Mandelic Acid Market 2025–2034: Chiral API Expansion, Encapsulated AHAs, and Biocatalytic Synthesis Driving $1,441.9 Million Outlook at 16.8% CAGR

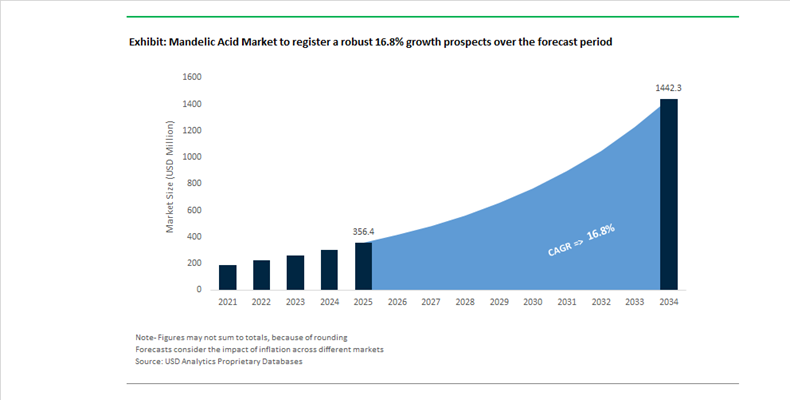

The Mandelic Acid Market is projected to surge from $356.4 Million in 2025 to $1,441.9 Million by 2034, registering a rapid CAGR of 16.8%. Growth is fueled by expanding pharmaceutical demand for high-purity chiral intermediates, rising adoption of alpha-hydroxy acids in dermatology-driven skincare, and accelerating transition toward biocatalytic synthesis routes with ultra-high enantiomeric excess. Mandelic acid serves as a critical precursor in antibiotic and anti-inflammatory active pharmaceutical ingredients while simultaneously gaining traction in cosmetic exfoliation, acne treatment, hyperpigmentation management, and sensitive-skin formulations. Increasing regulatory scrutiny on solvent residues and stereochemical purity is reshaping upstream synthesis strategies and downstream application positioning across pharma and personal care value chains.

In late 2023 and early 2024, Jiangxi Keyuan Biopharm entered a strategic supply agreement with a leading South Korean cosmetics conglomerate to deliver high-purity DL-mandelic acid for K-Beauty applications, reflecting a 21% rise in mandelic-based serum launches over two years. In 2024, BASF introduced an eco-friendly mandelic acid line designed for premium cosmetic applications with reduced environmental footprint during synthesis. During the same year, AHA Labs launched buffered mandelic formulations targeting reactive and low-tolerance skin types, while Wishtrend introduced its 5% Skin Prep Water for daily-use exfoliation. Good Molecules also released a 10% mandelic acid serum combined with phytic acid and gluconolactone, illustrating the multi-acid “cocktail” strategy gaining popularity in affordable skincare segments. In late 2024, Evonik expanded mandelic acid production capacity to meet rising clean-label exfoliant demand, with new lines operational through 2025.

Strategic consolidation and technological innovation accelerated through 2025 and early 2026. In early 2025, Vivalto Partners acquired Linnea SA to scale pharmaceutical-grade mandelic acid derivatives and strengthen global supply of high-purity chiral building blocks. In mid-2025, manufacturers began transitioning toward enzyme-engineered biocatalytic synthesis capable of achieving 99.9% enantiomeric excess, addressing premium pharmaceutical requirements for stereoselective APIs. In February 2026, Almond Clear Focus introduced its Micro-Encapsulated Mandelic Complex, enabling controlled time-release of concentrations above 10% while minimizing irritation, expanding applicability for sensitive skin treatments. In the same month, researchers reported advances in chiral covalent organic framework membrane technology using mandelic acid as a model molecule, enabling high-efficiency enantioseparation and potentially reducing production costs of L-mandelic acid for pharmaceutical manufacturing.

Mandelic Acid Market Trends and Opportunities: Clinical-Grade Skincare Shift and Sustainable Production Breakthroughs

Formulator Shift Toward Barrier-Safe Exfoliation and Tech-Driven Mandelic Acid Actives in Prestige Skincare

The Mandelic Acid market is witnessing a decisive transition toward biocompatible, barrier-preserving exfoliation systems, driven by increasing demand for sensitive skin-friendly AHAs and clinically validated skincare actives. Prestige skincare brands are actively replacing aggressive exfoliants with Mandelic Acid due to its larger molecular structure, enabling controlled epidermal penetration and significantly reduced irritation profiles compared to Glycolic Acid. This shift aligns with the rising demand for “glass skin” outcomes without compromising skin-barrier integrity, a key differentiator in premium skincare formulations.

Market adoption has accelerated following strategic repositioning by major beauty conglomerates. In September 2025, The Estée Lauder Companies emphasized “breakthrough claims” and night-time repair innovations, incorporating Mandelic Acid as a core ingredient to address both efficacy and tolerability benchmarks. Clinical validation further strengthens this trend, with 5% to 10% Mandelic Acid formulations now widely recognized as safe across diverse phototypes. A 2025 dermatological study demonstrated that 10% Mandelic Acid delivers effective skin renewal with minimal inflammatory response, contrasting sharply with the irritation associated with 30% Glycolic Acid peels.

From a demand-side perspective, “barrier-safe exfoliation” has emerged as a high-intent SEO keyword and consumer search driver, influencing formulation pipelines globally. Prestige retailers reported reduced product return rates linked to adverse reactions, reinforcing Mandelic Acid’s positioning as a next-generation AHA for sensitive skin markets.

Regulatory Tightening and Supply Chain Risk in China Reshaping Global Mandelic Acid Sourcing

The global Mandelic Acid supply chain is undergoing recalibration due to heightened regulatory scrutiny in China, the dominant production hub. In December 2025, the China National Institutes for Food and Drug Control (NIFDC) introduced stringent Technical Guidelines for Cosmetic Raw Material Filing Updates, mandating three-batch equivalence testing for any process modification. This significantly elevates compliance costs and introduces operational rigidity for manufacturers.

The regulatory framework reclassifies process changes as regulated exceptions rather than routine optimizations, forcing key suppliers in Shaanxi and Shandong to pause production enhancements during mandatory monitoring periods. This has reduced supply flexibility and increased lead-time uncertainty, directly impacting global Mandelic Acid procurement strategies.

In response, multinational cosmetic and pharmaceutical companies are intensifying due diligence through traceability dossiers and regulatory alignment protocols, particularly in line with the European Commission’s SCCS Notes of Guidance (12th revision), which emphasize systemic exposure and ingredient safety. This trend is accelerating the shift toward multi-source procurement strategies and regional supplier diversification, positioning regulatory compliance as a competitive differentiator in the Mandelic Acid market.

Expansion of Medical-Grade Mandelic Acid in Acne and Hyperpigmentation Treatment Protocols

A significant growth avenue lies in the medicalization of Mandelic Acid, transitioning it from a cosmetic ingredient to a dermatologically endorsed therapeutic adjunct. Its efficacy in treating post-inflammatory hyperpigmentation (PIH), melasma, and acne vulgaris is supported by robust clinical evidence, making it a preferred option in prescription-strength skincare regimens.

An 18-month prospective study (published in 2025) demonstrated that 30% Mandelic Acid achieved ≥30% improvement in periorbital melanosis, while exhibiting a lower post-treatment exfoliation rate (5.7%) compared to 14.3% for Lactic Acid. This superior tolerability profile enhances patient compliance, a critical factor in long-term dermatological treatments.

Additionally, Mandelic Acid’s bactericidal properties are driving its integration into post-antibiotic acne maintenance therapies, addressing the growing global concern around antibiotic resistance in dermatology. Regulatory developments are further amplifying this opportunity. The FDA’s increasing restrictions on over-the-counter hydroquinone-based skin-lightening products have created a substantial market gap, positioning Mandelic Acid as a safe, non-toxic alternative for melasma and pigmentation management. This is expected to drive strong demand across both cosmeceutical and pharmaceutical-grade Mandelic Acid segments.

Green Chemistry and Bio-Based Mandelic Acid Production Unlocking Sustainable Market Growth

Sustainability-driven innovation is emerging as a transformative opportunity in the Mandelic Acid market, particularly through the development of green synthesis pathways and bio-based production technologies. Traditional manufacturing methods, reliant on benzaldehyde and cyanide intermediates, are increasingly being scrutinized due to environmental and safety concerns.

Breakthrough research in late 2025 by institutions including the National University of Singapore and the Max Planck Institute demonstrated the feasibility of producing high-purity (R)-Mandelic Acid (>99% enantiomeric excess) using artificial enzyme cascades derived from renewable feedstocks such as glucose and glycerol. This approach represents a paradigm shift toward circular chemistry and low-carbon manufacturing.

Advancements in metabolic engineering have further enhanced commercial viability, with E. coli-based production systems achieving titres of 9.58 g/L, the highest reported yield to date. These innovations eliminate hazardous inputs and align with global regulatory and ESG frameworks.

From a commercial standpoint, leading beauty and personal care companies are actively pursuing bio-based Mandelic Acid sourcing to meet 2030 Net Zero commitments and clean beauty standards. The integration of sustainable ingredients with recyclable packaging ecosystems is expected to redefine product differentiation strategies. Consequently, green Mandelic Acid production is poised to become a high-growth, high-margin segment, attracting investment across biotechnology, specialty chemicals, and advanced skincare markets.

Mandelic Acid Market Share and Segmentation Insights

DL-Mandelic Acid Dominates Commercial Production Through Cost-Efficient Synthesis

DL-mandelic acid held 72.80% of the Mandelic Acid Market share in 2025, making it the most widely produced and commercially utilized form of mandelic acid across pharmaceutical, cosmetic, and chemical manufacturing industries. DL-mandelic acid is a racemic mixture containing equal proportions of D- and L-enantiomers, and it is typically produced through cost-efficient synthetic routes that support large-scale industrial production. This form is widely used in cosmetic formulations, dermatological chemical peels, pharmaceutical intermediates, and specialty chemical synthesis, where high enantiomeric purity is not required for functional performance. The compound’s antibacterial properties, keratolytic activity, and stability in formulation systems have supported its extensive adoption in skincare products and pharmaceutical processing. In 2025, advancements in chiral separation and asymmetric synthesis technologies have begun to influence the market by lowering the cost differential between racemic and optically pure forms. These developments have enabled expanded use of L-mandelic acid in enantioselective pharmaceutical synthesis, particularly in the production of active pharmaceutical ingredients where stereochemical purity significantly influences drug efficacy and safety.

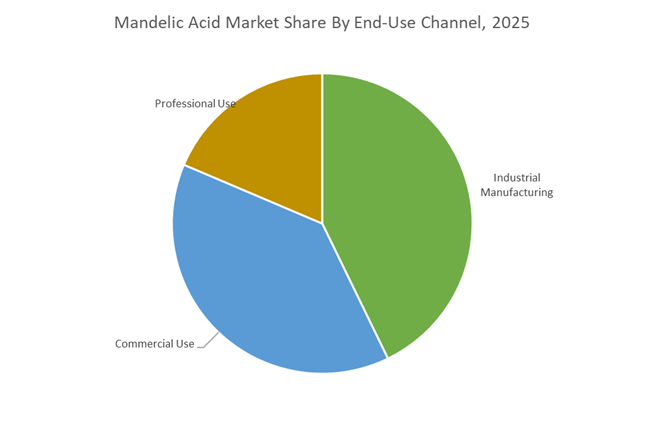

Industrial Manufacturing Channel Drives the Largest Share of Mandelic Acid Consumption

Industrial manufacturing accounted for 42.80% of the Mandelic Acid Market share in 2025, positioning it as the leading end-use channel for mandelic acid production and consumption. Mandelic acid is primarily utilized as a chemical intermediate in pharmaceutical synthesis, cosmetic ingredient manufacturing, and specialty chemical production, making industrial processing facilities the largest buyers of bulk mandelic acid. Pharmaceutical manufacturers use mandelic acid as a key precursor in the synthesis of antibiotics, cardiovascular drugs, and other active pharmaceutical intermediates, while cosmetic ingredient suppliers incorporate it into alpha hydroxy acid (AHA) skincare formulations used for exfoliation, acne treatment, and anti-aging products. Large-scale industrial processing requires consistent supply of high-purity mandelic acid with controlled impurity profiles, supporting strong demand from integrated chemical manufacturers. In 2025, leading producers have increasingly adopted vertically integrated production strategies, including backward integration into raw material supply and forward integration into derivative production such as mandelate salts, esters, and specialty pharmaceutical intermediates, strengthening supply chain control and improving quality assurance across the mandelic acid value chain.

Mandelic Acid Market Competitive Landscape

The mandelic acid market in 2026 is driven by high-purity (≥99.5%) specifications, chiral synthesis (≥98% enantiomeric excess), and biotech-enabled production routes. Competitive dynamics are centered on pharmaceutical-grade intermediates, dermatological AHAs, and green chemistry manufacturing, with Asia-Pacific emerging as the dominant hub for scalable DL-mandelic acid production.

BASF integrates biotech actives and local production to scale high-purity mandelic acid

BASF SE is strengthening its position in specialty mandelic acid through Verbund integration and its “Winning Ways” strategy, combining cost optimization with high-value care chemical innovation. Its Zhanjiang Verbund expansion enhances local supply of aromatic intermediates in Asia-Pacific, while “Beyond Beauty” initiatives integrate mandelic acid into multifunctional, biodegradable cosmetic systems. With strong vertical integration and €2.3 billion cost-saving targets, BASF is aligning high-purity mandelic acid production with climate-adaptive, biotech-driven formulation trends.

Evonik targets sensitive-skin and specialty acid segments with tailored mandelic acid solutions

Evonik Industries is focusing on high-margin mandelic acid applications in cosmeceuticals, positioning it as a low-irritation AHA for sensitive skin formulations and dermatological treatments. Its “Tailor Made” efficiency program supports faster innovation cycles and capital allocation toward specialty acids. With EBITDA guidance up to €2.0 billion and a focus on ROCE optimization, Evonik is advancing customized mandelic acid solutions that balance efficacy and tolerability in high-performance skincare and pharmaceutical formulations.

Hubei Biocause anchors global API supply with large-scale GMP-certified mandelic acid production

Hubei Biocause Pharmaceutical is a key volume supplier in the mandelic acid market, leveraging GMP-certified facilities and CRAM capabilities to serve regulated pharmaceutical markets in the U.S. and EU. With exports to over 85 countries and high-capacity production infrastructure, the company dominates API intermediate supply, particularly for cardiovascular and antibacterial drugs. Its strategic shift toward core biotechnology and chiral intermediate synthesis strengthens its role in high-purity mandelic acid supply chains.

Shengyu Chemical drives cost-efficient DL-mandelic acid production with upgraded purity standards

Shenyang Shengyi Pharmaceutical (Shengyu Chemical) is a major player in bulk DL-mandelic acid, controlling significant global volume through cost-efficient large-scale production. With over 70% of output focused on DL-type material, the company supports dye intermediates and pharmaceutical manufacturing. Upgrades to 99.5% purity standards align with rising demand for medical-grade skincare, while its strong Asia-Pacific footprint positions it as a key price influencer in global mandelic acid supply contracts.

Merck delivers high-purity chiral mandelic acid for precision pharma and advanced skincare

Merck KGaA (Sigma-Aldrich) leads in high-purity chiral mandelic acid, offering D- and L-isomers with >98% enantiomeric excess for pharmaceutical R&D and contract manufacturing. Its solutions support over 45% of CMOs requiring precision intermediates for drug synthesis. Expansion into multifunctional skincare formulations and flexible batch supply strengthens its position among specialty formulators. Through its “Sustainable Science” approach, Merck also provides LCA-backed transparency, aligning with evolving regulatory and sustainability requirements.

United States: Pharmaceutical-Grade Shift and Dermocosmetic Integration

The United States mandelic acid market is undergoing a structural repositioning from a predominantly cosmetic exfoliant toward a high-value pharmaceutical and dermocosmetic intermediate. In late 2025, domestic manufacturers reported a measurable shift toward deploying mandelic acid as a chiral building block for advanced Active Pharmaceutical Ingredients, aligning with the expansion of the U.S. biotech and specialty generics ecosystem. This transition reflects increasing demand for high-purity mandelic acid in stereoselective synthesis, particularly for complex intermediates used in antibiotics and urinary antiseptics. Regulatory momentum is reinforcing this trajectory, with FDA-monitored dossiers tightening and more than 20 new drug filings related to mandelic acid-based therapeutics recorded between 2024 and 2025, elevating compliance requirements and supplier qualification thresholds.

Parallel to pharmaceutical uptake, consumer-led dynamics are reshaping demand in skincare and medical aesthetics. By late 2025, approximately 40% of North American consumers selecting AHA-based skincare products favored mandelic acid over glycolic acid for sensitive skin and post-inflammatory hyperpigmentation applications. This preference is feeding directly into professional dermatology protocols, with 2026 clinical guidelines emphasizing mandelic acid-based “lunchtime peels” offering minimal downtime. Strategic consolidation in clean beauty is amplifying this effect, as acquisitions by groups such as L’Oréal Group have accelerated U.S. demand for pharmaceutical-grade inputs to support premium dermocosmetic pipelines. On the supply side, sustainability considerations are increasingly influential. By Q4 2025, U.S. chemical distributors reported a 15% rise in inquiries for greener synthetic routes, prompting investments in solvent-reduction technologies within the cyanohydrin process and reinforcing ESG-driven procurement criteria.

China: High-Purity Scale, Regulatory Acceleration, and Digital Traceability

China remains the global manufacturing anchor for mandelic acid, producing over 58% of worldwide supply as of early 2026. However, the strategic emphasis has shifted decisively from volume-led output to high-purity DL-type and optically pure L-type and D-type isomers designed to meet stringent pharmaceutical and export standards. This repositioning aligns with the Ministry of Industry and Information Technology’s 2025–2026 chemical industry plan, which targets steady annual value growth while prioritizing high-end specialty intermediates under its advanced supply mandate. Mandelic acid has emerged as a beneficiary of this policy framework due to its relevance in pharmaceuticals, functional skincare, and specialty chemicals.

Regulatory reform is further compressing time-to-market. In 2025, the National Medical Products Administration introduced 24 measures aimed at accelerating approval pathways for innovative ingredients, reducing registration timelines for mandelic acid-based skincare formulations by an estimated 30%. At the operational level, Chinese producers are integrating digitalization under the 2026 Industrial Digital Transformation Blueprint, deploying QR-code batch traceability and AI-driven process optimization to enhance consistency and auditability for international buyers. Innovation at the intermediate level is also material. Regional leaders such as Jiangxi Keyuan Biopharm reported late-2025 advances in precursor synthesis, achieving 15–20% efficiency gains through advanced chlorination technologies. Environmental compliance is becoming non-negotiable, with 2026 mandates requiring closed-loop water systems and energy-efficient distillation across chemical parks, reshaping cost structures and supplier competitiveness.

India: Import-Led Expansion and API-Centric Value Addition

India’s mandelic acid market is characterized by rapid demand expansion coupled with a structural reliance on imports. Trade data indicates 171 shipments between June 2024 and May 2025, representing a 25% year-on-year increase, primarily sourced from China and Germany. This growth is closely tied to India’s positioning as a global hub for pharmaceutical intermediates, particularly mandelic acid derivatives used in antibiotics and urinary antiseptics. Mid-2025 saw a notable surge in imports of high-purity D-mandelic acid to support domestic API manufacturing, reflecting tighter quality requirements and increasing downstream sophistication.

Pricing dynamics underscore this value shift. Bill of Lading data from July 2025 highlights premium pricing for L(+)-mandelic acid at approximately USD 15.60 per kilogram, significantly above racemic DL grades, driven by demand from cosmeceutical and dermatology-focused manufacturers. Policy support is reinforcing domestic value addition. The Production-Linked Incentive scheme for specialty chemicals is facilitating the development of blending and formulation units in Gujarat, enabling processors to convert imported bulk mandelic acid into higher-margin dermatological and pharmaceutical solutions. Simultaneously, a rise in imports of 99% purity laboratory-grade material in 2025 signals expanding R&D activity across academic institutions and private research labs, strengthening India’s role in formulation development rather than primary synthesis.

Germany: Sustainability Benchmarks and Enantiomer Specialization

Germany occupies a premium position in the mandelic acid market through its leadership in sustainable manufacturing and high-purity enantiomer production. In late 2025, major chemical groups such as BASF and Evonik expanded their portfolios of next-generation sustainable actives, with German-produced mandelic acid marketed at a 25–30% lower carbon footprint due to renewable energy integration. This sustainability credential is increasingly decisive for pharmaceutical and dermocosmetic buyers operating under stringent ESG frameworks.

Demand in Germany is heavily skewed toward high-purity D-mandelic acid for stereoselective drug synthesis and advanced pharmaceutical applications. Regulatory leadership is reinforcing this specialization, as German producers are at the forefront of compliance with the 2026 revision of EU REACH standards, offering comprehensive toxicity and environmental impact dossiers that are becoming a benchmark for global exporters. Scientific validation is adding further momentum. Research published in December 2025 by German-affiliated teams identified new mechanisms by which mandelic acid inhibits acne-related inflammation via the PI3K/AKT pathway, providing a credible foundation for next-generation dermatological products entering development cycles in 2026.

Japan: Premium Purity and Functional Diversification

Japan’s mandelic acid market is shaped by exacting purity standards and application-led diversification. In late 2025, Japanese cosmetic manufacturers expanded clean beauty formulations tailored to Asian skin profiles, leveraging mandelic acid’s ability to inhibit tyrosinase and reduce hyperpigmentation without irritation. This has reinforced its positioning as a gentle yet effective AHA within premium skincare portfolios. Procurement behavior reflects this emphasis on quality, with buyers increasingly specifying 98–99% purity grades and moving away from the 97% benchmarks common in more price-sensitive markets.

Beyond cosmetics, Japanese specialty chemical firms are exploring broader industrial applications. Mandelic acid is gaining attention as a stabilizer in premium perfume formulations and as an intermediate in high-end dye synthesis aligned with upcoming fashion cycles. These exploratory pathways indicate a measured but strategic expansion of mandelic acid usage beyond traditional skincare, anchored in Japan’s preference for functional performance, material precision, and long-term supplier reliability.

Comparative Snapshot: Country-Level Strategic Positioning in the Mandelic Acid Market

Mandelic Acid Market County Level Snapshot

|

Country

|

Strategic Focus

|

Key Demand Drivers

|

Regulatory and Policy Influence

|

Supply Chain Orientation

|

|

United States

|

Pharmaceutical-grade APIs and dermocosmetics

|

Chiral synthesis, sensitive-skin AHAs, medical aesthetics

|

FDA dossier tightening, clinical protocol updates

|

Domestic upgrades with sustainability-driven synthesis

|

|

China

|

High-purity scale and export compliance

|

Pharma-grade isomers, functional skincare

|

MIIT growth plan, NMPA fast-track reforms

|

Large-scale manufacturing with digital traceability

|

|

India

|

API intermediates and value-added processing

|

Antibiotics, urinary antiseptics, cosmeceuticals

|

PLI incentives for specialty chemicals

|

Import-led supply with domestic blending and R&D

|

|

Germany

|

Sustainable, high-purity enantiomers

|

Stereoselective drug synthesis, premium dermatology

|

EU REACH 2026 leadership

|

Low-carbon, compliance-driven production

|

|

Japan

|

Premium purity and functional diversification

|

Clean beauty, hyperpigmentation care, specialty chemicals

|

Stringent buyer specifications

|

High-purity imports for advanced formulations

|

Mandelic Acid Market Report Scope

Mandelic Acid Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$356.4 Million

|

|

Market Size (2034)

|

$1441.9 Million

|

|

Market Growth Rate

|

16.8%

|

|

Segments

|

By Type (DL-Mandelic Acid, L-Mandelic Acid), By Purity Grade (Pharmaceutical Grade, Cosmetic and Technical Grade, Reagent Grade), By Application (Pharmaceuticals, Cosmetics and Personal Care, Industrial Applications), By End-Use Channel (Professional Use, Commercial Use, Industrial Manufacturing)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF, Evonik Industries, Jiangxi Keyuan Biopharm, Hanhong Scientific, RL Chemical Industries, Shijiazhuang Hanhong Chemical, Shandong Chengxu Chemical, Lianhe Chemical Technology, Biotec, Haihang Industry, Merck

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Mandelic Acid Market Segmentation

By Type

- DL-Mandelic Acid

- L-Mandelic Acid

By Purity Grade

- Pharmaceutical Grade

- Cosmetic and Technical Grade

- Reagent Grade

By Application

- Pharmaceuticals

- Cosmetics and Personal Care

- Industrial Applications

By End-Use Channel

- Professional Use

- Commercial Use

- Industrial Manufacturing

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Mandelic Acid Market

- BASF

- Evonik Industries

- Jiangxi Keyuan Biopharm

- Hanhong Scientific

- RL Chemical Industries

- Shijiazhuang Hanhong Chemical

- Shandong Chengxu Chemical

- Lianhe Chemical Technology

- Biotec

- Haihang Industry

- Merck

*- List not Exhaustive