Metal Coatings Market Size, Corrosion Protection Demand, and Advanced Surface Technologies Outlook

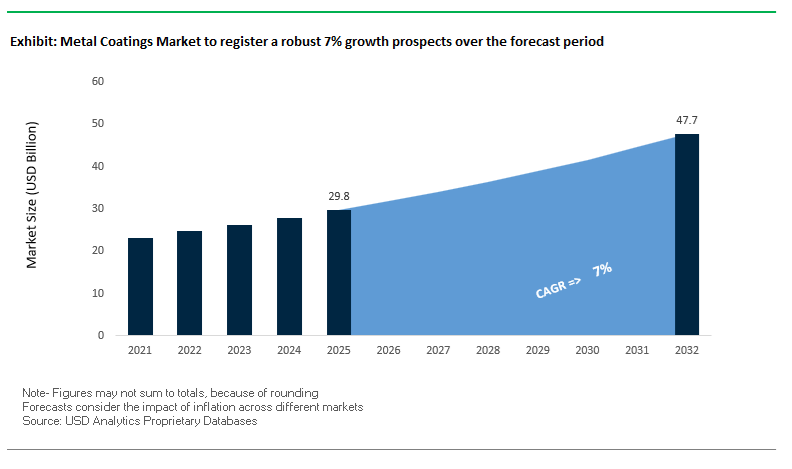

The global metal coatings market was valued at $29.8 billion in 2025 and is projected to reach $47.9 billion by 2032, expanding at a CAGR of 7%. This growth is driven by rising demand for protective metal coatings, anti-corrosion coatings, powder coatings, coil coatings, and functional surface treatments across automotive, construction, energy, packaging, and industrial manufacturing sectors. As industries increasingly prioritize asset durability, lifecycle extension, and environmental compliance, metal coatings have become essential for protecting substrates from corrosion, chemical exposure, UV degradation, and mechanical wear.

A key growth driver is the expanding need for high-performance coatings in harsh environments, particularly in offshore oil & gas, infrastructure, and marine applications, where corrosion-related losses remain substantial. Technologies such as zinc-rich primers, epoxy coatings, polyurethane coatings, and advanced pretreatment systems are being widely adopted to enhance adhesion, durability, and resistance to extreme conditions. Additionally, the shift toward lightweight metals in automotive and construction, including aluminum and advanced alloys, is increasing the demand for specialized coating systems that provide both protection and aesthetic appeal.

Sustainability is a major factor shaping market evolution. The transition toward low-VOC, PFAS-free, and bio-based coatings, along with the adoption of energy-efficient curing technologies, is accelerating due to regulatory pressure and ESG commitments. Innovations in cool roof coatings, functional coatings for food packaging, and advanced surface technologies are expanding application areas. Regionally, Asia-Pacific dominates due to strong industrial growth, while Europe and North America lead in advanced coating technologies and sustainability-driven innovation.

Market Analysis: Sustainable Coating Innovation, and Industrial Expansion Driving Market Evolution

The metal coatings industry is undergoing significant transformation driven by consolidation, strategic repositioning, and advanced material innovation. A major development occurred in February 2026, when AkzoNobel and Axalta initiated a mega-merger, combining AkzoNobel’s leadership in architectural metal coatings (coil and extrusion) with Axalta’s strong position in automotive metal coatings. This consolidation creates a powerful global entity capable of driving innovation and setting new standards in high-performance metal coating technologies.

Strategic expansion and capacity investments are reinforcing supply capabilities. In March 2026, Huntsman Corporation inaugurated an expanded facility in Hungary to produce specialty amines and catalysts used in polyurethane and epoxy metal coatings, strengthening supply for European automotive and industrial sectors. Similarly, Sherwin-Williams’ January 2025 integration of Suvinil in Brazil enhances its ability to deliver metal protective coatings across South America’s construction and oil & gas markets.

Sustainability and energy efficiency are becoming central to product innovation. Axalta’s 2025 R&D 100 Award-winning Fast Cure, Low Energy coating system enables automotive refinishing at lower temperatures and shorter oven cycles, significantly reducing energy consumption. PPG Industries reported that 44% of its 2024 sales came from sustainably advantaged products, driven in part by the adoption of PPG INNOVEL® PRO, a PFAS-free coating for metal beverage cans that meets stringent food-contact safety regulations.

Product innovation continues to enhance performance in extreme environments. Jotun’s November 2025 launch of upgraded zinc-rich barrier technologies improves corrosion resistance in saline offshore conditions, while offering better application efficiency through higher spread rates. Hempel A/S is also advancing fire protection solutions for metal infrastructure through its Hempafire Extreme range, aligned with its “Accelerate to Win” strategy and sustainability targets, including a 90% reduction in Scope 1 and 2 emissions by 2026.

Strategic realignment toward high-margin segments is evident across industry players. Nippon Paint’s January 2026 strategy pivot focuses on expanding its presence in industrial and automotive metal coatings, moving away from commodity decorative paints. BASF Coatings’ September 2025 corporate realignment, including leadership changes ahead of a spin-off, signals a stronger focus on surface technology and metal pretreatment solutions under its Chemetall brand.

Regional strategies and sustainability initiatives are also shaping market dynamics. Beckers Group’s March 2025 push for sustainable coil coatings in Asia-Pacific emphasizes bio-based resins and cool roof technologies, addressing urban heat challenges and energy efficiency requirements in industrial buildings.

Market Trend: Waterborne PVDF Coil Coatings Advancing Low-VOC Architectural Metal Finishes

The metal coatings industry is undergoing a significant transformation in the architectural coil coatings segment, with a rapid transition toward waterborne Polyvinylidene Fluoride (PVDF) systems. This shift is driven by the need to reconcile long-term durability requirements with increasingly stringent environmental regulations targeting volatile organic compound emissions. Traditional solvent-borne PVDF coatings have long been the benchmark for 20+ year weatherability, but new-generation waterborne formulations are now achieving equivalent performance while dramatically reducing environmental impact.

Advanced waterborne PVDF technologies deliver up to a 90% reduction in lifetime VOC emissions compared to solvent-based alternatives, positioning them as a preferred solution for sustainable construction projects. These systems maintain critical performance characteristics, including resistance to ultraviolet degradation, chemical chalking, and color fading, ensuring long-term façade integrity in high-exposure environments. Their integration with reflective pigment technologies is further enhancing their value proposition. Waterborne PVDF coatings used in cool-roof applications demonstrate 300% to 400% greater durability than conventional acrylic-based reflective coatings, which typically degrade within five to seven years.

Adoption rates are increasing rapidly as sustainability criteria become embedded in architectural specifications. By 2026, approximately 35% of new coil-coated metal projects include explicit low-VOC or sustainable coating requirements, reflecting a near doubling of demand compared to 2022. This trend is particularly pronounced in large-scale commercial and landmark developments, where lifecycle performance, environmental certification, and regulatory compliance are critical decision factors. Waterborne PVDF coatings are thus emerging as a cornerstone technology in next-generation architectural metal finishing.

Market Trend: Ultra-Durable Powder Coatings Redefining Corrosion Protection Standards in Heavy Equipment (ACE)

The agriculture, construction, and earthmoving (ACE) equipment sector is driving innovation in metal coatings through the adoption of ultra-durable powder coating systems. Manufacturers are increasingly replacing multi-layer liquid coating systems with high-performance powder coatings that offer superior corrosion resistance, improved process efficiency, and enhanced material utilization.

A key benchmark shift is evident in corrosion performance standards. Where 1,000-hour salt spray resistance was previously considered adequate, leading OEMs now require coatings to exceed 3,000 hours in Neutral Salt Spray testing under ASTM B117 conditions. Advanced epoxy-polyester hybrid powder coatings, combined with zirconium-based pretreatment technologies, are consistently meeting these requirements, achieving less than 2 mm creep at the scribe even under extended exposure. This level of protection is critical for heavy machinery operating in aggressive environments such as construction sites and agricultural fields.

Operational efficiency gains are another major driver of adoption. Single-coat, high-build powder systems eliminate the need for multiple application and curing stages, reducing overall energy consumption per coated component by 25% to 30%. This not only lowers operational costs but also supports sustainability objectives within manufacturing facilities. Additionally, high-edge coverage formulations improve coating uniformity on complex geometries, reducing material waste by approximately 15% compared to liquid coatings that tend to thin out at edges and corners.

These combined advantages are positioning ultra-durable powder coatings as the new standard for protective metal finishing in heavy equipment applications, aligning performance, efficiency, and environmental objectives.

Market Opportunity: US DOE Industrial Decarbonization Programs Accelerating Adoption of Low-Carbon Coating Technologies

The United States Department of Energy’s Industrial Decarbonization initiatives are creating a significant opportunity landscape for the metal coatings industry, particularly through programs focused on reducing emissions from industrial heat processes. Coating application and curing operations are energy-intensive, making them a primary target for decarbonization efforts.

The Industrial Heat Shot initiative aims to reduce greenhouse gas emissions from industrial heating processes by 85% by 2035. This ambitious target is driving innovation in alternative curing technologies, including electric infrared and ultraviolet systems, which can significantly reduce reliance on fossil fuel-based heating. Transitioning from conventional gas-fired convection ovens to these advanced curing methods can lower the carbon footprint of coating lines by more than 60%, creating both environmental and economic benefits.

Financial support is a critical enabler of this transition. Through the Industrial Demonstrations Program, more than $6.3 billion in federal funding has been allocated for large-scale deployment of low-carbon technologies. Coating manufacturers are leveraging this funding to modernize production lines, adopt energy-efficient curing systems, and develop new coating chemistries compatible with lower-temperature or alternative curing processes. This convergence of policy support, technological innovation, and sustainability targets is positioning decarbonized coating solutions as a major growth area within the metal coatings industry.

Market Opportunity: China’s GB 30981.2-2025 Standard Driving Mandatory Transition to Ultra-Low VOC Metal Coatings

China’s updated regulatory framework for industrial coatings is creating a large-scale transformation in the metal coatings market. The implementation of GB 30981.2-2025 introduces stringent requirements for volatile organic compound emissions and harmful substance content, mandating a shift toward ultra-low VOC and environmentally compliant coating systems across automotive and industrial sectors.

The regulation, released in September 2025 with enforcement beginning in February 2026, requires all metal coating operations to undergo recertification, creating immediate demand for compliant formulations. One of the most impactful changes is the strict definition of waterborne coatings, which must now contain more than 50% water by mass in their volatile components. This effectively eliminates “water-reducible” coatings that still rely heavily on organic solvents, forcing manufacturers to adopt genuinely low-emission technologies.

In addition to VOC restrictions, the standard introduces stringent limits on hazardous substances, including a maximum lead content of 90 mg/kg. This aligns industrial coating requirements with safety standards previously applied only to consumer products, significantly raising the bar for material purity and environmental safety.

Given China’s position as a global manufacturing hub, this regulatory shift is expected to influence supply chains and formulation strategies worldwide. Coating manufacturers that can deliver compliant, high-performance, ultra-low VOC solutions are well positioned to capture market share in one of the largest and fastest-evolving metal coatings markets globally.

Metal Coatings Market Share and Segmentation Insights

Coil Coating Captures 30.8% Share Driven by Pre-Painted Metal Demand in Construction and Appliances

The metal coatings market by process method is dominated by coil coating, accounting for 30.8% of the global market share in 2025, fueled by its unmatched efficiency in high-volume metal finishing applications. Coil coating is widely used for pre-painted steel and aluminum coils that supply key industries such as construction (roofing, facades), HVAC systems, and home appliances, delivering consistent color, uniform thickness, and superior surface finish at the lowest applied cost. A major advantage is its continuous production process, which enhances throughput and reduces operational variability. Additionally, coil coating lines are highly sustainable, capable of recovering and recycling over 95% of solvent emissions, ensuring compliance with stringent environmental regulations. This combination of cost efficiency, scalability, and eco-friendly processing positions coil coating as the preferred technology in the global metal coatings industry.

Corrosion Protection Holds 44.6% Share Due to High Economic Impact and Industrial Necessity

In the metal coatings market by functional requirement, corrosion protection leads with a 44.6% market share in 2025, underscoring its critical role in extending asset lifespan across industries. Infrastructure components such as bridges, pipelines, transmission towers, and automotive underbodies rely heavily on anti-corrosion coatings, including zinc-rich primers, galvanizing, and epoxy-based systems, to prevent material degradation in harsh environments. The dominance of this segment is further driven by the significant economic burden of corrosion, which accounts for approximately 3–4% of global GDP annually. As a result, industries prioritize protective metal coatings as the most cost-effective solution for minimizing maintenance costs and preventing structural failures. With rising investments in infrastructure and industrial assets, the demand for high-performance corrosion-resistant coatings continues to drive growth in this segment.

Competitive Landscape in the Metal Coatings Market

AkzoNobel drives profitability and laser-curing innovation in metal coatings

AkzoNobel remains a benchmark in industrial metal coatings, executing a “price-over-volume” strategy to sustain profitability. In Q1 2026, the company reported an adjusted EBITDA of €345 million with a margin expansion to 14.5%, despite a 9% revenue decline following divestments in South Asia. Its strategic exit from India and Pakistan has strengthened its balance sheet, reducing net debt/EBITDA to 2.0x and enabling focus on high-margin European and North American markets. AkzoNobel’s collaboration with IPG Photonics has introduced laser-curing technology that reduces energy consumption by up to 30%. Its Industrial Excellence Program has already eliminated over €980 million in operating expenses, supporting a targeted EBITDA margin above 16% by 2027.

PPG expands metal coatings portfolio with food-safe and data center innovations

PPG Industries is leveraging its R&D capabilities to expand into high-growth metal coating applications such as packaging and data centers. In April 2026, the company launched the first aluminum coil-applied PVC-NI coating in the U.S., meeting stringent FDA and EU food-contact safety standards for pet food packaging. PPG is also investing in radiation-curable coatings technology in France, targeting instant-cure industrial finishes. Its end-to-end protective solutions for hyperscale data centers include low-VOC coatings designed to withstand high-airflow corrosion environments. The acquisition of Ozark Materials has further strengthened PPG’s infrastructure coatings portfolio, integrating advanced metal adhesion technologies into its broader product ecosystem.

Sherwin-Williams leads architectural metal coatings with PVDF innovation and retail strength

The Sherwin-Williams Company dominates the North American architectural metal coatings segment, with a projected 38.2% market share in 2026 supported by its extensive retail network. Its Fluropon® PVDF coatings are industry benchmarks, now enhanced with solar-reflective pigments that reduce building cooling costs by approximately 15%. The company’s “Success by Design” approach integrates digital tools that assist contractors in specifying corrosion-resistant coatings for coastal and high-humidity environments. With record net sales of $23.57 billion in 2025, Sherwin-Williams is expanding into Asia-Pacific construction markets, leveraging its vertical integration and logistics capabilities to maintain supply chain efficiency and product consistency across global operations.

Axalta pioneers EV-focused metal coatings with fire-resistant and low-bake technologies

Axalta Coating Systems is at the forefront of innovation in metal coatings for electric vehicles and advanced mobility applications. In 2026, the company developed Alesta® e-PRO FG Black, a fire-resistant coating capable of delaying thermal propagation at temperatures above 1200°C, addressing critical EV battery safety requirements. Axalta’s Lumeera™ 3250 low-bake clearcoat enables simultaneous coating of metal and plastic components at 80°C, reducing CO₂ emissions by 16 kg per vehicle. Its TintMaster AI platform enhances production efficiency by reducing tinting cycles by 29%. Additionally, Axalta’s waterborne clearcoats have reduced solvent emissions by over 65%, reinforcing its leadership in sustainable automotive coatings.

BASF advances green steel coatings with waterborne DTM and chromium-free solutions

BASF plays a critical role in the metal coatings market by integrating advanced chemical formulations with sustainable coating technologies. At the American Coatings Show 2026, the company introduced a hydroxyl functional acrylate dispersion for waterborne 2K direct-to-metal systems, enabling a single-layer application that replaces traditional multi-coat processes. BASF’s #OurPlasticsJourney initiative is targeting Scope 3 carbon neutrality for industrial coatings by 2030. Its development of hexavalent chromium-free pre-treatments ensures compliance with environmental regulations while maintaining high corrosion resistance. The company is also expanding its Mangalore facility to support growing demand for Acronal® dispersions in South Asia’s industrial metal coatings sector.

Kansai Paint leads ultra-thin and self-healing metal coatings for automotive and aerospace

Kansai Paint is a technological leader in advanced metal coatings, particularly in Asia’s automotive and infrastructure sectors. In 2026, the company achieved a breakthrough in producing coatings with a film thickness of just 1 μm, significantly reducing material weight for aerospace and EV applications. Its self-healing coatings utilize elasticity control technology to absorb scratches and maintain surface integrity in high-end vehicles and appliances. Kansai has also entered a joint venture with PPG to expand automotive finishes in North America and Europe, leveraging its strong domestic market position. With 59% of its development portfolio focused on sustainability, Kansai is actively eliminating hazardous chemicals while advancing high-performance coating technologies.

China Metal Coatings Market: EV Integration and Non-Ferrous Metals Driving Advanced Coating Demand

China dominates the global metal coatings market, supported by its expansive electric vehicle (EV) ecosystem and non-ferrous metals industry. Government initiatives such as the “Action Plan for the Non-Ferrous Metals Industry (2025–2026)” are accelerating industrial growth while emphasizing ultra-high purity metals, recycling efficiency, and advanced coating technologies. The integration of AI-driven optimization systems is transforming coating processes by enabling real-time control over coating thickness, molecular alignment, and performance characteristics.

The country’s leadership in lithium-ion battery housing and lightweight magnesium-aluminum alloy structures is driving demand for high-performance coatings that enhance durability and corrosion resistance. China is also strengthening its supply chain through long-term international agreements for critical materials such as alumina and copper, ensuring stability for fluoropolymer coating applications. Sustainability remains a key focus, with the implementation of carbon footprint tracking systems for aluminum products, aligning coatings with global “green aluminum” standards. These developments position China as a leader in both volume production and next-generation coating innovation.

United States Metal Coatings Market: Smart Infrastructure and Aerospace Coating Innovations

The United States metal coatings market is characterized by high-value applications, digital transformation, and advanced material innovation, particularly in aerospace, infrastructure, and semiconductor sectors. The commercialization of multi-functional smart coatings, incorporating self-healing microcapsules and anti-icing properties, is enhancing performance in extreme environments such as aerospace and renewable energy installations.

Technological advancements include the adoption of IoT-enabled robotic coating systems, reducing material waste and improving precision in automotive and industrial applications. The use of Chemical Vapor Deposition (CVD) and Atomic Layer Deposition (ALD) technologies is enabling ultra-thin coatings for semiconductor devices and medical implants, reflecting the market’s shift toward high-precision applications. Infrastructure investments are driving demand for thermal-reflective and anti-abrasion coatings in bridges and power grids, ensuring long-term durability under changing climate conditions. Regulatory measures promoting domestic production of coating materials are further strengthening innovation and supply chain resilience in the U.S. market.

Germany Metal Coatings Market: Precision Engineering and Sustainable Finishing Leadership

Germany leads the European metal coatings market through its expertise in precision engineering, advanced plating technologies, and sustainability-driven manufacturing. The country is transitioning toward bio-based resins and waterborne coatings, aligning with stringent EU REACH regulations and reducing environmental impact.

Technological innovation includes the development of advanced plating chemicals and LED-based smart curing systems, significantly reducing energy consumption in industrial coating processes. Germany’s dominance in high-end automotive and mechanical engineering sectors is driving demand for durable, high-performance coatings used in precision components. The integration of real-time data analytics in plating lines is enhancing process control, reducing waste, and ensuring consistent coating quality. Regulatory frameworks such as the Supply Chain Due Diligence Act are also shaping the industry by requiring ethical sourcing of critical materials like cobalt and nickel. These factors reinforce Germany’s leadership in sustainable and precision-driven metal coating solutions.

India Metal Coatings Market: Infrastructure Boom and Manufacturing Expansion Accelerating Growth

India is emerging as a high-growth market for metal coatings, driven by large-scale infrastructure projects and expanding domestic manufacturing capabilities. Government initiatives such as the “Gati Shakti” master plan and “Make in India” program are fueling demand for protective coatings in railways, bridges, and public infrastructure.

The increasing use of pre-painted galvanized iron (PPGI) in housing projects under schemes like Pradhan Mantri Awas Yojana is boosting the demand for corrosion-resistant coatings. Investments in renewable energy infrastructure are also driving the adoption of coatings for solar panel structures and wind turbine towers, particularly in coastal regions where corrosion resistance is critical. A shift toward powder coatings in the appliance sector is improving durability while reducing VOC emissions. Additionally, the establishment of localized compounding centers by global manufacturers is enhancing supply chain efficiency and supporting the growth of EV manufacturing hubs across the country.

Japan Metal Coatings Market: Ultra-Thin Film Technologies and High-Speed Rail Applications

Japan’s metal coatings market is defined by its focus on advanced material science, ultra-thin coatings, and high-performance applications in electronics and transportation. The development of nano-composite coatings is enabling superior clarity, heat resistance, and durability for next-generation communication infrastructure such as 5G and 6G towers.

The country is also leading in the application of high-performance coatings for Maglev and Shinkansen rail systems, where low-friction and weather-resistant materials are essential for efficient operation. Infrastructure renewal projects are driving demand for coatings that can be applied over existing surfaces, reducing maintenance costs and downtime. Government incentives promoting energy-efficient building solutions, including cool-roof metal coatings, are further supporting market growth. Additionally, Japan’s strong presence in consumer electronics and robotics is fueling demand for premium aesthetic and functional coatings.

Brazil Metal Coatings Market: Mining, Infrastructure, and Industrial Coatings Expansion

Brazil is emerging as a key regional market for metal coatings, driven by its strong presence in mining, agriculture, and industrial infrastructure sectors. The demand for heavy-duty anti-corrosive coatings is particularly high in mining operations and iron ore transportation, where equipment is exposed to harsh environmental conditions.

Infrastructure development, including the expansion of e-commerce logistics centers, is increasing the need for durable, low-VOC coatings for warehouse systems and industrial facilities. The market also shows a preference for solvent-borne coatings in extreme industrial environments due to their durability and tolerance to surface contamination. Government support for the automotive sector is encouraging local production of OEM coatings and specialty finishes, strengthening domestic capabilities. Additionally, the adoption of ISO 12944 standards is aligning Brazil’s coating industry with global safety and performance benchmarks, enhancing its competitiveness in international markets.

Metal Coatings Market Report Scope

Metal Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$29.8 Billion

|

|

Market Size (2032)

|

$47.9 Billion

|

|

Market Growth Rate

|

7%

|

|

Segments

|

By Resin Type (Epoxy, Polyester, Polyurethane, Acrylic, Fluoropolymer, Plastisol, Siliconized Polyester, Alkyd, Others), By Technology (Water-borne, Solvent-borne, Powder Coatings, Radiation-Cured), By Process Method (Coil Coating, Extrusion Coating, Hot-Dip Galvanizing, Thermal, Batch Spray Coating, Anodizing and Electroplating), By Substrate Type (Steel, Aluminum, Galvanized Steel, Copper and Brass, Specialty Alloys), By End-Use Industry (Building and Construction, Automotive and Transportation, Consumer Goods and Appliances, Industrial Manufacturing, Energy and Power), By Functional Requirement (Corrosion Protection, Wear and Abrasion Resistance, UV and Weathering Resistance, Chemical and Heat Resistance, Aesthetic and Decorative)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Sherwin-Williams Company, PPG Industries, Inc., Akzo Nobel N.V., Nippon Paint Holdings Co., Ltd., Axalta Coating Systems Ltd., BASF SE, Kansai Paint Co., Ltd., Jotun A/S, Hempel A/S, RPM International Inc., Asian Paints Limited, Beckers Group, Tiger Coatings GmbH and Co. KG, KCC Corporation, Sika AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Metal Coatings Market Segmentation

By Resin Type

- Epoxy

- Polyester

- Polyurethane

- Acrylic

- Fluoropolymer

- Plastisol

- Siliconized Polyester

- Alkyd

- Others

By Technology

- Water-borne

- Solvent-borne

- Powder Coatings

- Radiation-Cured

By Process Method

- Coil Coating

- Extrusion Coating

- Hot-Dip Galvanizing

- Thermal

- Batch Spray Coating

- Anodizing and Electroplating

By Substrate Type

- Steel

- Aluminum

- Galvanized Steel

- Copper and Brass

- Specialty Alloys

By End-Use Industry

- Building and Construction

- Automotive and Transportation

- Consumer Goods and Appliances

- Industrial Manufacturing

- Energy and Power

By Functional Requirement

- Corrosion Protection

- Wear and Abrasion Resistance

- UV and Weathering Resistance

- Chemical and Heat Resistance

- Aesthetic and Decorative

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Metal Coatings Industry

- Sherwin-Williams Company

- PPG Industries, Inc.

- Akzo Nobel N.V.

- Nippon Paint Holdings Co., Ltd.

- Axalta Coating Systems Ltd.

- BASF SE

- Kansai Paint Co., Ltd.

- Jotun A/S

- Hempel A/S

- RPM International Inc.

- Asian Paints Limited

- Beckers Group

- Tiger Coatings GmbH & Co. KG

- KCC Corporation

- Sika AG

*- List not Exhaustive