Micro Perforated Films Market 2025–2034: Recyclable Mono-Materials, Adaptive Laser Perforation, and Private Equity Consolidation Reshaping Breathable Packaging

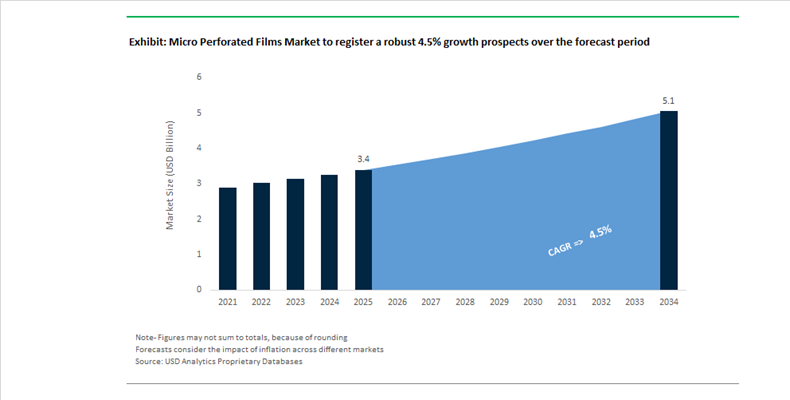

The Micro Perforated Films Market is projected to grow from $3.4 billion in 2025 to $5.1 billion by 2034, registering a CAGR of 4.5%. Demand is being driven by the global shift toward modified atmosphere packaging (MAP), eCommerce-ready breathable mailers, and recyclable mono-material film architectures. Micro perforated films—engineered with laser or mechanical apertures typically ranging from 50 to 200 microns—are critical for controlling oxygen transmission rate (OTR) and moisture vapor exchange in fresh produce, bakery, protein, and chilled food applications. The sector is undergoing structural consolidation and technological reinvention as sustainability mandates, particularly in Europe and North America, push converters toward recyclable, compostable, and fiber-integrated breathable solutions.

In November 2024, Amcor entered into a definitive agreement to acquire Berry Global, with completion in 2025. The $8.4 billion merger created one of the largest flexible packaging platforms globally, combining Amcor’s expertise in breathable produce films with Berry’s North American manufacturing depth. In November 2025, Sealed Air announced its $8.8 billion acquisition by Clayton, Dubilier & Rice, signaling a major transition of the CRYOVAC® innovator into private ownership. These transactions highlight strategic repositioning within the breathable films landscape, where scale, R&D capacity, and capital intensity increasingly determine competitiveness.

Product innovation is centered on mono-material recyclability and adaptive perforation. In February 2026, UFlex Limited launched F-HSS, a co-extruded, heat-sealable PET film engineered for laser perforation and full recyclability, showcased at PLASTINDIA 2026. In January 2026, Coveris introduced MonoFlexBP, a recyclable PP-based structure utilizing precision micro-perforation to regulate OTR for chilled meats and dairy. Meanwhile, PerfoTec expanded deployment of its real-time adaptive laser systems through 2024–2025, enabling dynamic perforation patterns based on measured produce respiration rates—extending berry shelf life by up to 50%. FlexSea commercialized seaweed-derived compostable films with laser micro-perforations in late 2025, providing a plastic-free breathable alternative for organic produce.

Large-scale capacity investments further reinforce growth momentum. In November 2025, Amcor announced a major North American expansion to install advanced extrusion and perforation lines supporting its recycle-ready AmPrima platform through 2026. In January 2026, Mondi secured nine WorldStar Awards, recognizing its integration of micro-perforation into recyclable fiber and film structures. Additionally, Sealed Air launched the AUTOBAG® 850HB in September 2025 to support breathable eCommerce mailers, while Mondi advanced PE-free wrappers across Europe, reflecting a structural shift toward micro-porous paper solutions. Collectively, these developments signal a market transitioning from commodity film supply to data-driven, recyclable, and respiration-optimized breathable packaging systems.

Micro Perforated Films Market Trends and Opportunities

Trend: Strategic Standardization of Breathable Films to Reduce Food Waste Across Retail Supply Chains

Global food retailers and brand owners are accelerating the standardization of micro perforated films as a core packaging format to directly address food waste reduction targets under the UN SDG 12.3 and the EU Farm to Fork Strategy. Unlike conventional sealed films, micro perforated packaging enables controlled gas exchange, reducing moisture accumulation and delaying microbial spoilage. This functionality is now being embedded at scale across fresh produce categories to minimize in-store shrinkage and extend consumer shelf life without chemical preservatives.

Industrial efficacy benchmarks published in March 2025 by PerfoTec demonstrated that laser micro perforated LinerBags extended banana shelf life by up to 21 days by precisely balancing oxygen, carbon dioxide, and humidity. Exporters adopting these formats reported logistics cost reductions and carbon footprint savings of up to 15% due to fewer rejected shipments. Retailers are translating these gains into formal procurement mandates. By mid-2025, Tesco confirmed the removal of over 2.3 billion pieces of conventional plastic, replacing them with PBAT-PLA micro perforated produce wraps certified under OK Compost standards.

The economic imperative is substantial. The EU generates nearly 59 million tonnes of food waste annually, valued at approximately €132 billion. Corporate disclosures from Unilever in 2024 show that the transition to breathable packaging formats across European fresh product lines was a material contributor to achieving a 50% reduction in virgin plastic use. As retailers increasingly link packaging performance to waste KPIs, micro perforated films are shifting from optional innovation to a standardized operational requirement.

Trend: Integration of Micro Perforation with MAP for Proteins and Ready-to-Eat Meals

Micro perforated films are rapidly converging with Modified Atmosphere Packaging to address spoilage risks in high-value protein and ready-meal segments. As MAP expands beyond produce into meat, poultry, and seafood, converters are engineering multilayer barrier films with precision perforation to prevent anaerobic spoilage while preserving visual quality and food safety.

Research published in 2025 confirms that combining MAP with calibrated micro perforation sustains an optimal 70–80% oxygen and 20–30% carbon dioxide environment. This balance preserves beef color bloom while suppressing aerobic bacterial growth, a critical factor for case-ready meat and e-commerce meal kits. To achieve this consistency at industrial scale, packaging leaders such as Uflex Ltd. and Amcor allocated nearly 25% of their 2025 packaging innovation budgets to laser-drilled antimicrobial micro perforated films. Typical perforation diameters of 1–2 mm are now engineered to deliver precise oxygen transmission rates tailored to protein respiration profiles.

Industry consolidation is reinforcing this trend. Strategic moves in late 2024, including acquisitions by Sealed Air, indicate a clear shift toward captive perforation capability. By internalizing perforation technology, film producers can offer integrated MAP solutions to global meat and poultry processors, reducing lead times and ensuring consistent quality across multinational supply chains.

Opportunity: Accelerated Transition to Home-Compostable Micro Perforated Films

The strongest near-term growth opportunity in the micro perforated films market lies in certified home-compostable substrates designed for organic waste streams. As single-use plastic bans tighten and municipal composting infrastructure expands, food service operators are demanding breathable packaging that delivers performance parity while meeting EN 13432 and equivalent standards.

Material innovation is advancing rapidly. Capacity data from September 2025 indicates that global bioplastic production, including PLA, PHA, and starch-based blends, is set to more than double by 2029. These materials offer the vapor permeability required to prevent condensation in salad bags, addressing a primary cause of bacterial decay in traditional plastics. A notable early adopter is Starbucks, which in early 2025 began rolling out home-compostable paper-based wraps with plant-derived breathable coatings across its EMEA operations. These wraps are designed to biodegrade in backyard compost within 90 days, aligning with Starbucks’ 2030 sustainable packaging roadmap.

Regulatory momentum is reinforcing adoption. The EU Packaging and Packaging Waste Regulation, effective from 2025, mandates that all packaging be recyclable or compostable by 2030. This is creating immediate demand for compostable micro perforated pouches across the $200-plus billion global food service and delivery market, positioning certified breathable biopolymers as a strategic growth lever.

Opportunity: High-Definition Printed Breathable Films for Premium Branding

Premium brands are increasingly leveraging micro perforated mono-material films as both a functional and visual differentiator. The ability to combine breathability with high-definition printing allows luxury food and cosmetic brands to eliminate secondary labels, simplify material structures, and improve recyclability without sacrificing shelf appeal.

Printability improvements are driving this shift. In late 2024, polyethylene accounted for 52.6% of the micro perforated films market, largely due to its favorable surface energy for high-speed, high-resolution printing. Converters now routinely apply laser perforation after printing to preserve uninterrupted graphics while maintaining breathability. Consumer perception data from Kerry Group in 2025 shows that 72% of shoppers associate extended shelf life with personal waste reduction, enabling brands to command premium pricing by visibly signaling sustainability benefits.

E-commerce growth is amplifying demand. In Asia-Pacific online grocery channels, transparent micro perforated polypropylene films are becoming standard for premium berry and stone-fruit exports from Latin America to China. These films withstand last-mile logistics stress while delivering a high-quality unboxing experience, positioning HD printed breathable packaging as a critical enabler of premium cross-border food trade.

Micro Perforated Films Market Share and Segmentation Insights

Polyethylene Films Dominate Micro Perforated Films Market Driven by Flexible Packaging Efficiency and Recyclability

Polyethylene accounted for 48.60% of the Micro Perforated Films Market share in 2025, making it the most widely used material for breathable flexible packaging applications. Polyethylene films offer a strong balance of cost efficiency, flexibility, sealability, and compatibility with laser or mechanical micro perforation technologies, which are essential for producing controlled gas transmission in packaging systems. These properties make polyethylene particularly suitable for fresh produce packaging, bakery packaging, and modified atmosphere packaging (MAP) applications, where maintaining product freshness requires controlled oxygen and carbon dioxide exchange. Polyethylene also integrates easily into high-speed packaging lines and supports various converting processes including lamination and printing. In 2025, sustainability initiatives across the packaging industry have accelerated the development of mono-material polyethylene packaging structures, allowing micro perforated films to maintain recyclability while still delivering the breathability required for perishable products. As retailers and regulators increasingly prioritize recyclable packaging formats, micro perforated polyethylene films are becoming a preferred solution for fresh food packaging systems designed for circular packaging economies.

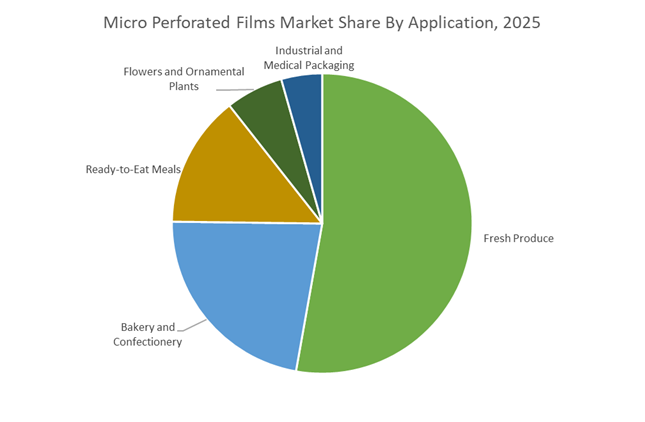

Fresh Produce Packaging Drives the Largest Demand for Micro Perforated Films

Fresh produce accounted for 52.80% of the Micro Perforated Films Market share in 2025, making fruits and vegetables the largest application segment for breathable packaging films. After harvest, fresh produce continues to respire by consuming oxygen and releasing carbon dioxide and moisture, which can accelerate ripening and spoilage if gas exchange is not properly controlled. Micro perforated films are engineered with precisely distributed microscopic holes that regulate oxygen and carbon dioxide transmission rates, maintaining optimal atmospheric conditions inside the package. This controlled environment helps extend the shelf life of leafy greens, berries, mushrooms, tomatoes, and other perishable fruits and vegetables, enabling longer distribution chains and improved product quality at retail. In 2025, increasing global focus on food waste reduction across supply chains has accelerated the adoption of advanced micro perforation technologies. Packaging manufacturers are developing product-specific perforation patterns and laser perforation techniques that optimize respiration balance for different produce varieties, enabling shelf life extensions of three to seven days while maintaining product freshness and reducing spoilage losses in retail and logistics networks.

Micro Perforated Films Market Competitive Landscape

The micro perforated films market in 2026 is driven by laser precision perforation, mono-material recyclable films, and shelf-life optimization technologies. Competitive advantage lies in respiration-matched packaging, anti-mist coatings, and integration of PCR content to meet ESG, EPR, and food waste reduction mandates.

Amcor scales recycle-ready micro perforated films with integrated PE platform and AI-enabled production support

Amcor plc is leading the micro perforated films market through its Scale-to-Sustainability strategy, leveraging its Berry Global integration to build the industry’s largest PE-based breathable film portfolio. The AmPrima® recycle-ready films deliver high clarity and puncture resistance while remaining compatible with PE recycling streams, addressing EPR compliance. Expansion of Calibrate™ technical services enables AI-assisted optimization of micro-perforated film performance on high-speed packaging lines. The company is investing heavily between 2025 and 2027 to expand specialty breathable film capacity for fresh produce and snacks. Its unified manufacturing network ensures consistent supply for high-volume applications. Amcor’s scale, innovation, and sustainability alignment position it as a dominant force in global flexible packaging.

Mondelēz drives global adoption of micro perforated packaging through snack shelf-life optimization and circular design

Mondelēz International plays a pivotal role in shaping micro perforated film demand by defining packaging standards across global snack supply chains. Its 2026 growth strategy emphasizes breathable packaging formats that maintain crispness and moisture balance in biscuits and baked snacks. The company is investing heavily in mono-material perforated films to achieve its 2030 goal of 100% recyclable packaging. Micro-perforation is being used as a resilience tool to reduce spoilage and logistics losses amid volatile raw material costs. With operations in over 150 countries, Mondelēz influences MAP technology adoption at scale. Its focus on shelf-life extension and circular packaging drives innovation across the industry.

UFlex advances high-clarity recyclable films with integrated rPET solutions and precision perforation technology

UFlex Limited is strengthening its leadership in sustainable micro perforated films through innovations in recycling and high-speed manufacturing. Its USFDA-approved single-pellet solution integrates over 30% rPET with virgin PET, enabling clear, durable, and recyclable lidding films. The F-HSS mono-material PET film replaces multi-layer laminates while maintaining heat-seal performance for bakery and confectionery packaging. The CERUFLEX 500 system enables precise, high-volume micro perforation and gravure printing, supporting large-scale production. Strategic partnerships are expanding its footprint in agricultural and pet food packaging. UFlex’s focus on circular materials and engineering excellence positions it strongly in Asia and MEA markets.

Coveris leads European mono-material innovation with high-barrier micro perforated films and closed-loop recycling systems

Coveris Group is defining the European micro perforated films market through its No Waste strategy and award-winning mono-material solutions. Its MonoFlexBP PP-based film delivers high oxygen transmission control and resealable functionality for chilled meat applications. The PaperFeel flow-wrap combines tactile appeal with advanced barrier and perforation performance, enhancing premium packaging differentiation. The ReCover division enables closed-loop recycling of post-consumer and industrial film waste into secondary packaging. Coveris also provides EPR advisory services to help brands navigate evolving regulatory frameworks. Its integrated sustainability and performance approach strengthens its leadership in high-value packaging segments.

TCL Packaging specializes in respiration-matched perforation and anti-mist films for premium fresh produce applications

TCL Packaging is a niche leader in high-precision micro perforated films tailored to the respiration rates of fresh produce. Its EarthFilm® compostable solutions provide sustainable alternatives for lidding and pouch applications, particularly for organic salads and herbs. The company’s scientific testing capabilities enable precise gas transmission rate optimization through customized perforation patterns. Integration of anti-mist technology ensures product visibility and extended shelf life, improving retail performance. Its recyclable LLDPE films comply with UK OPRL standards, supporting circular packaging initiatives. TCL’s focus on data-driven design and premium retail applications differentiates it in the market.

European Union (Germany and France): PPWR Enforcement and Mono-Material Redesign

The European Union is setting the global compliance baseline for micro perforated films through the implementation of the Packaging and Packaging Waste Regulation (PPWR 2025/40), formally published in January 2025. The regulation mandates that all packaging formats must be fully recyclable by August 12, 2026, effectively accelerating the phase-out of complex multi-material laminates. For micro perforated barrier films, this has triggered a structural redesign toward mono-material polyethylene and polypropylene solutions that still deliver controlled oxygen and moisture transmission for fresh food packaging. The regulatory pressure is particularly pronounced in Germany and France, where enforcement mechanisms are already aligned with circular economy roadmaps and retailer-level recyclability scorecards.

Leading converters are responding through precision engineering rather than material substitution alone. Mondi Group expanded its sustainable barrier portfolio in late 2025, introducing mono-material micro perforated films with a 95/5 material purity ratio that preserve oxygen and water vapor barrier performance for coffee and bakery applications. In parallel, Germany’s VerpackDG alignment measures introduced in 2025 provide targeted incentives for film converters deploying laser perforation in breathable produce bags, with documented reductions in food waste of up to 20%. Mondi’s Duino mill start-up in Italy further reinforces Southern Europe’s transition by integrating recycled containerboard with advanced coating and micro perforation lines, supporting paper-based alternatives for fresh produce packaging where plastic reduction targets are most stringent.

United States: Food Safety Traceability and High-Precision OTR Control

In the United States, regulatory momentum is anchored in food safety rather than recyclability alone. The U.S. Food and Drug Administration identified food chemical safety and microbiological risk mitigation as core priorities under its FY 2025 Human Food Program. This has accelerated adoption of laser micro perforated films equipped with AI-driven, real-time oxygen transmission rate control to inhibit pathogen growth in pre-cut salads and fresh convenience foods. Packaging performance is increasingly evaluated on its ability to dynamically regulate respiration rather than static barrier metrics.

Compliance with the FSMA Food Traceability Final Rule is an additional structural driver. With the January 20, 2026 deadline approaching, converters are integrating digital printing and QR-code architectures directly onto micro perforated films to support mandatory Key Data Elements for produce tracking. Innovation-led responses are also shaping the competitive landscape. Amcor launched its Lift-Off Winter 2025/26 challenge to accelerate development of compostable, high-performance OTR barriers, aiming to replace conventional plastic micro perforated films with nature-based systems by 2027. At the same time, 2025 tariffs on selected polymer resins are pushing U.S. converters toward near-shore sourcing and thinner-gauge micro perforated films that reduce resin usage by up to 20% without compromising mechanical strength.

India: EPR Spillover Effects and Fresh Commerce Acceleration

India’s micro perforated films market is being reshaped by Extended Producer Responsibility enforcement and structural changes in food distribution. The April 2025 EPR mandate requiring 30% recycled content in rigid plastics has created a spillover effect across flexible packaging, particularly for fresh produce windows and breathable pouches. Suppliers such as Ganesha Ecopet have significantly expanded rPET output to supply food-grade recycled resins compatible with micro perforation and moisture control requirements.

Demand-side acceleration is coming from quick-commerce platforms operating in Tier-1 cities. Rapid delivery models for berries, mushrooms, and leafy greens are increasing reliance on micro perforated fresh-lock pouches that manage condensation and respiration during short but intense logistics cycles. On the supply side, India has invested over INR 10,000 crore since 2022 in chemical recycling and decontamination infrastructure. By 2026, these assets are expected to enable scaled production of food-safe micro perforated films derived from post-consumer waste, aligning circularity objectives with high-growth urban food distribution.

China: Digital Manufacturing and Shelf-Life Optimization

China is advancing micro perforated film adoption through industrial digitalization and agricultural efficiency mandates. The Ministry of Industry and Information Technology released a 2026 manufacturing upgrade blueprint that incentivizes installation of high-speed laser perforation systems capable of sub-30 micron hole sizes. These investments are designed to elevate export quality for packaged agricultural goods and reduce spoilage during long-distance inland transport.

Field validation is reinforcing commercial uptake. Trials conducted during 2024–2025 demonstrated that laser micro perforated liners could extend banana shelf life by up to three weeks, leading to nationwide adoption for fruit logistics. At the consumer level, China’s CEWC 2025 directive to stimulate domestic consumption is driving premiumization in bakery and confectionery categories. In humid southern provinces, micro perforated crisp-touch films are increasingly specified to maintain texture and freshness, positioning breathable packaging as a quality differentiator rather than a cost add-on.

Saudi Arabia and United Arab Emirates: Circular Polymers and Controlled-Environment Agriculture

In the Gulf region, growth is closely linked to circular polymer strategies and controlled-environment agriculture. SABIC introduced more than 90 circular products in Q3 2025 under its TRUCIRCLE™ platform, including high-clarity polyolefins engineered for precision micro perforation. These materials are increasingly deployed in hydroponic and vertical farming applications across Saudi Arabia and the UAE, where breathable films play a critical role in moisture and gas management.

Logistics efficiency is also improving. Updates to S&P Global Platts FOB Straits nomination standards in February 2025 have streamlined export flows from the GCC, supporting global distribution of advanced resins used in micro perforated film production. This positions the region as a material innovation hub rather than only a feedstock supplier.

Comparative Snapshot: Country-Level Dynamics in the Micro Perforated Films Market

Micro Perforated Films Market County Level Snapshot

|

Region

|

Primary Policy Driver

|

Technology Focus

|

Key End-Use Pull

|

Strategic Implication

|

|

European Union

|

PPWR recyclability mandate

|

Mono-material laser perforation

|

Fresh food, bakery, coffee

|

Structural redesign of film architectures

|

|

United States

|

FSMA traceability and food safety

|

AI-driven OTR control, digital IDs

|

Pre-cut produce, convenience foods

|

Performance-led packaging adoption

|

|

India

|

EPR enforcement and Q-commerce

|

rPET-compatible micro perforation

|

Fresh produce, rapid delivery

|

Circular films at urban scale

|

|

China

|

Industrial digitalization

|

High-speed laser perforation

|

Agriculture, bakery

|

Shelf-life extension at scale

|

|

Saudi Arabia & UAE

|

Circular economy and CEA

|

High-clarity circular polyolefins

|

Hydroponics, vertical farming

|

Materials-led differentiation

|

Micro Perforated Films Market Report Scope

Micro Perforated Films Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.4 Billion

|

|

Market Size (2034)

|

$5.1 Billion

|

|

Market Growth Rate

|

4.5%

|

|

Segments

|

By Material Type (Polyethylene, Polypropylene, Polyethylene Terephthalate, Biodegradable and Compostable Materials), By Perforation Technology (Laser Perforation, Mechanical Perforation, Electrostatic Perforation), By Application (Fresh Produce, Bakery and Confectionery, Ready-to-Eat Meals, Flowers and Ornamental Plants, Industrial and Medical Packaging), By Packaging Format (Pouches, Bags and Liners, Wraps and Lidding Films, Rollstock)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor, Mondi Group, Sealed Air, Berry Global, SABIC, Coveris, Constantia Flexibles, Bolloré Group, Uflex, PerfoTec, Wipak Group, TC Transcontinental, Jindal Poly Films, Now Packaging, Siegwerk

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Micro Perforated Films Market Segmentation

By Material Type

- Polyethylene

- Polypropylene

- Polyethylene Terephthalate

- Biodegradable and Compostable Materials

By Perforation Technology

- Laser Perforation

- Mechanical Perforation

- Electrostatic Perforation

By Application

- Fresh Produce

- Bakery and Confectionery

- Ready-to-Eat Meals

- Flowers and Ornamental Plants

- Industrial and Medical Packaging

By Packaging Format

- Pouches

- Bags and Liners

- Wraps and Lidding Films

- Rollstock

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Micro Perforated Films Market

- Amcor

- Mondi Group

- Sealed Air

- Berry Global

- SABIC

- Coveris

- Constantia Flexibles

- Bolloré Group

- Uflex

- PerfoTec

- Wipak Group

- TC Transcontinental

- Jindal Poly Films

- Now Packaging

- Siegwerk

*- List not Exhaustive