Explosive Value Growth and Strategic Relevance of the Lithium-Ion Battery Recycling Industry

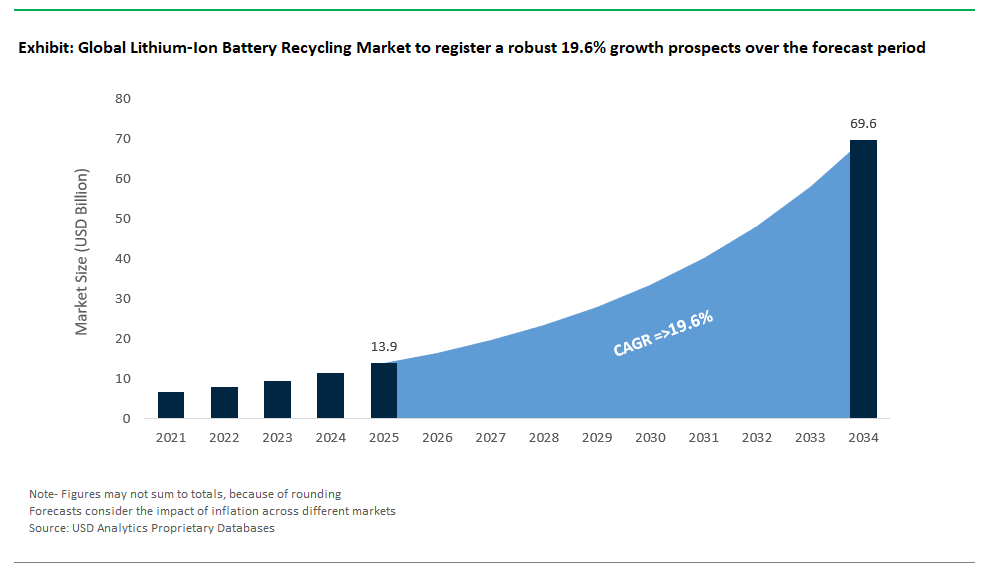

The global lithium-ion battery recycling market is experiencing unprecedented growth, with its value forecast to rise from $13.9 billion in 2025 to an astonishing $69.6 billion by 2034, registering a CAGR of 19.6%. This exponential expansion underscores the sector’s vital role at the intersection of the clean energy transition, sustainable resource management, and global supply chain security. The escalating adoption of electric vehicles (EVs), surging deployment of grid-scale energy storage, and the proliferation of consumer electronics have made efficient lithium-ion battery recycling an absolute necessity for future resource independence and environmental stewardship.

As millions of lithium-ion batteries reach end-of-life, the global recycling industry is fast becoming a linchpin of the circular economy. At its core, the lithium-ion battery recycling process encompasses pyrometallurgical (high-temperature), hydrometallurgical (chemical leaching), and emerging direct recycling technologies, all designed to extract and purify critical metals such as lithium, cobalt, nickel, and manganese. The sector is uniquely positioned to reduce reliance on mining virgin raw materials, mitigate environmental pollution, and address mounting safety and regulatory concerns associated with battery disposal. With new regulatory frameworks coming online and global EV fleets expanding rapidly, the sophistication, capacity, and strategic importance of lithium-ion battery recycling facilities are escalating on every continent.

Global Partnerships and Technological Breakthroughs Redefine Lithium-Ion Battery Recycling Market Dynamics

A surge in strategic investments, global alliances, and cutting-edge technological advancements is transforming the landscape of the lithium-ion battery recycling market. In July 2025, HyProMag USA and Intelligent Lifecycle Solutions (ILS) entered an agreement to leverage ILS’s third-generation magnet separation system, enhancing the separation and pre-processing of rare earth materials in South Carolina and Nevada. Although primarily focused on rare earths, this partnership exemplifies a broader push toward advanced recycling from complex electronic waste, a significant source of lithium-ion battery feedstock.

Similarly, in July 2025, Mkango Resources produced its first recycled rare earth alloy, underscoring the growing technical capability and commercial viability of closed-loop recycling for valuable metals many of which originate from lithium-ion batteries embedded in electronic waste. In the same month, A. O. Smith’s strategic review of opportunities in China, alongside strong boiler sales, reflects shifting industrial energy patterns that could have downstream impacts on battery demand and charging infrastructure worldwide.

Significant investments in Europe and Asia are further accelerating recycling capacity and innovation. Aurubis’s €85 million investment in Belgium (December 2024) integrates an innovative recycling plant aimed at copper and nickel metals vital to lithium-ion battery cathodes demonstrating the synergies between traditional non-ferrous metal recycling and advanced battery recycling. In November 2024, Veolia advanced sustainable copper recovery techniques, signaling an industry-wide drive to implement eco-friendly and highly efficient metal recovery solutions. The momentum extends to India, where Hindalco’s INR 2,000 crore investment in copper and e-waste recycling (August 2023) highlights the integration of battery recycling into broader industrial sustainability strategies.

Strategic partnerships remain key drivers. In February 2024, Cirba Solutions (US) and EcoPro (South Korea) signed an MoU to bolster lithium-ion battery recycling an international effort crucial to securing clean energy supply chains. Regional expansion is also visible in April 2023, as Glencore, FCC Embito, and Iberdrola launched a large-scale battery recycling initiative for Spain and Portugal, addressing supply chain vulnerabilities and regulatory requirements in Southern Europe. Market consolidation is evident in India with Nupur Recyclers’ acquisition of Frank Metals Recyclers (March 2024), strengthening non-ferrous and lithium-ion battery recycling capabilities. Together, these strategic moves illustrate how public and private stakeholders are building a globally resilient, circular supply chain for critical battery materials.

Surging EV End-of-Life Volumes and Technology Innovation Define Key Market Trends and Opportunities

Explosive Growth in End-of-Life EV Batteries Is Reshaping the Recycling Market

A transformative trend in the lithium-ion battery recycling industry is the explosive rise in end-of-life (EOL) batteries from electric vehicles. As EV fleets sold in the early 2010s approach their 8–15 year battery lifespan, the volume of retired batteries entering the recycling stream is skyrocketing. EVs are now projected to represent the fastest-growing source of recyclable lithium-ion batteries. Governments across North America, Europe, and Asia-Pacific are enacting strict battery recycling mandates such as the EU Battery Regulation requiring higher collection rates and improved material recovery. These mandates, coupled with the sheer scale of EV adoption, are driving massive investments in next-generation recycling plants, specialized logistics for battery handling, and novel disassembly and material recovery technologies. As a result, the global lithium-ion battery recycling market is forecast to grow from $1.33 billion in 2020 to $38.21 billion by 2030, driven almost entirely by the surge in EV battery retirements and the pressing need for a closed-loop materials supply.

Opportunity: Hydrometallurgical and Direct Recycling Set New Standards for Sustainability

A key opportunity for the market lies in hydrometallurgical and direct recycling innovations that deliver higher material recovery rates, purer outputs, and lower environmental footprints. Hydrometallurgical processes, which use chemical leaching to extract critical metals, are outpacing pyrometallurgical approaches in both recovery efficiency and sustainability. Companies like Umicore and Li-Cycle are making significant strides in this area, while R&D into deep eutectic solvents and microbe-based leaching continues to unlock new efficiencies. Direct recycling, though less mature, offers the promise of retaining the valuable cathode structure resulting in even lower costs and energy consumption. These advances are crucial for efficiently recycling not only high-value chemistries like NMC (Nickel-Manganese-Cobalt) but also the rapidly expanding Lithium Iron Phosphate (LFP) segment, which dominates stationary energy storage. Continued innovation will enable the development of batteries designed for easy recycling, driving a true circular economy for battery materials and reducing the environmental footprint of the entire energy storage ecosystem.

Industry Leaders and Emerging Innovators: Competitive Landscape of Lithium-Ion Battery Recycling

The competitive landscape of the global lithium-ion battery recycling market features an array of industry titans, innovative technology companies, and integrated recycling groups.

Umicore: Pioneering Comprehensive Closed-Loop Battery Recycling

Umicore stands as a global leader in battery materials technology and recycling, recovering critical metals such as cobalt, nickel, copper, and lithium from a broad spectrum of spent batteries and manufacturing scrap. With its advanced blend of pyrometallurgical and hydrometallurgical technologies, Umicore achieves exceptional recovery rates while maintaining a strong commitment to circular economy principles. Its vertically integrated operations from battery materials production to recycling enable Umicore to supply high-quality, recycled raw materials directly back to battery manufacturers, supporting a sustainable and resilient supply chain.

Li-Cycle: Hydrometallurgical Innovation and Global Spoke & Hub Expansion

Li-Cycle Holdings Corp. is redefining lithium-ion battery recycling with its patented "Spoke & Hub" model. The company’s hydrometallurgical process produces "black mass" at regional spokes, which is further refined at central hubs to yield battery-grade materials. With ongoing expansion in North America, Europe, and Asia, Li-Cycle is rapidly scaling its recycling footprint, delivering high recovery rates for lithium, cobalt, and nickel while minimizing emissions. The company’s focus on localized facilities and partnerships positions it as a critical player in meeting the surging demand for sustainable battery raw materials.

Redwood Materials: Closed-Loop Manufacturing and Strategic U.S. Expansion

Redwood Materials, founded by Tesla’s former CTO JB Straubel, has quickly become synonymous with closed-loop battery recycling in the United States. The company is building large-scale facilities in Nevada and beyond to process end-of-life batteries and manufacturing scrap, recovering and refining lithium, cobalt, nickel, and copper for reuse in new batteries. Redwood’s use of machine learning for process optimization, deep partnerships with automotive OEMs, and focus on localizing the battery supply chain support its goal of reducing U.S. dependence on foreign materials and establishing a robust domestic battery ecosystem.

GEM Co., Ltd.: Urban Mining and Scale Leadership in China

China’s GEM Co., Ltd. is a dominant force in the urban mining sector, with large-scale recycling bases processing over 100,000 tons of batteries annually. By integrating diverse recycling technologies, GEM efficiently recovers cobalt, nickel, and other strategic metals from a wide array of electronic waste and spent batteries. The company plays a central role in China’s circular economy and resource security strategies, ensuring that valuable battery materials are recirculated for new energy applications.

American Battery Technology Company: Domestic Supply Security and Process Innovation

American Battery Technology Company (ABTC) is focused on securing the U.S. supply of battery-grade metals through advanced extraction and recycling technologies. Supported by U.S. Department of Energy loan guarantees, ABTC is building a major recycling facility to process spent batteries and e-waste into high-purity lithium, cobalt, and nickel. The company’s emphasis on process innovation and sustainability is positioning it as a key player in developing a closed-loop, domestic supply chain for critical battery materials.

Source and Recycling Process Shape Global Lithium-Ion Battery Recycling Dynamics

By Source: Electric Vehicles (EVs) Command a Dominant Share in Lithium-Ion Battery Recycling (2025)

In 2025, electric vehicles (EVs) constitute the largest source segment within the global lithium-ion battery recycling market, commanding a substantial 48% share. This leadership is driven by the surging adoption of electric mobility across passenger cars, buses, and two/three-wheelers, which is resulting in large volumes of batteries reaching end-of-life (EOL). The rapid scale-up of EV fleets globally particularly in China, the United States, and Europe has accelerated battery retirement rates, creating a rich feedstock for recyclers and spurring investments in advanced collection and processing infrastructure. Meanwhile, consumer electronics such as smartphones, laptops, and power tools represent the second-largest source, accounting for 22% of the recycling market. However, this segment faces logistical hurdles in efficient collection due to device dispersion and fragmented consumer return behaviors. Energy Storage Systems (ESS), including grid-scale, residential, and industrial installations, are rapidly gaining traction as grid modernization and renewable integration drive significant deployment, thus emerging as a fast-growing source segment for spent lithium-ion batteries. Industrial applications, marine, and medical devices currently hold smaller shares but are projected to gain relevance, propelled by stricter sustainability regulations and an expanding focus on circularity in industrial battery usage worldwide.

.png)

By Recycling Process: Hydrometallurgical Technologies Take the Lead

Hydrometallurgical processes lead the global lithium-ion battery recycling market with a 42% share in 2025, primarily owing to their high recovery rates of critical battery metals such as lithium, cobalt, and nickel. The environmentally superior profile of hydrometallurgy, with its lower emissions and ability to recover metals in high purity, makes it increasingly favored by policymakers and industry leaders especially in China, Europe, and North America. Pyrometallurgical processes follow closely, holding a 35% market share. Pyrometallurgy retains strength due to its robust capability to handle diverse, mixed battery chemistries and its simplicity in scaling, though it faces scrutiny over energy consumption and CO₂ emissions. The direct recycling segment is on the rise as an innovative, cost-effective method, particularly for EV batteries, enabling the re-use of cathode materials with minimal processing, while mechanical/physical pre-treatment remains a vital initial stage covering sorting, shredding, and material separation. Although mechanical methods represent a smaller direct share, they are indispensable as a precursor to chemical recycling, and their importance is expected to grow as automation and AI-driven sorting technologies advance.

China: Policy-Driven Scale and Global Leadership in Lithium-Ion Battery Recycling

China is at the forefront of the global lithium-ion battery recycling market, driven by an unparalleled scale of battery production, consumption, and regulatory intervention. The Chinese government’s “Management Measures for the Recycling and Utilization of New Energy Vehicle Power Batteries” (2024) enforces stringent requirements on all players in the battery value chain, making battery collection, standardized recycling, and clear stakeholder responsibilities a legal obligation. This has catalyzed a wave of infrastructure investments, with companies like GEM and CATL establishing vast recycling bases capable of processing thousands of tons annually. The vast volume of end-of-life (EOL) batteries from China’s surging electric vehicle and consumer electronics sectors is fueling demand for advanced, large-scale recycling operations.

In parallel, China’s aggressive patent activity and technological innovation are reinforcing its global leadership in both hydrometallurgical and pyrometallurgical recycling approaches. Regulatory measures have also tightened standards on imported scrap, incentivizing domestic material recovery and high-quality output. As a result, China’s lithium-ion battery recycling ecosystem is not only meeting domestic circular economy targets but is also setting global benchmarks in process efficiency, environmental compliance, and resource security. These factors position China as a crucial supply base for the world’s clean energy and mobility transition.

United States: Federal Investments and Innovation Powering the Battery Recycling Revolution

The United States lithium-ion battery recycling market is undergoing rapid expansion, propelled by robust federal support and private-sector innovation. Key government initiatives most notably the Bipartisan Infrastructure Law and the Inflation Reduction Act have funneled significant investments into recycling infrastructure, with the Department of Energy allocating $335 million to accelerate the build-out of recycling plants nationwide. These measures are complemented by regulatory pressure to improve collection and responsible end-of-life management, alongside growing consumer and automaker demand for sustainable battery supply chains.

American companies like Redwood Materials are leveraging artificial intelligence and automation to optimize recovery rates and reduce costs, making the U.S. a hub for advanced process innovation. As the U.S. EV market accelerates expected to account for half of all new vehicle sales by 2030 the volume of EOL batteries entering the recycling stream will multiply, fueling further investment. Product innovations are emerging across the value chain, from safer battery collection and logistics to next-generation direct recycling technologies. Altogether, the U.S. is positioned to become a global leader in sustainable lithium-ion battery material recovery and circular manufacturing.

Germany: EU Regulation and Circular Economy Drive Battery Recycling Excellence

Germany stands as a central player in the European lithium-ion battery recycling market, distinguished by its rigorous implementation of EU Battery Regulation. The new EU Battery Law, enforced across Germany, mandates high recycling rate targets and compels manufacturers to take full responsibility for end-of-life battery collection and recycling. This regulatory clarity has attracted continuous investment in state-of-the-art recycling facilities and cutting-edge R&D, with Germany emerging as a hotspot for technological advancement, especially in hydrometallurgical and direct recycling processes.

Germany’s leadership is reinforced through strong cross-border industrial collaborations often involving automakers, recyclers, and chemical companies designed to build a truly circular battery economy across Europe. Major players, such as Umicore (based in Belgium but a key EU participant), are investing in processes that yield ultra-high purity recovered metals, enabling closed-loop supply chains. Germany’s combination of regulatory rigor, technological innovation, and circular economy focus has positioned it as both a policy trendsetter and an industrial powerhouse in global lithium-ion battery recycling.

South Korea: Strategic Partnerships and Technological Edge in Battery Recycling

South Korea has rapidly become a global leader in lithium-ion battery recycling, capitalizing on its dominant position as a battery manufacturing powerhouse. Domestic giants such as LG Chem and Samsung SDI have pioneered closed-loop recycling systems, creating vertically integrated partnerships with recycling specialists to recover critical metals and reintegrate them into battery production. Government policy is increasingly supportive, viewing battery recycling as a national strategic priority and incentivizing technological innovation and industrial investment.

South Korea is also active in global strategic alliances, such as EcoPro’s MoU with Cirba Solutions in the United States, enabling shared technology and expanded access to battery scrap supply. The country’s patent activity in waste battery recycling and focus on process innovation especially in efficiency and safety ensures that Korea’s lithium-ion battery recycling sector remains at the cutting edge. This positions South Korea as both a major supplier of recycled materials and a key node in the international EV and electronics supply chain.

Japan: Mature Recycling Systems and Advanced Material Recovery

Japan’s lithium-ion battery recycling market is characterized by a mature, highly efficient ecosystem developed over decades. Leveraging its legacy as a leader in electronics and automotive manufacturing, Japan has built robust battery collection and waste management systems that emphasize resource efficiency and environmental stewardship. Regulatory policies enforce comprehensive EOL battery collection and recycling, with ongoing government-backed R&D focused on enhancing recovery rates and purity especially for high-value metals such as cobalt and nickel.

Japanese companies such as Sumitomo Metal Mining have pioneered advanced recycling methods, including efficient processes for cobalt recovery, while contributing to global knowledge sharing on urban mining and circular economy practices. Japan’s strong integration of recycled materials back into new battery production, combined with its active participation in global supply chains, ensures its continued influence on sustainable battery lifecycle management worldwide.

Canada: Innovation and Circular Economy at the Core of Battery Recycling Expansion

Canada is emerging as North America’s innovation hub for lithium-ion battery recycling, driven by a combination of federal support for clean technology and proactive industry leadership. Canadian companies like Li-Cycle and Lithion Recycling Inc. are building commercial-scale hydrometallurgical recycling plants that achieve high-purity critical metal recovery and serve the burgeoning U.S. and Canadian EV manufacturing sectors. Federal and provincial initiatives promote circular economy goals, incentivizing both R&D and infrastructure development.

Strategic partnerships with global battery and automotive manufacturers are enabling secure and steady feedstock supplies, while Canada’s regulatory framework for battery stewardship is evolving to support responsible end-of-life management. As North America’s EV market grows, Canada’s ability to deliver sustainable, high-quality recycled materials will become increasingly vital for the continent’s energy transition.

Finland: European Leadership in Lithium Recovery and Sustainable Recycling

Finland’s lithium-ion battery recycling market is recognized for its expertise in advanced material recovery and sustainable process innovation. Homegrown players like Fortum have developed unique technologies for efficient lithium extraction from battery waste, contributing to the European Union’s ambition of creating a closed-loop battery supply chain. National policy emphasizes the circular economy and sustainable resource management, driving investments in both pilot and full-scale recycling facilities.

Finland is fully aligned with EU Battery Regulation requirements, maintaining some of the highest recycling targets globally. The country’s industrial ecosystem supports collaboration between research institutes, recycling companies, and battery manufacturers, making Finland a critical supplier of recovered raw materials for the European battery industry.

Australia: Building a Domestic Battery Recycling Industry from Mining to Circularity

Australia’s lithium-ion battery recycling sector is rapidly evolving, as the country seeks to complement its role as a leading lithium miner with a strong domestic recycling industry. Recent government initiatives support the establishment of local recycling plants and the development of innovative methods to process various battery chemistries efficiently and sustainably. Australia’s focus extends across the value chain, from mining through manufacturing to recycling, aiming to maximize value addition and environmental benefits.

The growing volume of EOL batteries from both electric vehicles and stationary energy storage systems is driving demand for robust collection and recycling systems. As regulatory frameworks are developed to ensure responsible battery disposal and material recovery, Australia is positioning itself as a future leader in the global battery material supply chain, closing the loop from mineral extraction to sustainable recycling.

Lithium-Ion Battery Recycling Market Report Scope

Lithium-Ion Battery Recycling Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$13.9 Billion

|

|

Market Size (2034)

|

$69.6 Billion

|

|

Market Growth Rate

|

19.6%

|

|

Segments

|

By Source (Electric Vehicles (EVs - passenger cars, buses, 2/3 wheelers), Consumer Electronics (smartphones, laptops, tablets, power tools), Energy Storage Systems (ESS - grid-scale, residential, industrial), Industrial Applications (forklifts, AGVs, robotics), Marine, Medical Devices, Manufacturing Scrap (from battery production))

By Battery Chemistry (Lithium Cobalt Oxide (LCO), Lithium Nickel Manganese Cobalt Oxide (NMC), Lithium Iron Phosphate (LFP), Lithium Nickel Cobalt Aluminum Oxide (NCA), Lithium Manganese Oxide (LMO), Lithium Titanate Oxide (LTO), Other Lithium-Ion Chemistries)

By Recycling Process (Hydrometallurgical Process, Pyrometallurgical Process, Direct Recycling, Mechanical/Physical Pre-treatment)

By Recovered Material (Lithium, Cobalt, Nickel, Manganese, Copper, Aluminum, Graphite, Electrolyte, Other materials)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Umicore N.V., Li-Cycle Holdings Corp., Redwood Materials, Inc., GEM Co., Ltd., American Battery Technology Company (ABTC), Ecobat (formerly Johnson Controls Battery Recycling), Fortum Oyj, Brunp Recycling Technology Co., Ltd. (CATL's recycling subsidiary), Raw Material Cycle Co., Ltd. (Japan), SungEel Hi-Tech Co., Ltd. (South Korea), Lithion Recycling Inc., Glencore PLC (in its recycling and trading activities), Accurec Recycling GmbH, Attero Recycling Pvt. Ltd., Cirba Solutions (formerly Retriev Technologies)

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Lithium-Ion Battery Recycling Market Segmentation

By Source

- Electric Vehicles (EVs - passenger cars, buses, 2/3 wheelers)

- Consumer Electronics (smartphones, laptops, tablets, power tools)

- Energy Storage Systems (ESS - grid-scale, residential, industrial)

- Industrial Applications (forklifts, AGVs, robotics)

- Marine

- Medical Devices

- Manufacturing Scrap (from battery production)

By Battery Chemistry

- Lithium Cobalt Oxide (LCO)

- Lithium Nickel Manganese Cobalt Oxide (NMC)

- Lithium Iron Phosphate (LFP)

- Lithium Nickel Cobalt Aluminum Oxide (NCA)

- Lithium Manganese Oxide (LMO)

- Lithium Titanate Oxide (LTO)

- Other Lithium-Ion Chemistries

By Recycling Process

- Hydrometallurgical Process

- Pyrometallurgical Process

- Direct Recycling

- Mechanical/Physical Pre-treatment

By Recovered Material

- Lithium

- Cobalt

- Nickel

- Manganese

- Copper

- Aluminum

- Graphite

- Electrolyte

- Other materials

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Lithium-Ion Battery Recycling Market

- Umicore N.V.

- Li-Cycle Holdings Corp.

- Redwood Materials, Inc.

- GEM Co., Ltd.

- American Battery Technology Company (ABTC)

- Ecobat (formerly Johnson Controls Battery Recycling)

- Fortum Oyj

- Brunp Recycling Technology Co., Ltd. (CATL's recycling subsidiary)

- Raw Material Cycle Co., Ltd. (Japan)

- SungEel Hi-Tech Co., Ltd. (South Korea)

- Lithion Recycling Inc.

- Glencore PLC (in its recycling and trading activities)

- Accurec Recycling GmbH

- Attero Recycling Pvt. Ltd.

- Cirba Solutions (formerly Retriev Technologies)