Microcapsule Market 2025–2034: Biodegradable Encapsulation, Nutrient Stabilization, and Controlled-Release Platforms Drive High-Growth Trajectory

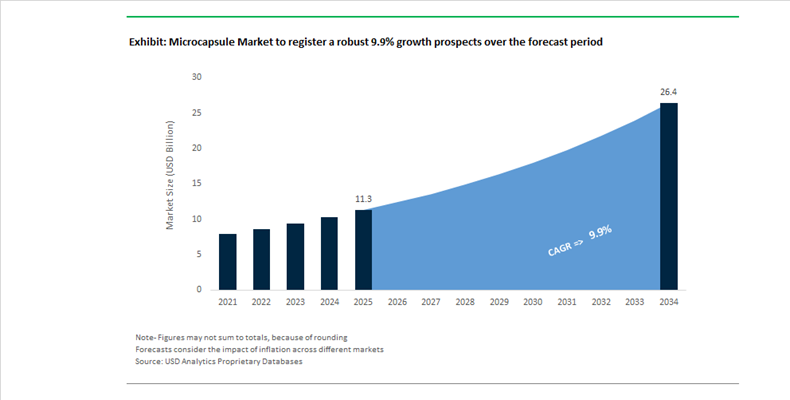

The Microcapsule Market is projected to expand from $11.3 billion in 2025 to $26.4 billion by 2034, reflecting a strong CAGR of 9.9%. Growth is being propelled by regulatory pressure on microplastics, rising demand for controlled-release actives, and technological advancements in spray drying, fluidized bed coating, coacervation, and polymeric microsphere systems. Microencapsulation is increasingly viewed as a precision-delivery platform rather than a simple protective coating mechanism, with applications spanning personal care, pharmaceuticals, textiles, agriculture, and functional foods. The market is undergoing a structural pivot toward biodegradable, plant-based, and microplastic-free shell materials, particularly in Europe and Asia-Pacific, where environmental regulations are accelerating reformulation cycles.

In November 2025, Givaudan expanded its PlanetCaps™ biodegradable fragrance technology into personal care. Originally developed for fabric care, the platform eliminates microplastic-based capsules and aligns with tightening ECHA regulations while preserving long-lasting scent release in shampoos and body washes. This strategic move complements Givaudan’s early 2026 announcement to expand encapsulation capacity at its Singapore facility, supporting its goal of transitioning its entire fragrance capsule portfolio to biodegradable solutions by 2030. Parallel innovation in agrochemicals emerged in late 2024 when Milliken & Company launched a microplastic-free polymer encapsulation system for pesticides, enabling timed release while minimizing runoff and regulatory risk.

Nutritional and pharmaceutical encapsulation technologies are advancing rapidly. In October 2025, BASF introduced Lutavit® A/D3 1000/200 NXT, a combined microencapsulated vitamin beadlet for animal feed that enhances stability and simplifies dosing logistics. In May 2024, Lubrizol launched LIPOFER™, designed to encapsulate iron for food fortification, masking metallic taste and preventing oxidative discoloration. Consumer-facing innovation accelerated in early 2025 when TopGum introduced microencapsulated caffeine gummies engineered for high loading and sustained release. Meanwhile, in November 2024, Yili Group partnered with Xampla to deploy plant-protein-based capsules for vitamin fortification in dairy, eliminating synthetic polymers from nutrient delivery systems.

Industrial-scale investment underscores long-term confidence in encapsulation platforms. In August 2025, Capsulae committed €5 million to new French facilities featuring closed-circuit spray drying and fluidized bed systems for probiotics and enzyme coatings. Textile applications expanded in January 2025 when Devan launched Sleep Tight, embedding microcapsules in fibers for nocturnal active release. In pharmaceuticals, InnoCore Pharmaceuticals secured EU Just Transition Fund backing in November 2025 to advance peptide-loaded microspheres using its SynBiosys® platform, targeting extended-release metabolic therapies. Collectively, these developments confirm that the microcapsule market is transitioning from niche additive technology to a cross-sector controlled-delivery infrastructure supporting sustainability, stability, and precision performance across global value chains.

Microcapsule Market Trends and Opportunities

Trend: Mandatory Shift Toward Biodegradable Microcapsules in Personal Care and Detergents

The microcapsule market is undergoing a structural transformation as consumer goods manufacturers respond to tightening microplastics regulations, most notably Regulation (EU) 2023/2055 restricting intentionally added synthetic polymer microparticles. This regulatory shift has moved biodegradable and non-persistent microcapsules from a niche innovation into a compliance-driven necessity across personal care, home care, and fabric care applications. From October 17, 2025, the EU’s first phase of mandatory microplastics disclosure requirements came into force, compelling fragrance houses and formulators to redesign encapsulation chemistries while preserving performance attributes such as scent longevity and controlled release.

Leading fragrance suppliers such as Givaudan have accelerated investments in compliant platforms like PlanetCaps™, which eliminate persistent synthetic polymers while maintaining encapsulation integrity during manufacturing and consumer use. To meet rising global demand, Givaudan announced capacity expansion plans in Singapore targeted for commissioning by Q1 2026, underscoring the industrial-scale pivot toward biodegradable encapsulation. Similarly, CPL Aromas expanded its AromaCore Bio technology in January 2025, introducing friction-activated biodegradable capsules for shampoos and conditioners that release fragrance during hair brushing and degrade naturally after disposal.

Beyond compliance, biodegradability is becoming a lever for premiumization. New laundry serum formats launched in December 2025 integrate microcapsules with fragrance loads approaching 40%, delivering residual scent performance for up to one year of storage. In the $120+ billion global fabric care market, this long-lasting sensory performance is being used to justify higher price points while aligning brands with the EU Zero Pollution Action Plan’s target of reducing microplastic emissions by 30% by 2030.

Trend: Expansion of Self-Healing and Functional Microcapsules in Smart Infrastructure

Microencapsulation is redefining material performance in the construction and infrastructure sector by enabling self-healing, energy-efficient, and longer-lasting building materials. Aging infrastructure, rising maintenance costs, and the urgent need to decarbonize cement-intensive industries are driving adoption of microcapsule-enabled “active” materials. Large-scale trials reported in late 2025 show that biomineralized self-healing concrete systems, incorporating microcapsules loaded with microbial spores and nutrients, can autonomously repair cracks up to 2.0 mm wide and restore structural strength by as much as 135% after healing.

Advanced encapsulation chemistries are also gaining traction. Microcapsules with urea-formaldehyde shells containing epoxy resins or isocyanates such as TDI and IPDI demonstrate initial repair efficiencies between 80% and 95% when activated by mechanical stress from crack propagation. Studies highlighted in MDPI during 2024–2025 confirm that these systems significantly extend service life in bridges, tunnels, and marine structures, reducing lifecycle carbon emissions by delaying repair and replacement cycles.

In parallel, Phase Change Material microcapsules are being integrated into wallboards, plasters, and insulation to regulate indoor temperatures through latent heat absorption and release. This functionality supports Energy Star and LEED certification objectives and positions microcapsules as a critical enabling technology within the $500 billion global green building market, where energy efficiency and durability are increasingly linked to asset valuation and regulatory approval.

Opportunity: Microencapsulation to Unlock Ambient-Stable Functional Foods and Probiotics

Functional foods and probiotics represent a high-growth opportunity for the microcapsule market as manufacturers seek to overcome the historical limitations of cold-chain dependence and poor gastric survival. Microencapsulation technologies now allow live microorganisms and sensitive bio-actives to withstand thermal processing, extended shelf storage, and acidic gastric conditions, enabling their incorporation into mainstream ambient food formats.

In early 2025, multinational food producers launched ambient-stable “Happy Gut” cereal ranges using clinically validated probiotic strains protected by multi-layer microencapsulation. This innovation enables live culture delivery without refrigeration, expanding addressable markets and accelerating penetration of gut-health products into mass retail. Precision encapsulation is also being applied to minerals and micronutrients, where advanced enteric coatings and spray-drying eliminate metallic off-tastes associated with iron and zinc fortification. This allows everyday products such as plant-based milks and functional beverages to be fortified without compromising sensory quality, aligning with the proactive wellness behavior now observed in approximately 60% of global consumers.

Looking ahead, the convergence of microbiome sequencing and encapsulated delivery systems is paving the way for personalized nutrition. By 2026, manufacturers are expected to deploy microcapsules engineered to release targeted probiotic strains in specific regions of the lower intestine, maximizing therapeutic efficacy and opening premium, prescription-adjacent nutrition segments.

Opportunity: Compliance-Driven Adoption of Microencapsulated Agrochemicals

The agrochemical sector is emerging as a structurally attractive growth avenue for microcapsules as regulators enforce tighter controls on pesticide usage, drift, and environmental contamination. Microencapsulation enables controlled-release formulations that reduce active ingredient load per hectare while maintaining or improving efficacy, directly supporting Green Deal and Integrated Pest Management mandates across Europe and North America.

In November 2025, the Codex Alimentarius Commission adopted updated guidelines on pesticide purity and stability, favoring encapsulated formulations that minimize volatilization, runoff, and groundwater leaching. Industry disclosures from late 2025 indicate that microencapsulated herbicides and insecticides are increasingly viewed as the optimal solution for precision agriculture, offering timed release, improved rainfastness, and enhanced worker safety by limiting direct exposure.

Investment momentum is building around bio-based encapsulation polymers. In October 2025, BASF and IFF announced strategic collaborations to develop next-generation bio-based encapsulation systems for agro-actives. These initiatives aim to reduce the environmental footprint of intensive farming by up to 20% while delivering sustained pest control, positioning microencapsulation as a cornerstone technology in the transition toward more sustainable and regulation-compliant agriculture.

Microcapsule Market Share and Segmentation Insights

Spray Technologies Lead the Microcapsule Market Through Scalable and Cost-Efficient Encapsulation Processes

Spray technologies accounted for 42.80% of the Microcapsule Market share in 2025, establishing them as the most widely used encapsulation approach across food, pharmaceutical, and agrochemical industries. Spray-based encapsulation methods such as spray drying, spray cooling, and spray chilling enable efficient encapsulation of active ingredients into protective shells while maintaining controlled particle size and functional release characteristics. These technologies are particularly suitable for high-volume production because they offer excellent scalability, lower processing costs, and compatibility with heat-sensitive compounds, making them widely adopted in industrial encapsulation systems. Spray drying remains the most dominant technique due to its ability to convert liquid emulsions or suspensions into free-flowing microencapsulated powders used in nutraceuticals, flavors, pharmaceuticals, and crop protection products. In 2025, advancements in atomization nozzle design, drying chamber aerodynamics, and digital process control systems have significantly improved spray drying efficiency, reducing energy consumption while increasing production yields and particle uniformity. These improvements allow manufacturers to produce highly consistent microcapsules while maintaining the economic advantages that make spray technologies the preferred encapsulation method for large-scale industrial production.

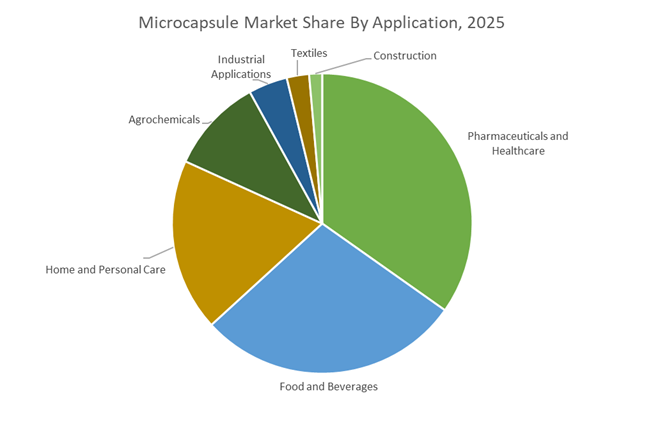

Pharmaceuticals and Healthcare Sector Drives the Largest Demand for Microencapsulation Technologies

Pharmaceuticals and healthcare accounted for 34.80% of the Microcapsule Market share in 2025, making the sector the largest consumer of advanced microencapsulation technologies. Microencapsulation plays a critical role in modern drug formulation by enabling controlled drug release, protection of active pharmaceutical ingredients, improved bioavailability, taste masking, and targeted delivery mechanisms. These benefits are particularly valuable in oral drug formulations, injectable therapies, topical treatments, and implantable drug delivery systems. Pharmaceutical manufacturers use microencapsulation techniques to protect sensitive drug molecules from environmental degradation while ensuring predictable release profiles that enhance therapeutic efficacy and patient compliance. In 2025, the growing pipeline of biologic therapeutics, peptide drugs, and protein-based medicines has significantly increased demand for advanced encapsulation systems capable of maintaining molecular stability during storage and delivery. New polymer carriers and encapsulation materials are being developed to protect fragile biologics while enabling sustained-release delivery systems, which reduce dosing frequency and improve treatment outcomes in chronic disease management.

Microcapsule Market Competitive Landscape

The microcapsule market in 2026 is driven by biodegradable polymer encapsulation, stimuli-responsive release systems, and ECHA-compliant microplastic-free technologies. Competitive leadership is defined by precision microfluidics, natural polymer shells, and smart-release systems that enhance bioavailability and reduce environmental persistence across pharma, agrochemical, and personal care applications.

BASF drives regulatory-compliant microencapsulation with scalable vitamin and personal care innovations

BASF SE maintains a dominant position in the microcapsule market through its Verbund integration and large-scale, sustainable production capabilities. Its Lutavit® A/D3 NXT platform delivers high-stability vitamin encapsulation with an 18-month shelf life, addressing animal nutrition performance requirements. In personal care, VitaGuard A stabilizes retinol through controlled-release microcapsules, improving efficacy and reducing skin irritation. BASF is aligning its portfolio with EU Regulation 2024/3190, ensuring food-contact and cosmetic compliance with BPA- and BPS-free materials. Its ability to scale biodegradable encapsulation technologies reduces carbon footprint by approximately 15% compared to conventional systems. BASF’s combination of regulatory readiness, process scale, and innovation secures its leadership in high-performance encapsulation.

Givaudan accelerates biodegradable fragrance delivery with PlanetCaps™ and high-load encapsulation systems

Givaudan is redefining the microcapsule landscape through its PlanetCaps™ biodegradable technology, eliminating synthetic microplastics in fragrance delivery. Expansion into personal care in 2025–2026 enables scalable deployment across body and hair applications with diverse scent profiles. Its IRRESISTIBLE Laundry Serum demonstrates advanced encapsulation with a 40% fragrance load and extended scent release lasting up to one year. Capacity expansion in Singapore strengthens its global manufacturing footprint for sustainable scent technologies. Under its 2030 strategy, Givaudan is targeting biotech beauty and specialty adjacencies where encapsulation enhances sensory performance. Its focus on eco-friendly, high-load delivery systems positions it as a leader in premium fragrance microcapsules.

IFF advances plastic-free encapsulation platforms through bioscience integration and portfolio optimization

International Flavors & Fragrances (IFF) is strengthening its position in sustainable microencapsulation through its ENVIROCAP platform, a plastic-free scent delivery system tailored for next-generation fabric care. The company is integrating bioscience and polymer expertise through its collaboration with BASF to develop advanced bio-based encapsulation technologies. With $10.89 billion in 2025 revenue, growth is increasingly driven by encapsulated oils, enzymes, and fragrance systems. IFF’s ongoing portfolio reset, including divestment of non-core businesses, is redirecting capital toward high-margin encapsulation solutions. Its focus on sustainable performance and functional delivery systems supports strong adoption across home care and personal care sectors. IFF’s innovation pipeline positions it as a key player in biodegradable microcapsule technologies.

Syngenta integrates smart-release agrochemical microcapsules with AI-driven crop management platforms

Syngenta is a global leader in agricultural microencapsulation, focusing on controlled-release systems that improve crop yield and reduce environmental impact. Its Evelta biofungicide leverages encapsulation to enhance efficacy against persistent fungal threats in EU and UK markets. The Ecovelex seed treatment platform demonstrates regulatory acceptance of sustainable encapsulated biologicals, particularly in maize applications. Syngenta integrates its Cropwise® digital platform with encapsulated inputs, enabling AI-driven application based on real-time disease pressure. Strategic partnerships with SAP are enhancing supply chain optimization for encapsulated seed technologies. Its “Crop System” approach positions Syngenta at the forefront of precision agriculture and smart-release agrochemicals.

Lonza leads pharmaceutical microencapsulation with lipid nanoparticle delivery and CDMO integration

Lonza Group is the benchmark for pharmaceutical-grade microencapsulation, specializing in lipid nanoparticle (LNP) systems for mRNA therapeutics and advanced drug delivery. Its encapsulation technologies ensure high stability and targeted delivery of sensitive genetic materials, supporting next-generation vaccines and therapies. Lonza’s CDMO model enables seamless transition from lab-scale development to commercial manufacturing within a validated regulatory framework. The company is expanding its API encapsulation services, focusing on taste masking and controlled-release formulations to improve patient compliance. Its expertise in biocompatible materials ensures compliance with stringent USFDA and EMA standards. Lonza’s leadership in precision drug delivery positions it at the core of high-value pharmaceutical microcapsule applications.

United States: Compliance-Driven Automation and High-Value Functional Uses

The United States microcapsule market is being reshaped by regulatory compliance requirements and application pull from pharmaceuticals and infrastructure. The U.S. Environmental Protection Agency has mandated Workplace Chemical Protection Programs for facilities handling high-volume chemicals used in capsule synthesis, with key exposure monitoring and control deadlines set for November 9, 2026. This requirement is accelerating investment in enclosed, automated microencapsulation systems that minimize operator exposure while improving batch-to-batch consistency. Manufacturers are prioritizing in-line monitoring, closed reactors, and robotic handling as baseline capabilities rather than optional upgrades.

Policy-led R&D funding is reinforcing this shift. Under the Bioeconomy Executive Order, federal grants issued in 2025 prioritized plant-based capsule shells, triggering a 35% increase in research spending on chitosan and alginate systems to replace melamine-formaldehyde chemistries in consumer goods. Demand-side adoption is strongest in pharmaceuticals, where the U.S. Food and Drug Administration emphasized bioavailability and bioequivalence in its 2025 industry guidance. As a result, microencapsulation has become standard in new oral drug development to protect sensitive APIs and enable targeted intestinal release. Beyond healthcare, the U.S. Department of Transportation funded pilot programs in late 2025 using microencapsulated self-healing agents in concrete, signaling durable infrastructure as an emerging non-traditional growth vector.

Germany: Microplastic Compliance and Precision Performance Formulations

Germany’s microcapsule landscape is defined by rapid alignment with European chemical policy and high-performance formulation requirements. In response to the European Chemicals Agency restriction on intentionally added microplastics, German leaders such as BASF and Evonik completed portfolio transitions in 2025 to ensure all new fragrance and detergent capsules meet biodegradability criteria by January 2026. This has shifted R&D focus toward bio-based walls and rapid environmental disintegration without compromising release precision.

Agriculture and food are parallel demand anchors. BASF’s Liberty Lock formulation, launched in late 2025, uses advanced microencapsulation to deliver herbicides only upon leaf contact, improving weed control while reducing drift and leaching. In food applications, standards introduced by the Federal Ministry of Food and Agriculture have accelerated use of spray-dried microcapsules for omega-3s and probiotics, now embedded across a significant share of new health-oriented dairy launches. Germany is also emerging as a smart textile hub, integrating microencapsulated phase change materials into athletic wear through collaborations with Aachen-based textile organizations, enabling dynamic thermal regulation for 2026 commercialization.

China: Industrial Upgrading and Scale in Pharma and Agriculture

China is advancing microcapsule adoption through industrial modernization and targeted subsidies. The Ministry of Industry and Information Technology 2026 blueprint prioritizes reductions in hazardous byproduct emissions, leading to the phased shutdown of low-tech coacervation units and rapid replacement with spray-drying and fluid-bed coating systems, particularly in Jiangsu. This transition is improving environmental performance while raising the technical baseline for domestic suppliers.

High-value applications are scaling in parallel. Electronic-grade microcapsules used in CMP slurries recorded strong uptake in 2025 to support advanced semiconductor fabrication, where controlled release of abrasive particles is critical. Pharmaceutical policy alignment has also fast-tracked approvals for pH- and enzyme-responsive smart drugs as China’s drug market expands. In agriculture, subsidies under the Rural Revitalization Plan are accelerating deployment of microencapsulated fertilizers, with pilot programs in the Yangtze River basin demonstrating meaningful reductions in nitrogen runoff, positioning controlled-release inputs as a policy-backed standard.

Switzerland: Corporate-Led Innovation in Sustainable Scent Delivery

Switzerland functions as a global command center for microcapsule innovation through multinational fragrance and flavor companies. Givaudan expanded its PlanetCaps™ platform in November 2025, extending biodegradable, microplastic-free capsules into personal care and scaling production capacity in Singapore in early 2026. This expansion reflects brand-owner demand for compliant, high-performance scent delivery systems across home and personal care.

Similarly, International Flavors & Fragrances introduced ENVIROCAP™ in mid-2025, a biopolymer-based system designed for precise release during fabric wear rather than wash cycles. Both companies have deployed AI-driven robotic dosing to control capsule wall thickness with high precision, directly linking manufacturing accuracy to fragrance release performance. Switzerland’s role is therefore less about volume production and more about setting global technology standards that cascade across regional manufacturing hubs.

India: Export-Oriented Pharma and Clean-Label Food Applications

India’s microcapsule market is expanding through pharmaceutical exports and consumer-driven clean-label preferences. The Department of Pharmaceuticals, India reported that microencapsulation now underpins the majority of exported value-added generics, driven by taste masking and controlled release requirements for pediatric and geriatric medicines. This has positioned Indian manufacturers as cost-efficient, formulation-focused partners for global pharma supply chains.

Food and packaging are additional accelerators. Demand for natural encapsulation using gums and resins rose sharply in 2025, aligned with clean-label trends that discourage synthetic polymers. In urban logistics, rapid delivery platforms are adopting microencapsulated oxygen scavengers in flexible films to extend shelf life of berries and pre-cut vegetables during short delivery windows. These use cases are reinforcing India’s role as an application-driven innovator rather than a commodity capsule producer.

South Korea: Electronics and Beauty-Led Functionalization

South Korea’s microcapsule market is anchored in advanced electronics and premium beauty. Companies such as LG Chem and Samsung SDI are integrating microcapsules into liquid silicone rubber systems for EV battery thermal management, where heat-absorbing capsules mitigate thermal spikes during fast charging. This positions microencapsulation as a safety-critical material technology within next-generation mobility.

In consumer markets, the K-beauty sector is driving rapid innovation. The growth of mist-to-serum products in 2025 has relied on microencapsulated vitamins that remain stable in aqueous formulations and release upon application. This fusion of material science and sensory performance is sustaining South Korea’s leadership in high-margin cosmetic applications.

Comparative Snapshot: Country-Level Dynamics in the Microcapsule Market

Microcapsule Market County Level Snapshot

|

Country / Region

|

Primary Policy or Demand Driver

|

Technology Emphasis

|

Core End-Use Sectors

|

Strategic Positioning

|

|

United States

|

WCPP compliance and bioavailability guidance

|

Automated, enclosed systems

|

Pharma, infrastructure

|

Compliance-led premiumization

|

|

Germany

|

ECHA microplastic restriction

|

Biodegradable precision capsules

|

Agrochemicals, food, textiles

|

Regulation-aligned performance

|

|

China

|

MIIT green upgrading and subsidies

|

Spray-drying, smart release

|

Pharma, semiconductors, agriculture

|

Scale with modernization

|

|

Switzerland

|

Corporate sustainability leadership

|

Biopolymer scent delivery, AI dosing

|

Home and personal care

|

Global innovation hub

|

|

India

|

Export pharma and clean-label demand

|

Natural encapsulation

|

Generics, food, packaging

|

Application-driven growth

|

|

South Korea

|

EV safety and K-beauty trends

|

Thermal and cosmetic capsules

|

Batteries, cosmetics

|

High-value functional niches

|

Microcapsule Market Report Scope

Microcapsule Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$11.3 Billion

|

|

Market Size (2034)

|

$26.4 Billion

|

|

Market Growth Rate

|

9.9%

|

|

Segments

|

By Technology (Spray Technologies, Physicochemical Encapsulation, Chemical Encapsulation, Mechanical Encapsulation), By Coating Material (Polymers, Gums and Resins, Lipids and Waxes, Carbohydrates, Proteins), By Application (Pharmaceuticals and Healthcare, Food and Beverages, Home and Personal Care, Agrochemicals, Textiles, Construction, Industrial Applications)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF, Givaudan, International Flavors and Fragrances, Evonik Industries, Symrise, SABIC, Dow, Balchem, Encapsys, Lycored, Ingredion, Lonza, 3M, Mitsubishi Chemical, Shin-Etsu Chemical

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Microcapsule Market Segmentation

By Technology

- Spray Technologies

- Physicochemical Encapsulation

- Chemical Encapsulation

- Mechanical Encapsulation

By Coating Material

- Polymers

- Gums and Resins

- Lipids and Waxes

- Carbohydrates

- Proteins

By Application

- Pharmaceuticals and Healthcare

- Food and Beverages

- Home and Personal Care

- Agrochemicals

- Textiles

- Construction

- Industrial Applications

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Microcapsule Market

- BASF

- Givaudan

- International Flavors and Fragrances

- Evonik Industries

- Symrise

- SABIC

- Dow

- Balchem

- Encapsys

- Lycored

- Ingredion

- Lonza

- 3M

- Mitsubishi Chemical

- Shin-Etsu Chemical

*- List not Exhaustive