Market Analysis: Strategic Acquisitions and Next-Gen Technologies Drive the Medical Devices Market

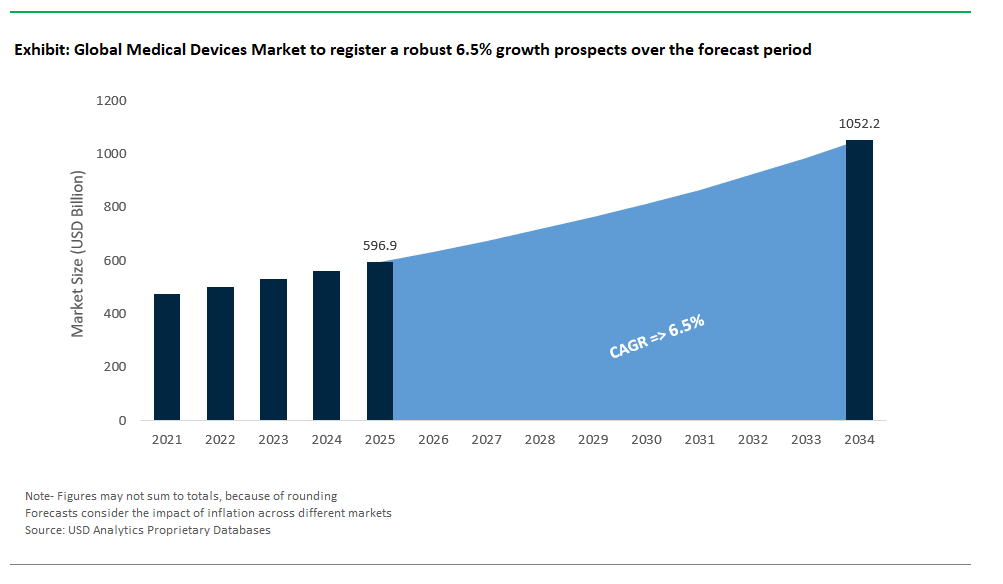

The Global Medical Devices Market Size is estimated at $596.9 Billion in 2025 and is forecast to register an annual growth rate (CAGR) of 6.5% to reach $1052.1 Billion by 2034.

The medical devices market is undergoing rapid transformation, marked by a wave of strategic acquisitions and breakthrough technological advancements. In July 2025, Innovia Medical expanded its specialized surgical instruments portfolio by acquiring both Grace Medical, known for single-use ENT implants, and Hurricane Medical, a producer of ophthalmic surgical devices. Similarly, EnChannel bolstered its electrophysiology R&D with the acquisition of Acutus Medical’s AcQMap high-resolution imaging platform and associated catheter devices, enhancing its capabilities in cardiac diagnostics and mapping.

Expansion into advanced eye care and minimally invasive solutions is also reshaping the sector. EssilorLuxottica’s acquisition of Optegra significantly broadens its reach from eyewear into AI-powered medtech and surgical instruments, strengthening its footprint in the European ophthalmology market. Quasar Medical grew its manufacturing presence and technological capacity with the acquisition of Nordson’s contract manufacturing businesses in Ireland and Mexico, while Merit Medical expanded its wound care portfolio by acquiring Biolife Delaware, the developer of StatSeal and WoundSeal hemostatic devices for post-procedural care. Additionally, Resonetics invested in U.S.-based nitinol gun drilling operations from Medical Component Specialists, advancing domestic production of critical device components.

High-value deals and innovations continue to shape the medical devices market. In May 2024, Johnson & Johnson MedTech completed its $13.1 billion acquisition of Shockwave Medical, gaining access to intravascular lithotripsy (IVL) technology for cardiovascular interventions reinforcing J&J’s leadership in heart vessel treatments. Meanwhile, CMR Surgical’s Versius robotic system surpassed 5,000 global procedures, highlighting the steady growth and adoption of robotic-assisted surgery. At the forefront of therapeutic innovation, Francis Medical is advancing a transurethral ablation device for prostate cancer using water vapor to selectively target cancer cells, with plans to extend its benefits to kidney and bladder cancers.

Collectively, these developments underscore a dynamic and competitive global medical devices market, where acquisitions, robotics, AI-powered medtech, and novel therapies are reshaping healthcare delivery. As leading companies expand portfolios, invest in cutting-edge manufacturing, and deploy next-gen surgical technologies, the market is poised for continued innovation and growth across a diverse range of clinical specialties.

Key Innovations in the Medical Devices Market

Trend: AI-Enabled Predictive Recalls for Implantable Devices

The medical devices market is rapidly advancing with the integration of AI-enabled predictive recall systems, marking a critical shift in patient safety and device lifecycle management. Leveraging cloud-based artificial intelligence and real-time analytics, these systems can identify early indicators of component failures such as pacemaker lead degradation well before traditional monitoring methods detect issues. This proactive capability significantly reduces the risk of sudden device malfunctions, mitigating the need for emergency surgical interventions and enhancing long-term patient outcomes.

Regulatory bodies are playing an instrumental role in accelerating adoption through initiatives that fast-track the approval of AI-driven predictive maintenance algorithms. These programs streamline the review process for digital health innovations, enabling quicker integration into clinical workflows. As a result, post-market surveillance is becoming more dynamic, improving device reliability and fostering stronger trust between manufacturers, healthcare providers, and patients. With AI technology evolving rapidly, predictive recall solutions are poised to become a standard feature for high-risk implantable devices, redefining safety protocols and operational efficiency in the medical devices industry.

Opportunity: 3D-Printed Bioresorbable Pediatric Airway Stents

A transformative opportunity in the medical devices sector lies in the development of 3D-printed bioresorbable airway stents tailored for pediatric patients with severe airway disorders, such as tracheobronchomalacia. Traditional metallic stents pose significant challenges, including high complication rates and the need for repeated surgical removal. In contrast, bioresorbable stents, created from advanced materials like poly-L-lactic acid (PLLA), are designed to naturally degrade within the body over time, eliminating the need for secondary interventions. Clinical trials indicate remarkable success, with patient-specific 3D-printed stents delivering improved airway stability and substantially reducing complication rates.

The pediatric airway device market remains largely underserved, presenting an attractive niche for manufacturers. Regulatory incentives, including provisions under the Orphan Drug Act, are further accelerating innovation by providing financial support and tax credits for products addressing rare conditions. These supportive frameworks, combined with the critical unmet need for safer and more effective pediatric airway solutions, create a strong business case for investment in this space. As 3D printing technologies advance and material science innovations continue, bioresorbable airway stents are set to revolutionize pediatric airway management and unlock significant growth in the global medical devices market.

Competitive Landscape: Medical Devices Market

Medtronic: Engineering the Extraordinary in Medical Technology

Medtronic stands at the forefront of the global medical devices market, offering an extensive portfolio that spans cardiovascular, diabetes, neuroscience, surgical, and renal therapies. As a market leader, Medtronic continues to drive transformation with groundbreaking innovations such as the MiniMed™ 780G system which recently expanded its CE Mark indications in Europe for broader diabetes care and the Hugo™ robotic-assisted surgery system, which is reshaping minimally invasive procedures through enhanced precision and real-world trial success. The company’s leadership in advanced therapies is reinforced by its recent FDA approval for Adaptive Deep Brain Stimulation for Parkinson’s, bringing closed-loop, real-time therapy adjustments to neurological care. Medtronic is also investing heavily in R&D and global expansion, notably growing its innovation center in India. The company’s continuous progress in digitalization, value-based healthcare, and sustainability, alongside moves like the intended spin-off of its diabetes division into a standalone company, ensure that Medtronic remains synonymous with next-generation, connected, and patient-centric medical devices worldwide.

Johnson & Johnson MedTech: Expanding the Horizons of Surgical and Interventional Devices

Johnson & Johnson’s MedTech division is a powerhouse in surgical, orthopaedic, and interventional medical devices, consistently setting new standards in precision, efficiency, and clinical outcomes. J&J’s Ethicon brand leads in surgical energy systems with the recent launch of the DUALTO™ Energy System and continues to advance minimally invasive and robotic-assisted procedures, highlighted by the debut of the OTTAVA™ Robotic Surgical System and AI-powered MONARCH™ QUEST for bronchoscopy. In cardiac care, Biosense Webster’s electrophysiology mapping and ablation systems are pushing the frontiers of arrhythmia management, while the newly resumed VARIPULSE™ line reaffirms J&J’s commitment to safety and innovation. Orthopaedics remain a core focus, with digital platforms and data-driven tools empowering personalized joint and spine solutions. Recent acquisitions, such as Shockwave Medical, reinforce J&J’s strategy to address complex clinical needs across cardiovascular, neurovascular, and breast aesthetics. Through a blend of robust product launches and digital transformation, Johnson & Johnson MedTech is elevating its global presence in the evolving medical devices sector.

Abbott Laboratories: Advancing Patient Outcomes with Connected and Minimally Invasive Devices

Abbott Laboratories is a diversified leader in the medical devices market, renowned for its innovations across cardiovascular, diabetes, and neuromodulation fields. Abbott’s FreeStyle Libre CGM systems remain the global benchmark for sensor-based glucose monitoring, with new generations like Libre 3 and Stelo bringing greater convenience and connectivity to diabetes care. In cardiovascular medicine, Abbott’s portfolio from XIENCE Sierra™ stents to the minimally invasive MitraClip™ and Volt™ PFA System for cardiac ablation demonstrates commitment to both clinical excellence and patient comfort. The company’s neuromodulation devices are improving lives for those with movement disorders and chronic pain, while its diagnostic division has made a significant leap with the launch of a laboratory-based blood test for concussion. Abbott’s strong focus on lab automation, digital health integration, and expanding access to cutting-edge devices in emerging markets further solidifies its position as a champion of innovation and patient-centered care in the medical device industry.

Siemens Healthineers: Redefining Precision and Digitalization in Medical Devices

Siemens Healthineers continues to shape the future of medical technology with its focus on diagnostic imaging, molecular imaging, advanced therapies, and laboratory diagnostics all underpinned by AI and digital health solutions. Their portfolio features industry-leading systems, such as the virtually helium-free MAGNETOM Flow MRI and the photon-counting NAEOTOM Alpha® CT, both setting new standards for sustainability, image quality, and workflow efficiency. The company’s syngo.via and other healthcare IT platforms empower enterprise-wide data integration and analytics, critical for precision medicine and operational excellence. Siemens’ commitment to local manufacturing, evidenced by new facilities in India, and the creation of an AI Lab for neuroimaging in partnership with IISc, exemplify its global innovation strategy. Advanced therapy systems, like the ARTIS icono for angiography, and robust laboratory diagnostics continue to reinforce Siemens Healthineers as a leading force in digital, value-based, and personalized healthcare solutions worldwide.

Intuitive Surgical: Leading the Robotic Surgery Revolution in the Medical Devices Market

Intuitive Surgical has cemented its role as the global leader in robotic-assisted surgery, transforming operating rooms with the iconic da Vinci surgical systems. The newly launched da Vinci 5 sets the bar higher with next-gen computing, force feedback, and enhanced machine vision, expanding possibilities for minimally invasive procedures. Intuitive’s focus on telesurgery, demonstrated by the first remote dual-console procedures spanning 4,000 miles, signals a new era of global surgical collaboration and patient access. FDA-cleared advanced energy instrumentation and new indications for the da Vinci SP system further expand the clinical utility of Intuitive’s platform. The Ion™ Endoluminal System advances early lung cancer diagnosis with minimally invasive biopsy capabilities. Intuitive’s digital solutions, telepresence training, and investment arm (Intuitive Ventures) ensure the company’s innovation pipeline remains robust, further embedding robotic and AI-driven technologies at the heart of the modern medical devices landscape.

Market Share and Segmentation Insights: Medical Devices Market

By Product Type: Diagnostic Devices Lead, Monitoring Devices Expand Fastest

Within the medical devices market, Diagnostic Devices command the largest market share at 29.4% in 2025, supported by the increasing prevalence of chronic diseases and the critical role of advanced diagnostics such as MRI and CT scanners in early detection and patient management. This segment remains the backbone of hospital and laboratory workflows, catering to an aging global population and higher diagnostic awareness.

Monitoring Devices represent the fastest-growing segment, with a CAGR of 7.8% through 2034. The surge in remote patient monitoring (RPM), telehealth integration, and continuous health tracking (e.g., wearable ECG, blood glucose, and oxygen monitors) is transforming chronic disease management and post-acute care. Implants also show robust growth, as innovations in orthopedic, cardiovascular, and neurostimulator devices address the needs of a rising elderly population and demand for enhanced patient outcomes. Meanwhile, Therapeutic Devices, Surgical Devices, and Other Medical Devices (e.g., infusion pumps, mobility aids) remain integral to the expanding continuum of care, each contributing to a diverse product landscape.

.png)

By End User: Hospitals & Clinics Dominate, Home Healthcare Surges

On the end-user front, Hospitals & Clinics account for the largest share at 50.8% in 2025, underscoring their pivotal role in handling high patient volumes, complex procedures, and acute care interventions. These facilities drive demand for comprehensive medical device portfolios, from imaging systems to advanced surgical tools, to support a wide range of clinical services.

Home Healthcare Settings are the fastest-growing segment, advancing at a CAGR of 8.7%. This acceleration is fueled by the global shift toward cost-effective, patient-centric models, an aging demographic, and technological advancements that make complex care feasible at home (e.g., home dialysis, portable ventilators, wearable monitors). Ambulatory Surgical Centers (ASCs) are also expanding rapidly, thanks to minimally invasive surgery trends and reimbursement incentives. Diagnostic Laboratories and Research & Academic Institutes, while smaller in share, continue to play critical roles in disease detection, medical innovation, and device development.

United States: Regulatory Advancements Fuel Medical Device Innovation

The United States medical devices market continues to be the global leader in innovation and adoption, underpinned by a robust regulatory framework that supports rapid product introductions and patient-centric care. Recent FDA approvals underscore the pace of innovation such as Boston Scientific’s FARAPULSE Pulsed Field Ablation (PFA) System for atrial fibrillation, Abbott’s Spinal Cord Stimulation (SCS) Systems for chronic pain, and Edwards Lifesciences’ Evoque Tricuspid Valve Replacement System for severe valve leakage all in 2024. The FDA’s dynamic regulatory landscape is not only encouraging the launch of next-generation therapeutic devices but also shaping new safety and cybersecurity norms. With the June 2025 update to its cybersecurity guidance, the FDA now requires more rigorous premarket and post-market protocols for devices with software components, including mandatory Software Bill of Materials (SBOMs) and penetration test reports. This proactive approach is crucial, given that a 2025 study revealed 65% of medical devices failed initial penetration tests due to unaddressed vulnerabilities. Manufacturers must now ensure continuous risk monitoring, rapid response to post-market vulnerabilities, and direct communication with customers measures that enhance trust and raise the bar for digital health security.

Growth in AI-enabled medical devices is another hallmark of the U.S. market. By March 2025, over 950 AI-enabled devices had gained FDA approval, with 107 approvals occurring just in 2024. This ongoing regulatory attention to AI is pushing companies to invest in risk-based design, ongoing model validation, and robust cybersecurity. Meanwhile, 3D printing is expanding at the point of care, especially in specialties such as congenital heart disease and oncology. U.S. hospitals are leveraging patient-specific 3D models for improved surgical planning, operational efficiency, and patient education, with reimbursement frameworks for 3D medical models gaining traction in 2025. This innovation wave is supported by evolving reimbursement policies, allowing healthcare systems to bring 3D printing production in-house to cut costs and improve turnaround. Together, these factors cement the United States’ role as the premier environment for medical device innovation, rapid commercialization, and digital transformation.

Germany: Digitalization, Regulation, and AI Drive Medical Device Market Growth

Germany’s medical devices market is undergoing rapid digital transformation, driven by nationwide policy initiatives and evolving European regulations. The April 2025 nationwide rollout of the Electronic Patient Record (ePA) system marks a pivotal shift in the country’s healthcare infrastructure. By enabling secure, interoperable exchange of diagnoses, treatments, and medication records, the ePA is establishing a robust foundation for integrating data from medical devices, wearables, and remote monitoring solutions. This digital backbone is essential for real-time patient care, data-driven diagnostics, and personalized health management. Additionally, Germany’s focus on digital health aligns with EU objectives to create a pan-European, data-driven healthcare ecosystem, ensuring German providers remain at the cutting edge of medical technology and health informatics.

Stricter EU Medical Device Regulation (MDR) and In Vitro Diagnostic Regulation (IVDR), effective January 2025, are further raising the bar for manufacturers. New mandates include prompt reporting of device supply interruptions, expanded requirements for quality management and documentation, and staged rollouts of the EUDAMED database for market surveillance. For in-house device manufacturing, clinics must now demonstrate the absence of equivalent CE-certified products and comply with strict quality assurance. These regulatory shifts are steering the German market toward higher standards of safety, traceability, and transparency. Alongside this, Germany is accelerating investments in AI-driven diagnostics and remote monitoring areas vital for managing an aging population and the rising prevalence of chronic disease. Companies like CardioSecur exemplify this trend, offering smartphone-based smart ECG solutions for proactive heart health monitoring. Collectively, Germany’s focus on digitalization, advanced regulation, and AI integration is positioning the country as a leader in Europe’s future-ready medical devices sector.

India: Policy Push and Digital Infrastructure Transform the Medical Devices Landscape

India’s medical devices market is poised for exponential growth, propelled by strategic policy measures and an expanding digital health infrastructure. The National Medical Devices Policy 2023 has set the sector on an ambitious path to grow from USD 11 billion in 2022 to USD 50 billion by 2030 and raise India’s global market share from 1.5% to as much as 12%. The policy’s multifaceted approach supports domestic manufacturing, incentivizes R&D, and reduces import dependence through robust Production Linked Incentive (PLI) schemes. As of March 2025, the PLI scheme has enabled the manufacturing of 54 unique medical devices across 21 projects, spanning high-tech modalities such as Linear Accelerators, MRI, CT Scanners, heart valves, and stents. These advances not only boost self-reliance in advanced medical equipment but also open avenues for affordable healthcare innovations that can serve both domestic and global markets.

India’s drive for digital health integration is equally transformative. With over 73.9 crore (739 million) Ayushman Bharat Health Accounts (ABHA) IDs created by early 2025, India is rapidly building a digital ecosystem that facilitates data exchange from connected medical devices, enhances care coordination, and supports national health initiatives. The Council of Scientific and Industrial Research (CSIR) is advancing sustainable medical technologies, exemplified by the February 2025 launch of India’s first indigenous automated biomedical waste treatment plant at AIIMS New Delhi. Such innovations are aligned with “Make in India” and sustainability missions, driving the development of cost-effective, eco-friendly solutions for the country’s unique healthcare challenges. Together, progressive policy, indigenous manufacturing, and digital health enablement are setting the stage for India to emerge as a global force in the medical devices industry.

Japan: Regulatory Modernization and Advanced Wearables Boost Market Innovation

Japan’s medical devices market is undergoing major regulatory modernization, supporting innovation and expedited commercialization. The 2025 amendment to the Pharmaceuticals and Medical Devices (PMD) Act has introduced faster, more flexible processes for bringing advanced devices to market. Notably, conditional approval is now permitted for devices addressing serious diseases with unmet clinical needs, allowing earlier entry if efficacy is reasonably predicted. This framework incentivizes R&D, enabling Japanese companies to accelerate the development of novel therapies, wearables, and diagnostic platforms. The new rules also mandate robust adverse event information collection and streamlined reporting for minor manufacturing changes, reducing the time to market for iterative improvements. Such regulatory reforms are instrumental in ensuring that Japan remains competitive and responsive to the fast-evolving landscape of medical technologies.

Japan is also a global leader in biosensor innovation and wearable health technologies. Researchers are pioneering the use of advanced materials particularly graphene to develop next-generation, ultra-sensitive wearable biosensors for continuous health monitoring. These devices provide real-time insights into stress and mental health biomarkers, leveraging graphene’s exceptional conductivity and flexibility. Japan’s strategic emphasis on R&D is fostering a pipeline of lightweight, biocompatible wearables designed for early diagnosis, preventive healthcare, and the management of chronic conditions. This dual focus on regulatory agility and cutting-edge R&D ensures Japan’s medical devices sector remains at the forefront of both domestic and international market opportunities.

Canada: Digital Health Strategy and Telehealth Integration Fuel Market Growth

Canada’s medical devices market is rapidly modernizing through digital transformation, as evidenced by the British Columbia Digital Health Strategy updated in April 2025. The nationwide focus is on creating a connected, patient-centered healthcare system where digital tools empower patients to access health information and manage their care more efficiently. Providers are gaining streamlined access to comprehensive patient histories, facilitating seamless communication and reducing administrative burden. These reforms are establishing a secure, interoperable framework for the integration of connected medical devices, supporting improved diagnosis, remote monitoring, and coordinated care. As provinces invest in long-term digital health infrastructure, the Canadian market is primed for sustained growth in advanced diagnostics, imaging, and IoMT (Internet of Medical Things) solutions.

The surge in telehealth and remote monitoring services is another major growth driver. Canada’s robust digital health infrastructure enables the widespread deployment of connected medical devices, allowing clinicians to deliver high-quality care across vast and often remote geographies. Ongoing integration of new digital tools is improving workflow efficiency and care delivery, while also fostering a supportive environment for medical device innovation. As a result, demand is increasing for secure, interoperable devices capable of seamless data exchange and remote diagnostics attributes that are vital in both public health networks and private care settings. This focus on connectivity, patient empowerment, and digital transformation is positioning Canada’s medical devices market as a leader in North American healthcare modernization.

Brazil: Regulatory Evolution and Public Health Investment Accelerate Market Momentum

Brazil’s medical devices market is advancing rapidly due to regulatory enhancements and rising public health investment. In July 2025, Brazil’s National Health Surveillance Agency (ANVISA) will enforce Unique Device Identification (UDI) requirements, compelling companies to mark devices and submit traceability data for improved post-market surveillance. This aligns Brazil with global best practices and ensures greater safety and transparency for both providers and patients. Meanwhile, the Unified Health System (SUS) is set for a 6.2% budget increase in 2025, a move that will bolster both primary and specialized care services. This budgetary expansion is expected to drive new procurement and broader adoption of medical devices within public hospitals and clinics nationwide.

A major focus area in Brazil’s device market is diagnostics and the shift toward homecare solutions. The growing demand for user-friendly, portable medical devices supports the management of chronic diseases and enables remote monitoring, which is increasingly critical in a geographically vast nation. With regulatory frameworks evolving and public investment on the rise, Brazil’s medical devices sector is well-positioned for long-term growth, innovation, and improved health outcomes particularly in diagnostics, homecare, and portable device segments. Companies that align with new compliance mandates and address homecare trends are likely to find significant opportunities in this dynamic Latin American market.

France: Health Innovation and Aging Demographics Reshape Device Demand

France’s medical devices market is on an upward trajectory, propelled by the “France Health Innovation 2030” strategy, which prioritizes investment in AI, digital technologies, and the development of innovative health solutions. Business France’s global promotion of French medical device innovation, including the launch of a “Medical Devices” marketplace at Arab Health 2025, highlights the country’s ambitions to become a global leader in medical technology exports. The national strategy accelerates R&D in advanced diagnostics, connected health devices, and personalized medicine enabling French firms to compete globally in high-growth segments. Digital transformation is also central, with substantial infrastructure and incentive programs supporting telemedicine, e-health integration, and the digitization of patient pathways.

France’s aging population and high prevalence of chronic diseases are key demand drivers for advanced medical devices. Chronic illnesses account for nearly 80% of national health expenditure, creating a sustained need for devices that enable early diagnosis, effective monitoring, and home-based care. The share of French residents aged 65+ is projected to climb from 20% in 2020 to nearly 30% by 2040, intensifying demand for healthcare technologies that support aging in place. In response, both startups and established firms are expanding portfolios in diabetes management, cardiovascular monitoring, and telehealth solutions. Regulatory support and a strong push for digitalization are further catalyzing growth, ensuring France remains a pivotal player in the global medical devices market.

Medical Devices Market Report Scope

Medical Devices Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$596.9 Billion

|

|

Market Size (2034)

|

$1052.1 Billion

|

|

Market Growth Rate

|

6.5%

|

|

Segments

|

By Product Type (Diagnostic Devices, Therapeutic Devices, Monitoring Devices, Surgical Devices, Implants, Other Medical Devices.), By Technology (Conventional Electro-Mechanical & Disposable Devices, Wearable & Remote Monitoring Devices, Telehealth & mHealth Devices, Robotic Surgery Systems, 3D Printing for Medical Devices, Augmented/Virtual Reality (AR/VR) in Medical Devices, Nanotechnology in Medical Devices, AI & Machine Learning Integrated Devices), By End User (Hospitals & Clinics, Ambulatory Surgical Centers (ASCs), Diagnostic Laboratories, Home Healthcare Settings, Research & Academic Institutes)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Medtronic plc., Johnson & Johnson (J&J MedTech), Abbott Laboratories, Siemens Healthineers AG, GE HealthCare Technologies Inc., Koninklijke Philips N.V., Stryker Corporation, Boston Scientific Corporation, Danaher Corporation, Baxter International Inc., Becton, Dickinson and Company (BD), Intuitive Surgical, Inc., Zimmer Biomet Holdings, Inc., Teleflex Incorporated, Terumo Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Medical Devices Market Segmentation

By Product Type

- Diagnostic Devices

- Therapeutic Devices

- Monitoring Devices

- Surgical Devices

- Implants

- Other Medical Devices.

By Technology

- Conventional Electro-Mechanical & Disposable Devices

- Wearable & Remote Monitoring Devices

- Telehealth & mHealth Devices

- Robotic Surgery Systems

- 3D Printing for Medical Devices

- Augmented/Virtual Reality (AR/VR) in Medical Devices

- Nanotechnology in Medical Devices

- AI & Machine Learning Integrated Devices

By End User

- Hospitals & Clinics

- Ambulatory Surgical Centers (ASCs)

- Diagnostic Laboratories

- Home Healthcare Settings

- Research & Academic Institutes

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Medical Devices Market

- Medtronic plc.

- Johnson & Johnson (J&J MedTech)

- Abbott Laboratories

- Siemens Healthineers AG

- GE HealthCare Technologies Inc.

- Koninklijke Philips N.V.

- Stryker Corporation

- Boston Scientific Corporation

- Danaher Corporation

- Baxter International Inc.

- Becton, Dickinson and Company (BD)

- Intuitive Surgical, Inc.

- Zimmer Biomet Holdings, Inc.

- Teleflex Incorporated

- Terumo Corporation

* List Not Exhaustive

Research Coverage

This USDAnalytics report delivers in-depth market sizing, CAGR, and value projections for the global medical devices market, placing recent developments such as AI-enabled predictive recalls, robotic surgery, remote monitoring, and digital transformation at the core of its industry review. The study covers comprehensive segmentation by product type (diagnostic, therapeutic, monitoring, surgical devices, implants, others), by technology (conventional, wearable, telehealth, robotic, 3D printing, AR/VR, nanotechnology, AI-integrated), and by end user (hospitals, ASCs, diagnostic labs, home healthcare, research institutes).

Profiles of leading companies Medtronic, J&J MedTech, Abbott, Siemens Healthineers, GE HealthCare, Philips, Stryker, Boston Scientific, Danaher, Baxter, BD, Intuitive Surgical, Zimmer Biomet, Teleflex, Terumo are included, with their recent strategies and innovation focus. Geographic analysis spans North America, Europe, Asia Pacific, South America, and Middle East & Africa. The report includes historic data (2021–2024) and forecast data (2025–2034), providing insights into market dynamics, regulatory trends, R&D pipelines, and technological advancements. The scope is structured for industry professionals seeking actionable intelligence on market evolution, leading innovations, and global opportunities.

Deliverables:

- Full Market Research Report (PDF, Excel): Complete data tables, market charts, and visual insights.

- Country-Level Forecasts & Analysis.

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis.

- Recent Developments & News Tracker

- Executive Summary & Analyst Insights.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.