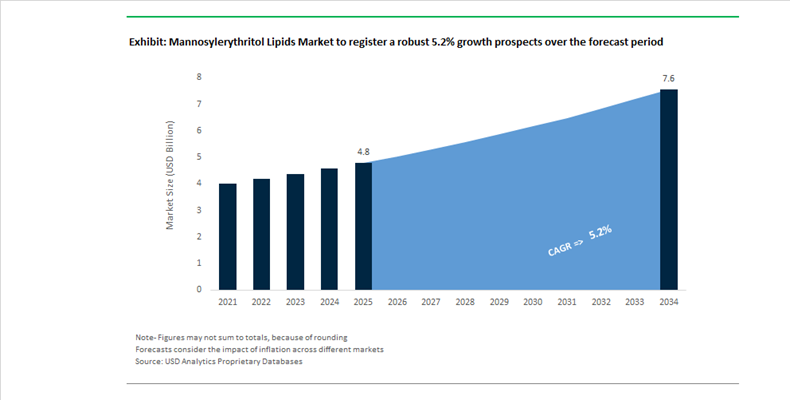

The Mannosylerythritol Lipids (MEL) Market is projected to grow from $4.8 billion in 2025 to $7.6 billion by 2034, registering a CAGR of 5.2%. Market expansion is driven by rising demand for bio-based surfactants, glycolipid biosurfactants, and skin-mimetic ingredients across premium cosmetics, industrial formulations, agriculture, and feed additives. MELs, produced via yeast fermentation, are valued for their emulsification efficiency, biodegradability, antimicrobial functionality, and barrier-repair properties comparable to natural ceramides. Regulatory pressure to reduce petrochemical surfactants and growing consumer preference for vegan, animal-free, and clean-label ingredients are accelerating investment in precision fermentation, sustainable carbon feedstocks, and micro-encapsulation technologies for improved formulation stability.

In February 2024, Toyobo initiated an eight-year high-precision continuous cultivation program supported by Japan’s NEDO under the Bio Manufacturing Revolution Promotion Project, transitioning MEL production from laboratory research to industrial-scale bio-manufacturing. In 2024, the U.S. Environmental Protection Agency expanded TSCA registration for Locus Performance Ingredients’ biosurfactant portfolio, facilitating broader commercialization of glycolipids including MELs in consumer and industrial applications. Research commercialized in 2024 demonstrated the first MEL production using microalgae-derived oil, enabling an animal-free and land-independent supply chain model attractive to premium eco-conscious brands. In early 2025, Locus Fermentation Solutions secured $40 million in investment to scale fermentation infrastructure, addressing one of the primary bottlenecks in glycolipid supply. Throughout 2025, Asian producers including Toyobo and Jiangxi Keyuan shifted toward sugarcane-based carbon sources, leveraging Ustilago scitaminea strains to enhance MEL-B yields with improved cost efficiency.

Strategic diversification and cosmetic integration accelerated in 2025 and early 2026. In early 2025, Vivalto Partners acquired Linnea SA to expand pharmaceutical-grade bio-lipid and specialty surfactant capabilities, indirectly strengthening the high-purity MEL value chain. In September 2025, Evonik launched its Next Markets initiative targeting circular and bio-based chemicals, leveraging biosurfactant expertise to develop broader glycolipid blends including MELs for industrial coatings and advanced personal care. In late 2025, Toyobo began piloting MEL as a pesticide adjuvant and methane-reduction feed additive, positioning it within sustainable agriculture and livestock emissions management strategies. In February 2026, Kao identified precision selective cleansing as a core pillar of its FY2026 plan, integrating MEL into high-end cosmetic brands for barrier repair and profit expansion in global markets. In early 2026, brands introduced clean-label complexes featuring micro-encapsulated MELs to enhance stability in water-based serums, reinforcing MEL’s positioning as a skin-mimetic alternative to synthetic ceramides in next-generation dermatological formulations.

The MELs market has entered a decisive commercialization phase as industrial-scale fermentation removes the historical cost barrier that confined usage to luxury cosmetic brands. Between 2024 and 2025, producers achieved meaningful economies of scale, narrowing the cost differential with specialty synthetic surfactants and enabling MELs to compete directly with sodium lauryl sulfate in mass-market personal care. This transition is structurally important because clean beauty demand is no longer niche driven but mainstream, with retailers and brand owners requiring surfactants that are biodegradable, microbiome friendly, and compliant with tightening consumer safety expectations.

In January 2024, Evonik inaugurated the world’s first industrial-scale rhamnolipid facility in Slovakia, a milestone that catalyzed investor and customer confidence across the entire microbial biosurfactant category, including MELs. By the third quarter of 2025, industry disclosures showed that average microbial biosurfactant production costs had stabilized near USD 5.30 per kilogram, bringing MELs into a commercially viable range for large-volume formulations. Dermatological performance data is reinforcing this shift. Laboratory studies referenced in 2025 consumer goods analyses indicate that MEL-based formulations demonstrate ceramide-like skin affinity and deliver approximately 18% lower cytokine release compared with conventional surfactants, directly addressing irritation concerns. Capacity expansion is also globalizing supply. Kaneka Corporation and Locus Fermentation Solutions expanded green production footprints through late 2024, with Kaneka highlighting adoption of its biosurfactant technologies by large downstream customers such as Starbucks Japan and Sony, providing a replicable manufacturing and logistics model for MELs to penetrate mass-market personal care.

Beyond cosmetics, MELs are rapidly gaining strategic importance in agriculture as multifunctional biostimulants. Unlike conventional adjuvants that act only as wetting agents, MELs function as elicitors that prime plant immune responses while improving soil–water dynamics. This dual functionality is driving adoption across foliar sprays, seed treatments, and soil remediation programs as growers seek yield stability under climate stress and regulatory pressure to reduce synthetic chemical inputs.

Field-level data is accelerating uptake. In January 2025, Locus Agriculture released large-scale U.S. row crop trial results showing that biosurfactant-based biologicals increased yields by 4 to 37% across 23 crop categories, translating into an average incremental return of USD 46 per acre in wheat production. Independent validation further supports efficacy. A 2024 FAO AGRIS report demonstrated that MEL-B homologs at 158 mg per liter increased seed germination and lateral root development by 65%, positioning MELs as both growth promoters and antifungal biocontrol agents. Soil health applications are expanding in parallel. Field data released in October 2024 showed that biosurfactant treatments can alleviate soil compaction affecting roughly 68 million acres of U.S. farmland, preventing yield losses that can reach 60% due to restricted root penetration and water runoff. These outcomes are positioning MELs as cornerstone inputs in regenerative and climate-resilient agriculture systems.

As conventional oil reservoirs mature, MELs are emerging as high-value alternatives to synthetic surfactants in enhanced oil recovery and environmental remediation. Their ability to dramatically reduce interfacial tension under high salinity and temperature conditions gives MELs a technical edge in chemical flooding and microbial EOR programs, particularly in shale and tight reservoirs where oil is trapped in nanopores.

Commercial field performance has validated this opportunity. In November 2025, Locus Bio-Energy reported results from the Delaware Basin showing that wells treated with its SUSTAIN biosurfactant technology achieved a 20% increase in oil production and a 23% reduction in water–oil ratio, delivering a twelve-fold return on investment within six months. Environmental regulation is further expanding demand. Following the U.S. Environmental Protection Agency’s 2024 updates to the National Contingency Plan, oil spill response frameworks now prioritize dispersants that are highly biodegradable and low in aquatic toxicity. MELs, which exceed 90% biodegradability within 28 days, are increasingly positioned as primary alternatives for sensitive marine environments. Broader energy trends reinforce momentum. Public outlooks from the U.S. Energy Information Administration indicate continued growth in global liquid fuel production from mature fields, sustaining long-term demand for biosurfactant-enabled EOR solutions.

The most technologically advanced opportunity for MELs lies in pharmaceutical and nutraceutical delivery systems. MELs naturally self-assemble into stable micelles and vesicles, enabling their use as biocompatible nanocarriers that enhance solubility, cellular uptake, and targeted delivery of active compounds. This capability is attracting increasing R&D investment as drug developers seek alternatives to synthetic lipids that can trigger immune responses.

By 2024, more than 3,200 pharmaceutical formulations globally incorporated biosurfactants to improve bioavailability across multiple therapeutic areas, with MELs favored for their membrane permeability and low immunogenicity. Strategic capital commitments underscore future scale. In its 2025 Strategic Factbook, Evonik disclosed three-digit million euro investments into lipids and biosolutions for mRNA delivery, signaling strong downstream demand for naturally derived lipid components in lipid nanoparticle systems. Clinical research is also advancing. Studies published in MDPI in August 2025 demonstrated that MEL-based nanocarriers can enhance delivery efficiency of neuroprotective and anticancer drugs while reducing systemic toxicity, aligning with the requirements of the rapidly expanding nanocarrier drug delivery segment. As regulatory scrutiny intensifies around excipient safety and biodegradability, MELs are increasingly positioned as next-generation functional lipids for targeted, high-value pharmaceutical applications.

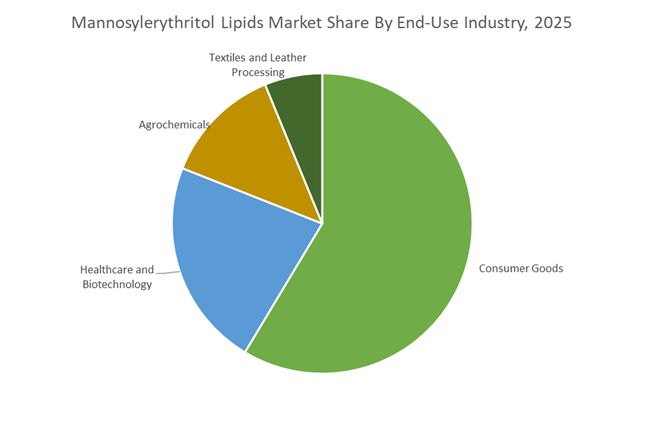

Consumer goods accounted for 58.60% of the Mannosylerythritol Lipids (MEL) Market share in 2025, making it the largest end-use industry for these bio-based surfactants. Mannosylerythritol lipids are microbial glycolipid biosurfactants produced through fermentation, widely valued for their biodegradability, low toxicity, skin compatibility, and excellent emulsification properties. These characteristics make MELs particularly suitable for personal care products, skincare formulations, shampoos, body washes, cosmetics, and eco-friendly household cleaning products. Consumer goods manufacturers increasingly incorporate MELs into product formulations as part of broader efforts to replace conventional petrochemical surfactants with sustainable and naturally derived ingredients. Their ability to deliver effective cleansing, foaming performance, and mildness for sensitive skin supports their adoption in premium cosmetic and hygiene products. In 2025, the growing global demand for green chemistry ingredients and sustainable consumer product formulations has encouraged MEL producers to scale up industrial fermentation capacity and downstream purification processes, improving production efficiency and supporting broader use of MEL biosurfactants in commercial personal care and household product markets.

The consumer goods sector remains the primary driver of demand for mannosylerythritol lipids, as global personal care and home care brands integrate bio-based surfactants into sustainable product portfolios. MELs are increasingly used in facial cleansers, moisturizing creams, hair care formulations, dishwashing liquids, and eco-labeled household detergents, where their emulsifying capacity, moisturizing properties, and biodegradability provide advantages over conventional surfactants. Large consumer product manufacturers are particularly attracted to MELs because they support clean-label ingredient positioning and environmentally responsible formulation strategies, aligning with consumer expectations for natural and sustainable products. In 2025, MEL manufacturers have focused heavily on process optimization and fermentation technology improvements to reduce production costs and expand supply capacity. These developments are enabling MEL ingredients to transition from high-value niche cosmetic applications toward broader use in mass-market personal care and household cleaning products, expanding the addressable market for biosurfactants within the global consumer goods industry.

The mannosylerythritol lipids (MELs) market in 2026 is transitioning toward industrial-scale biomanufacturing, driven by precision fermentation, controlled fatty acid profiles (C8–C14), and high-purity biosurfactants. Competitive dynamics center on continuous cultivation systems, enantiomeric purity, and bio-based surfactants tailored for clean beauty, agrochemicals, and specialty industrial applications.

Toyobo Co., Ltd. is positioning itself as a pioneer in MEL biomanufacturing through its NEDO-backed continuous cultivation systems, aimed at reducing production costs and enabling large-scale commercialization. Its patented MEL technologies and focus on ceramide-mimetic functionality allow positioning beyond surfactants into high-value skincare actives. Expansion into pesticide adjuvants and methane-reduction feed additives highlights diversification of MEL applications. Integration of biotechnology with its Green Strategy reinforces Toyobo’s role in replacing petrochemical surfactants with bio-based functional lipids.

Evonik Industries is leveraging its industrial-scale fermentation infrastructure to expand its glycolipid portfolio, including MELs, within a broader biosurfactant platform. Its Slovakia facility serves as a blueprint for scalable production, while investments exceeding €3 billion in next-generation solutions emphasize biogenic carbon feedstocks and full biodegradability. Strategic distribution expansion in North America accelerates adoption in cleaning and industrial formulations, positioning Evonik as a leader in high-performance, sustainable biosurfactants.

Kao Corporation is advancing MEL applications by combining microbial fermentation with consumer product innovation under its “Kirei World” strategy. Its selection for NEDO biomanufacturing initiatives and development of olfactory receptor analysis technologies enable sensory-enhanced formulations using MELs for emulsification and skin barrier repair. Vertical integration across brands such as Curél and Bioré allows rapid commercialization of MEL-based ingredients, particularly in skincare and hygiene products aligned with clean beauty and sustainability standards.

Kaneka Corporation is leveraging its expertise in fermentation and biodegradable polymers to develop MEL-like functional lipids for medical, pharmaceutical, and specialty applications. Its Green Planet™ platform and decarbonization strategy support the transition toward sustainable chemical production. Expansion into women’s healthcare and collaboration with government-led decarbonization initiatives position Kaneka’s bio-based surfactants as safe, high-performance ingredients for sensitive applications requiring strict regulatory compliance.

Locus Fermentation Solutions is redefining MEL production through modular micro-brewery systems that enable localized, scalable manufacturing of 100% bio-based, PFAS-free biosurfactants. Its Ferma™ glycolipid line delivers multifunctional performance in personal care, combining cleansing and conditioning properties with a low carbon footprint. Integration of bioinformatics accelerates R&D cycles, while its CarbonNOW™ program supports carbon-neutral chemical sourcing. Beyond cosmetics, Locus is expanding into oilfield applications, leveraging MELs for environmentally compliant enhanced oil recovery solutions.

Japan represents the global innovation nucleus of the mannosylerythritol lipids market, with leadership anchored in precision fermentation, diastereomer control, and downstream functional performance validation. In late 2025, Toyobo Co., Ltd. announced the commercial-scale optimization of its proprietary fermentation platform for Ceramela, a glycolipid MEL engineered to replicate the barrier-repair efficacy of natural ceramides. Process refinements across temperature and agitation control during a 14-day fermentation cycle enabled consistently high-purity outputs, positioning MELs as credible bio-based substitutes in premium dermatological formulations. This reinforces Japan’s competitive edge in high-function cosmetic actives rather than commodity biosurfactants.

Beyond personal care, Japan is extending MEL utility into agriculture and household products. Toyobo’s mid-2025 launch of SurfMellow, a yeast-derived MEL biosurfactant, demonstrated superior leaf-surface adhesion at lower application rates compared to petroleum-based adjuvants, significantly enhancing the performance of microbial biocontrol agents. At the molecular level, Japan remains the global leader in selective production of d-MEL-B, with 2025 advances using Pseudozyma tsukubaensis strains pushing yields beyond 73 g/L. Sustainability is increasingly embedded at the brand level, as Kao Corporation integrated biosurfactants into its detergent portfolio under the 2025 K27 strategy to achieve measurable lifecycle CO2 reductions by 2026. Long-term credibility is further supported by a 10-year safety standardization program finalized in 2025 between National Institute of Advanced Industrial Science and Technology and private industry, targeting sensitive-skin medical applications of MEL-A and MEL-B.

Germany’s mannosylerythritol lipids market is defined by scale-up execution, regulatory leadership, and integration into the circular bioeconomy. In 2025, Evonik Industries AG confirmed that its Innovation Growth Areas are delivering accelerated returns, underpinned by world-scale biosurfactant production assets that include glycolipid-based systems. These investments mark a decisive pivot away from fossil-derived surfactants toward industrial-grade biosurfactants capable of meeting performance, consistency, and supply security requirements across cleaning, agriculture, and specialty applications.

Sustainability compliance is not incremental but structural. German MEL producers are adopting ISCC PLUS-certified feedstocks to align with the EU’s 2026 circular economy targets, with Evonik’s Scopeblue portfolio now incorporating glycolipid surfactants that achieve materially lower carbon footprints compared with 2023 baselines. Germany is also leading regulatory groundwork. In preparation for the 2026 REACH revision, German stakeholders are submitting the first comprehensive environmental toxicity and exposure dossiers for MELs in industrial and institutional cleaning uses, effectively shaping global compliance benchmarks. Beyond surfactancy, late-2025 pilot programs in German biotech laboratories validated MELs as lipid carriers for mRNA drug delivery, exploiting their ability to form stable lamellar phases that enhance cellular uptake. This positions MELs as multifunctional bio-lipids rather than single-use surfactants.

The United Kingdom mannosylerythritol lipids market is transitioning from laboratory innovation to early-stage commercialization, driven by partnerships and policy-aligned sustainability funding. In 2026, Holiferm entered a strategic partnership with Cosy Cottage to launch MEL-based personal care and pet care products. This represents the first substantive retail deployment of MELs in the UK as direct replacements for synthetic surfactants, signaling growing confidence in consumer acceptance and supply reliability.

Process innovation is reducing historical cost barriers. In 2025, the Manchester Innovation Lab disclosed a patented gravity-separation fermentation technique that materially lowers energy intensity during MEL purification, addressing one of the principal bottlenecks in biosurfactant economics. Government alignment is reinforcing scale-up prospects, with targeted allocations from the 2025 Green Economy Fund directed toward MEL production platforms that displace palm oil-derived sulfonates in household cleaners. Collectively, these developments position the UK as a commercialization testbed for low-energy, low-impact MEL production rather than a volume manufacturing hub.

In the United States, the mannosylerythritol lipids market is gaining traction through regulatory endorsement and diversification into agriculture and industrial cleaning. The U.S. EPA expanded its Safer Choice criteria in 2025 to accelerate certification pathways for biosurfactants, driving increased demand for MEL-A in industrial-strength bio-degreasers and institutional cleaning formulations. This regulatory validation is reducing buyer risk and accelerating procurement cycles for microbial lipids across public and private sector applications.

Strategic capital reallocation is reshaping the competitive landscape. In December 2025, major chemical conglomerates completed divestments of legacy performance materials businesses to reinvest in advanced precision biosolutions, prioritizing domestic microbial lipid manufacturing capacity. Agricultural applications are emerging as a parallel growth vector. Following USDA assessments highlighting rising synthetic fertilizer costs in 2025, U.S. agribio firms initiated pilot programs deploying MELs as natural antimicrobial agents capable of inhibiting fungal pathogens in high-value berry crops. These developments underscore the U.S. market’s orientation toward regulatory-backed, application-driven adoption rather than upstream fermentation leadership.

China’s mannosylerythritol lipids market is advancing rapidly through policy prioritization, scale economics, and process digitalization. Under the MIIT High-end Chemical Supply roadmap for 2026, biosurfactants including MELs are formally designated as strategic specialty chemicals, catalyzing investment in fermentation capacity and purification infrastructure. In 2025, Chinese producers expanded output of 98% and higher purity MEL-C grades, targeting the fast-growing C-Beauty segment where performance consistency and sensory attributes are critical.

Operational excellence is being reinforced through digital tools. Leading manufacturers in Jiangsu implemented AI-driven fermentation monitoring systems in late 2025, achieving an 18% reduction in batch-to-batch variability in glycolipid structure. This improvement directly enhances suitability for cosmetics and specialty applications that demand molecular uniformity. China’s trajectory emphasizes scale combined with tightening quality control, positioning the country as a dominant supplier across both domestic and export-oriented MEL value chains.

|

Country / Region |

Strategic Emphasis |

Core Applications |

Policy and Regulatory Influence |

Competitive Differentiation |

|

Japan |

Precision fermentation and diastereomer control |

Premium cosmetics, agricultural adjuvants |

Long-term safety standardization |

High-purity MEL-B leadership |

|

Germany |

World-scale biosurfactants and compliance |

Industrial cleaning, pharma delivery |

REACH 2026 and circular economy mandates |

Regulatory benchmark setting |

|

United Kingdom |

Commercial pilots and energy-efficient processes |

Personal care, pet care |

Green Economy funding |

Low-energy purification innovation |

|

United States |

Regulatory-backed demand and agro-bio use |

Industrial degreasers, crop protection |

EPA Safer Choice expansion |

Application-driven adoption |

|

China |

Capacity scale and digital process control |

Cosmetics, specialty chemicals |

MIIT high-end supply roadmap |

High-purity MEL-C at scale |

|

Parameter |

Details |

|

Market Size (2025) |

$4.8 Billion |

|

Market Size (2034) |

$7.6 Billion |

|

Market Growth Rate |

5.2% |

|

Segments |

By Type (Mannosylerythritol Lipids), By Purity Grade (Pharmaceutical Grade, Cosmetic Grade, Industrial Grade), By Application (Personal Care and Cosmetics, Household and Industrial Cleaning, Pharmaceuticals, Agriculture, Food and Beverage), By End-Use Industry (Consumer Goods, Healthcare and Biotechnology, Agrochemicals, Textiles and Leather Processing) |

|

Study Period |

2019- 2025 and 2026-2034 |

|

Units |

Revenue (USD) |

|

Qualitative Analysis |

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking |

|

Companies |

Toyobo, Kao Corporation, Evonik Industries, Holiferm, Kanebo Cosmetics, Kyowa Hakko Bio, Damy Chemicals, Solvay, GlycoSurf, Locus Fermentation Solutions, Allied Carbon Solutions, Shaanxi Deguan Biotechnology, Jeneil Biotech, Givaudan, Kaneka Corporation |

|

Countries |

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa |

*- List not Exhaustive

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

2. Mannosylerythritol Lipids Market Landscape & Outlook (2025–2034)

2.1. Introduction to Mannosylerythritol Lipids Market

2.2. Market Valuation and Growth Projections (2025–2034)

2.3. Bio-Based Surfactant Demand and Clean Label Transition

2.4. Fermentation Scale-Up and Sustainable Carbon Feedstocks

2.5. Cosmetic, Industrial, and Agricultural Application Expansion

3. Innovations Reshaping the Mannosylerythritol Lipids Market

3.1. Trend: Industrial Fermentation Scale-Up and Cost Optimization

3.2. Trend: MELs as Multifunctional Biostimulants in Agriculture

3.3. Opportunity: Enhanced Oil Recovery and Environmental Remediation Applications

3.4. Opportunity: MEL-Based Nanocarriers for Drug Delivery Systems

4. Competitive Landscape and Strategic Initiatives

4.1. Mergers and Acquisitions

4.2. R&D in Precision Fermentation and Glycolipid Engineering

4.3. Sustainability and Circular Bio-Based Production Strategies

4.4. Market Expansion and Regional Manufacturing Scale-Up

5. Market Share and Segmentation Insights: Mannosylerythritol Lipids Market

5.1. By Type

5.1.1. Mannosylerythritol Lipids

5.2. By Purity Grade

5.2.1. Pharmaceutical Grade

5.2.2. Cosmetic Grade

5.2.3. Industrial Grade

5.3. By Application

5.3.1. Personal Care and Cosmetics

5.3.2. Household and Industrial Cleaning

5.3.3. Pharmaceuticals

5.3.4. Agriculture

5.3.5. Food and Beverage

5.4. By End-Use Industry

5.4.1. Consumer Goods

5.4.2. Healthcare and Biotechnology

5.4.3. Agrochemicals

5.4.4. Textiles and Leather Processing

5.5. By Region

5.5.1. North America

5.5.2. Europe

5.5.3. Asia Pacific

5.5.4. South and Central America

5.5.5. Middle East and Africa

6. Country Analysis and Outlook of Mannosylerythritol Lipids Market

6.1. United States

6.2. Canada

6.3. Mexico

6.4. Germany

6.5. France

6.6. Spain

6.7. Italy

6.8. UK

6.9. Russia

6.10. China

6.11. India

6.12. Japan

6.13. South Korea

6.14. Australia

6.15. South East Asia

6.16. Brazil

6.17. Argentina

6.18. Middle East

6.19. Africa

7. Mannosylerythritol Lipids Market Size Outlook by Region (2025–2034)

7.1. North America Mannosylerythritol Lipids Market Size Outlook to 2034

7.1.1. By Type

7.1.2. By Purity Grade

7.1.3. By Application

7.1.4. By End-Use Industry

7.1.5. By Region

7.2. Europe Mannosylerythritol Lipids Market Size Outlook to 2034

7.2.1. By Type

7.2.2. By Purity Grade

7.2.3. By Application

7.2.4. By End-Use Industry

7.2.5. By Region

7.3. Asia Pacific Mannosylerythritol Lipids Market Size Outlook to 2034

7.3.1. By Type

7.3.2. By Purity Grade

7.3.3. By Application

7.3.4. By End-Use Industry

7.3.5. By Region

7.4. South America Mannosylerythritol Lipids Market Size Outlook to 2034

7.4.1. By Type

7.4.2. By Purity Grade

7.4.3. By Application

7.4.4. By End-Use Industry

7.4.5. By Region

7.5. Middle East and Africa Mannosylerythritol Lipids Market Size Outlook to 2034

7.5.1. By Type

7.5.2. By Purity Grade

7.5.3. By Application

7.5.4. By End-Use Industry

7.5.5. By Region

8. Company Profiles: Leading Players in the Mannosylerythritol Lipids Market

8.1. Toyobo

8.2. Kao Corporation

8.3. Evonik Industries

8.4. Holiferm

8.5. Kanebo Cosmetics

8.6. Kyowa Hakko Bio

8.7. Damy Chemicals

8.8. Solvay

8.9. GlycoSurf

8.10. Locus Fermentation Solutions

8.11. Allied Carbon Solutions

8.12. Shaanxi Deguan Biotechnology

8.13. Jeneil Biotech

8.14. Givaudan

8.15. Kaneka Corporation

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures

The Mannosylerythritol Lipids Market was valued at $4.8 billion in 2025 and is projected to reach $7.6 billion by 2034, expanding at a CAGR of 5.2%. Growth is driven by increasing replacement of petrochemical surfactants with bio-based alternatives. Expansion of fermentation capacity and clean-label demand are accelerating adoption. Cosmetics and consumer goods remain the primary growth engines.

The transition to industrial-scale fermentation is removing historical cost barriers associated with MEL production. Investments by companies such as Locus Fermentation Solutions and Toyobo are improving yield efficiency and reducing unit costs. Production costs for biosurfactants have stabilized, enabling MELs to compete with synthetic surfactants. This shift is expanding adoption from premium cosmetics into mass-market personal care and cleaning products.

MELs are increasingly positioned as skin-mimetic ingredients with ceramide-like barrier repair functionality. Their low irritation profile and microbiome compatibility make them suitable for sensitive skin formulations. Micro-encapsulation technologies introduced in 2026 are improving stability in water-based serums. This is driving adoption in premium skincare, particularly in Asia and Europe.

MELs are gaining traction in agriculture as multifunctional biostimulants that enhance crop yield and soil health. In energy, they are used in enhanced oil recovery due to their ability to reduce interfacial tension under extreme conditions. Pharmaceutical applications are expanding with MEL-based nanocarriers for targeted drug delivery. These diversified applications are creating new high-margin growth avenues.

Key players include Toyobo, Evonik Industries, Kao Corporation, Kaneka Corporation, and Locus Fermentation Solutions. These companies are investing in precision fermentation, continuous cultivation, and bio-based feedstocks. Strategic focus includes scaling production, expanding into agriculture and pharma applications, and integrating MELs into consumer products. Partnerships and government-backed programs are accelerating commercialization globally.