Global Lubricant Packaging Market Outlook: Size, Growth Rate, and Key Insights

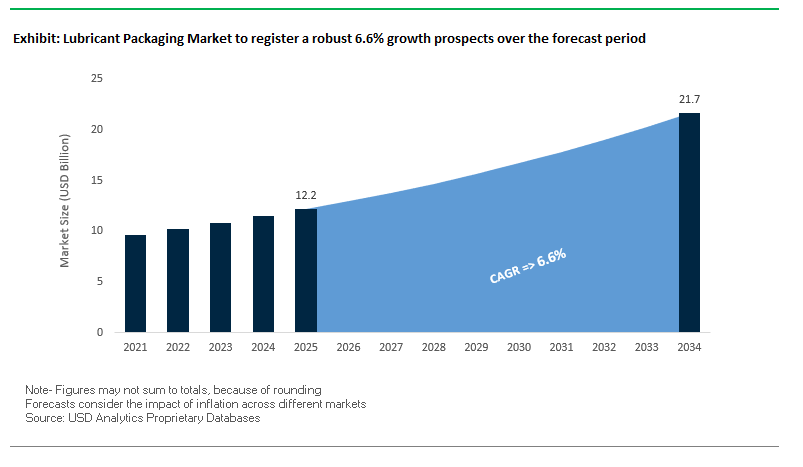

The global lubricant packaging market is projected to grow from USD 12.2 billion in 2025 to USD 21.7 billion by 2034, registering a healthy CAGR of 6.6%. This growth is being driven by rising industrial demand, sustainability-focused packaging innovations, and a shift towards lightweight flexible formats that lower costs and carbon emissions. Industry professionals are particularly evaluating how sustainability and smart packaging integration are reshaping supply chain strategies and customer engagement. Moreover, the increasing use of post-consumer recycled (PCR) plastic is setting new benchmarks for environmental compliance and brand reputation. For buyers, the key questions revolve around how packaging formats will adapt to new regulatory standards, the impact of flexible packaging on logistics, and the role of digital traceability technologies in protecting brand integrity.

Key Insights for professionals

- Sustainability transformation: Repsol’s use of 60% PCR plastic in containers cuts carbon emissions by 25%.

- Shift to flexible packaging: Up to 60% less plastic use and reduced logistics costs with pouches and bag-in-box solutions.

- Smart packaging adoption: RFID tags and QR codes enable supply chain visibility and anti-counterfeit protection.

- Recycled material integration: ExxonMobil’s Mobil™ brand uses 50% PCR plastic pails in India, driving industry-wide adoption.

Market Analysis: Strategic Developments and Industry Realignments

The lubricant packaging sector has entered a phase of rapid innovation and consolidation, with companies actively pursuing sustainability and global market expansion. In August 2025, Repsol introduced sustainable lubricant packaging using 60% PCR plastic, deployed in one-liter, four-liter, and five-liter containers under its Reciclex suite. In the same month, Toyo Ink Europe launched Steraflex GIO flexographic printing ink, compliant with upcoming European safety regulations. These developments highlight the parallel tracks of material innovation and regulatory alignment shaping the industry’s evolution.

Consolidation is another defining trend. In July 2025, Shell Lubricants completed its acquisition of Raj Petro Specialities Pvt. in India, strengthening its presence in a high-growth Asian market. Around the same time, Brazil’s Vibra Energia entered talks with Cosan S.A. to acquire its lubricants business Moove, reflecting a strong drive for scale in Latin America. Earlier, in April 2025, Fuchs acquired IRMCO, enhancing its industrial lubricant portfolio, while in March 2025, D-A Lubricant Company acquired Crystal Packaging, expanding custom blending capabilities. These moves underscore how lubricant companies are not only optimizing packaging but also strengthening vertical integration to gain competitive advantage.

Investor pressure and sustainability commitments are adding further momentum. In February 2025, activist investors urged BP to consider divesting its Castrol business, while SK Lubricants announced in December 2024 its plan to use mono-material containers for improved recyclability. Meanwhile, Fuchs Group’s acquisition of Boss Lubricants in January 2025 reaffirmed the European consolidation wave.

Emerging Trends and Strategic Opportunities in the Lubricant Packaging Market

Strategic Shift Towards High-Density Polyethylene (HDPE) with Post-Consumer Resin Integration

The lubricant packaging market is increasingly driven by sustainability mandates, corporate ESG commitments, and consumer demand for environmentally responsible packaging. A significant trend is the adoption of HDPE incorporating post-consumer resin (PCR), enabling manufacturers to produce bottles with recycled content without compromising performance. Material science innovations have allowed companies like ExxonMobil Chemical to increase PCR content in lubricant bottles to 50%, enhancing impact strength and stress-crack resistance. In India, Shell exceeded government PCR targets in early 2025, producing over three million bottles containing 30% recycled content for passenger car, motorcycle, and commercial vehicle lubricants. Advanced initiatives now focus on creating closed-loop recycling systems, where used lubricant bottles are collected and remanufactured into new packaging, significantly reducing waste. For instance, Shell’s sustainable packaging efforts in India are projected to prevent over 350 tonnes of plastic annually from entering landfills, highlighting tangible environmental impact. This trend reflects a clear movement toward circularity and sustainable packaging adoption in the lubricant industry.

Adoption of Lightweighting and Advanced Composite Materials for Logistics Efficiency

Another pivotal trend in lubricant packaging is lightweighting and the integration of advanced composite materials to improve logistics efficiency and reduce environmental impact. Reducing container weight directly mitigates freight-related carbon emissions, with flexible bladders in bulk liquid transport reportedly reducing emissions by up to 40% compared to traditional drums. Advanced composite containers also optimize payload, enabling transport of up to 28 tons of liquid versus the traditional 24 tons, reducing shipment frequency and associated costs. Material science breakthroughs, including thinner yet stronger container walls with advanced coatings, maintain structural integrity and prevent leaks, ensuring safe transport of lubricants. This trend highlights how packaging innovations not only improve operational efficiency but also contribute to corporate sustainability goals.

Development of Integrated Smart Packaging with QR Codes and NFC Tags

The demand for supply chain transparency, anti-counterfeiting, and enhanced consumer engagement is creating a strong market opportunity for smart lubricant packaging. Technologies such as QR codes and NFC tags enable instant product authentication, as evidenced by companies like Scantrust and Dupont, helping prevent counterfeit lubricants in the market. Furthermore, the EU Digital Product Passport (DPP) regulations support the use of QR codes for delivering comprehensive lifecycle information, including material composition, recycling pathways, and environmental impact. Smart packaging also facilitates direct consumer engagement; brands like Castrol are providing easy access to product data sheets, instructional content, and loyalty programs via QR codes, enhancing the overall user experience. The integration of smart technologies is set to redefine transparency, trust, and customer interaction in lubricant packaging.

Expansion of Reusable and Refillable Container Systems in the Industrial Sector

The industrial lubricant segment presents a high-growth opportunity for reusable and refillable packaging systems. Solutions offered by companies such as iCan Fluid Transfer System and THIELMANN address the challenge of single-use plastic waste while delivering long-term cost efficiencies. Reusable containers reduce the volume of plastic consumed and discarded, while durable materials like HDPE and stainless steel ensure superior protection of lubricant quality throughout the supply chain. Although initial investments are higher, the lifecycle cost benefits—including savings in procurement, disposal, and logistics—make reusable systems an attractive option for industrial clients. Adoption of these systems also aligns with corporate sustainability strategies, offering both environmental and operational advantages.

Competitive Landscape: Leading Players Reshaping Lubricant Packaging

The global lubricant packaging market is highly competitive, with energy giants and specialized packaging companies shaping product innovation and market strategies. Companies are focusing on recycled materials, smart packaging, and lightweighting technologies to balance performance, regulatory compliance, and sustainability goals. Below are the leading players and their positioning:

Shell plc: Sustainability-Driven Packaging Innovation

Shell continues to be one of the most influential players in the lubricant industry, investing heavily in packaging aligned with circular economy principles. In July 2025, it completed the acquisition of Raj Petro Specialities Pvt., reinforcing its Indian market position. The company is piloting stainless steel lubricant cans within reusable packaging systems in France. Its strategy prioritizes lightweight, reusable, and recycled packaging formats while maintaining strong market presence through flagship brands Shell Helix and Rimula.

ExxonMobil Corporation: Pioneering Recycled Content Integration

ExxonMobil’s Mobil™ brand has been a frontrunner in introducing PCR-based packaging. In February 2023, it launched pails made with 50% PCR plastic in India, signaling a scalable sustainability strategy. With packaging formats spanning pails, drums, and plastic bottles, ExxonMobil leverages its global supply chain to integrate eco-friendly practices. Its dual focus on high-performance lubricants and sustainable packaging solutions is central to its competitive strength.

TotalEnergies SE: Leveraging an Integrated Value Chain

TotalEnergies continues to expand lubricant packaging through its Total and Elf brands, with a growing focus on eco-friendly formulations and packaging. The company benefits from an integrated business model, giving it control across manufacturing and distribution, ensuring flexibility in packaging adoption. Its commitment to carbon reduction, supported by strong R&D investment, positions it as a reliable player for both industrial and automotive lubricant users.

Chevron Corporation: Advancing Eco-Friendly Lubricant Solutions

Chevron’s lubricant packaging strategy supports its broader sustainability agenda. In February 2022, the company formed a joint initiative with Bunge North America to develop renewable feedstocks, reinforcing its eco-focused credentials. Known for its Delo and Havoline brands, Chevron continues to innovate in packaging formats such as metal drums and plastic bottles, while embedding environmental responsibility in its operations.

Berry Global Inc.: Specialist in Sustainable Packaging Solutions

As a leading packaging manufacturer, Berry Global plays a critical role in the lubricant supply chain. The company specializes in bottles, pails, and closures, with a strong push towards PCR resin integration. Its global scale, coupled with expertise in materials science, enables it to supply durable yet sustainable packaging formats tailored for lubricant applications. Berry Global is uniquely positioned as a dedicated packaging supplier, providing OEMs with reliable, eco-friendly solutions.

Lubricant Packaging Market Share Insights

Bottles & Cans Lead Market Share by Packaging Type in the Lubricant Packaging Industry

Bottles and cans command 38% of the lubricant packaging market, establishing themselves as the most widely used format for consumer automotive and aftermarket lubricants. Their dominance is underpinned by the massive demand for passenger car engine oils sold in 1-quart bottles and 5-liter cans, particularly in DIY maintenance and quick-lube service channels. High-density polyethylene (HDPE) bottles dominate this category thanks to their chemical resistance, durability, and cost-effectiveness, making them the industry standard for packaged lubricants. Drums follow with a 25% share, acting as the industrial and commercial backbone of lubricant distribution, especially for bulk oils in workshops, fleets, and manufacturing facilities. Pails, IBCs, grease cartridges, and other formats serve specialized needs, but the market’s volume is heavily concentrated in bottles and cans, reflecting their critical role in automotive aftermarket consumption and global distribution efficiency.

Automotive End-Users Dominate Lubricant Packaging Market Share

The automotive sector holds 45% of the lubricant packaging industry’s market share, making it the largest end-user by a significant margin. This dominance stems from the global vehicle parc and the constant requirement for engine oils, gear oils, and greases, which are consumed both by passenger cars and heavy-duty fleets. Automotive packaging spans a wide range—from small bottles for retail consumers to large drums and pails for fleet operators—illustrating the segment’s diverse consumption patterns. Industrial users form the second largest group, characterized by complex lubrication requirements in machinery, compressors, and hydraulic systems, demanding versatile formats like pails, drums, and IBCs. Niche sectors such as metal fabrication, marine, and power generation contribute smaller shares but impose specialized performance requirements, such as packaging resistant to aggressive chemicals or suited for offshore durability. Collectively, automotive dominance is reinforced by the sector’s global scale, high lubricant turnover, and stringent performance demands on packaging integrity.

United States Lubricant Packaging Market Driven by Regulatory Compliance and Sustainable Innovations

The U.S. lubricant packaging industry is heavily influenced by a fragmented regulatory environment, with the Environmental Protection Agency (EPA) and state-level boards driving a shift toward recyclable and environmentally friendly packaging materials. The adoption of post-consumer recycled (PCR) plastics has become a key trend, reflecting growing regulatory and consumer pressure for sustainable packaging solutions. Technological advancements, such as ultra-lightweight plastic containers and smart packaging solutions with QR codes and RFID tags, are enabling real-time tracking, product authentication, and improved transport efficiency.

Corporate investments are playing a crucial role in market expansion. Shell’s acquisition of a 49% stake in Blue Tide Environmental LLC in late 2022 emphasizes the move toward circular economy initiatives and lubricant recycling systems. Key applications in the automotive, industrial, and marine sectors are driving demand for leak-proof, tamper-evident, and transport-efficient packaging, while sustainability campaigns, like Mobil’s 50% PCR plastic pails, are enhancing corporate responsibility and reducing plastic waste.

Germany’s Lubricant Packaging Market Advances Through Circular Economy and Industry 4.0 Innovations

Germany’s lubricant packaging market operates under the stringent German Packaging Act (VerpackG) and broader EU regulations, incentivizing the use of recyclable materials and efficient recycling systems. The market is at the forefront of technological innovation, with companies developing durable and high-performance container designs. The integration of Industry 4.0 solutions, including automation and AI, is streamlining production processes and improving operational efficiency.

Germany also leads in the circular economy, promoting packaging that is easily sorted and recyclable. Companies such as OKS Spezialschmierstoffe are aligning product development with environmental and hygiene guidelines, while Repsol’s sustainable lubricant packaging, incorporating 60% PCR and reducing carbon emissions by 25%, demonstrates the country’s commitment to eco-friendly practices.

China’s Lubricant Packaging Market Expands Through Government Initiatives and Domestic Manufacturing

China’s lubricant packaging industry is benefiting from the government’s dual carbon goal and the Action Plan for Large-Scale Equipment Updates and Consumer Goods Replacement, which encourage sustainable materials and limit excessive packaging. Regulatory reforms are influencing packaging standards for food-grade lubricants, emphasizing safety, compliance, and shared responsibility between manufacturers and printers.

Technological advancements, including automation and AI-driven production, are enhancing efficiency, while ongoing infrastructure projects and industrial modernization are fueling demand for durable and reliable lubricant packaging. Domestic manufacturing is expanding to meet local demand, with the automotive and industrial sectors serving as major drivers for high-quality and specialized packaging solutions.

India’s Lubricant Packaging Market Strengthens With Make in India and Sustainable Investments

India’s lubricant packaging market is witnessing growth driven by the Make in India initiative, encouraging domestic production and technological upgrades. Companies like Shell India are pioneering sustainable packaging, producing millions of bottles with 30% PCR content and aiming for full PCR integration by 2025. Technological adoption is growing, particularly in advanced packaging solutions for the automotive and industrial sectors.

Corporate investments, such as ExxonMobil’s $110 million plant in Raigad, Maharashtra, demonstrate strong commitment, with an annual production capacity of 159,000 kiloliters. Key applications in the automotive and manufacturing sectors, coupled with rising vehicle ownership, are major drivers for leak-proof, sustainable, and transport-efficient lubricant packaging in India.

Japan’s Lubricant Packaging Market Leads in Advanced Materials and High-Performance Products

Japan’s lubricant packaging market benefits from the country’s precision manufacturing expertise and innovation in advanced material technologies. Regulatory changes effective June 1, 2025, introducing a positive list for synthetic materials in packaging, are driving safer and compliant packaging solutions for food-grade and industrial lubricants.

Major players are focusing on specialty and value-added products, developing packaging with superior aesthetic and functional properties, such as self-sealing containers and enhanced barrier performance. Innovations like bio-polypropylene (bio-PP) from renewable feedstock, used by companies including LyondellBasell, align with Japan’s 2030 and 2050 environmental targets, further reinforcing the market’s sustainability focus.

Brazil’s Lubricant Packaging Market Accelerates Through Sustainable Practices and Strategic Investments

Brazil’s lubricant packaging industry is supported by the National Solid Waste Policy, encouraging sustainable practices and the use of recyclable materials, including plastic and metal packaging. Technological advancements focus on biodegradable, recyclable, and compostable solutions, with bio-based polyethylene derived from sugarcane lowering fossil fuel dependence.

Corporate investments are driving market growth, exemplified by Ardagh Group’s glass production facility, catering to Brazil’s growing lubricant market. Strong demand in the automotive, industrial, and agricultural sectors, along with increasing consumption of processed and ready-to-use lubricants, is boosting the adoption of high-performance, sustainable packaging solutions.

Lubricant Packaging Market Report Scope

Lubricant Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$12.2 Billion

|

|

Market Size (2034)

|

$21.7 Billion

|

|

Market Growth Rate

|

6.6%

|

|

Segments

|

By Material (Plastic, Metal, Flexible Packaging), By Packaging Type (Bottles & Cans, Pails, Drums, Kegs, IBC, Grease Cartridges, Others), By End-User (Automotive, Industrial, Power Generation, Chemical Industry, Metal Fabrication, Marine, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Bemis Company (now Amcor), Greif, Inc., Scholle IPN, Mauser Packaging Solutions, Ball Corporation, Silgan Holdings Inc., Mondi plc, WestRock Company, Orora Limited, Sealed Air Corporation, BWAY Corporation, Time Technoplast Ltd., Balmer Lawrie & Co. Ltd., Universal Lubricants LLC, Mold-Tek Packaging Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Lubricant Packaging Market Segmentation

By Material

- Plastic

- Metal

- Flexible Packaging

By Packaging Type

- Bottles & Cans

- Pails

- Drums

- Kegs

- IBC

- Grease Cartridges

- Others

By End-User

- Automotive

- Industrial

- Power Generation

- Chemical Industry

- Metal Fabrication

- Marine

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Lubricant Packaging Market

- Bemis Company (now Amcor)

- Greif, Inc.

- Scholle IPN

- Mauser Packaging Solutions

- Ball Corporation

- Silgan Holdings Inc.

- Mondi plc

- WestRock Company

- Orora Limited

- Sealed Air Corporation

- BWAY Corporation

- Time Technoplast Ltd.

- Balmer Lawrie & Co. Ltd.

- Universal Lubricants LLC

- Mold-Tek Packaging Ltd.

* List Not Exhaustive

Methodology

The research methodology for the global Lubricant Packaging Market integrates a combination of primary and secondary approaches to deliver precise, actionable insights for industry professionals. Primary research involved detailed interviews with packaging engineers, lubricant manufacturers, sustainability officers, and supply chain experts across key regions to gather firsthand perspectives on packaging innovations, regulatory compliance, and smart technology adoption. Secondary research included analysis of company reports, industry journals, trade publications, regulatory frameworks, and sustainability disclosures to validate market trends, growth drivers, and competitive dynamics. Market sizing, CAGR, and segment forecasts were triangulated using both top-down and bottom-up approaches, with careful attention to packaging material adoption, flexible formats, smart technologies, and recycled content integration. Regional dynamics were assessed against government policies, environmental mandates, and automotive and industrial lubricant demand patterns. The methodology ensures USDAnalytics provides a robust, fact-based, and industry-relevant perspective on lubricant packaging market growth, strategic opportunities, and technological trends.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.