Market Overview: Rising Biocompatibility Standards and High-Purity Silicone Advancements Accelerate Medical Grade Silicone Rubber Market Growth

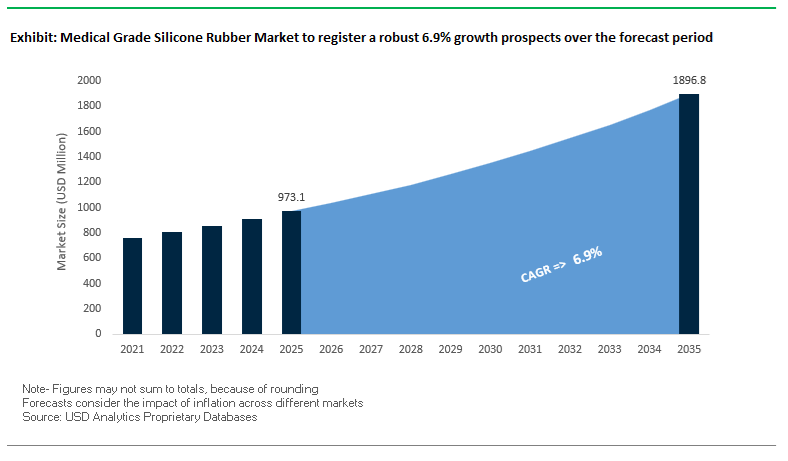

The Medical Grade Silicone Rubber Market is projected to expand from USD 973.1 million in 2025 to USD 1,896.4 million by 2035, reflecting a strong CAGR of 6.9%. The industry is being reshaped by stringent biocompatibility standards, advanced sterilization requirements, and increasing adoption of Liquid Silicone Rubber (LSR) in next-generation medical devices, wearables, and implantable components. Manufacturers are under pressure to meet ISO 10993, USP Class VI, and cGMP compliance, making purity control, extractables management, and long-term material stability critical competitive differentiators.

Rising demand for drug delivery systems, bioprocessing tubing, prosthetic components, wound care products, soft tissue implants, and wearable biosensors is accelerating advanced silicone rubber usage. Vendors are designing specialized LSR grades with ultra-low VOCs, high tear strength, optical clarity, and enhanced sterilization endurance, ensuring performance stability after >50 autoclave cycles at 121°C. The ability to offer materials across a broad 40A–80A Shore hardness range enables deeper penetration into surgical, implantable, and diagnostic applications.

Key Insights for Device OEMs, Bioprocessing Firms & Healthcare Material Engineers

- ISO 10993 + USP Class VI certification remains mandatory for long-term and implantable silicone applications.

- Advanced LSR formulations withstand >50 high-temperature autoclave cycles, ensuring longevity in reusable medical equipment.

- Extractables control below 200 ppm is critical for drug delivery systems and bioprocessing tubing to maintain purity and prevent contamination.

- Shore hardness flexibility (40A–80A) supports application versatility—catheters, gaskets, seals, implantables, and wearables.

Market Analysis: Product Innovation, Sustainability Breakthroughs & Regulatory Tightening Shape the Global Medical Grade Silicone Rubber Landscape

The global medical-grade silicone segment is undergoing accelerated transformation driven by material innovation, sustainability mandates, and stricter regulatory oversight. In October 2025, Elkem strengthened its leadership in smart medical materials by launching a new biocompatible electro-conductive SILBIONE™ LSR, designed specifically for wearable healthcare devices and biosensor platforms requiring both elasticity and electrical signal transmission. This aligns with the sector’s shift toward next-generation diagnostic patches, remote patient monitoring systems, and flexible electronics, where traditional silicones lack the electrical responsiveness needed for bio-signal integration.

Sustainability has become a defining priority, with September 2025 marking a significant milestone as Elkem announced a mechanical recycling pathway for silicone rubber, addressing one of the industry's longstanding environmental challenges. This breakthrough supports the broader push toward a Circular Economy for medical elastomers, appealing to OEMs facing rising ESG compliance requirements. Parallel to this, in April 2025, Elkem’s BLUESIL™ LSR 3935 earned the Ringier Technology Innovation Award, showcasing continued progress in formulating high-performance LSRs for demanding, repetitive-use medical applications.

Regulatory pressure also continues to intensify. In March 2025, global reports noted a surge in FDA and EMA cGMP inspections targeting silicone raw material suppliers—particularly those supporting implantable and long-term contact devices. This shift underscores the necessity for manufacturers to maintain robust documentation, traceability, and extremely low extractables and leachables profiles. Meanwhile, Momentive’s contract extension in October 2024 for high-volume LSR supply to a major Continuous Glucose Monitoring (CGM) manufacturer signals sustained market confidence in premium silicone elastomers that guarantee adhesion, durability, and skin compatibility for extended wear.

The innovation cycle continued into December 2025, when Wacker Chemie AG introduced new ELASTOSIL® addition-curing LSR grades with enhanced self-bonding capability, enabling multi-component molding without primers. This directly responds to OEM demand for integrated manufacturing processes that streamline assembly, reduce cycle time, and support complex device geometries. Advances like these, combined with Elkem’s Q3 2025 announcement of strong operational performance, indicate resilient demand for specialty medical silicones despite global economic fluctuations.

Breakthrough Material Science Trends and Commercial Opportunities Shaping Long-Term Implants, Bioelectronic Interfaces, Smart Adhesives, and Sterilization-Resilient Silicone Systems

Market Trend 1: Ultra-High Purity, Low-Extractable Silicone Qualification for Long-Term Implantable Drug-Delivery Systems

A defining materials trend in the medical grade silicone rubber market is the rigorous push toward ultra-high purity, low-extractable silicone elastomers engineered for long-term implantable drug delivery devices, where chemical stability, biocompatibility, and extractables control directly influence regulatory qualification. Under emerging standards such as YY/T 0884-2021, implantable silicones must maintain Residual Volatile Substances below 0.5% by weight, specifically limiting low-molecular-weight siloxanes such as D4, D5, and D6, which are known to migrate and compromise drug-release predictability.

Biocompatibility expectations continue to rise. Materials must fully comply with ISO 10993-5, ensuring that extracts do not induce cytotoxicity—defined as no observable cell death or morphological damage in more than 50% of cultured cells. Additionally, manufacturers must demonstrate full USP Class VI compliance, which requires implants to produce minimal tissue irritation and zero acute systemic toxicity in vivo.

Drug-delivery silicones increasingly require ultra-low leachable concentrations, with advanced formulations achieving release levels below the pathogen MIC threshold of 10 μg/mL, ensuring no interference with antimicrobial kinetics or drug stability. These performance metrics collectively frame a trend toward regulator-driven purity specifications, pushing suppliers to engineer implantable silicones with unprecedented chemical cleanliness, biological neutrality, and controlled extractables.

Market Trend 2: Rapid Adoption of Conductive and Dielectric Silicone Elastomers for Next-Generation Wearable and Implantable Bioelectronics

The second major trend reshaping the market is the integration of conductive, dielectric, and hybrid silicone elastomers optimized for neural interfaces, wearable sensors, implantable stimulators, and soft bioelectronic systems. Standard silicone encapsulants used in neurostimulators and implantable pulse generators exhibit a dielectric constant (εr) of 2.75–5 at 1 kHz, enabling ultra-low parasitic capacitance and minimizing high-frequency signal distortion.

Equally critical is dielectric durability: medical silicone insulators designed for high-voltage neurostimulator circuits deliver breakdown strengths between 370–385 V/mil, ensuring robust protection for microelectronics in physiological environments. The inherent Si–O backbone gives silicone a high Dry Arc Resistance of 120–145 seconds, outperforming most medical polymers and ensuring safety in densely packed bioelectronic assemblies.

For strain sensors, electrodes, and soft robotics, conductive silicone formulations incorporate CNTs or silver particulates to achieve controlled sheet resistance levels from 10¹ to 10⁴ Ω/sq, enabling tunable conductivity for biomechanical monitoring, electrophysiological mapping, and stretchable circuitry. This trend marks the evolution of silicone from a passive biocompatible matrix into an active electronic material platform, enabling high-precision diagnostics and long-term implantable devices.

Market Opportunity 1: Smart, On-Demand Debonding Silicone Adhesives Enabling Painless Removal in Wound Care and Wearables

A high-value commercial opportunity lies in the development of smart silicone pressure-sensitive adhesives (PSAs) that deliver secure attachment during use yet detach painlessly on demand. Advanced MR-fluid-based or stimulus-responsive adhesives achieve detachment switching speeds of 100–500 milliseconds, ensuring nearly instantaneous removal for elderly patients, sensitive skin applications, and neonatal care.

Next-generation smart adhesives are engineered with a dual-performance mechanical profile—initial pull-off strengths reaching up to 5.6 MPa for secure fixation during daily movement, followed by a >90% reduction in adhesion force once activated by a mild stimulus such as heat or UV exposure. Conventional silicone PSAs remain <1 N/cm peel strength, but smart variants enable new categories of reusable sensors, long-wear wound dressings, and detachable medical monitoring patches.

This opportunity is expanding rapidly as healthcare shifts toward remote monitoring and continuous physiological tracking, requiring adhesives that are atraumatic, biocompatible, customizable, and compatible with long-duration wear—all areas where silicone chemistry offers a unique advantage.

Market Opportunity 2: Engineering Silicone Rubbers Resilient to High-Level Disinfection (HLD) and Novel Sterilization Cycles

Another major opportunity is emerging around silicones engineered to withstand repeated high-level disinfection (HLD) and modern sterilization processes, particularly Vaporized Hydrogen Peroxide (VHP) which is increasingly replacing steam autoclaving for sensitive devices. Growth in reusable surgical instruments and robotic systems has generated demand for elastomers capable of surviving up to 1,000 sterilization cycles without failure.

Mechanical integrity remains a key challenge. Studies show traditional materials experience ≤2% hardness loss after 100 VHP cycles, but long-term exposure may cause six-fold increases in crack length after 200 cycles due to oxidative degradation. New silicone formulations aim to restrict crack propagation, increase tear resistance, and maintain elasticity across repeated VHP cycles.

An important advantage is that VHP sterilization operates at only 35°C–60°C, compared to 121°C–135°C for steam autoclaves, eliminating thermally induced elasticity loss—one of the leading failure modes of legacy silicone systems. This creates a strong market opportunity for VHP-resilient silicone rubbers designed for surgical tools, reprocessable tubing, diagnostic devices, and multi-use implant delivery systems.

Medical Grade Silicone Rubber Market Share Analysis

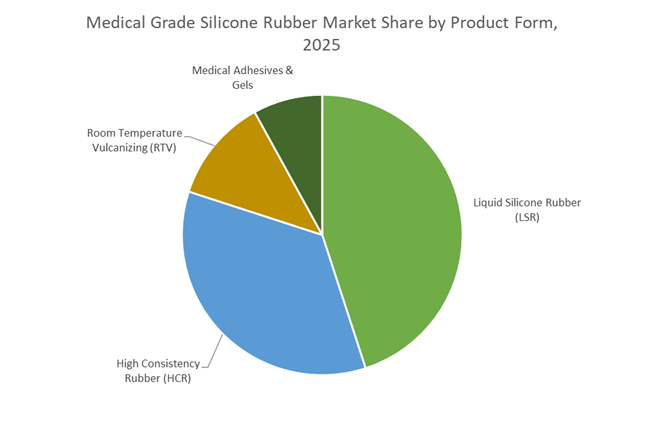

Market Share by Product Form: Liquid Silicone Rubber (LSR) Leads Due to Precision Moldability and High-Volume Medical Manufacturing Efficiency

Liquid Silicone Rubber (LSR) holds the leading share of the global medical grade silicone rubber market—approximately 45%—because it is uniquely optimized for the stringent, high-volume, and precision-driven requirements of modern medical manufacturing. Its low-viscosity, two-part platinum-cure chemistry enables Liquid Injection Molding (LIM), a highly automated, closed-loop process that delivers exceptional speed, accuracy, and reproducibility—capabilities that are essential for medical OEMs scaling production of components like syringe seals, pump diaphragms, valves, baby-care products, and micro-molded wearable device components. LSR’s ability to fill ultra-thin, micro-engineered geometries with uniformity makes it indispensable for next-generation diagnostic devices and compact drug delivery platforms, where tolerance deviation is unacceptable. Furthermore, the inherently high purity and low extractables of platinum-cured LSR—combined with compliance to USP Class VI and ISO 10993 biocompatibility standards—make it the material of choice for patient-contact and implant-adjacent applications without requiring extensive post-curing. Its stability over a wide temperature range, resistance to sterilization (autoclave, EtO, gamma), and low compression set ensure consistent long-term performance. These properties, combined with reduced waste and higher throughput relative to HCR or RTV silicones, explain why LSR continues to dominate the market and attract investment from medical device manufacturers seeking efficiency, safety, and superior engineering performance.

Market Share by Application: Medical Devices Dominate Owing to Biocompatibility, Precision Requirements, and Expansion of Minimally Invasive Care

The Medical Devices segment is the largest application area for medical grade silicone rubber—capturing roughly 40% of global demand—because silicone is indispensable for the performance, safety, and regulatory compliance of diagnostic, surgical, and therapeutic devices. Medical grade silicone rubber’s unmatched biocompatibility, chemical inertness, thermal stability, and sterilization resilience make it a critical material across a wide spectrum of components, from seals and gaskets in infusion pumps and ventilators to precision-molded membranes, respiratory masks, and peristaltic pump tubing. The combination of elasticity, softness, and durability allows silicone to maintain functional integrity under cyclic loading, making it ideal for reusable surgical devices as well as high-volume disposables. The surge in minimally invasive surgery, home healthcare devices, and the proliferation of connected, wearable medical technologies further amplify silicone demand, as these devices require hypoallergenic, skin-contact-safe materials that remain comfortable over extended wear. Moreover, the rise in chronic diseases—diabetes, cardiovascular disorders, respiratory conditions—directly expands the consumption of silicone-based components in drug delivery systems, diagnostic cartridges, and therapeutic equipment. With global healthcare systems moving toward advanced automation, portable medical technologies, and higher sterilization standards, the medical devices segment maintains its dominant share as the primary driver of high-performance silicone rubber consumption.

Country Analysis: Strategic National Drivers Shaping the Global Medical Grade Silicone Rubber Market

United States: Leadership in Implant-Grade Silicone and Wearable Medical Device Integration

The United States remains at the forefront of global Medical Grade Silicone Rubber (MGSR) innovation, driven by its sophisticated medical device ecosystem, rapid adoption of long-term implantable technologies, and strong FDA-led regulatory pathways. The launch of DOW SILASTIC MG-740 in March 2024, a next-generation implantable-grade silicone engineered for enhanced long-term biocompatibility, underscores the country’s leadership in high-purity elastomer development. This product category is essential for Class III implantables such as neurostimulators, cardiovascular implants, and orthopedic systems that require exceptional stability, minimal extractables, and superior sterilization compatibility. The U.S. also dominates wearable medical technology, as seen with Solventum’s Hi-Tack Silicone Tape introduced in October 2024, a skin-friendly and extended-wear silicone adhesive designed for up to seven days of continuous monitoring—an important milestone as remote healthcare expands into mainstream clinical practice.

Stringent FDA regulatory requirements, including USP Class VI and ISO 10993 compliance, continue to accelerate the U.S. transition toward highly purified Liquid Silicone Rubber (LSR) formulations capable of long-term implantation and high-frequency sterilization cycles. Moreover, over $500 million in polymer R&D investment across 2024–2025 reflects a national priority to expand domestic capacity for advanced elastomers supporting vascular catheters, respiratory devices, diagnostic instruments, and soft robotics. With the U.S. intensifying support for material science innovation, its role in defining next-generation MGSR solutions remains unmatched.

Germany & the European Union: MDR-Driven Material Innovation and Sustainable Silicone Advancements

The European MGSR market is heavily shaped by strict regulatory oversight under the evolving EU Medical Devices Regulation (MDR), which mandates extensive biocompatibility, traceability, and validation of all silicone materials used in medical implants and wearables. This regulatory pressure directly elevates demand for high-consistency silicone rubber (HCR) and medical-grade LSR formulations that meet long-term implantation requirements. European manufacturers like WACKER have responded aggressively: in January 2024, the company announced a major specialty silicone production expansion in Karlovy Vary, Czech Republic, boosting regional access to medical elastomers and improving supply chain resilience for European OEMs.

Sustainability has become a central competitive differentiator in Europe, with WACKER showcasing SILPURAN® eco 2114, its first biomethanol-based silicone gel, at COMPAMED 2025. This sustainable material supports growing demand for eco-designed medical adhesives used in wound care patches, glucose monitors, and transdermal drug delivery systems. Additionally, EU research bodies continue accelerating innovation in controlled-release silicone gels engineered to deliver active pharmaceutical ingredients (APIs) through advanced transdermal systems, expanding silicone’s role from a passive carrier to an active therapeutic enabler. These regulatory and environmental forces position Europe as a high-value hub for premium, compliant, and sustainable medical silicone rubber technologies.

China: Scaling High-Volume LSR Capacity and Becoming a Global Manufacturing Center for Medical Devices

China is rapidly becoming the world’s largest producer of medical-grade Liquid Silicone Rubber (LSR), supported by extensive industrial policies and massive domestic demand for tubing, catheters, ventilator components, and IV systems. A landmark example is Elkem Silicones’ $50 million expansion in Zhangjiagang in July 2024, which significantly increases China’s ability to serve both local and global medical OEMs requiring high-purity elastomers for regulated healthcare applications. This aligns with China’s broader strategy to internalize production of silicone precursors such as polysiloxanes, reducing dependency on foreign suppliers while ensuring stable availability for high-growth medical sectors.

Chinese manufacturers like Shenzhen Tenchy Silicone have also accelerated localized production of critical medical components through new product launches such as medical-grade silicone tubing in October 2024. Combined with national policy mandates supporting chemical precursor self-sufficiency and end-to-end device manufacturing, China continues reinforcing its position as the global high-volume production hub for medical-grade silicone components. This expansion is especially impactful for ventilator lines, dialysis systems, infusion sets, and other high-throughput medical device categories essential to global healthcare infrastructure.

Japan: Advancements in Ultra-High Purity Silicone and Surface-Engineered Implantable Materials

Japan retains its position as a global leader in ultra-high purity silicones, benefiting from decades of precision chemical engineering and a strong domestic focus on biocompatible implantables. Companies such as Shin-Etsu Chemical supply some of the world’s purest silicone monomers, allowing Japanese producers to achieve exceptionally low leachable profiles—critical for permanent implants including breast implants, cardiac devices, and neuromodulation systems. This technological edge supports the rising demand for silicone materials engineered for extremely low inflammatory response and long-term physiological stability.

Japanese R&D is also pioneering surface-engineered silicone rubbers, integrating microgroove patterning and carbon-ion implantation technologies. These innovations significantly mitigate issues such as capsule contracture in implants and minimize tissue irritation in long-term medical placements. Moreover, Japan’s emerging work in silicone additive manufacturing supports the customization trend in orthopedics and patient-specific surgical devices, strengthening its leadership in specialty medical-grade silicone solutions.

Norway & the Nordic Region: Pioneering Circular Economy Solutions for Sustainable Silicone Elastomers

Norway and the broader Nordic region are global frontrunners in sustainability-focused MGSR development, particularly through innovations in recycling and circular economy models for thermoset silicones. In September 2025, Elkem announced a breakthrough in mechanical recycling for High Consistency Rubber (HCR), demonstrating that up to 50% HCR waste can be reintegrated into new formulations without compromising material performance. This achievement represents a major step toward overcoming the long-standing recyclability challenges associated with crosslinked silicone elastomers.

Additionally, the Nordic region’s strong biomedical sectors continue promoting advanced Silbione medical- and implant-grade materials that emphasize patient safety, low environmental impact, and long-term performance. Norway's leadership in material sustainability positions the region as an influential contributor to the global shift toward low-carbon, circular medical silicone ecosystems, providing models for scalable, environmentally responsible production.

India: Growing Domestic Medical Device Ecosystem and Localization of Implantable Silicone Technology

India’s Medical Grade Silicone Rubber market is expanding rapidly due to strong government initiatives aimed at bolstering domestic medical device manufacturing capacity. The country’s policy environment—including schemes under the Ministry of Chemicals and Fertilizers and the Ministry of Health—supports the localization of implantable technologies and silicone-based critical components. India’s push for self-reliance, reinforced by quality standardization and local production incentives, is enabling manufacturers to scale output of LSR and HCR for applications such as surgical devices, wound management, respiratory care, and catheter systems.

The country is also witnessing rising investments from both domestic and global medical device companies, seeking to capitalize on India’s expanding healthcare infrastructure and growing patient demand. With a strategic shift toward indigenous production of implantable-grade materials, India is poised to emerge as a major regional producer of medical-grade silicone systems that meet international biocompatibility and performance benchmarks.

Competitive Landscape: Material Purity, Biocompatibility Leadership & Integrated Solutions Define Market Positioning

The competitive environment for medical-grade silicone rubber is shaped by biocompatibility performance, sustainability leadership, sterilization resistance, and ability to support automated medical manufacturing workflows. Companies focusing on high-purity LSR/HCR grades, optical clarity, low extractables, and integrated device assembly solutions are securing stronger relationships with major medical OEMs. The ability to supply silicone grades engineered for implants, diagnostics, bioprocessing, and wearables remains a key differentiator.

Dow Inc. – Dow advances integrated biomedical silicone systems for high-purity medical device manufacturing

Dow leverages its extensive SILASTIC™ Biomedical portfolio—spanning LSR, HCR, adhesives, and high-purity fluids—to act as a complete silicone ecosystem provider for medical device OEMs. Its strength lies in delivering integrated solutions, including primers, coatings, and bonding materials that support seamless device assembly and long-term component performance. With over 89% of its R&D pipeline aligned to sustainability objectives, Dow is investing heavily in circular silicone initiatives and renewable-powered manufacturing. Its biomedical grades maintain stringent compliance with USP Class VI and ISO 10993 standards, making Dow one of the most trusted suppliers for implantables, wound care products, surgical components, and diagnostic systems.

Wacker Chemie AG – Wacker leads in platinum-cured, ultra-pure medical LSR for high-precision molding and implantables

Wacker's ELASTOSIL® and SILPURAN® product lines are renowned for extremely low extractables, premium optical clarity, and compliance with stringent regulatory frameworks. The company emphasizes platinum-cured LSR technologies, ensuring consistent purity and biocompatibility for long-term implants, catheters, prosthetics, and complex molded medical components. Its strong cleanroom manufacturing capabilities and ability to customize rheology, curing profiles, and bonding properties make Wacker a preferred partner for precision medical device molders. The December 2025 launch of self-bonding ELASTOSIL® LSR grades underscores Wacker’s commitment to multi-component molding and manufacturing efficiency.

Shin-Etsu Chemical Co., Ltd. – Shin-Etsu excels in optical-grade, ultra-low-contamination LSR for sensors and implantable applications

Shin-Etsu’s KE Series offers exceptional purity (<200 ppm low-molecular siloxanes), optical clarity, and durability, making it ideal for optical sensors, diagnostic instruments, and implantable components. Its silicone technologies are engineered for superior chemical resistance and thermal stability, supported by a siloxane bond energy of 106 kcal/mol, which ensures long-term structural integrity through sterilization cycles and chemical exposure. Shin-Etsu’s expertise in precision molding grades and advanced formulations positions it strongly in markets demanding contamination-free, high-transparency elastomers for lens components, CGM sensors, and microfluidic devices.

Momentive Performance Materials Inc. – Momentive specializes in drug-delivery and bioprocessing silicones with advanced self-lubricating LSR systems

Momentive focuses heavily on silicone solutions for biopharma processing, drug delivery devices, and medical tubing, offering materials validated to USP Class VI and ISO 10993 standards. Its SILOPREN™ and Addisil® lines include high-consistency elastomers and advanced LSRs engineered for friction reduction, chemical compatibility, and cleanability. The company’s self-lubricating silicone technology (e.g., SILOPREN™ LSR 4635 SL) enables easier insertion of tubing and catheters, while supporting automated extrusion and molding environments. Momentive’s longstanding supply relationship with CGM manufacturers underscores its leadership in skin-contact, long-wear medical silicone applications.

Elkem ASA – Elkem drives sustainable medical silicones with recyclable LSR solutions and electro-active elastomers

Elkem’s SILBIONE™ and BLUESIL™ medical-grade silicones emphasize purity, durability, and sustainability, making the company a key innovator in circular silicone manufacturing. The September 2025 breakthrough in mechanical silicone recycling positions Elkem at the forefront of environmentally responsible elastomer production. Its product portfolio includes high-performance LSR and HCR grades with exceptional biocompatibility, thermal resistance, and mechanical stability. Elkem is also pioneering electro-conductive and electro-active silicone materials for biosensors, wearable health monitors, and soft robotics in medical applications—areas experiencing rapid adoption. Strong financial performance in Q3 2025 further validates the resilience of its specialty silicone division.

Medical Grade Silicone Rubber Market Report Scope

Medical Grade Silicone Rubber Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$973.1 Million

|

|

Market Size (2035)

|

$1896.4 Million

|

|

Market Growth Rate

|

6.9%

|

|

Segments

|

By Product Form (Liquid Silicone Rubber, High Consistency Rubber, Room Temperature Vulcanizing, Medical Adhesives & Gels), By Application (Prosthetics & Implants, Medical Devices, Drug Delivery Systems, Medical Tapes & Wound Care, Wearable Medical Devices), By Curing Mechanism (Addition Cure, Condensation Cure), By End User (Hospitals & Clinics, Ambulatory Surgery Centers, Research Institutes & Labs)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Dow, Wacker Chemie, Shin-Etsu Chemical, Momentive, Elkem Silicones, Trelleborg, 3M, Avantor (NuSil), Rogers Corporation, KCC Silicone, Specialty Silicone Products, Primasil, Applied Silicone, Freudenberg Group, Saint-Gobain

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Medical Grade Silicone Rubber Market Segmentation

By Product Form

- Liquid Silicone Rubber (LSR)

- High Consistency Rubber (HCR)

- Room Temperature Vulcanizing (RTV)

- Medical Adhesives & Gels

By Application

- Prosthetics & Implants

- Medical Devices

- Drug Delivery Systems

- Medical Tapes & Wound Care

- Wearable Medical Devices

By Curing Mechanism

- Addition Cure

- Condensation Cure

By End User

- Hospitals & Clinics

- Ambulatory Surgery Centers

- Research Institutes & Labs

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Medical Grade Silicone Rubber Market

- Dow

- Wacker Chemie

- Shin-Etsu Chemical

- Momentive

- Elkem Silicones

- Trelleborg

- 3M

- Avantor (NuSil)

- Rogers Corporation

- KCC Silicone

- Specialty Silicone Products

- Primasil

- Applied Silicone

- Freudenberg Group

- Saint-Gobain.

*- List not Exhaustive

Research Coverage: Medical Grade Silicone Rubber Market

The latest Medical Grade Silicone Rubber Market study from USDAnalytics delivers an end-to-end strategic view for decision-makers as this report investigates demand evolution across implants, medical devices, drug delivery systems, bioprocessing components, and connected wearables under tightening global biocompatibility and sterilization rules. It tracks material science breakthroughs in high-purity LSR and HCR platforms, self-bonding grades, electro-conductive silicones, smart adhesives, and sterilization-resilient elastomers while mapping their impact on OEM design roadmaps and automated molding workflows. Through quantitative market modelling and rigorous analysis reviews, the study benchmarks vendors on purity control, extractables/leachables profiles, long-term stability, and regulatory readiness, and it highlights how sustainability initiatives such as silicone recycling and circular elastomer programs are reshaping sourcing strategies. Integrating technology roadmaps, segment-wise demand outlooks, pricing dynamics, and risk assessments across global healthcare value chains, this report is an essential resource for medical device OEMs, contract manufacturers, material engineers, and investors seeking to optimize silicone rubber portfolios, de-risk supply chains, and align future product pipelines with evolving clinical, regulatory, and ESG expectations.

Scope Highlights

- Segmentation By Product Form – Liquid Silicone Rubber (LSR), High Consistency Rubber (HCR), Room Temperature Vulcanizing (RTV), Medical Adhesives & Gels

- Segmentation By Application – Prosthetics & Implants, Medical Devices, Drug Delivery Systems, Medical Tapes & Wound Care, Wearable Medical Devices

- Segmentation By Curing Mechanism – Addition Cure, Condensation Cure

- Segmentation By End User – Hospitals & Clinics, Ambulatory Surgery Centers, Research Institutes & Labs

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Time Frame: Historic data from 2021 to 2025 and forecast data from 2026 to 2034.

- Companies Covered: Analysis / profiles of 15+ leading medical grade silicone rubber manufacturers, converters, and solution providers across the global value chain.