Low VOC Adhesives Market 2025–2034: Water-Based Technologies, Recyclable PSAs, and Sustainable Construction Driving $140 Billion Outlook at 5.1% CAGR

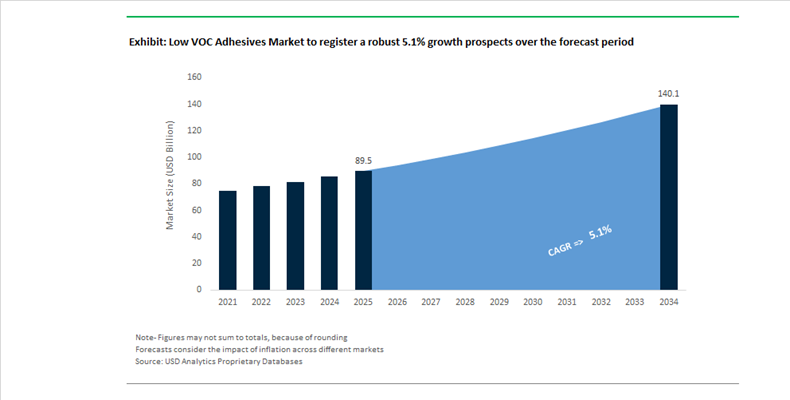

The Low VOC Adhesives Market is projected to grow from $89.5 billion in 2025 to $140 billion by 2034, registering a CAGR of 5.1%. Market expansion is being driven by tightening indoor air quality regulations, green building certifications, automotive cabin emission standards, and food-safe packaging compliance. Water-based adhesives, solvent-free polyurethane systems, low-odor acrylic pressure-sensitive adhesives (PSAs), and bio-based polymer dispersions are increasingly replacing traditional solvent-borne chemistries across construction, packaging, automotive, medical, and electronics applications. Regulatory frameworks targeting volatile organic compound emissions, combined with ESG-linked procurement strategies, are accelerating reformulation across the adhesive value chain.

In February 2024, Wacker Chemie introduced new dispersible polymer powders at PAINTINDIA, enabling very low VOC tile adhesive formulations for India’s rapidly expanding sustainable infrastructure sector. In early 2024, Toyochem launched Oribain EXK 21-046, a low-odor acrylic PSA engineered for enclosed environments such as vehicle interiors and building airspaces where emission control is critical. In May 2024, H.B. Fuller acquired ND Industries, adding Vibra-Tite branded anaerobic, cyanoacrylate, and UV-curable low-VOC adhesives to strengthen its electronics and automotive fastening portfolio. In March 2025, Bostik invested $27 million to expand production of specialty low-emission and bio-based adhesives at its Middleton facility, while Arkema received the American Chemistry Council’s Sustainability Leadership Award for Kynar Aquatec PVDF water-based coatings recognized for reduced lifecycle carbon footprint and low VOC content. In July 2025, Henkel launched Loctite Liofol LA 7837/LA 6265, a solvent-free retort packaging adhesive eliminating energy-intensive drying processes and reducing CO2 emissions in high-thermal food packaging applications.

Strategic acquisitions and digital innovation accelerated in 2025 and early 2026. At Labelexpo Europe 2025, Henkel showcased wash-off and repulpable PSAs such as Aquence PS 3017 RE that enhance PET bottle recyclability while maintaining low-emission compliance. In January 2026, Henkel signed an agreement to acquire ATP Adhesive Systems, expanding its water-based specialty tape portfolio with more than 90% low-VOC technologies serving automotive, medical, and construction markets. In the same month, 3M introduced its “Ask 3M” AI-powered Digital Materials Hub assistant to accelerate discovery of new low-emission adhesive materials under its sustainability-driven operating model. In February 2026, Sika announced the acquisition of Akkim, adding an R&D-driven portfolio of low-VOC construction adhesives and expanding distribution across Eastern Europe, the Middle East, and North Africa, reinforcing the shift toward compliant, high-performance bonding systems in global infrastructure development.

Strategic Trends and High-Impact Opportunities Shaping the Low VOC Adhesives Market

Trend: Furniture and Cabinetry Reformulation Accelerates Under EPA Formaldehyde Enforcement

The low VOC adhesives market is experiencing a structural demand uplift as the furniture and cabinetry sector responds to the full enforcement of the EPA’s TSCA Title VI formaldehyde standards. As of 2024 to 2025, regulated composite wood products such as MDF, particleboard, and hardwood plywood are required to meet stringent emission thresholds, including limits as low as 0.05 ppm for certain plywood categories. These enforceable standards have eliminated the commercial viability of conventional urea formaldehyde resins, forcing manufacturers to reformulate rapidly toward no added formaldehyde and ultra low emitting formaldehyde adhesive systems.

This regulatory shift is reshaping adhesive selection criteria across the value chain. Waterborne polyacetate dispersions and soy based adhesives have emerged as preferred solutions due to their compliance profile and compatibility with high speed furniture assembly lines. Third party certification is reinforcing adoption. To participate in the EPA’s mandatory third party certification program, furniture producers are increasingly securing GREENGUARD Gold and CARB Phase 2 approvals, which are now widely referenced in corporate procurement policies. Industry disclosures indicate that certified compliant products are seeing faster uptake in the United States office furniture market, where ESG driven workplace wellness initiatives are prioritizing indoor air quality. At the supplier level, capital allocation is shifting decisively toward water based synthetic adhesives, which now dominate new capacity additions as solvent based systems are phased out due to their association with respiratory and neurological health risks.

Trend: Bio-Based Polyol Investments Reshape High-Performance PUR Adhesive Portfolios

A second defining trend in the low VOC adhesives market is the strategic pivot toward bio based polyols as feedstocks for reactive polyurethane hot melt systems. Chemical producers are actively decoupling from petroleum based supply chains by scaling renewable polyols derived from soy, castor oil, and sugar. These materials enable the production of high performance PUR adhesives that deliver strong structural bonds with negligible VOC emissions, aligning sustainability objectives with manufacturing efficiency.

By 2024, global consumption of bio polyols reached a notable inflection point, with soy based polyols accounting for more than 45% of total volume. North America represents a major demand center, supported by the EPA BioPreferred program, which has accelerated adoption across furniture, electronics, and construction applications. Product innovation is reinforcing momentum. In April 2025, Tex Year introduced the R3220 bio based PUR hot melt adhesive containing 40% renewable content. Designed for electronics and furniture assembly, the system combines rapid curing and high initial strength with compliance to DIN and USDA green certification criteria. Beyond sustainability, these reactive PUR systems offer tangible operational benefits. Lower application temperatures, often below 100 degrees Celsius, reduce energy consumption and enable bonding of thermally sensitive substrates that would be damaged by traditional solvent based curing processes.

Opportunity: Low VOC Structural Adhesives for Electric Vehicle Battery Pack Assembly

The rapid global expansion of electric vehicle manufacturing is creating a high value opportunity for low VOC adhesives engineered for extreme thermal and mechanical environments. With more than 14 million electric cars registered globally in 2023, automakers are increasingly relying on structural adhesives to replace mechanical fasteners in battery packs and vehicle chassis. These adhesive systems must deliver high bond strength, thermal conductivity, and fire resistance while emitting minimal volatile compounds to avoid gas accumulation in sealed battery enclosures.

Product innovation is advancing quickly. In late 2024, Henkel Adhesive Technologies launched Loctite TLB 9300 APSi, an injectable thermally conductive adhesive designed for EV battery systems. The formulation integrates structural bonding with efficient heat dissipation to cooling plates, supporting battery longevity and safety while maintaining a low VOC profile. Automakers including Ford and Tesla now use structural adhesives in close to 80% of EV chassis bonding operations, enabling significant lightweighting. Industry benchmarks suggest that a 10% reduction in vehicle weight can improve energy efficiency by 6 to 8%. Safety requirements are also tightening. In the second quarter of 2025, suppliers such as Bostik and DuPont introduced low VOC, fire resistant adhesive systems tailored for high voltage LFP and emerging solid state battery architectures.

Opportunity: Low VOC Pressure Sensitive Adhesives for Recyclable E-Commerce Packaging

The convergence of e commerce growth and circular economy mandates is opening a significant opportunity for low VOC pressure sensitive adhesives in packaging. Brand owners and converters are accelerating the transition toward mono material and paper based packaging formats that can be easily recycled, creating strong demand for water based PSAs that do not contaminate recycling streams or emit harmful solvents.

Innovation in this space is gaining regulatory and commercial validation. In July 2025, UFlex Limited received a patent for its waterborne heat seal coating composition designed to enable full paperization of flexible packaging. These coatings eliminate the need for plastic laminated films, allowing finished packages to be processed in conventional paper recycling facilities. At the same time, packaging leaders such as Mondi Group and Amcor launched fully recyclable polyethylene and polypropylene mono material films in 2025. These systems rely on low VOC, high clarity adhesives that preserve package integrity while keeping all components within a single polymer family. Driven by the EU Green Deal, water based PSAs now represent roughly one third of the high performance adhesive technology segment, positioning them as a cornerstone of recyclable, direct to consumer packaging strategies aligned with 2030 sustainability targets.

Low VOC Adhesives Market Share and Segmentation Insights

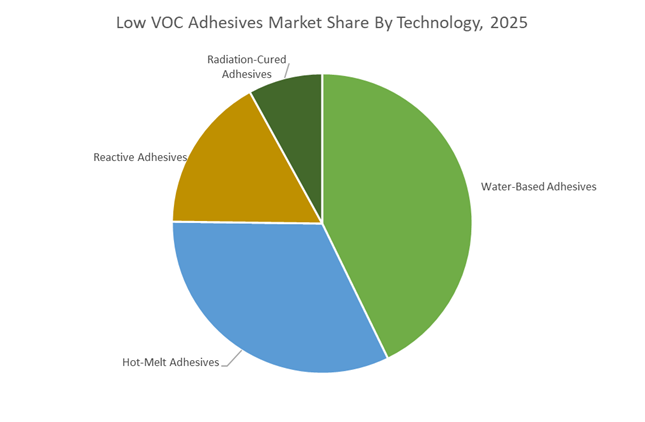

Water-Based Adhesive Technology Leads Low VOC Adhesives Market Through Regulatory Compliance and Performance Advancements

Water-based adhesives accounted for 42.80% of the Low VOC Adhesives Market share in 2025, making them the leading technology used in environmentally compliant adhesive formulations. Water-based adhesive systems are widely adopted because they significantly reduce volatile organic compound (VOC) emissions compared with traditional solvent-based adhesives while maintaining reliable bonding performance. These adhesives are extensively used across packaging, construction materials, woodworking, and industrial assembly applications, where manufacturers must meet increasingly strict environmental and workplace safety regulations. Water-based adhesive formulations offer advantages including low toxicity, reduced flammability, simplified regulatory compliance, and compatibility with existing application equipment, which has accelerated their adoption in high-volume manufacturing environments. In 2025, advances in polymer dispersion technology and hybrid latex formulations have enabled water-based adhesives to achieve bond strength, heat resistance, and moisture durability comparable to solvent-based systems. These improvements have allowed manufacturers to replace solvent adhesives in demanding industrial applications while maintaining production efficiency and consistent product performance.

Packaging Industry Drives the Largest Demand for Low VOC Adhesives in Sustainable Packaging Systems

Packaging applications accounted for 38.60% of the Low VOC Adhesives Market share in 2025, positioning the packaging sector as the largest consumer of environmentally compliant adhesive technologies. Adhesives are essential for corrugated box sealing, carton closing, label attachment, flexible packaging lamination, and case sealing operations, making them critical components in modern packaging production lines. The large-scale growth of food packaging, e-commerce shipping materials, and consumer goods packaging continues to drive high-volume adhesive consumption globally. Packaging manufacturers increasingly prefer low VOC adhesive formulations to comply with environmental regulations and meet sustainability commitments from major consumer brands and retailers. In 2025, a major innovation focus within the packaging sector is the development of adhesives compatible with recyclable packaging materials. Low VOC adhesive systems are being engineered to support repulpable paper packaging, removable label adhesives, and recycling-friendly bonding systems, ensuring that adhesives do not contaminate recycling streams while maintaining the strong bonding performance required for high-speed packaging operations.

Low VOC Adhesives Market Competitive Landscape

The low VOC adhesives market in 2026 is driven by water-based specialty tapes, solvent-free polymer systems, and bio-based feedstocks aligned with PPWR and SCAQMD regulations. Competition is intensifying around carbon transparency, circular adhesive chemistries, and high-performance bonding solutions for EV assembly, green buildings, and sustainable packaging.

Henkel scales water-based and silane-modified adhesive platforms for sustainable bonding ecosystems

Henkel AG & Co. KGaA is expanding beyond traditional adhesives into integrated low-VOC bonding systems through the acquisition of ATP Adhesive Systems, where over 90% of products are water-based and low-carbon. Its Loctite MS 9650 silane-modified polymer adhesive eliminates silicone and isocyanates, supporting lightweight automotive assembly with improved safety. Bio-based construction adhesives further strengthen its green building portfolio, while integration capabilities across tapes and liquid systems position Henkel as a full-spectrum bonding solutions provider for automotive, electronics, and medical applications.

H.B. Fuller drives low-emission innovation with ECO-driven technologies and construction expansion

H.B. Fuller Company is reinforcing its leadership in sustainable adhesives through ECO 2 Driven™ technology, eliminating chemical blowing agents in roofing adhesives while maintaining performance. Strategic acquisitions in building materials and a $50 million allocation toward manufacturing optimization enhance efficiency of low-VOC product lines. With EBITDA of $621 million and a 2026 target of $660 million, the company is scaling compostable, migration-safe, and solvent-free adhesives across construction, packaging, and hygiene sectors.

Sika integrates digital construction and low-VOC adhesives for infrastructure decarbonization

Sika AG is leveraging its “Fast Forward” strategy to combine digitalization with advanced low-emission adhesive systems tailored for green construction and infrastructure projects. Investments of CHF 120–150 million are accelerating innovation, while EBITDA margins approaching 20% reflect strong operational execution. Measurable reductions in Scope 1 and 2 emissions and integration with sensor-based construction technologies enable optimized curing and performance of low-VOC sealants in large-scale infrastructure and EV-related applications.

Arkema strengthens bio-based adhesive innovation through Bostik’s global platform

Arkema, through Bostik, is expanding its low VOC adhesive portfolio by integrating advanced polymer technologies and bio-based raw materials. Acquisition of specialty adhesive developers enhances capabilities in façade bonding and construction applications. With €2.7 billion in sales and a presence in over 50 countries, Bostik is scaling “smart adhesives” for EV battery assembly and flooring systems. Vertical integration within Arkema ensures access to sustainable monomers, supporting high-performance, low-emission pressure-sensitive and structural adhesives.

MAPEI advances ultra-low VOC construction adhesives with carbon-neutral product lines

MAPEI S.p.A. is differentiating through its Zero Line portfolio, combining EC1 Plus-certified low-VOC adhesives with fully offset lifecycle emissions. Products such as Ultrabond Eco V4 Evolution Zero and Ultraplan Eco 3215 Zero deliver rapid curing and high durability while maintaining strict indoor air quality standards. Its use of LCA methodologies and EPDs ensures full transparency in carbon and VOC metrics, positioning MAPEI as a preferred partner for sustainable construction and certification-driven projects.

3M develops compliant low-VOC adhesive systems for industrial and high-tech applications

3M Company is aligning its adhesives portfolio with stringent VOC regulations through hybrid polymer technologies and high-solids formulations. Products like 3M™ Hi-Strength 90 CA Spray Adhesive (<25% VOC) meet GREENGUARD® and SCAQMD standards while delivering strong bonding performance. Strategic regulatory compliance measures and investments in EBO production for AI data centers highlight its expansion into high-tech applications, where low-outgassing adhesives are critical for protecting sensitive electronic and optical components.

United States: Regulatory Flexibility Driving Reformulation and Capital Reallocation

The United States low VOC adhesives market is entering a recalibration phase shaped by regulatory sequencing and targeted capital deployment. In July 2025, the U.S. Environmental Protection Agency finalized an interim rule extending the compliance deadline for stricter VOC emission limits on aerosol coatings and adhesives from July 2025 to January 17, 2027. This 18-month extension has materially altered reformulation timelines, allowing adhesive manufacturers to optimize raw material sourcing, qualify alternative polymers, and reconfigure production lines without immediate regulatory disruption. Rather than delaying action, most U.S. producers are using this window to accelerate the transition toward solvent-free, water-based, and reactive systems that are structurally aligned with post-2027 enforcement.

Capital expenditure patterns underscore this shift. During its October 2025 Investor Day, H.B. Fuller outlined a strategy centered on high-margin, tech-enabled adhesive segments, with low-emission and solvent-free chemistries at the core of its growth agenda. Parallel innovation is visible in industrial bonding, where Henkel introduced Technomelt PUR 6260 ECO in November 2025. This bio-based polyurethane hot melt contains 60% renewable content and delivers a 40% lower carbon footprint, making it particularly relevant for automotive interiors and durable goods manufacturing. Additionally, U.S. R&D investments during 2025 increasingly targeted circular economy adhesive platforms that enable controlled debonding of automotive components, a capability aligned with 2026 vehicle recyclability mandates.

China: Policy-Led Shift from Volume Chemistry to Integrated Green Adhesive Solutions

China’s low VOC adhesives market is being reshaped by industrial policy that prioritizes quality, emissions reduction, and system-level solutions. The Ministry of Industry and Information Technology released its September 2025 Work Plan for Stabilizing Growth, targeting more than 5% annual growth in the petrochemical and chemical sectors while explicitly prioritizing high-end specialty chemicals, including low VOC adhesives and coatings. Importantly, the plan mandates measurable pollution and carbon reductions, pushing traditional adhesive suppliers away from commodity solvent systems toward integrated green solutions for construction, automotive, and electronics applications.

Supply chain localization is a defining theme. Beijing’s 2026 strategy for electronic chemicals has accelerated domestic capacity for UV-curable and water-based adhesives used in semiconductor packaging and display manufacturing, reducing reliance on imported solvent-based products. At the same time, China’s chemical park modernization program is incentivizing the deployment of AI-enabled process optimization under the “AI + Petrochemicals” framework. For low VOC adhesive producers, this translates into tighter process control, lower VOC leakage, and improved consistency in polymer synthesis, strengthening China’s position as both a large consumption market and a competitive export base for compliant adhesive technologies.

Germany: Bio-Based Innovation and Energy-Efficient Bonding as Competitive Levers

Germany continues to set the technical and regulatory benchmark for low VOC adhesives in Europe, driven by occupational safety rules, energy efficiency targets, and bio-based material adoption. At LIGNA 2025, Jowat SE introduced Jowacoll GROW 125.00, a surface adhesive formulated with 30% bio-based content under ISO 16620-4. The product allows furniture and interior manufacturers to meet renewable material quotas without modifying existing processing equipment, a key adoption enabler for mid-scale producers.

Regulatory compliance has further accelerated innovation. German manufacturers are leading the shift toward PUR hot melts with diisocyanate content below 0.1% by weight, in line with EU safety restrictions enforced during 2024–2025. This transition eliminates hazardous material labeling while preserving performance in structural bonding. Energy efficiency is another differentiator. New hot melt systems commercialized in late 2025 operate at processing temperatures as low as 99°C, enabling packaging converters to cut bonding-related energy consumption by up to 45%. In parallel, Henkel expanded its Thin Organic Coating portfolio in December 2025, integrating low-emission aesthetic finishes for metal surfaces that combine corrosion protection with reduced VOC levels.

India: Policy-Backed Ecosystem Development for Solvent-Free Adhesives

India’s low VOC adhesives market is transitioning from fragmented growth to ecosystem-level development, anchored by industrial policy and infrastructure creation. The Indian government increased the allocation under the Production-Linked Incentive scheme by 76% to ₹19,500 crore in the FY2025–26 budget, with a clear emphasis on specialty chemicals and technical textiles. Low VOC adhesives, particularly solvent-free lamination systems for flexible packaging, are direct beneficiaries of this funding focus as domestic converters seek to meet global brand sustainability requirements.

Strategically, the NITI Aayog 2025 roadmap outlines the creation of world-class chemical hubs aimed at doubling India’s share of the global chemical value chain by 2030. These hubs are being designed with shared utilities, effluent treatment, and testing infrastructure, lowering entry barriers for small and mid-sized adhesive formulators. The introduction of a dedicated Chemical Fund in 2025 further supports this transition by financing green manufacturing upgrades, enabling Indian producers to adopt water-based, reactive, and hot-melt adhesive technologies at scale.

Switzerland: Global Sustainability Governance and Low-VOC System Leadership

Switzerland’s influence on the low VOC adhesives market is global rather than purely domestic, anchored by multinational innovation and governance standards. In March 2025, Sika AG, in collaboration with BASF, launched a next-generation epoxy hardener that reduces VOC emissions by up to 90% compared with conventional systems. This development enables high-gloss flooring and construction applications in sensitive indoor environments such as hospitals and schools, where air quality regulations are most stringent.

Governance and disclosure are equally influential. In late 2025, Sika confirmed full alignment with the EU Corporate Sustainability Reporting Directive by 2026, committing to granular disclosure of VOC content across its global adhesive and sealant portfolio. This level of transparency is setting a de facto benchmark for multinational adhesive suppliers, reinforcing Switzerland’s role as a standards-setter in low VOC adhesive compliance and sustainability reporting.

Low VOC Adhesives Market: Country-Level Strategic Snapshot

Low VOC Adhesives Market County Level Snapshot

|

Country

|

Primary Policy or Market Driver

|

Strategic Industry Response

|

Implication for Low VOC Adhesives

|

|

United States

|

Extended EPA compliance timeline

|

Accelerated reformulation and circular R&D

|

Shift toward solvent-free and debondable systems

|

|

China

|

MIIT growth and pollution mandates

|

Localization and AI-enabled production

|

Expansion of water-based and UV-curable adhesives

|

|

Germany

|

EU safety and energy efficiency rules

|

Bio-based, low-temperature bonding

|

Premium, regulation-ready adhesive solutions

|

|

India

|

PLI expansion and chemical hubs

|

Ecosystem development for green manufacturing

|

Rapid scale-up of solvent-free lamination

|

|

Switzerland

|

Global sustainability governance

|

Ultra-low VOC system innovation

|

Benchmarking for global compliance and reporting

|

Low VOC Adhesives Market Report Scope

Low VOC Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$89.5 Billion

|

|

Market Size (2034)

|

$140 Billion

|

|

Market Growth Rate

|

5.1%

|

|

Segments

|

By Technology (Water-Based Adhesives, Hot-Melt Adhesives, Reactive Adhesives, Radiation-Cured Adhesives), By Composition (Polyurethane, Epoxy, Acrylic, Vinyl Acetate Ethylene), By Application (Construction, Packaging, Automotive and Transportation, Woodworking and Furniture, Consumer and DIY, Footwear and Leather), By End-Use Industry (Residential and Commercial Building, Food and Beverage Packaging, Automotive Manufacturing, Medical and Healthcare, Electronics and Electrical)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel, H.B. Fuller, Sika, Arkema, 3M, Jowat, Illinois Tool Works, Huntsman Corporation, Wacker Chemie, Pidilite Industries, MAPEI, Dow, BASF, RPM International, Nan Pao Resins Chemical

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Low VOC Adhesives Market Segmentation

By Technology

- Water-Based Adhesives

- Hot-Melt Adhesives

- Reactive Adhesives

- Radiation-Cured Adhesives

By Composition

- Polyurethane

- Epoxy

- Acrylic

- Vinyl Acetate Ethylene

By Application

- Construction

- Packaging

- Automotive and Transportation

- Woodworking and Furniture

- Consumer and DIY

- Footwear and Leather

By End-Use Industry

- Residential and Commercial Building

- Food and Beverage Packaging

- Automotive Manufacturing

- Medical and Healthcare

- Electronics and Electrical

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Low VOC Adhesives Market

- Henkel

- H.B. Fuller

- Sika

- Arkema

- 3M

- Jowat

- Illinois Tool Works

- Huntsman Corporation

- Wacker Chemie

- Pidilite Industries

- MAPEI

- Dow

- BASF

- RPM International

- Nan Pao Resins Chemical

*- List not Exhaustive