Unprecedented Growth in the Medical Coatings Market: Value, CAGR, and Future Outlook

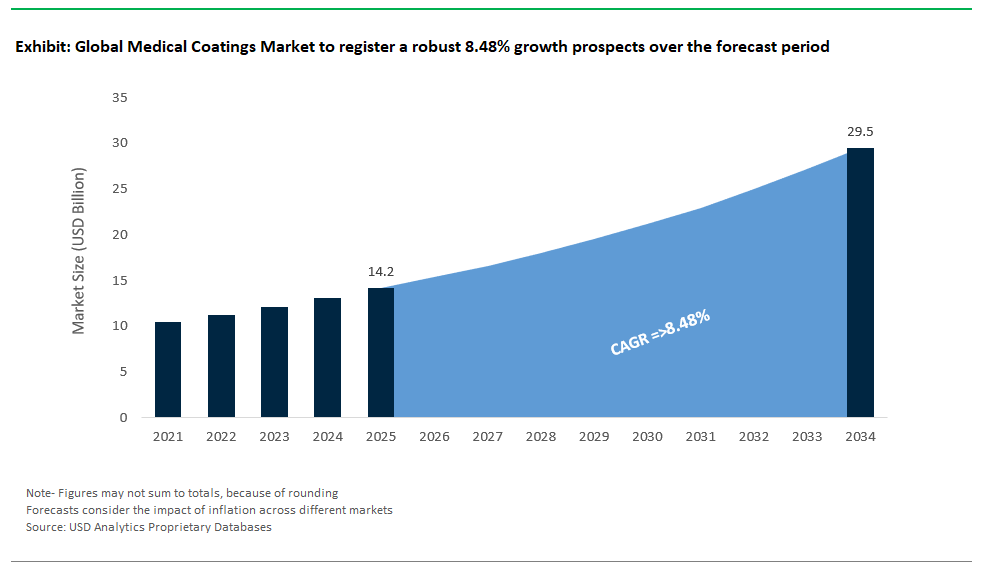

The medical coatings market is on its path of growth at a rapid pace, expected to reach USD 14.2 billion by 2025 from USD 14.2 billion in 2017, soaring in the rate of nearly double as of 2034 at a 8.48% CAGR. This growth is fueled by the continuous advancements in medical technologies, an increase in the number of minimally invasive surgeries performed and rising regulatory requirements for performance and patient safety of medical devices. With increasing sophistication and specialization of medical devices, the demand for advanced surface treatments that improve performance and biocompatibility, and provide safety, is rising exponentially, making medical coatings a key enabler in the global medtech industry.

Medical coatings are instrumental in increasing the quality and efficiency of the latest medical devices, implants and surgical instruments. Designed for a great deal more than appearance, these coatings provide key functional attributes - bio-compatibility, lower friction for easy device navigation (lubricious), local activation of drug therapies, and prevention of corrosion and microbial colonization. With various coating technologies such as hydrophilic, antimicrobial, drug-eluting, and anti-thrombogenic, they can be used for cardiovascular, orthopedic, dental, and diagnostic devices. The continuous evolution of the industry drives by these advancements is also bringing the technology closer to fulfilling its promise of adding unique, tailored surface treatments with the highest medical and biocompatibility requirements, to improve patient outcomes and prevent infections, pushing for continuous market innovation and adoption.

Dynamic Market Movements: Recent Innovations and Strategic Shifts in Medical Coatings

The Medical Coatings Market is witnessing a surge of product launches, technology advancements, and strategic partnerships, all underscoring its pivotal role in modern healthcare. In July 2025, Hydromer expanded its hydrophilic coating portfolio with a new biocompatible variant, enhancing the lubricity and safety of catheters and guidewires a direct response to the booming demand for minimally invasive procedures. Around the same time, Surmodics announced the commercial rollout of its next-generation lubricious coating, engineered for superior durability and reduced particulate generation, especially valuable in complex cardiovascular interventions.

In June 2025, DSM Biomedical spotlighted a novel bioactive coating for orthopedic implants, promising faster bone integration and reduced infection risks, marking a leap in implant surface modification. Biocoat Inc. followed in May with a major manufacturing expansion for its hydrophilic coatings in Pennsylvania, addressing surging global requirements for lubricious coatings in medical devices. April saw Covalon Technologies Ltd. introduce an antimicrobial-coated surgical drape, extending infection control technologies beyond devices to surgical environments. In March, Harland Medical Systems launched the CTS1200, an automated dip coating system designed for precision and consistency in coating complex device geometries, mirroring the industry’s pivot to automation and stringent quality control.

The momentum continued with Hydromer’s February release of PFAS-free hydrophilic coatings, responding to increasing environmental and regulatory scrutiny around chemical safety. In January 2025, PPG Industries unveiled new biocompatible coatings for in-vitro diagnostic devices, elevating assay reliability. Late 2024 saw Freudenberg Medical acquire a European specialty coating provider, strengthening capabilities in PTFE and silicone coatings, and AST Products partner with a university for novel anti-thrombogenic coating development. Collectively, these strategic moves highlight the sector’s focus on infection control, sustainability, automation, and advancing device performance.

Trends and Opportunities Transforming the Medical Coatings Industry

Antimicrobial Medical Coatings Propel Infection Control Innovation

A defining trend in the Medical Coatings Market is the explosive rise in demand for antimicrobial coatings. Driven by the persistent threat of hospital-acquired infections (HAIs) and mounting antibiotic resistance, medical device manufacturers and healthcare facilities are rapidly adopting coatings that inhibit bacterial adhesion and biofilm formation. Studies indicate that antimicrobial-coated devices can reduce HAIs by as much as 38%, underscoring their value in safeguarding patient outcomes. Global regulatory agencies now prioritize infection prevention, with governments such as the U.S. Department of Health and Human Services allocating significant budgets to infection control technologies. The increasing number of invasive procedures and indwelling devices catheters, stents, and joint replacements further amplifies the need for reliable antimicrobial solutions. The April 2025 launch of Covalon’s antimicrobial surgical drape illustrates the expanding application of these coatings, while ongoing R&D efforts are unlocking new silver-ion, peptide, and quaternary ammonium-based formulations. The long-term impact is a measurable reduction in healthcare-associated infections, greater patient safety, and a paradigm shift in medical device design toward inherent infection resistance.

Lubricious Coatings Enable Breakthroughs in Minimally Invasive Surgery

The rapid shift toward minimally invasive surgery (MIS) is generating robust demand for hydrophilic and lubricious coatings on medical devices. As procedures like angioplasty, endoscopy, and neurovascular interventions rely on the precise navigation of flexible, friction-sensitive instruments, coatings that reduce device resistance are essential. Hydromer’s July 2025 product expansion and Biocoat Inc.’s manufacturing growth highlight how market leaders are responding to this trend. These coatings ensure smoother insertion, minimize tissue trauma, and improve maneuverability, directly contributing to procedural success and faster patient recovery. Industry data project continued growth for hydrophilic coatings, supported by new PFAS-free formulations (as seen with Hydromer) and hybrid coatings that combine lubricity with antimicrobial or drug-eluting features. Advanced application technologies, such as Harland’s automated dip coating, are crucial for uniform coverage of complex device shapes. The result: broader adoption of MIS techniques, fewer complications, reduced costs, and a new standard of patient care.

Competitive Landscape: Key Innovators Shaping the Medical Coatings Market

The global Medical Coatings Market is defined by a mix of specialty coating providers, multinational chemical firms, and integrated medtech suppliers, each advancing technology and market reach.

Hydromer Advances Hydrophilic and PFAS-Free Coating Technologies

Hydromer Inc. leads in the development of hydrophilic and biocompatible coatings, serving catheters, guidewires, and minimally invasive instruments. The July 2025 launch of its HydroGlide biocompatible variant, alongside the February 2025 debut of PFAS-free coatings, underscores Hydromer’s commitment to safety, performance, and regulatory compliance. Their global expansion and broad portfolio spanning lubricious, anti-thrombogenic, and custom formulations position Hydromer at the forefront of sustainable, next-generation medical coatings.

DSM-Firmenich Delivers Bioactive and Drug-Eluting Coatings for Implants

DSM-Firmenich, through its DSM Biomedical division, is renowned for bioactive, biocompatible, and drug-eluting coatings used in cardiovascular, orthopedic, and dental devices. The June 2025 introduction of a new bioactive coating for orthopedic implants advances bone integration and infection reduction. With global operations and a strong emphasis on innovation, DSM-Firmenich is a leader in disruptive coating technologies that address unmet clinical needs and enhance device performance.

Surmodics Leads in Durable Lubricious and Surface Modification Technologies

Surmodics, Inc. specializes in highly durable, lubricious, and drug-delivery coatings for interventional devices. The July 2025 rollout of next-generation lubricious technology reflects Surmodics’ mission to improve device safety and performance critical for regulatory approval and market success. The company’s integrated solutions include coating formulations and turnkey application services, supporting OEMs in delivering superior minimally invasive products.

Biocoat Inc. Expands Hydrophilic Coatings and Full-Service Solutions

Biocoat Inc. provides comprehensive hydrophilic coating solutions, including abrasion-resistant, biocompatible formulations and coating application equipment. The May 2025 expansion of its manufacturing capabilities addresses surging demand, while its EMERSE product line ensures precision in dip coating. Biocoat’s end-to-end offering from materials development to application technology supports medical device makers in achieving consistent, high-performance results.

Covalon Technologies Drives Innovation in Antimicrobial and Infection Control Coatings

Covalon Technologies Ltd. is a leader in antimicrobial coatings and patented infection control solutions for medical devices and surgical products. The April 2025 launch of its antimicrobial-coated surgical drape highlights Covalon’s push beyond device coatings into broader clinical environments. The company’s proprietary CovaBond™ and Covalon® antimicrobial technologies continue to set industry benchmarks for reducing hospital-acquired infections and improving patient outcomes.

Medical Coatings Market Share Analysis: Coating Type and Application Insights for 2025

Hydrophilic and Antimicrobial Coatings Reshape the Market’s Competitive Landscape

Hydrophilic/lubricious coatings command a leading 28% share of the global medical coatings market in 2025, underpinned by the rapid adoption of minimally invasive surgery (MIS) techniques and the growing use of guidewires, catheters, and endovascular devices that demand ultra-low friction performance. Antimicrobial coatings, with a 22% share, have surged in importance due to heightened awareness of hospital-acquired infections (HAIs), a trend amplified in the wake of COVID-19. The market is also experiencing robust growth in drug-eluting coatings, now expanding beyond cardiovascular stents into orthopedic implants for controlled drug delivery and infection prevention. Anti-thrombogenic coatings are essential for blood-contacting devices such as heart valves and dialysis equipment, supporting safer long-term implantation. Other segments, including biocompatible, radiopaque, corrosion-resistant, and wear-resistant coatings, collectively address niche but critical demands ranging from improved imaging visibility to extended instrument life and implant acceptance. The ongoing focus on next-generation hybrid operating rooms and robotic-assisted procedures is further stimulating demand for multifunctional, high-performance coatings.

.png)

Applications: Medical Devices and Implants Anchor Coating Demand

Medical devices are the primary application for medical coatings, accounting for 40% of the market, with catheters, guidewires, and injection devices leading the charge. These applications rely heavily on hydrophilic and antimicrobial coatings to ensure patient safety, comfort, and device longevity. Medical implants, comprising 30% of demand, are increasingly benefiting from drug-eluting and biocompatible coatings to enhance healing and integration in orthopedic, cardiovascular, and dental applications. Surgical instruments and tools (20%) prioritize corrosion and wear-resistant coatings to enable repeated sterilization and maintain precision, while the in-vitro diagnostics (IVD) segment (7%) uses specialized coatings to deliver anti-fouling properties crucial for accuracy in microfluidic and biosensor devices. The remaining market wearable sensors, robotics, and specialty devices reflects the sector’s broadening scope as advanced coatings enable new frontiers in minimally invasive and personalized medicine.

United States: Innovation Powerhouse in Advanced Medical Coatings

The United States is the global leader in medical coatings innovation and commercialization. With more than $30 billion invested in nanotechnology since 2001 through the National Nanotechnology Initiative (NNI), the U.S. has established a robust ecosystem for the development of advanced nanocoatings, plasma spray, and drug-eluting technologies. Federal agencies like the NIH and FDA set high benchmarks for safety, efficacy, and biocompatibility, prompting manufacturers to continually upgrade their coatings for regulatory compliance and patient outcomes. Major medical device hubs including Minnesota, California, and Massachusetts drive substantial demand for antimicrobial, hydrophilic, and drug-eluting coatings in cardiovascular, orthopedic, and neurovascular segments. Expansion by top coating firms such as Hydromer, Surmodics, and Biocoat underscores the U.S.’s ongoing leadership in R&D and production. The country’s focus on infection control and device safety ensures sustained demand for next-generation medical coatings across devices and implants.

Further reinforcing its global dominance, the U.S. is also at the cutting edge of coating solutions for surgical tools, wearables, and diagnostic devices, supported by a highly collaborative ecosystem of academia, research hospitals, and private industry. Stringent FDA approval processes drive continuous innovation in coating safety, durability, and performance, making the U.S. a reference point for global best practices in the medical coatings sector.

Germany: Precision Engineering and Regulatory Leadership

Germany stands at the forefront of precision engineering and high-performance medical coatings, driven by strong investments in R&D and a highly developed medical device industry. The focus on proprietary technologies like Endexo® from Evonik Health Care demonstrates leadership in biocompatibility and surface modification. PVD (Physical Vapor Deposition) and CVD (Chemical Vapor Deposition) technologies are widely used in Germany for applying thin, durable coatings to implants and surgical instruments, ensuring compliance with stringent EU Medical Device Regulations (MDR). The country is a major hub for orthopedic, dental, and cardiovascular devices, each demanding specialized coatings for enhanced safety and longevity.

German companies also pioneer anti-thrombogenic and anti-inflammatory coatings for stents and implants, pushing boundaries in cardiovascular innovation. The strategic emphasis on quality, regulatory compliance, and high-precision manufacturing has cemented Germany’s reputation as a global leader in functional and durable medical coatings, with growing activity in wear-resistant and smart coatings for next-generation applications.

China: Expanding Infrastructure and Cost-Effective Innovation

China is rapidly emerging as both a manufacturing powerhouse and a high-potential consumer market for medical coatings. National initiatives such as “Made in China 2025” promote the domestic development of advanced medical devices and high-value coatings, supporting an expansive and modernizing healthcare sector. China is witnessing significant investments in advanced coating techniques including plasma spray, antimicrobial, and biocompatible solutions to meet domestic demand for orthopedic implants, cardiovascular stents, and surgical instruments. Local companies are scaling up production and seeking global partnerships for technology transfer and R&D.

The regulatory landscape is evolving, with increasing emphasis on product safety, quality, and traceability, bringing Chinese coatings more in line with global standards. As the sector grows, China is developing cost-effective yet high-performance coatings to support its large-scale healthcare infrastructure and rising middle-class demand for sophisticated, safe medical devices.

Japan: Pioneering Nanotechnology and Bioactive Coatings

Japan’s medical coatings market is defined by a strong foundation in biomaterials science and nanotechnology. Continuous R&D focuses on the development of ultra-thin, highly functional coatings such as nanocoatings for drug delivery and improved device integration. Japanese manufacturers are recognized for their leadership in cardiovascular, neurovascular, and dental coatings, meeting strict regulatory standards for performance and patient safety.

Government initiatives promote collaborative research between academia and industry, fostering breakthrough coatings with bioactive and anti-thrombogenic properties that speed healing and enhance implant acceptance. Japan’s innovation ecosystem consistently delivers advanced coatings for both traditional medical devices and new fields like wearable sensors and precision diagnostics, solidifying its position as a global leader in medical coatings science.

South Korea: Regional Hub for High-Tech Medical Coatings

South Korea is rapidly strengthening its position as a regional leader in medical coatings, with heavy investment in R&D for drug-eluting stents, orthopedic implants, and advanced antimicrobial solutions. Korean companies excel in smart surface modification technologies and integration of nanomaterials, driving innovation in cardiovascular and orthopedic applications. Government support for medical device manufacturing and high-tech material R&D is accelerating the country’s capabilities in high-precision coatings.

South Korea’s strategic focus on innovation, export growth, and global partnerships ensures rising competitiveness in both domestic and international markets for advanced medical coatings, particularly as demand grows for infection prevention and long-term implant success.

United Kingdom: Focused on Functional and Sustainable Coating Solutions

The UK combines strong academic research with industry expertise in biomaterials and surface engineering to develop next-generation medical coatings. Government funding and policy initiatives address public health challenges such as HAIs, supporting market demand for advanced antimicrobial and hydrophilic coatings in orthopedic implants, surgical instruments, and cardiovascular devices.

UK-based companies and research groups are at the forefront of developing functional coatings that enhance device biocompatibility, reduce infection risks, and enable minimally invasive procedures. The regulatory environment is adapting post-Brexit but continues to align closely with EU standards, maintaining high safety and performance requirements for coatings and finished devices.

France: Expertise in Polymer Chemistry and High-Performance Medical Coatings

France’s medical coatings sector is built on strong polymer chemistry expertise, supporting the development of hydrophilic, drug-eluting, and biocompatible formulations for cardiovascular, orthopedic, and surgical applications. R&D activity is robust, with focus on advancing the properties and safety of coatings used in implants and surgical tools.

French companies contribute to the European medical coatings landscape with their emphasis on performance, safety, and regulatory compliance. The strict EU MDR framework governs device safety and coating standards, pushing continuous improvement and quality assurance in coating application and testing.

Switzerland: Global Leader in Precision and Biocompatible Coatings

Switzerland is synonymous with precision medical technology and advanced materials science. The country’s medical coatings industry specializes in high-precision, long-lasting coatings for complex implants and surgical tools, utilizing state-of-the-art PVD and CVD deposition techniques. Stringent SwissMedic and EU MDR regulations ensure the highest standards for device and coating safety.

Swiss companies are renowned for developing highly durable, biocompatible, and wear-resistant coatings tailored for orthopedic, dental, and cardiovascular implants, maintaining the country’s reputation as a premier source of high-quality medical coatings for critical healthcare applications.

Medical Coatings Market Report Scope

Medical Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$14.2 Billion

|

|

Market Size (2034)

|

$29.5 Billion

|

|

Market Growth Rate

|

8.48%

|

|

Segments

|

By Coating Type (Hydrophilic/Lubricious Coatings, Antimicrobial Coatings, Drug-Eluting Coatings, Anti-Thrombogenic Coatings, Biocompatible Coatings, Corrosion-Resistant Coatings, Wear-Resistant Coatings, Radiopaque Coatings, Others)

By Material (Polymer Coatings, Metallic Coatings, Ceramic Coatings, Nanocoatings, Others)

By Application (Medical Devices, Medical Implants, Surgical Instruments & Tools, In-vitro Diagnostic Devices, Others)

By End-Use Industry (Hospitals & Clinics, Ambulatory Surgical Centers, Medical Device Manufacturers, Research & Academic Institutions, Other Healthcare Facilities

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Hydromer Inc., DSM-Firmenich, Surmodics, Inc., Biocoat Inc., Covalon Technologies Ltd., Harland Medical Systems Inc., PPG Industries, Freudenberg Medical, AST Products Inc., Specialty Coating Systems (SCS), Heraeus Group, Medicoat AG, Precision Coating Company, Inc., Endura Coatings, Applied Medical Coatings

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Medical Coatings Market Segmentation

By Coating Type

- Hydrophilic/Lubricious Coatings

- Antimicrobial Coatings

- Drug-Eluting Coatings

- Anti-Thrombogenic Coatings

- Biocompatible Coatings

- Corrosion-Resistant Coatings

- Wear-Resistant Coatings

- Radiopaque Coatings

- Others

By Material

- Polymer Coatings

- Metallic Coatings

- Ceramic Coatings

- Nanocoatings

- Others

By Application

- Medical Devices

- Medical Implants

- Surgical Instruments & Tools

- In-vitro Diagnostic Devices

- Others

By End-Use Industry

- Hospitals & Clinics

- Ambulatory Surgical Centers

- Medical Device Manufacturers

- Research & Academic Institutions

- Other Healthcare Facilities

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Medical Coatings Market

- Hydromer Inc.

- DSM-Firmenich

- Surmodics, Inc.

- Biocoat Inc.

- Covalon Technologies Ltd.

- Harland Medical Systems Inc.

- PPG Industries

- Freudenberg Medical

- AST Products Inc.

- Specialty Coating Systems (SCS)

- Heraeus Group

- Medicoat AG

- Precision Coating Company, Inc.

- Endura Coatings

- Applied Medical Coatings

* List Not Exhaustive