Latin America Water Treatment Chemicals Market Outlook

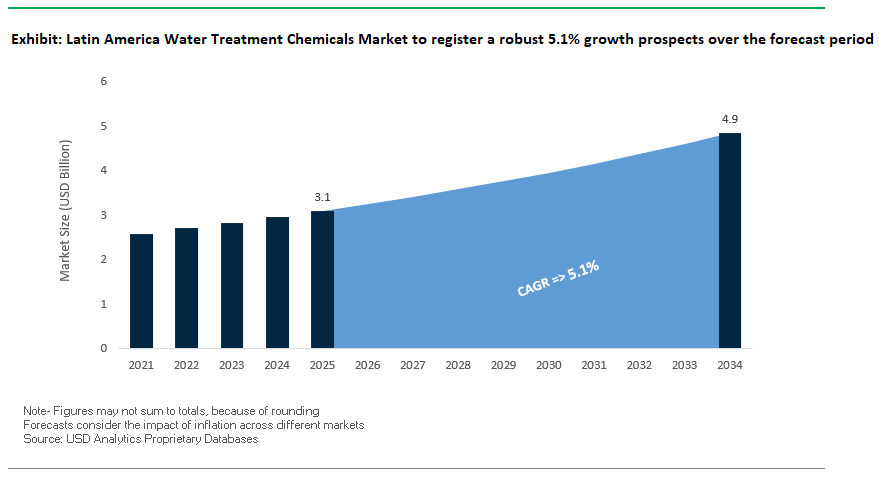

Latin America Water Treatment Chemicals Market Size is estimated at $3.1 Billion in 2025 and is forecast to register an annual growth rate (CAGR) of 5.1% to reach $4.9 Billion by 2034.

The Latin American water treatment chemicals market is influenced by the region’s ecological diversity, complex industries, and increasing urban water stress. This leads to a highly varied demand landscape. The fast-changing market requires region-specific chemical formulations, especially those that support low-sludge, energy-efficient, and resource-recovery-oriented treatment processes.

In the Amazon Basin, water is rich in humic substances and natural organic matter. Utilities increasingly depend on pre-ozonation (1–3 mg/L) to oxidize hard-to-treat organics before coagulation. This approach follows Brazil’s CONAMA 357 standards, which set the conditions and requirements for wastewater discharge and water quality for different receiving bodies. Additionally, bio-based coagulants from local plants like Tamarindus indica (Tamarind) can cut alum demand by up to 40%. This offers advantages in costs and less sludge volume, as demonstrated in studies by Embrapa and other research institutions focused on sustainable alternatives.

In the Andean mining areas of Chile and Peru, acid mine drainage (AMD) and cyanide-laced wastewater create serious environmental risks. Chemical treatment here is intensive and highly regulated. Dosing lime slurry at pH 9.0–10.5 allows for the removal of over 95% of dissolved heavy metals, producing 1.8–3.5 kg/m³ of sludge. This method is common for heavy metal removal in mining wastewater. The SO₂/air process helps break down leftover cyanide to below 0.2 mg/L in gold mining operations, complying with Peru’s MINEM standards, which set environmental quality expectations and allowed limits for mining wastewater.

Urban centers in dry areas like northern Mexico and coastal Peru are increasingly depending on desalinated water due to severe water shortages. Seawater reverse osmosis (SWRO) facilities in these regions use antiscalants at 3–8 ppm to deal with high silica levels (over 250 ppm), common in many coastal water sources. This chemical is crucial for maintaining the efficiency and lifespan of membranes. While NOM-013-SSA1 mainly refers to health and safety standards for hazardous waste facilities, it reflects the broader regulatory context for industrial operations, including water treatment. Specific rules for water quality and discharge in desalination plants may fall under different NOMs or local environmental standards.

Throughout the region, differing regulations since each country has its own environmental laws and standards and climate changes, which can cause unpredictable water availability and quality, are driving innovation in region-specific chemical formulations. Emphasis is increasing on solutions that promote low-sludge production, energy-efficient methods (like advanced oxidation for hard-to-treat wastewater), and resource-recovery treatment, such as extracting nutrients from wastewater. The Latin American market is set for significant growth in water and wastewater treatment due to rising industrialization, urbanization, and a strong commitment to strict government regulations and sustainable practices. Brazil is expected to hold the largest market share in the region, driven by growing environmental awareness and the adoption of better treatment technologies.

Market Trend: Localized Green Chemistry and AI Integration Reshape Water Treatment in Latin America

Latin America’s water treatment chemicals market is undergoing a major change driven by water shortages, environmental regulations, and economic pressures. With 50% of the region at risk of drought (UN 2024) and Brazil’s Novo Marco do Saneamento requiring universal wastewater treatment by 2033, industries and local governments are swiftly adopting bio-based, low-cost substitutes for traditional chemicals. In Brazil, SABESP has implemented acacia-derived tannin coagulants in São Paulo’s water systems, reducing alum usage by 40% and sludge by 30%. Chile’s copper mining industry is moving to lignin flocculants supported by CORFO to achieve 90% water reuse in arid regions. On the digital front, Veolia’s Aquavista™ platform in Mexico uses AI for real-time dosing control, cutting chlorine and antiscalant use in beverage plants by 25%. This combination of green chemistry and smart dosing technologies is changing procurement strategies across sectors especially in municipalities and the food and beverage industry while meeting environmental, social, and governance (ESG) targets and reducing operating costs by up to 50%. Latin America is no longer just keeping pace; it is setting new standards for low-carbon, digitally optimized water treatment solutions.

Market Opportunity: Mining and Agribusiness Water Circularity Unlocks $1B+ in Chemical Demand

The drive for water circularity in Latin America's mining and agribusiness sectors is creating a valuable market for advanced water treatment chemicals. With Chile’s 2024 Water Code enforcing mine water recycling and Argentina’s lithium triangle booming with direct lithium extraction (DLE) projects, the demand for selective antiscalants, chitosan-based coagulants, and high-recovery RO chemicals is rising. Codelco’s Andina mine has pioneered copper recovery from tailings using natural polymers, saving $10 million annually on water costs. Meanwhile, Raízen’s enzyme-based vinasse treatment in Brazil’s sugar industry yields biogas and fertilizer, aligning with circular economy goals. In Colombia, solar-powered electrocoagulation systems are eliminating pesticide residues in coffee wastewater to meet EU export standards. Municipal decentralization adds further momentum. Peru’s Agua Tumbes program and $500 million from the IDB for Caribbean resorts are boosting demand for nanobubble disinfection, PFAS-free coagulants, and biofilm-resistant pipeline cleaners. Coupled with Vale’s $2 billion ESG investment and EU deforestation compliance rules for soy and coffee exports, this trend represents a multi-billion-dollar chance for water chemical suppliers who can offer sector-specific, sustainable, and efficient formulations.

Competitive Analysis- Latin America Water Treatment Chemicals Market

The water treatment chemicals market in Latin America is very fragmented. It features strong multinational players in high-capital sectors, regional champions for public contracts, and numerous small formulators catering to small utilities and agribusinesses. This market structure highlights the region's economic differences and the variety of water-intensive industries like mining, food processing, and power generation. The market is changing rapidly due to regulatory reforms, shifts in global trade, ESG financing, and opportunities in mineral extraction, prompting a shift in competitive strategies.

Tier 1: Multinational Dominance in Strategic Verticals

Global companies like Ecolab (Nalco), Solenis, BASF, and Kemira hold about 45% of the market. They focus on high-barrier industries like mining, automotive, and pulp and paper. These firms stand out by offering technology-driven services such as IoT-enabled monitoring, effective tailings management, and low total cost of ownership chemical programs, combined with strong localization strategies. Ecolab’s acquisition of Brazil’s Hydronan, BASF’s investment in a Monterrey facility, and Solenis’ expansion into Chile’s Antofagasta copper region show how these companies secure long-term contracts and reduce logistical challenges. Additionally, local formulation centers and trade finance capabilities allow them to handle currency fluctuations and comply with various national regulations, particularly in Brazil and Mexico.

Tier 2: Regional Champions Leveraging Policy and Proximity

Regional players like Quimipur (Brazil), PQUISA (Mexico), Dipsa (Argentina), and Procobre (Chile) together capture around 30% of the market. They rely on strong local relationships, specific sector knowledge, and quick responses to public tenders. Their success relies on precise targeting, such as PQUISA’s work with PEMEX standards or Procobre’s alignment with Codelco’s procurement practices, along with cost-sensitive formulations for high-altitude or low-quality water. Many regional champions operate within trading blocs like Mercosur to manage tariffs and raw material import duties, making them cost-effective yet specialized options compared to multinationals.

Tier 3: Fragmented Local Formulators and Undercutting Strategies

The lowest tier includes over 10,000 micro and small enterprises that provide low-cost chemical solutions to rural municipalities, smaller agribusinesses, and decentralized industrial areas. These firms compete by underpricing multinationals by 30% to 50%, though this often comes at the cost of long-term reliability or regulatory compliance. While they lack research and development or digital capabilities, they serve a large, underserved market of price-sensitive clients, particularly outside major cities in Brazil, Argentina, and Colombia. However, between 2025 and 2030, Brazil is expected to reduce its number of local formulators by 30% due to new sanitation laws and enforcement by the national water agency (ANA).

Strategic Battlegrounds and Technology Differentiation

- Different country dynamics are creating tougher competition. Brazil’s sanitation law has sparked a rush for public contracts, with Ecolab and Quimipur leading the way. In Mexico, nearshoring is driving increased industrial water demand, benefiting BASF and local firms like PQUISA. Chile’s mining and lithium growth has positioned Solenis and Procobre as key players, especially in tailings and brine treatment. Argentina is experiencing a surge in oil-and-gas-specific chemical activity, particularly in the Vaca Muerta basin, driven by companies like Dipsa and Kemira.

- Technological advancements are now essential for competition. Companies are customizing formulations for low-TDS Andean waters, using solar-powered dosing systems in remote mines, and providing Spanish and Portuguese-compatible digital dashboards. These innovations focus on delivering effective solutions specific to regional water chemistries, infrastructure challenges, and climate variability.

Regulatory and Financial Arbitrage as Strategic Levers

- Both multinational and regional firms are increasingly taking advantage of regulatory differences to strengthen their positions. In Brazil, compliance with ANA 2024 standards serves as both a barrier and an advantage. In Argentina, companies are adjusting to complex import substitution rules, and in Colombia, businesses utilize Pacific Alliance agreements to increase exports and access favorable financing. Furthermore, ESG-linked financing from organizations like the Inter-American Development Bank (IDB) is transforming procurement by linking water treatment projects to sustainability goals. This trend benefits firms with formal ESG reporting and lifecycle assessment abilities.

Outlook and Competitive Shifts (2025–2035)

- The market is set for major changes. Chile’s plan to build over 20 desalination plants by 2030 will drive demand for specialty antiscalants, membrane cleaners, and reverse osmosis biofouling inhibitors. Chinese companies, such as Sinopec and ChemChina, are expected to aggressively price their offerings, particularly in the mining sector. Additionally, green finance initiatives will favor companies that embrace circular water economy principles, focusing on reuse, recycling, and optimizing resource use.

Latin America Water Treatment Chemicals Market– Segmentation Insights (2025–2034)

By Type of Chemical: Coagulants Lead, Membrane Cleaners Expand Rapidly

In the Latin America water treatment chemicals market, coagulants and flocculants hold the largest share at 35.1% in 2025, driven by widespread use in municipal and industrial water clarification processes. Countries like Brazil, Argentina, and Colombia rely heavily on river water sources such as the Amazon and Paraná, which contain high levels of turbidity and suspended solids. As a result, coagulants especially aluminum sulfate and ferric chloride are critical for ensuring safe drinking water and meeting discharge standards in wastewater treatment plants. Additionally, their use in industrial sectors such as food processing, pulp & paper, and ethanol production reinforces their dominance in the regional chemical mix.

Meanwhile, membrane cleaning chemicals are expected to register the fastest CAGR of 7.5% during the forecast period, propelled by the rising adoption of reverse osmosis (RO) and nanofiltration (NF) technologies across Chile, Mexico, and coastal regions facing water scarcity. These chemicals are vital for maintaining membrane efficiency in desalination plants and industrial RO systems by removing scale, biofilm, and organic fouling. As Latin American nations ramp up investments in sustainable water solutions and water reuse, the demand for effective membrane cleaning agents is set to surge especially in mining-heavy economies and urban coastal hubs with limited freshwater access.

.png)

By Application: Municipal Sector Dominates, Industrial Demand Grows Fastest

By application, the municipal water treatment sector accounts for the largest share at 42.9% in 2025, reflecting ongoing efforts to address chronic water infrastructure deficits across major urban centers in Brazil, Peru, and Colombia. Investment in drinking water purification, sewage treatment, and rural sanitation programs has elevated the use of chemical solutions like chlorine disinfectants, coagulants, and corrosion inhibitors. Regulatory support, including national clean water frameworks and partnerships with international development banks, further anchors municipal chemical demand.

Conversely, the industrial segment is forecast to grow at the fastest CAGR of 6.4% from 2025 to 2034, driven by strong chemical consumption in Latin America’s mining, energy, and ethanol industries. Chile and Peru’s mining operations, which generate large volumes of metal-laden wastewater, require extensive use of pH adjusters, scale inhibitors, and coagulants to meet discharge norms. Meanwhile, Brazil’s sugarcane ethanol plants use water treatment chemicals extensively for boiler feed and process water recycling. The hospitality-led commercial segment also contributes meaningfully, with hotels and resorts in Mexico and the Caribbean adopting cooling water treatment programs to meet hygiene and energy efficiency standards.

Latin America Water Treatment Chemicals Report Scope

Latin America Water Treatment Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.1 Billion

|

|

Market Size (2034)

|

$4.9 Billion

|

|

Market Growth Rate

|

5.1%

|

|

Segments

|

By Type of Chemical (Coagulants and Flocculants, Biocides and Disinfectants, pH Adjusters and Softeners, Scale and Corrosion Inhibitors, Defoamers and Antifoaming Agents, Oxygen Scavengers, Membrane Cleaning Chemicals, Other Specialty Chemicals), By Application (Municipal Water Treatment, Industrial Water Treatment, Commercial Water Treatment), By End-User Industry (Municipal (Water and Sewage Utilities), Industrial), By Form of Chemical (Liquid, Powder/Solid

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ecolab Inc. (U.S.), Solenis LLC (U.S.), Kemira Oyj (Finland), SNF Floerger (France), BASF SE (Germany), Kurita Water Industries Ltd. (Japan), Veolia Water Technologies (France), The Dow Chemical Company (U.S.), Nouryon (The Netherlands), Solvay S.A. (Belgium), Italmatch Chemicals S.p.A. (Italy), Buckman (U.S.),

|

|

Countries

|

Brazil, Mexico, Colombia, Argentina, Chile, Peru

|

Latin America Water Treatment Chemicals Market Segmentation

By Type of Chemical

- Coagulants and Flocculants

- Biocides and Disinfectants

- pH Adjusters and Softeners

- Scale and Corrosion Inhibitors

- Defoamers and Antifoaming Agents

- Oxygen Scavengers

- Membrane Cleaning Chemicals

- Other Specialty Chemicals

By Application

- Municipal Water Treatment

- Drinking Water Treatment

- Municipal Wastewater Treatment

- Industrial Water Treatment

- Cooling Water Treatment

- Boiler Water Treatment

- Process Water Treatment

- Industrial Wastewater Treatment

- Water Reuse and Recycling

- Water Desalination

- Sludge Treatment

- Commercial Water Treatment

By End-User Industry

- Municipal (Water and Sewage Utilities)

- Industrial

- Oil and Gas and Petrochemicals

- Mining and Metallurgy

- Power Generation

- Food and Beverage

- Chemical Manufacturing

- Pulp and Paper

- Pharmaceutical

- Electronics and Semiconductors

- Other Manufacturing Industries

By Form of Chemical

By Country

- Brazil

- Mexico

- Colombia

- Argentina

- Chile

- Peru

- Rest of Latin America

Top Companies in Latin America Water Treatment Chemicals Market

- Ecolab Inc. (U.S.)

- Solenis LLC (U.S.)

- Kemira Oyj (Finland)

- SNF Floerger (France)

- BASF SE (Germany)

- Kurita Water Industries Ltd. (Japan)

- Veolia Water Technologies (France)

- The Dow Chemical Company (U.S.)

- Nouryon (The Netherlands)

- Solvay S.A. (Belgium)

- Italmatch Chemicals S.p.A. (Italy)

- Buckman (U.S.)

* List Not Exhaustive

Research Coverage

The Latin America Water Treatment Chemicals Market Report by USDAnalytics provides an in-depth exploration of the region’s rapidly transforming water treatment sector, influenced by climate variability, resource scarcity, and ESG-driven regulations. The report captures the structural shift toward bio-based chemistries, smart digital dosing systems, and high-performance antiscalants, supported by regulatory frameworks like Brazil’s Novo Marco do Saneamento and Chile’s Water Code reforms.

Scope Includes:

- Segmentation By Type of Chemical: Coagulants & Flocculants, Scale and Corrosion Inhibitors, Biocides, pH Adjusters, Membrane Cleaners, Defoamers, Oxygen Scavengers, Specialty Chemicals

- Segmentation By Application: Municipal Water Treatment (Drinking, Wastewater), Industrial Water Treatment (Cooling, Boiler, Process, Mining), Water Reuse & Desalination, Commercial Water Treatment

- Segmentation By End-User: Municipal Utilities, Mining & Metallurgy, Oil & Gas, Food & Beverage, Chemical Manufacturing, Power Generation, Pulp & Paper, Pharmaceutical, Electronics

- Segmentation By Form: Liquid and Powder/Solid

- Geographic Focus: Major demand hubs include Brazil’s sanitation modernization projects, Chile’s mining belt, Mexico’s desalination zones, and agribusiness clusters across Argentina and Colombia.

- Study Period: Historic: 2021–2024; Forecast: 2025–2034

- Leading Players: Ecolab, Solenis, BASF, Kemira, SNF Floerger, Veolia, Kurita Water Industries, Italmatch Chemicals, Nouryon, Solvay.

Methodology

The report leverages a rigorous research methodology combining primary interviews, regulatory intelligence, and advanced forecasting models:

- Primary Research: Direct engagement with executives from global leaders (e.g., Ecolab, Solenis), Latin American regional players, and municipal water authorities in Brazil, Mexico, and Chile. Insights validated through interviews with process engineers in mining, ethanol, and desalination plants.

- Secondary Research: Examination of government frameworks (e.g., Brazil’s ANA 2024 standards, Chile’s Water Code), Inter-American Development Bank (IDB) financing disclosures, sustainability reports from Tier 1 suppliers, and local procurement databases.

- Market Modeling: Utilization of bottom-up segmental analysis, incorporating capital flows in mining desalination projects, bio-based chemical adoption rates, and PPP-driven municipal upgrades. Forecasting aligned with historical price trends, ESG financing pipelines, and regional drought projections (UN, FAO).

- Validation Framework: Integration of case studies including SABESP’s tannin-based coagulant adoption, Codelco’s lignin flocculants in mining, and Veolia’s AI-driven chemical optimization in Mexican beverage plants. All data verified against regional benchmarks, REACH compliance, and ESG-linked procurement guidelines.

Deliverables

- Complete Market Research Report (PDF, Excel): data tables, market charts, and visual insights.

- Country-Level Forecasts & Analysis

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis

- Recent Developments & News Tracker

- Executive summary and key takeaway slides for boardroom presentations

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements