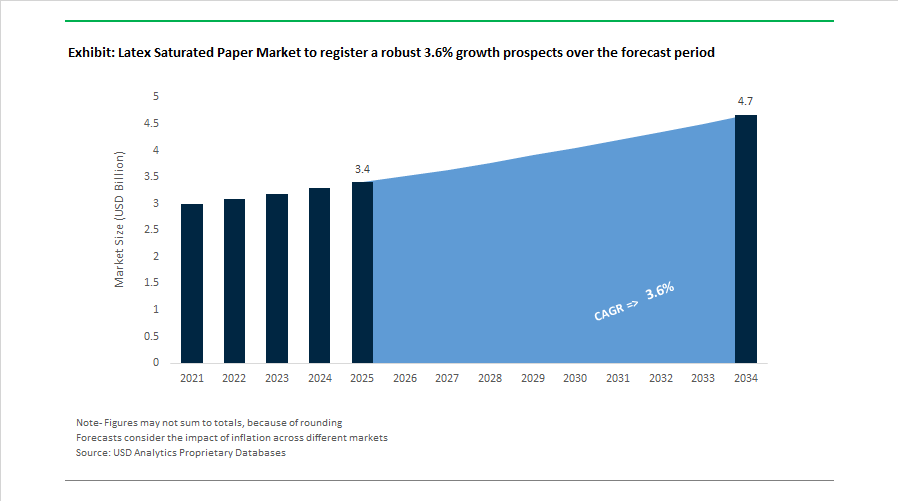

The Latex Saturated Paper Market is projected to grow from $3.4 billion in 2025 to $4.7 billion by 2034, registering a CAGR of 3.6%. Market expansion is being shaped by rising demand for high-performance creped base papers, wet-strength specialty papers, and sustainable fiber-based substrates across automotive tapes, industrial masking, luxury packaging, filtration media, and point-of-purchase signage. Latex saturation technology remains central to enhancing tensile strength, moisture resistance, flexibility, and dimensional stability in technical paper applications where plastic-free performance is required.

In March 2024, Ahlstrom announced capacity expansion for creped base paper production in the United States to support downstream latex saturation converters serving high-end masking tapes and protective spacers. In September 2024, the company initiated a feasibility study to add saturation and release coating capabilities for tape base papers to address growing demand across automotive, aerospace, and construction tape markets in the Americas. These investments underscore strengthening regional integration between base paper production and latex impregnation operations, reinforcing supply chain resilience in specialty tape and industrial adhesive substrates.

Sustainability-linked innovation continues to redefine competitive positioning. In December 2024, Ahlstrom introduced PFAS-free water-repellent filtration media using proprietary saturation processes for air-oil separation in industrial engines and power generation systems. In August 2025, SWM International, now part of Mativ, expanded its Thinpact ESG strategy through diversification of latex-saturated and fiber-based portfolios into marine-biodegradable and botanical-fiber-based materials. In February 2026, Saica Group launched the first adhesive tape manufactured entirely from recycled paper fibers, utilizing advanced saturation techniques to achieve industrial-grade tack and strength while maintaining circularity credentials.

Strategic Trends and High-Value Opportunities in the Latex Saturated Paper Market

Trend: Automotive Interior Materials Shift Toward Sustainable Latex-Saturated Nonwovens

The latex saturated paper market is benefiting from a structural transformation in automotive interior design, where OEMs are moving away from traditional vinyl, PVC, and leather substrates toward engineered fiber-based composites. Modern vehicle cabins are increasingly positioned as mobile offices, increasing demand for interior materials that combine low volatile organic compound emissions, acoustic dampening, thermal comfort, and high-definition printability for backlit panels and decorative trims. Latex-saturated nonwovens meet these requirements by offering dimensional stability, controlled porosity, and compatibility with water-based coatings, making them attractive for next-generation dashboards, door panels, and headliners.

Sustainability compliance is accelerating adoption. In December 2024, Ahlstrom introduced PFAS-free saturated and filtration media with advanced water-repellent properties, directly addressing tightening EU REACH restrictions and U.S. state-level bans on fluorinated chemicals in automotive textiles. Lightweighting mandates further strengthen the business case, with 2025 technical assessments showing that replacing mechanically bonded textiles with latex-saturated nonwovens can reduce interior component weight by up to 15%, a critical advantage for extending battery electric vehicle driving range. At the same time, suppliers such as Freudenberg and Ahlstrom are integrating recycled PET and cellulose blends into saturation lines. In April 2025, fine-filament process innovations improved tensile strength and durability of recycled-content substrates, reinforcing their suitability for long-life automotive interiors.

Trend: Supply Chain Integration and Portfolio Rationalization Reshape Competitive Positioning

The latex saturated paper market is also being reshaped by strategic portfolio rationalization across the chemicals and materials sector. Large producers are exiting commoditized adhesive and polymer segments to concentrate capital and innovation on specialty binder-paper systems where pricing power and customer stickiness are higher. This shift is tightening supplier ecosystems and elevating the strategic importance of latex saturation as a value-added capability rather than a downstream processing step.

In December 2024, Dow completed the sale of its flexible packaging laminating adhesives business to Arkema, allowing Dow to refocus investment on high-value water-based and acrylic binder technologies used in specialty paper applications. Financial disclosures from Trinseo in Q2 2025 highlight a similar strategy, with deliberate reductions in low-margin volumes while CASE applications, including high-performance saturants, delivered resilient growth despite broader market volatility. Vertical integration is becoming a competitive differentiator. In September 2024, Ahlstrom initiated feasibility studies to add direct saturation and release coating capabilities at U.S. production sites, aiming to shorten lead times and improve responsiveness for industrial tape and technical paper customers by consolidating papermaking and saturation under one operational umbrella.

Opportunity: High-Performance Filtration Media for EV Batteries and Industrial Systems

The global shift toward electrification and stricter industrial air quality standards is opening a high-growth opportunity for latex saturated papers in advanced filtration applications. In electric vehicles, the transition toward 800-volt battery architectures and higher energy densities is increasing demand for filtration materials that combine mechanical robustness with chemical resistance and thermal stability. Saturated papers are increasingly specified as reinforcement layers in multi-stage filtration and separator systems, where consistency and durability are critical.

In August 2025, researchers at the Norwegian University of Science and Technology announced the HiSep-II smart filter coating for lithium-sulfur batteries, demonstrating the potential to extend charge cycles from 200 to 1,000. Latex saturated papers are positioned as the structural backbone for such ultra-thin coatings, enabling scalability in large battery packs. Beyond batteries, industrial air and water filtration markets are adopting latex-impregnated papers to meet emerging molecular filtration requirements. The December 2025 launch of Flow2Save and PurXcel filtration media underscored demand for energy-efficient HVAC and water treatment solutions capable of removing VOCs and PFAS. Flame-retardant saturated paper facers introduced in October 2025 further support thermal runaway protection requirements in EV battery enclosures and adjacent building applications.

Opportunity: Bio-Based and Compostable Saturants Enable Circular Packaging Compliance

Regulatory pressure is creating a long-term growth runway for bio-based latex alternatives in packaging-grade saturated papers. The EU Packaging and Packaging Waste Regulation, which entered into force in February 2025, mandates that all packaging placed on the EU market be designed for recycling by 2030. This requirement is accelerating R&D investment into bio-latex systems derived from lignin, starch, and plant oils that preserve paper recyclability while delivering moisture resistance and mechanical strength.

Material innovation is progressing rapidly. In May 2025, Lignin Industries secured €3.9 million to commercialize its patented Renol bio-based thermoplastic, which is being evaluated as a saturant for e-commerce packaging and durable paper applications. These materials offer functional parity with fossil-based plastics while significantly lowering carbon footprints. Market validation is also emerging through consumer-facing products. In October 2025, the launch of the GreenPod Home coffee pod portfolio demonstrated the feasibility of home-compostable saturated paper structures, aligning with EU targets for reusable and compostable takeaway packaging between 2027 and 2028. Together, these developments position bio-based saturants as a strategic growth pillar for suppliers aligned with circular economy objectives.

Latex saturated paper Market Share and Segmentation Insights

Medium-Weight 100–200 gsm Latex Saturated Paper Leads the Market Through Strength and Processing Versatility

Latex saturated paper with a basis weight of 100–200 gsm accounted for 42.80% of the Latex Saturated Paper Market share in 2025, making it the most widely used weight category across industrial applications. Medium-weight saturated papers provide the optimal balance of mechanical strength, flexibility, tear resistance, and processability, which are critical properties for demanding applications such as masking tape backings, abrasive sandpaper backings, gaskets, industrial wipes, and reinforced technical papers. Latex impregnation enhances the structural integrity of paper fibers, improving wet strength, durability, and resistance to mechanical stress, allowing these materials to perform reliably in manufacturing and industrial environments. The 100–200 gsm range delivers sufficient thickness for durability while maintaining the conformability required for coating, printing, lamination, and die-cutting processes used in industrial paper converting. In 2025, manufacturers are also investing in advanced latex polymer formulations that enhance fiber bonding and tensile strength, enabling lightweight saturated papers to achieve comparable performance levels, supporting industry trends toward reduced material usage and improved logistics efficiency.

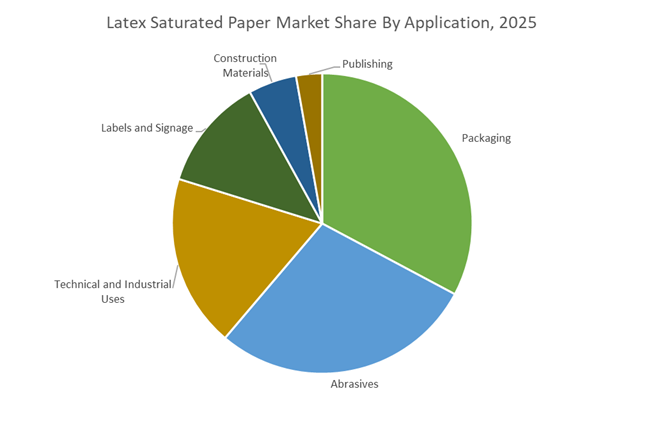

Packaging Applications Drive the Largest Demand for Latex Saturated Paper

Packaging represented 32.80% of the Latex Saturated Paper Market share in 2025, establishing it as the leading application segment for latex saturated paper materials. Latex-saturated papers are widely used in reinforced packaging papers, tape backings, protective wrapping materials, and tamper-evident packaging systems, where high tear resistance and structural durability are essential for protecting goods during transportation and handling. The latex impregnation process enhances the strength, flexibility, and printability of paper substrates, making them suitable for packaging materials that require both mechanical performance and visual branding capabilities. The rapid expansion of global e-commerce logistics and online retail distribution networks continues to increase demand for durable packaging solutions capable of withstanding long-distance shipping and automated handling systems. In 2025, packaging manufacturers increasingly utilize latex saturated papers in reinforced shipping envelopes, security packaging, and branded packaging tapes, where their combination of tear resistance, adhesive compatibility, and printable surface properties supports the evolving requirements of modern e-commerce packaging and supply chain logistics.

Competitive Landscape in the Latex Saturated Paper Market

The Latex Saturated Paper Market is characterized by strong competition among specialty paper manufacturers focusing on high-performance saturated base papers, pressure-sensitive adhesive (PSA) release liners, abrasive backing papers, filtration substrates, and sustainable fiber-based packaging solutions. Key players are strengthening their market positions through strategic acquisitions, advanced latex impregnation technologies, sustainable fiber innovations, and expanded saturation infrastructure.

Ahlstrom Expands Latex Saturated Technical Paper Capacity Through Strategic Acquisition and LamiBak™ Innovation

Ahlstrom continues to strengthen its leadership in the latex saturated paper market through its “Purify and Protect” transformation strategy (2024–2026), focusing on advanced fiber-based specialty materials. In May 2025, the company acquired the Stevens Point operation in the United States, significantly expanding its production capacity for technical saturated papers and pressure-sensitive adhesive (PSA) release liners in North America. Product innovation is highlighted by the launch of LamiBak™ Flex in early 2025, a high-barrier latex-saturated base paper designed for flexible food packaging, featuring a PFAS-free natural grease barrier that enables the replacement of plastic and metallic substrates with 100% recyclable wood pulp materials. Ahlstrom also completed a major saturation and lamination line investment in Brazil in June 2024, strengthening supply for filtration and industrial backing applications. Its sustainability leadership was reinforced by achieving the EcoVadis Platinum rating in 2025, ranking among the top 1% of companies globally.

Mativ Strengthens Polymer-Infused Saturated Fiber Solutions for Industrial Tapes and Filtration Markets

Mativ Holdings, formed through the merger of Neenah and SWM, has emerged as a major innovator in specialty latex-saturated papers and engineered fiber materials for industrial applications. According to its February 2026 earnings report, Mativ generated $1.99 billion in full-year 2025 revenue, with its Sustainable Packaging and Filtration segments driving a 19% increase in Adjusted EBITDA. The company’s core advantage lies in its Digital-to-Analog saturation platforms, enabling precise impregnation of paper fibers with synthetic rubber binders such as SBR and NBR, widely used in automotive gaskets, industrial tapes, and durable bookbinding materials.

In late 2025, Mativ divested its legacy engineered papers business to Evergreen Hill Enterprise, redirecting capital toward latex-saturated release liners for medical and industrial tape markets. The company also launched Neenah Color Capsule™ 2026, a premium saturated design paper engineered for luxury packaging and high-resolution graphic printing applications.

Munksjö Consolidates Global Abrasive Backing Leadership Through Strategic Asset Acquisition

Munksjö has strengthened its competitive position in the global latex saturated abrasive backing paper market through strategic asset expansion and production upgrades. In October 2025, the company completed the acquisition of Ahlstrom’s Abrasives business, reinforcing its leadership in latex-saturated abrasive backings used for precision sanding, automotive refinishing, and industrial grinding applications. To support growing demand in emerging markets, Munksjö launched the ExpanDecor expansion project at its Caieiras facility in Brazil during 2025–2026, which will double the plant’s production capacity for specialty saturated papers serving the South American construction and furniture manufacturing sectors. With 14 advanced paper machines worldwide, the company focuses on highly customized saturated substrates, including ultra-thin high-saturation papers introduced in 2025 that offer superior delamination resistance in wet-sanding environments. Leveraging more than 500 years of papermaking heritage, Munksjö combines renewable raw materials with advanced saturation technologies for both wet and dry industrial applications.

Kimberly-Clark Professional Develops Advanced Saturated Fiber Wipes for Cleanroom and Industrial Applications

Kimberly-Clark Professional (KCP) is expanding its presence in the technical saturated paper and wiping materials market, driven by its “Powering Care” transformation strategy targeting high-performance industrial hygiene solutions. In late 2025, the company entered a strategic joint venture with Suzano for its International Family Care and Professional (IFP) business, leveraging Suzano’s large-scale eucalyptus pulp supply to reduce production costs for base sheets used in latex-saturated technical wipes.

Over the past decade, Kimberly-Clark has invested more than $47 million in alternative fiber research, resulting in the 2025 launch of next-generation biodegradable technical wipes produced through a specialized latex saturation process that eliminates linting while maintaining environmental sustainability. The company also reported a 21% increase in adjusted income from discontinued operations in 2025, reflecting operational restructuring as it progresses toward a 100% natural forest-free product portfolio by 2030.

Stora Enso Accelerates Bio-Based Saturation Technology for Sustainable Technical Papers

Stora Enso is a key innovator in the sustainable latex saturated paper industry, focusing on bio-based fiber materials and plastic-free packaging substrates. The company recently scaled production of its AvantForte WhiteTop kraftliner, a 100% virgin fiber packaging paper designed to meet the durability and sustainability requirements of premium consumer brands seeking plastic-free packaging alternatives.

Between 2024 and 2025, Stora Enso intensified research into lignin-based binders as a replacement for synthetic latex (SBR) in paper saturation, part of its “Carbon-Neutral Saturation” initiative aimed at producing fully bio-based moisture-resistant composite papers. The company has also implemented geospatial traceability across its raw material supply chain to comply with the EU Deforestation Regulation (EUDR) introduced in 2025. Additionally, Stora Enso plans to increase the recycled fiber content of its technical papers to 50% by 2026, while maintaining the structural integrity required for high-performance saturated paper applications.

United States Latex Saturated Paper Market: Performance Materials Driving Industrial and Consumer Adoption

The United States latex saturated paper market is advancing through targeted innovation in technical performance, filtration media, and compliant consumer substrates. Neenah Paper, operating under the Mativ portfolio, strengthened the industrial abrasives segment in 2025 with the launch of DURAFLAT® Fibre. This latex-saturated backing delivers enhanced dimensional stability and curl resistance under high-humidity operating conditions, positioning it as a credible replacement for traditional vulcanized fiber in grinding discs used across metal fabrication and heavy manufacturing. Parallel investments by Ahlstrom at its Taylorville, Illinois site underscore rising demand for saturated filter media. The multi-million-dollar upgrade, scheduled for completion in Q4 2026, integrates advanced saturation and corrugation technologies to support next-generation synthetic and cellulose-blend filtration for industrial air and fluid management systems.

Regulatory alignment and print media diversification are further expanding addressable applications. New Consumer Product Safety Commission rules under 16 CFR part 1218, effective February 21, 2026, are encouraging consumer product manufacturers to adopt latex-saturated substrates due to their low-VOC and non-toxic binding characteristics. In parallel, FiberMark’s Endura-Print range, introduced in late 2025, targets wide-format UV-curable and latex ink printing for eco-oriented signage and display graphics. Macroeconomic tailwinds are reinforcing capital deployment, as post-rate-cut financing conditions in H2 2025 have led U.S. specialty paper producers to project a 12% increase in 2026 capital expenditure to modernize saturation and coating lines.

Germany Latex Saturated Paper Market: Circularity Compliance and PFAS-Free Reformulation

Germany’s latex saturated paper market is being reshaped by regulatory-driven design changes and sustainability-led material science. The EU Packaging and Packaging Waste Regulation, Regulation (EU) 2025/40, fully applicable from August 12, 2026, is compelling German manufacturers to redesign saturated labels and durable papers to meet harmonized recyclability and circularity criteria. This shift is accelerating R&D in mono-material constructions and recyclable latex systems, particularly for pressure-sensitive labels and specialty packaging used in food and consumer goods.

Public investment and chemical compliance pressures are reinforcing this transition. Following the February 2025 constitutional reform easing the debt brake, federal funding for sustainable packaging infrastructure has increased, benefiting innovators such as Paper Earth, which upcycles textile waste into durable saturated papers. Concurrently, alignment with European Chemicals Agency directives for 2025–2026 is pushing producers toward PFAS-free latex emulsions for food-contact applications. Early-stage ventures in Darmstadt, including CeraSleeve, are piloting silica-based additives to replace plastic-heavy barrier layers, aiming for fully recyclable saturated paper products in the 2026 consumer cycle.

India Latex Saturated Paper Market: EPR Enforcement and Retail-Led Volume Growth

India’s latex saturated paper market is entering a structurally important phase driven by regulatory accountability and retail expansion. The Environment Protection Rules introducing Extended Producer Responsibility for packaging, effective April 1, 2026, require brand owners to manage the full lifecycle of paper-based packaging, including latex-saturated formats. This mandate is prompting converters and brand owners to prioritize durable, recyclable saturated papers that reduce material waste while meeting functional performance requirements for moisture resistance and strength.

Demand-side momentum is reinforced by organized retail growth, which is sustaining double-digit expansion through 2026. This trend is driving uptake of latex-saturated Point-of-Purchase displays, promotional posters, and durable signage that can withstand frequent handling and humid store environments. On the supply side, the emergence of pulp and paper innovation hubs in Bangalore and Mumbai has accelerated development of aqueous-coated cups, heat-resistant technical kraft liners, and leak-proof saturated substrates. Additionally, expanded specialty chemical clusters in Gujarat and Tamil Nadu have increased domestic output of SBR and NBR binders, reducing reliance on imported saturation-grade latex by an estimated 15% for the 2026 fiscal year.

China Latex Saturated Paper Market: Industrial Policy Alignment and EV-Focused Applications

China’s latex saturated paper market is increasingly aligned with national industrial policy and advanced manufacturing demand. Under the MIIT-led industrial added value plan for 2025–2026, which targets 5% annual growth, technical papers for electronics and electric vehicle supply chains are prioritized. This policy emphasis is supporting the scaling of latex-impregnated backings for abrasives, insulation layers, and specialty components used in high-precision manufacturing.

Infrastructure and energy transition requirements are broadening application scope. Despite structural adjustments in real estate, continued 6% growth in infrastructure projects during 2025 has sustained demand for moisture-resistant wall coverings and latex-saturated sandpaper backings. The formal inclusion of the paper sector in China’s national carbon market in 2025 is also reshaping operations, with mills required to report Scope 1 and 2 emissions from the 2026 compliance cycle onward. At the application frontier, Chinese manufacturers are deploying latex-saturated paper in lithium-ion battery separators and internal gaskets, leveraging the material’s chemical resistance and thermal stability to support EV component reliability.

Latex Saturated Paper Market: Country-Level Strategic Summary

Latex Saturated Paper Market County Level Snapshot

|

Region

|

Primary Driver

|

Key Strategic Shift

|

Commercial Implication

|

|

United States

|

Industrial performance and compliance

|

Investment in abrasives, filtration, and low-VOC substrates

|

Higher penetration in grinding, filtration, and signage

|

|

Germany

|

Circular economy regulation

|

PFAS-free latex systems and recyclable designs

|

Premium demand for compliant specialty papers

|

|

India

|

EPR enforcement and retail growth

|

Lifecycle accountability and local binder sourcing

|

Volume growth in POP and durable packaging

|

|

China

|

Industrial policy and EV demand

|

Technical paper focus and carbon reporting

|

Expansion into electronics and battery components

|

Latex Saturated Paper Market Report Scope

Latex Saturated Paper Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.4 Billion

|

|

Market Size (2034)

|

$4.7 Billion

|

|

Market Growth Rate

|

3.6%

|

|

Segments

|

By Basis Weight (Below 50 gsm, 50–100 gsm, 100–200 gsm, Above 200 gsm), By Composition (Cellulosic Fibers, Synthetic Fibers, Hybrid Fiber Blends), By Saturating Agent (Styrene Butadiene Rubber Latex, Nitrile Butadiene Rubber Latex, Acrylic Latex, Bio-Based Latex), By Application (Abrasives, Packaging, Labels and Signage, Technical and Industrial Uses, Construction Materials, Publishing), By End-Use Industry (Automotive and Aerospace, Building and Construction, Food and Beverage, Retail and Luxury Goods, Electronics and Electrical)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ahlstrom, Neenah Paper, FiberMark, Monadnock Paper Mills, Mafatlal Industries, Schweitzer-Mauduit International, Lydall, Hollingsworth and Vose, Lantor, Infador, Munksjö Group, Carey Group, Imperial Saturated International, Glatfelter Corporation, Naroflex

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Latex Saturated Paper Market Segmentation

By Basis Weight

- Below 50 gsm

- 50–100 gsm

- 100–200 gsm

- Above 200 gsm

By Composition

- Cellulosic Fibers

- Synthetic Fibers

- Hybrid Fiber Blends

By Saturating Agent

- Styrene Butadiene Rubber Latex

- Nitrile Butadiene Rubber Latex

- Acrylic Latex

- Bio-Based Latex

By Application

- Abrasives

- Packaging

- Labels and Signage

- Technical and Industrial Uses

- Construction Materials

- Publishing

By End-Use Industry

- Automotive and Aerospace

- Building and Construction

- Food and Beverage

- Retail and Luxury Goods

- Electronics and Electrical

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Latex Saturated Paper Market

- Ahlstrom

- Neenah Paper

- FiberMark

- Monadnock Paper Mills

- Mafatlal Industries

- Schweitzer-Mauduit International

- Lydall

- Hollingsworth and Vose

- Lantor

- Infador

- Munksjö Group

- Carey Group

- Imperial Saturated International

- Glatfelter Corporation

- Naroflex

*- List not Exhaustive