Market Overview: Electrification Scale, Power-Density Demands, and Supply Security Are Reshaping the Magnetic Materials Landscape

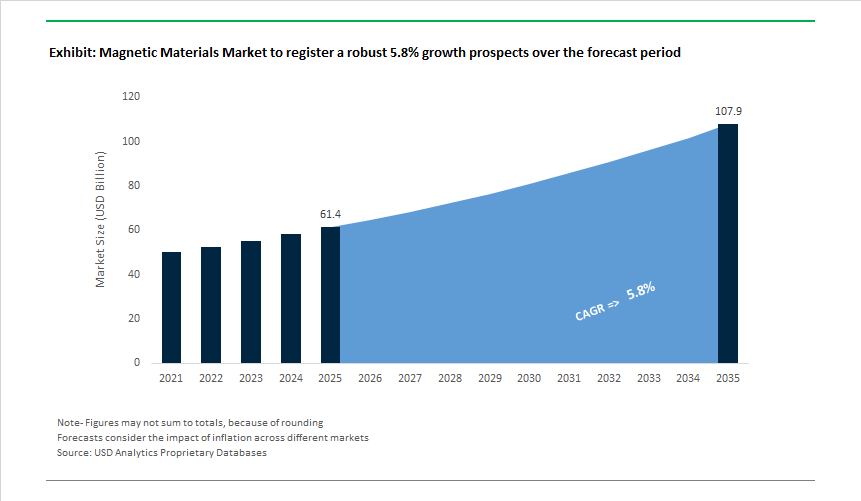

The Magnetic Materials Market stands at USD 61.4 billion in 2025 and is projected to reach USD 107.9 billion by 2035, expanding at a 5.8% CAGR as magnets and soft magnetic alloys become system-critical enablers of electrified mobility, energy efficiency, and digital infrastructure. Unlike many advanced materials markets, growth here is not discretionary; it is structurally tied to electrification intensity, motor efficiency targets, and the physics of power conversion.

On the permanent magnet side, demand is being fundamentally altered by the shift from internal combustion to electric drivetrains. Battery electric vehicles materially increase magnet intensity: traction motors based on permanent magnet synchronous designs require multiple times the rare-earth content of legacy ICE platforms. This makes NdFeB magnets a strategic input, not just a component, across automotive, robotics, wind turbines, and industrial automation. The dominance of sintered NdFeB, accounting for roughly 71% of the high-performance permanent magnet segment in 2025, reflects the lack of viable substitutes where high torque density, efficiency, and compact motor design are required. For OEMs, magnet availability and pricing volatility now directly influence vehicle cost structures, motor architecture choices, and long-term platform risk.

In parallel, soft magnetic materials are becoming critical to the next wave of power electronics miniaturization. Nanocrystalline and amorphous alloys enable inductors, transformers, and chokes to operate at switching frequencies exceeding 1 MHz, unlocking up to threefold reductions in passive component size. This capability is central to compact EV inverters, high-density data-center power supplies, telecom rectifiers, and fast-charging infrastructure, where power density and thermal management increasingly dictate system competitiveness. Here, magnetic materials function as performance multipliers, enabling architectures that silicon and wide-bandgap semiconductors alone cannot deliver.

The concentration of rare-earth processing and metal refining capacity creates exposure that has elevated magnetic materials into a strategic policy concern across major economies. This is accelerating investment in alternative sourcing, magnet recycling, material efficiency improvements, and motor designs that reduce-but do not eliminate-rare-earth dependence. Importantly, these efforts tend to complement rather than displace NdFeB usage in high-performance applications, reinforcing the market’s structural demand base.

Looking ahead, competitive advantage in the magnetic materials market will be defined by control over critical materials, application-specific performance engineering, and supply resilience, rather than sheer production volume. As electrification deepens and power systems move toward higher frequency and density, magnetic materials are increasingly treated as foundational infrastructure inputs, with procurement, policy, and technology decisions converging around their availability and performance.

Market Analysis: Recent Policy Moves, Price Shocks and Capacity Ramp-Ups

Global activity emphasises supply-chain reshoring, raw-material price volatility, and targeted capacity investments. In January 2024 India launched its National Critical Minerals Mission (NCMM) to secure critical minerals including rare earths, signalling early policy momentum toward domestic mineral strategy. October 2024 Lynas completed Phase 1 of its Kalgoorlie processing facility, expanding non-Chinese separation capacity and demonstrating private sector commitments to diversify REE supply outside Asia. In January 2025 the U.S. Department of Defense allocated USD 285 million under the Defense Production Act (FY2024) to develop rare earth supply chains for military-grade magnets, reflecting strategic interest in downstream magnet capacity.

Geopolitical and market stress intensified through 2025. In April 2025 China implemented export controls on rare earth magnets (including NdFeB alloys), provoking immediate global supply disruptions and prompting accelerated diversification plans. Price signals followed: November 2025 benchmark NdPr oxide prices were reported up ~28.9% YoY, reinforcing cost pass-through risk for magnet users. National industrial policy responses emerged rapidly - November 2025 India approved a Rare Earth Permanent Magnet (REPM) Manufacturing Scheme (₹7,280 crore) to develop ~6,000 MTPA integrated REPM capacity, while December 2025 the U.S. government increased strategic equity stakes in critical minerals and downstream magnet projects to shore up domestic production. On the manufacturing front, MP Materials’ Fort Worth magnet facility became operational in 2024 (highlighted in October 2025 updates), and Lynas advanced US-partnered heavy-REE separation plans - together these moves indicate momentum toward a more diversified, though still nascent, non-Chinese magnet ecosystem.

Magnetic Materials Market Trends and Opportunities

Intensive R&D into Rare-Earth-Free Permanent Magnets for Traction Motors

The dominance of rare-earth elements in high-performance permanent magnets has become a strategic vulnerability rather than a materials advantage. With over 90% of rare-earth processing capacity concentrated in a single geography, automotive OEMs and governments are accelerating the commercialization of iron-based and manganese-based magnet chemistries that can be produced from abundant domestic resources.

A pivotal milestone was reached in October 2025 when Niron Magnetics began construction of its first commercial-scale facility in Sartell, Minnesota. Designed for 1,500 tons per year of rare-earth-free iron nitride magnets, the project is supported by U.S. federal funding and a strategic development partnership with Stellantis to validate these magnets in EV traction motors. The significance lies in manufacturability: iron nitride enables high coercivity without rare-earth elements, addressing both cost volatility and supply-chain risk.

Parallel progress is being made in manganese bismuth (MnBi) systems. Research published in late 2025 highlights MnBi’s positive temperature coefficient of coercivity, meaning magnetic stability improves as operating temperatures rise—an inversion of the behavior seen in NdFeB magnets. With optimized MnBi thin films achieving 70–80 emu/g saturation magnetization, these materials are increasingly attractive for high-temperature motor environments where thermal management remains a major cost and design constraint.

Policy is reinforcing this shift. The EU’s 2025 RESourceEU Action Plan explicitly targets a 30–50% reduction in rare-earth dependency by 2029, acknowledging that local magnet production can be multiple times more expensive unless alternative material systems mature. This has repositioned rare-earth-free magnets from a research curiosity to a strategic industrial priority.

Shift to High-Frequency, Low-Loss Soft Magnetic Composites (SMCs)

The transition to wide-bandgap (WBG) power electronics—Silicon Carbide and Gallium Nitride—is fundamentally reshaping soft magnetic material requirements. As inverter switching frequencies move from kilohertz toward the hundreds of kilohertz and beyond, traditional laminated electrical steels face prohibitive eddy current losses. This is accelerating adoption of Soft Magnetic Composites (SMCs), which enable three-dimensional magnetic flux paths and dramatically lower high-frequency losses.

By late 2025, GaN-based inverters paired with optimized SMC cores were demonstrating system efficiencies above 97.5% in 800V architectures. Unlike laminated steels, SMCs rely on individually insulated iron particles, suppressing eddy currents even as switching frequencies approach 1 MHz. This capability is unlocking more compact motor-integrated inverters and reducing the size of passive components in on-board chargers.

Miniaturization benefits are already visible. Industry disclosures from September 2025 indicate that GaN/SiC-based designs can achieve up to a 40% reduction in magnetic component volume, enabling faster charging profiles—such as 10–80% recharge in ~20 minutes—without thermal runaway. These performance gains are inseparable from advances in soft magnet design.

On the manufacturing side, GKN Powder Metallurgy showcased industrial-scale SMC production in 2025, pairing materials supply with FEM and CFD-based thermal simulation to co-design magnetic components for EV traction inverters. This integration of materials science with system engineering reflects a broader shift: soft magnetic materials are no longer commodities but co-developed subsystems.

Magnetic Materials for High-Efficiency Hydrogen Electrolyzers

Hydrogen production and handling is emerging as a non-obvious but high-value growth vector for magnetic materials. Beyond motors and generators, magnets are now being explored as active efficiency enhancers in electrochemical systems.

In 2025, researchers at Indian Institute of Technology Bombay demonstrated that applying external magnetic fields during water electrolysis can reduce energy consumption by ~19% while tripling hydrogen production rates. This magneto-electrocatalysis approach leverages cobalt-oxide nanostructures that sustain magnetization, offering a pathway to retrofit existing electrolyzers rather than replace them entirely.

Downstream, hydrogen liquefaction remains one of the most energy-intensive steps in the value chain. National Institute for Materials Science is advancing Active Magnetic Regenerative Refrigeration (AMRR) systems that exploit the magnetocaloric effect to achieve cryogenic temperatures near 20 K (−253°C). As of 2025, these systems are demonstrating materially lower energy penalties than conventional gas-cycle refrigeration, positioning magnetic materials as enablers of hydrogen logistics rather than passive components.

Additionally, high-power electrolyzer stacks require low-loss electrical steels and high-flux magnets in rectifiers and compression units, creating a secondary but scalable demand channel tied directly to gigawatt-scale hydrogen deployments.

Advanced Thin-Film Magnets for Next-Generation Computing

At the opposite end of the application spectrum, magnetic materials are becoming central to post-DRAM memory architectures. AI workloads are exposing the latency and energy limitations of conventional memory hierarchies, accelerating interest in Spin-Orbit Torque MRAM (SOT-MRAM).

In October 2025, a collaboration involving TSMC and Industrial Technology Research Institute demonstrated a 64-kilobit SOT-MRAM device with 1-nanosecond switching speed and multi-year data retention. Achieved using nanometer-scale cobalt and tungsten layers, this performance places SOT-MRAM in direct competition with SRAM for on-chip cache applications.

Power efficiency is the decisive factor. Research from Tohoku University reported write energies as low as 156 femtojoules, eliminating the high current densities that constrained earlier MRAM generations. For AI accelerators, this translates into meaningful reductions in data movement energy—one of the largest contributors to total compute power consumption.

Further miniaturization is underway. In late 2025, Intel and Georgia Institute of Technology demonstrated 7 nm-class SOT-MRAM with bit densities approaching 14.8 Mb/mm², relying on ultra-precise thin-film deposition to maintain magnetic phase stability under 400°C CMOS back-end processing constraints.

Market Share Analysis: Magnetic Materials Market

Market Share by Material Type: Permanent Magnets as the Backbone of Torque-Dense Electrification

Permanent magnets account for approximately 55% of the global Magnetic Materials Market because they uniquely deliver continuous magnetic fields without ongoing electrical excitation, making them indispensable in efficiency-critical systems. The dominance of Neodymium-Iron-Boron (NdFeB) magnets is structurally linked to the rise of compact, high-torque electric motors, where 30%–50% mass reduction versus induction motors directly translates into longer driving range, higher payload capacity, or smaller system footprints. This advantage compounds at scale: lighter motors reduce cooling requirements, structural reinforcement, and overall system complexity. Technologically, the segment’s leadership has been reinforced by thermal breakthroughs, with 2025-grade NdFeB magnets maintaining magnetic stability up to 220°C, enabling placement directly in high-heat zones such as EV drivetrains, industrial servomotors, and wind turbine generators. Equally important is the market’s strategic pivot toward heavy rare earth–free alloys, which mitigate supply-chain volatility while preserving high energy density—an inflection point that has shifted permanent magnets from a cost risk to a long-term procurement asset. Together, efficiency gains of around 10% at the motor level, rising electrification intensity, and de-risked material sourcing explain why permanent magnets remain the economic and technological anchor of the magnetic materials value chain.

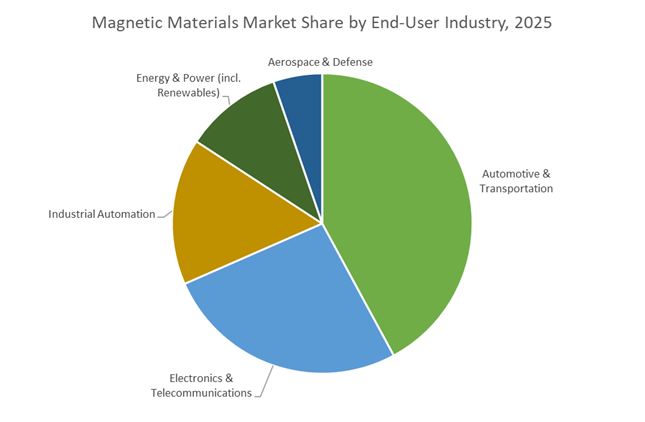

Market Share by Application: Automotive & Transportation Driving Structural Magnet Intensity

Automotive and transportation represent around 40% of total magnetic materials demand, positioning the segment as the primary volume and innovation driver. This leadership is not cyclical but structural: modern electric and hybrid vehicles now embed 2–3 kg of rare-earth magnets per vehicle, more than three times the magnet intensity of internal combustion platforms. The near-universal adoption of brushless DC (BLDC) motors—exceeding 90% penetration in EVs—locks permanent magnets into the core of propulsion, power steering, braking, thermal management, and auxiliary systems. Beyond road vehicles, transportation electrification is expanding into rail, aerospace actuation, and heavy-duty platforms, while adjacent demand from direct-drive offshore wind turbines—with up to 600 kg of neodymium magnets per 15 MW unit—reinforces scale economics for automotive-grade magnet production. From a systems perspective, optimized magnet selection delivers 20%–30% reductions in total energy consumption, aligning OEM procurement with tightening emissions regulations and lifecycle sustainability targets. As a result, automotive and transportation buyers are not merely consuming magnets—they are shaping material specifications, capacity investments, and long-term supply strategies, securing this segment’s position as the single most influential end-use market for magnetic materials in 2025 and beyond.

Competitive Landscape Overview: Incumbents Span Permanent Magnet Makers to Soft-Magnet Specialists and Recyclers

Market leaders differentiate on magnet performance (BHmax, coercivity, temperature stability), soft-magnetic core loss at high frequency, vertical integration into REE supply, and recycling/processing capabilities. Success factors include secure NdPr feedstock, advanced alloy formulations that reduce heavy-rare-earth content, high-frequency soft magnetic solutions for power conversion, and strategic geographic footprint to serve automotive and energy sectors.

TDK Corporation: Broad Supplier Of Permanent and Soft Magnetic Solutions Enabling Electrification

TDK supplies both NdFeB permanent magnets and soft magnetic ferrite/amorphous alloys; its strategy emphasises rare-earth-saving NdFeB grades for EV motors and improved ferrite materials for high-frequency power supplies. TDK’s global R&D/manufacturing footprint enables close OEM collaboration on custom magnetic components, and the company is focused on improving ferrite performance at higher switching frequencies to support converter miniaturisation.

Hitachi Metals (Metglas): Leader in Amorphous and Nanocrystalline Soft Magnetics For Efficiency Gains

Hitachi Metals (Metglas/FINEMET®) is a global leader in amorphous and nanocrystalline soft magnetic alloys that deliver very low core loss - ideal for distribution transformers and high-frequency power electronics. Its investment in Soft Magnetic Composite (SMC) powder cores and 3D magnetic circuit designs positions it to capture demand for compact EV inductors and high-efficiency grid components.

Shin-Etsu Chemical: High-Performance Ndfeb Magnets With Focus On Dy-Reduction

Shin-Etsu is a major producer of sintered NdFeB magnets, developing grades with high coercivity and thermal stability while reducing dependence on heavy rare earths like Dysprosium. Its precision magnetics serve robotics, HDD, and high-performance servo motors where high BHmax and tight tolerances are required, and it maintains strict quality and traceability across Japanese and Chinese production lines.

Lynas Rare Earths: Non-Chinese Ndpr Producer Scaling Separation Capacity For Magnet Feedstock

Lynas is the largest non-Chinese separated REO producer (NdPr oxide) and completed Phase 1 of the Kalgoorlie plant to expand separation capacity. With strategic investments and a U.S. DoD partnership for heavy REE separation, Lynas is central to feedstock diversification and supports the magnet industry’s broader ambition to localise upstream processing.

VACUUMSCHMELZE (VAC): Premium Alloy Specialist for Extreme Environments and Recycling Pilots

VAC specialises in high-end soft and permanent magnetic alloys (SmCo, nanocrystalline foils) for aerospace, medical and high-temperature applications; SmCo retains performance above 350°C for extreme-temperature motors. VAC also invests in European magnet recycling pilots aimed at building closed-loop supply chains and reducing reliance on primary rare earth imports.

India has positioned itself as the fastest-emerging challenger in the global rare earth permanent magnets (REPM) market, driven by an explicit shift from import dependence to end-to-end localization. The ₹7,280 crore ($870 million) cabinet-approved scheme announced on November 26, 2025, marks India’s first large-scale intervention focused specifically on sintered NdFeB magnet manufacturing, a segment critical for EV traction motors, wind turbines, and industrial servomotors. Of the total outlay, ₹6,450 crore is structured as sales-linked incentives over five years, while ₹750 crore is allocated to capital subsidies to establish 6,000 MTPA of domestic magnet capacity—signaling a clear volume and scale ambition.

Execution has already begun. In November 2025, Lohum commissioned India’s first integrated REPM facility in Uttar Pradesh, designed to process both primary and recycled rare earth feedstock. The plant targets 20% import substitution for domestic magnet demand, creating strategic insulation against global price volatility and export controls. For OEMs, this materially lowers supply-chain risk in EV and grid-scale motor deployments while anchoring India within the Asia-Pacific magnet manufacturing map.

China: MOFCOM Export Controls and Extraterritorial Magnet Governance

China remains the systemic regulator of the global magnetic materials ecosystem, leveraging both scale and law. Effective November 8, 2025, the Ministry of Commerce (MOFCOM) imposed comprehensive export controls covering medium and heavy rare earths, processing equipment, and magnet manufacturing technologies—a move that extends beyond raw materials into process know-how. The implications are structural: global automakers, defense contractors, and electronics firms must now treat magnet sourcing as a geopolitical compliance function, not just procurement.

The regulatory reach deepened further with the “0.1% de minimis rule”, effective December 1, 2025, which subjects foreign-made magnets to Chinese export licensing if Chinese-origin REEs account for ≥0.1% of material value. Combined with the “50% rule”—presuming license denial for entities majority-owned by firms on China’s control lists—this framework effectively embeds Chinese oversight across EV motors, robotics, aerospace actuators, and 6G hardware, reinforcing China’s role as a whole-chain magnet gatekeeper.

United States: Heavy Rare Earth Recovery and Defense-Grade Qualification

The United States is rebuilding its heavy rare earth (HREE) supply chain, prioritizing Dysprosium (Dy) and Terbium (Tb)—elements essential for high-temperature NdFeB magnets used in EV traction motors and aerospace systems. On December 1, 2025, the Department of Energy (DOE) announced a $134 million funding program to commercialize REE recovery from mine tailings and e-waste, explicitly targeting supply resilience rather than spot-market substitution.

Industrial validation followed quickly. In December 2025, Energy Fuels confirmed that its 99.9% purity dysprosium oxide, produced in Utah, passed qualification tests for a major South Korean automotive OEM. The company plans to scale Tb and Sm oxide output by early 2026. Alongside DOE-backed Rare Earth Demonstration Facilities, this positions the U.S. as the primary non-Chinese source of heavy rare earth oxides, critical for defense and EV electrification strategies.

Japan: GX 2040 Vision Anchors Decarbonized Magnet Production

Japan is integrating magnetic materials into its long-term industrial decarbonization framework, rather than treating them as a standalone commodity segment. The GX 2040 Vision, approved on January 18, 2025, channels R&D subsidies toward low-carbon NdFeB magnets, soft magnetic alloys, and recycling technologies, aligning magnet manufacturing with national climate and energy-security goals. This policy linkage gives Japanese suppliers a structural advantage in ESG-sensitive automotive and electronics markets.

The 7th Strategic Energy Plan (February 2025) further identifies data centers, AI infrastructure, and next-generation vehicles as priority demand centers. In response, Japanese firms are scaling amorphous and nanocrystalline soft magnetic ribbons, where ultra-low core loss improves grid efficiency for AI-optimized power networks. This positions Japan as a leader in energy-efficient magnetics, particularly for high-frequency and low-loss applications.

European Union: RESourceEU and Mandatory Magnet Circularity

The European Union is reframing magnetic materials through mandatory circular-economy regulation rather than direct capacity competition. The RESourceEU Action Plan, launched in December 2025, mandates that 25% of the EU’s strategic raw material consumption must be met through recycling by 2030, directly targeting the bloc’s ~90% dependence on Chinese rare earth magnets.

Policy measures extend beyond targets. By mid-2026, the EU plans to restrict exports of permanent magnet scrap, ensuring domestic recyclers retain access to feedstock. New regulations will also require minimum recycled content in magnets sold within the EU, embedding recycled NdPr into consumer electronics, appliances, and mobility platforms. For suppliers, compliance capability is becoming as critical as magnetic performance.

South Korea: Advanced Packaging and Automotive Qualification Hub

South Korea occupies a strategic mid-stream role, integrating diversified rare earth inputs into high-value electronics and automotive systems. Under the government’s ₩360.6 billion ($273 million) advanced packaging mandate, low-loss magnetic substrates are being developed for HBM4 and AI accelerator packaging, where electromagnetic stability is essential at extreme data rates.

Equally significant is supply-chain diversification. In 2025, South Korean magnet producers successfully qualified U.S.-sourced dysprosium and terbium oxides for EV traction motors, reducing reliance on Chinese-heavy supply routes. This qualification capability—bridging U.S. upstream materials with Korean manufacturing precision—cements South Korea’s role as a global integration node for EVs, semiconductors, and high-temperature magnetic systems.

2025 Strategic Matrix: Magnetic Materials Market Developments

Magnetic Materials Market Developments Matrix

|

Country

|

Primary Market Driver

|

2025 Strategic Milestone

|

Key Material Focus

|

|

India

|

EVs & self-reliance

|

₹7,280 Cr national REPM scheme

|

Sintered NdFeB magnets

|

|

China

|

Resource sovereignty

|

MOFCOM extraterritorial controls

|

Heavy REEs & processing tech

|

|

United States

|

Defense & EV resilience

|

$134M DOE REE recovery funding

|

Dy, Tb & Sm oxides

|

|

Japan

|

GX 2040 & energy efficiency

|

GX 2040 Vision approval

|

Soft magnetic alloys

|

|

European Union

|

Circular economy

|

RESourceEU recycling mandates

|

Recycled NdPr & magnet scrap

|

|

South Korea

|

AI & EV integration

|

Qualification of U.S. HREEs

|

High-temp automotive magnets

|

Magnetic Materials Market Report Scope

Magnetic Materials Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$61.4 Billion

|

|

Market Size (2035)

|

$107.9 Billion

|

|

Market Growth Rate

|

5.8%

|

|

Segments

|

By Material Type (Permanent Magnets—Rare Earth, Non-Rare Earth; Soft Magnetic Materials—Soft Ferrites, Electrical Steels, Amorphous & Nanocrystalline Alloys, SMC; Semi-Hard Magnetic Materials), By Product Form (Sintered Magnets, Bonded Magnets, Laminated Cores, Powders & Slurries, Ribbons & Foils), By Core Technology/Innovation (Additive Manufacturing, Short-Loop Recycling, Dysprosium-free / Low-Dy Magnets, AI-Designed Magnetic Geometries), By Application (Automotive, Electronics, Energy, Industrial, Healthcare), By End-User Industry (Automotive & Transportation, Electronics & Telecommunications, Industrial Automation, Aerospace & Defense, Energy & Power)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Hitachi Metals / Proterial, TDK Corporation, Shin-Etsu Chemical Co. Ltd., MP Materials Corp., VAC GmbH & Co. KG, Ningbo Yunsheng Co. Ltd., Zhongke Sanhuan High-Tech, Neo Performance Materials, Arnold Magnetic Technologies, Lynas Rare Earths Ltd., DMEGC Magnetic Ltd., Bunting Magnetics Co., Metglas Inc., Baotou Steel Rare Earth, Daido Steel Co. Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Magnetic Materials Market Segmentation

By Material Type

- Permanent (Hard) Magnets:

- Rare Earth

- Non-Rare Earth

- Soft Magnetic Materials:

- Soft Ferrites

- Electrical Steels

- Amorphous & Nanocrystalline Alloys

- Soft Magnetic Composites (SMC)

- Semi-Hard Magnetic Materials

By Product Form

- Sintered Magnets

- Bonded Magnets

- Laminated Cores

- Powders & Slurries

- Ribbons & Foils (Amorphous)

By Core Technology/Innovation

- Additive Manufacturing

- Short-Loop Recycling

- Dysprosium-free / Low-Dysprosium Magnets

- AI-Designed Magnetic Geometries

By End-User Industry

- Automotive & Transportation

- Electronics & Telecommunications

- Industrial Automation

- Aerospace & Defense

- Energy & Power

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Magnetic Materials Market

- Hitachi Metals, Ltd. (Proterial)

- TDK Corporation

- Shin-Etsu Chemical Co., Ltd.

- MP Materials Corp.

- Vacuumschmelze (VAC) GmbH & Co. KG

- Ningbo Yunsheng Co., Ltd.

- Zhongke Sanhuan High-Tech Co., Ltd.

- Neo Performance Materials

- Arnold Magnetic Technologies

- Lynas Rare Earths Ltd.

- DMEGC Magnetic Ltd.

- Bunting Magnetics Co.

- Metglas, Inc.

- Baotou Steel Rare Earth

- Daido Steel Co., Ltd.

*- List not Exhaustive