Global Molded Fiber Packaging Market Overview: Eco-Friendly Innovation Driving Growth

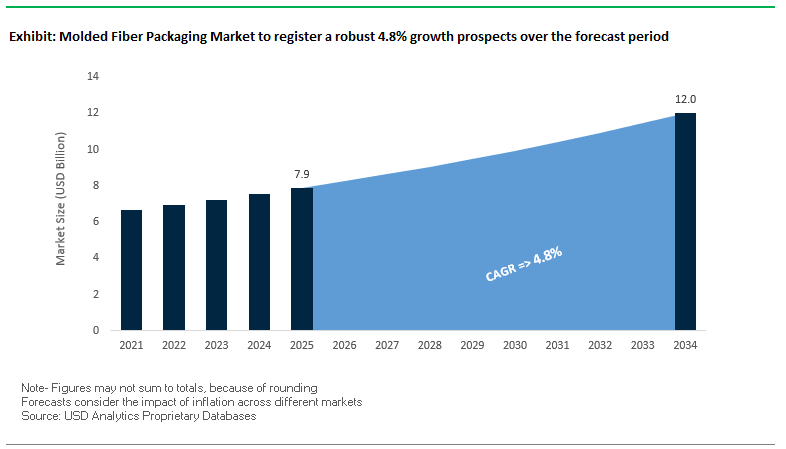

The global molded fiber packaging market is projected to grow from USD 7.9 billion in 2025 to USD 12 billion by 2034, reflecting a CAGR of 4.8%. This growth is underpinned by the worldwide transition toward sustainable, eco-friendly packaging solutions, a movement accelerated by government regulations, consumer awareness, and the rising dominance of e-commerce. Molded fiber packaging has emerged as a strong alternative to plastics due to its biodegradability, recyclability, and low carbon footprint, making it highly attractive for both established and emerging industries.

For buyers and industry professionals, the market addresses key concerns such as packaging performance, regulatory compliance, and supply chain sustainability. The versatility of molded fiber enables its use in food, electronics, healthcare, agriculture, and logistics, making it a strategic investment for businesses navigating stricter packaging mandates and green consumer expectations.

Key Insights for Industry Stakeholders

- E-Commerce and Food Delivery Expansion: Rapid online shopping and takeaway food growth are fueling demand for shock-absorbing, lightweight molded fiber packaging.

- Circular Economy Leadership: Over 65% of molded fiber packaging uses recycled newsprint and cardboard, making it a key player in sustainable materials.

- Entry into High-Value Segments: Electronics and healthcare sectors are increasingly adopting precision-molded inserts that combine strength with a premium look.

- Technology Upgrades: Thermoforming and dry molding advancements are improving production efficiency with cycle times as low as 3.5 seconds.

Market Analysis: Strategic Developments and Industry Momentum

The molded fiber packaging market is experiencing accelerated transformation, marked by investments in new facilities, cross-industry collaborations, and groundbreaking applications. In October 2024, Google transitioned its Pixel, Fitbit, and Nest product packaging to entirely plastic-free formats, achieved through a partnership with Veritiv and Shandong Kaili Specialty Paper Co. This move exemplifies the push from global brands toward stronger, more versatile paper-based solutions.

The momentum continued in December 2024, when PulPac AB secured a €20 million loan from the European Investment Bank to expand its patented Dry Molded Fiber (DMF) technology across Europe. This was followed by strategic milestones in February 2025, when HZ Green Pulp introduced the first DMF plant in Malaysia and Nippon Molding licensed the same technology in Japan. The adoption of DMF technology in Asia highlights its role as a scalable and eco-friendly alternative to single-use plastics.

By March 2025, PulPac partnered with SIG to explore molded fiber closures as substitutes for plastic caps and lids. The innovation drive expanded further in April 2025, when Diageo initiated live bar trials of a paper-based Johnnie Walker bottle, a first-of-its-kind experiment in molded fiber applications. Industry collaborations deepened in June 2025, when PulPac and Matrix Pack agreed to co-develop molded fiber lids for takeaway drinks.

Meanwhile, in July 2025, Tekni-Plex launched a 200,000-square-foot molded fiber facility in Ohio, reinforcing North American production capacity. That same month, market analysts flagged growing opportunities in agriculture through biodegradable seedling trays, signaling fresh avenues for fiber packaging. The innovation landscape culminated in August 2025, when the introduction of graphene-oxide coatings enhanced molded fiber disposables, offering grease- and moisture-resistant solutions without harmful PFAS chemicals.

Emerging Trends and Growth Opportunities in the Molded Fiber Packaging Market

Strategic Capacity Expansion by Major Players to Meet Surging Demand

The molded fiber packaging market is experiencing a wave of aggressive capacity expansion, driven by escalating demand across foodservice, e-commerce, and healthcare applications. Leading manufacturers are no longer relying on incremental upgrades but are making multi-million-dollar commitments to expand facilities and adopt advanced molding technologies. For instance, in November 2023, India-based start-up Fibmold secured $10 million in funding from Omnivore and Accel to build facilities that upcycle agricultural waste into molded fiber packaging. Such funding highlights investor confidence in sustainable packaging. Similarly, Renew is developing an industrial hemp pulp facility, projected to produce 30 tons of pulp per day by Q4 2026, signaling how alternative fibers are moving into industrial-scale production. In Asia, Nippon Molding’s adoption of PulPac’s Modula Dry Molded Fiber (DMF) machine in April 2025 marks a critical leap toward water-saving, high-speed production, strengthening the region’s technological edge. These expansions underline the industry’s dual strategy: scaling output while embedding innovation into manufacturing.

Product Innovation Driven by Corporate Sustainability Commitments

Corporate sustainability targets are catalyzing breakthroughs in molded fiber packaging that extend beyond simple plastic replacement. Multinationals are using molded fiber as a core enabler of their plastic-free packaging strategies. In 2025, Google achieved its landmark goal of making all hardware packaging, including Pixel, Fitbit, and Nest, 100% plastic-free, creating sustained demand for high-performance molded fiber solutions. Likewise, Bayer’s partnership with PAPACKS to develop biodegradable packaging for Aspirin reflects the pharmaceutical sector’s growing reliance on molded fiber to meet recyclability mandates by 2030. Technical innovation is also reshaping product performance. New plant-based coatings are being engineered to improve resistance to oxygen and water vapor, allowing molded fiber to serve in sensitive applications such as food preservation and pharmaceutical storage. This marks a paradigm shift from molded fiber being perceived merely as protective packaging to being a high-performance, multi-functional material aligned with sustainability-driven innovation.

Capitalizing on Legislative Bans on Single-Use Plastics and PFAS

The regulatory landscape is one of the most powerful drivers of molded fiber adoption. Governments worldwide are enforcing strict bans on single-use plastics, creating immediate substitution opportunities. In India, the Ministry of Environment, Forest and Climate Change has enforced a ban on disposable plastic plates, cups, and trays since July 2022, seizing over 775,000 kg of banned items. This legislative shift is directly funneling demand toward molded fiber alternatives. In the United States, momentum is building around PFAS restrictions, which are critical in food packaging due to their grease- and water-resistant applications. With states rolling out model legislation banning PFAS, molded fiber packaging with safe, PFAS-free coatings is emerging as a compliance-ready solution. Meanwhile, the European Union’s PPWR directive is reshaping the packaging ecosystem by demanding recyclability and waste reduction. Molded fiber, being recyclable, compostable, and lightweight, aligns perfectly with this policy-driven shift. Collectively, these regulatory measures are not temporary shifts but structural accelerants for long-term market growth.

Penetration into New, High-Value Industrial and Logistics Sectors

Beyond traditional use cases in foodservice and consumer goods, molded fiber packaging is making strong inroads into industrial and logistics segments, driven by its durability and sustainability credentials. The e-commerce sector is a prime example, where molded fiber accounted for more than 680,000 metric tons of protective packaging in 2023, with adoption by 88 of the top 100 global e-commerce logistics providers. Its cushioning performance ensures safe shipment of fragile goods while meeting environmental targets. In industrial and automotive packaging, over 1.2 million cubic meters of foam and plastics have been replaced by molded fiber inserts for machinery, electronics, and white goods, driven by superior vibration dampening properties. Healthcare applications represent another fast-growing vertical: in 2023, over 930,000 metric tons of molded fiber products were used in hospitals and clinics worldwide for bedpans, trays, and specimen containers, across more than 27,000 facilities. These expansions into high-value sectors reinforce molded fiber’s versatility and position it as a transformative force in the global packaging landscape.

Competitive Landscape: Key Players Driving the Molded Fiber Packaging Industry

The molded fiber packaging industry is highly competitive, with global leaders advancing through technological innovation, regional expansions, and sustainability-driven strategies. Companies are increasingly focusing on precision applications, lightweighting, and circular economy integration to capture demand from high-growth sectors like food delivery, electronics, and healthcare.

Huhtamaki Oyj strengthens global sustainability leadership

Huhtamaki Oyj (Finland) is recognized as a pioneer in molded fiber food packaging, offering eco-friendly fiber lids, trays, and cartons. The company has invested heavily in thermoforming and dry molding technologies to develop advanced, high-performance alternatives to plastics. With a strong global footprint and commitment to circular economy models, Huhtamaki is enhancing its modular production capacity to meet growing regulatory and consumer demands for sustainable packaging.

Brodrene Hartmann A/S expands in agricultural packaging

Brodrene Hartmann A/S (Denmark) focuses primarily on egg and fruit packaging. With its strong reliance on recycled raw materials and vertically integrated supply chains, the company ensures consistent, sustainable production. Hartmann is investing in new global facilities to strengthen its position in agricultural packaging markets, while delivering protective, biodegradable, and recyclable solutions designed for food safety and efficiency.

Pactiv Evergreen, Inc. targets foodservice sector growth

Pactiv Evergreen (USA) is a prominent supplier of molded pulp trays, cups, and foodservice packaging. The company leverages large-scale production capabilities in North America, catering to quick-service restaurants and institutional catering providers. Its product development aligns with shifting consumer preferences and regulatory mandates, positioning Pactiv Evergreen as a go-to provider of sustainable foodservice packaging solutions.

UFP Technologies, Inc. delivers precision molded fiber solutions

UFP Technologies (USA) specializes in protective molded fiber packaging for healthcare, electronics, and automotive industries. The company stands out for its expertise in custom design and precision manufacturing, meeting complex requirements for cushioning, anti-static protection, and stability. UFP continues to innovate packaging designs that not only safeguard high-value goods but also enhance consumer experience, particularly in electronics unboxing.

PulPac AB scales Dry Molded Fiber technology globally

PulPac AB (Sweden) is the driving force behind Dry Molded Fiber (DMF) technology, a breakthrough innovation that reduces water usage by up to 99% and energy consumption by 80% compared to wet molding. Operating as a licensor, PulPac partners with companies like SIG and Matrix Pack to commercialize its high-speed production machinery—PulPac Modula and Scala—globally. These platforms enable rapid development of lids, trays, and cutlery designed to replace single-use plastics.

DS Smith plc advances circular economy packaging solutions

DS Smith (UK) provides sustainable packaging solutions with a strong molded fiber portfolio targeting retail, consumer electronics, and logistics sectors. Its closed-loop material recovery systems and custom fiber packaging designs help global brands reduce environmental impact while achieving efficiency gains. DS Smith’s molded fiber products are fully recyclable and central to its vision of transitioning industries away from plastic packaging through resource-efficient innovations.

Molded Fiber Packaging Market Share Insights

Molded Fiber Packaging Market Share by Product Type

Trays dominate the molded fiber packaging market, accounting for 32% of total demand in 2025. Their leadership is directly tied to their widespread use in the food and beverage sector—particularly egg cartons, fruit trays, and meat and poultry packaging. These applications represent steady, high-volume consumption, making trays the backbone of molded fiber production. Their cost-effectiveness, stackability, and ease of mass manufacturing further strengthen their dominance. Clamshells follow with 22% share, emerging as a fast-growth category fueled by their ability to replace clear plastic clamshells in retail applications ranging from bakery items to electronics accessories. Their hinged design provides a balance of product visibility and protection, appealing to both retailers and eco-conscious consumers. End caps, while holding a smaller share, are essential in industrial and automotive applications where molded fiber provides sustainable corner and edge protection during transit. This segment thrives on B2B demand rather than consumer-facing factors, highlighting its resilience. Boxes and bowls & cups, meanwhile, represent the growing consumer-facing shift, driven by the expansion of food delivery platforms and quick-service restaurants (QSRs). With global plastic bans tightening, these segments are gaining traction as sustainable solutions for ready-to-eat meals and takeout packaging, aligning directly with the surging demand in foodservice packaging.

Molded Fiber Packaging Market Share by End-User Industry

The food and beverage industry is the undisputed driver of the molded fiber packaging market, holding a commanding 68% share in 2025. This dominance is underpinned by the enormous global consumption of single-use packaging in sectors such as egg cartons, trays for produce, and fast-food containers. More importantly, the F&B sector is under the most direct regulatory scrutiny, with plastic bans and extended producer responsibility (EPR) mandates accelerating the shift to molded fiber. Electrical and electronics packaging accounts for 11% of the market, and while smaller in volume, it is highly valuable. This segment relies on custom-molded designs for cushioning delicate products like smartphones, laptops, and high-value components, aligning with corporate ESG commitments to reduce plastic in supply chains. Healthcare packaging represents 7% of demand, where molded fiber solutions cater to sterile medical trays, instrument holders, and diagnostic devices. Here, the premium is placed on safety and hygiene while retaining eco-friendly credentials, making it a niche but high-value category. The automotive sector also uses molded fiber in industrial transit packaging for sensitive components such as bumpers, battery modules, and fragile electronic parts, with growth tied to the automotive industry’s sustainability push. Finally, personal care and cosmetics is an emerging premiumization-driven segment, where molded fiber packaging’s natural aesthetic reinforces brand identity for eco-conscious consumers in products like compacts, foundation trays, and luxury gift sets, enabling companies to position sustainability as part of their value proposition.

United States: Innovations in Non-Wood Fibers and Foodservice Packaging Fuel Market Growth

The United States molded fiber packaging market is undergoing a rapid transformation, with strong momentum driven by the adoption of non-wood fibers such as sugarcane bagasse, wheat straw, and bamboo. These alternative fibers are being integrated into molded packaging solutions to meet sustainability targets while offering versatility in shaping complex forms. In addition, U.S. companies are investing heavily in coatings and additives research to enhance moisture and oil resistance, particularly for foodservice applications. The exploration of food-safe PFAS alternatives, such as graphene oxide, signals a critical industry pivot toward safer and more eco-friendly products.

Foodservice packaging stands out as a core growth driver in the U.S., supported by surging demand for cups, lids, and clamshells used in delivery and takeout. Local bans on EPS foam containers further accelerate this transition to molded fiber solutions. E-commerce packaging is another high-potential segment, with companies positioning molded fiber as a green substitute for plastic inserts in protective shipping. A noteworthy example is Dart Container Corporation’s collaboration with PulPac to bring Dry Molded Fiber (DMF) production lines to the domestic market, demonstrating strategic efforts to scale sustainable packaging.

China: Government Support and Electronics Packaging Cement Market Leadership

China is emerging as a global powerhouse in molded fiber packaging, underpinned by strong government-led sustainability policies. Beijing’s push for biodegradable and eco-friendly packaging has created a highly favorable regulatory landscape, encouraging both domestic and multinational companies to invest in sustainable alternatives. This regulatory emphasis aligns with China’s role as a hub for electronics manufacturing, where molded fiber packaging is increasingly used to protect sensitive devices during transport.

The e-commerce boom in China adds another layer of demand, with leading platforms prioritizing sustainable packaging for high-volume deliveries. On the supply side, companies like Sinar Mas are expanding production capacity with new paper plants to address the rising need for pulp-based products. Automation and advanced molding technologies are being rapidly integrated to meet high-volume requirements, improving scalability for the electronics, food, and beverage sectors. These advancements firmly position China as a leader in both manufacturing efficiency and adoption of molded fiber solutions.

Germany & France: EU Regulations and Premium Packaging Drive Adoption

Germany and France play pivotal roles in Europe’s molded fiber packaging landscape, where regulatory pressures and consumer expectations for sustainability converge. The EU’s Single-Use Plastics Directive has been a game-changer, forcing industries to move away from conventional plastics and embrace recyclable and biodegradable packaging. This regulatory shift has spurred rapid adoption of molded fiber, particularly in high-value markets.

European brands are leveraging molded fiber for premium applications in cosmetics, electronics, and gourmet food products, capitalizing on its eco-friendly image and upscale feel. Partnerships between manufacturers and technology providers, such as Omni-Pac Group’s collaboration with HP to digitize production, highlight Europe’s leadership in merging sustainability with advanced manufacturing. Innovation in product design also sets the region apart, exemplified by Hartmann’s "Plus View" egg carton, which enhances consumer experience by combining functionality with visual appeal. Together, Germany and France embody a market where regulation, technology, and premium positioning create a dynamic growth environment.

India: Rising Food & Beverage Consumption and Startup Investments Reshape the Market

India’s molded fiber packaging market is expanding rapidly, fueled by strong growth in the food and beverage sector. Increasing consumption of packaged foods and the expansion of quick-service restaurants are generating demand for molded trays, clamshells, and containers. Government-led sustainability initiatives and corporate commitments to plastic reduction are further accelerating adoption. Amazon India’s adoption of molded pulp packaging and Godrej Interio’s use of recycled molded fiber in furniture packaging reflect how both global and domestic brands are aligning with eco-friendly packaging trends.

India’s market is also seeing momentum from venture capital and startup activity. Companies like Cirkla are attracting early-stage funding to scale sustainable packaging technologies, signaling strong investor confidence. At the same time, local manufacturers are focusing on automating production and optimizing supply chains to balance cost efficiency with sustainability goals. This combination of corporate adoption, startup innovation, and government support is setting India on a fast-track trajectory for molded fiber packaging growth.

Japan: Dry Molded Fiber Technology and High-Quality Standards Redefine Packaging

Japan’s molded fiber packaging industry is being shaped by both regulatory and consumer-driven sustainability goals. The government’s Act on Promotion of Resource Circulation for Plastics has intensified efforts to reduce plastic waste, creating a clear shift toward alternatives such as molded fiber. This aligns with growing public concern about marine litter and resource conservation, making molded fiber a natural fit for the Japanese market.

Technology adoption is a defining feature, with companies like Nippon Molding pioneering the use of PulPac’s Dry Molded Fiber (DMF) technology. The successful testing of PulPac Modula machines highlights how Japan is integrating cutting-edge processes to expand fiber-based packaging portfolios. Beyond technology, Japan emphasizes high-quality and responsible packaging. Nippon Molding’s commitment to offering resource-efficient, circular packaging solutions underscores the nation’s focus on balancing performance, sustainability, and consumer trust.

Brazil: Abundant Raw Materials and Foodservice Growth Stimulate Demand

Brazil represents a unique opportunity for molded fiber packaging, driven by both abundant raw materials and market demand. With one of the strongest pulp and forestry sectors in the world, Brazil has a built-in advantage in securing raw materials for molded fiber production. According to the Brazilian Tree Industry, a significant portion of national forestry output is dedicated to pulp, ensuring consistent and cost-effective supply chains for molded fiber manufacturers.

On the demand side, Brazil’s large foodservice and packaged food industries are key growth engines. As brand owners shift away from conventional packaging in response to environmental regulations, molded fiber trays, clamshells, and containers are becoming mainstream solutions. The combination of regulatory pressure, raw material availability, and strong food sector demand makes Brazil one of the most strategically attractive markets in Latin America for molded fiber packaging growth.

Molded Fiber Packaging Market Report Scope

Molded Fiber Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$7.9 Billion

|

|

Market Size (2034)

|

$12 Billion

|

|

Market Growth Rate

|

4.8%

|

|

Segments

|

By Product Type (Trays, Clamshells, End Caps, Boxes, Bowls & Cups, Others), By Molded Type (Thick Wall, Transfer Molded, Thermoformed Fiber, Processed Pulp), By Source (Wood Pulp, Non-Wood Pulp), By End-User Industry (Food & Beverage, Electrical & Electronics, Healthcare, Automotive, Personal Care & Cosmetics, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Huhtamaki Oyj, Brodrene Hartmann A/S, UFP Technologies, Inc., CKF Inc., Sabert Corporation, Pro-Pac Packaging Limited, Sonoco Products Company, Genpak, LLC, Henry Molded Products, Inc., Keiding, Inc., EnviroPAK Corporation, Eco-Products, Inc. (A subsidiary of Novolex), Fabri-Kal, Thermoform Engineered Quality LLC, Maspack Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Molded Fiber Packaging Market Segmentation

By Product Type

- Trays

- Clamshells

- End Caps

- Boxes

- Bowls & Cups

- Others

By Molded Type

- Thick Wall

- Transfer Molded

- Thermoformed Fiber

- Processed Pulp

By Source

By End-User Industry

- Food & Beverage

- Electrical & Electronics

- Healthcare

- Automotive

- Personal Care & Cosmetics

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Molded Fiber Packaging Market

- Huhtamaki Oyj

- Brodrene Hartmann A/S

- UFP Technologies, Inc.

- CKF Inc.

- Sabert Corporation

- Pro-Pac Packaging Limited

- Sonoco Products Company

- Genpak, LLC

- Henry Molded Products, Inc.

- Keiding, Inc.

- EnviroPAK Corporation

- Eco-Products, Inc. (A subsidiary of Novolex)

- Fabri-Kal

- Thermoform Engineered Quality LLC

- Maspack Limited

*List not Exhaustive

Research Coverage

This report investigates the global molded fiber packaging market with a comprehensive focus on eco-friendly innovations, regulatory impacts, and technological breakthroughs shaping the industry. It delivers in-depth analysis reviews on strategic developments, corporate sustainability initiatives, and product performance upgrades that position molded fiber as a high-potential replacement for plastics. By highlighting growth drivers, barriers, and transformative applications across foodservice, healthcare, electronics, and industrial packaging, this report is an essential resource for stakeholders navigating sustainability mandates and evolving consumer demands. With detailed competitive benchmarking, technology adoption mapping, and forward-looking forecasts, USDAnalytics ensures readers gain actionable insights to strengthen market positioning and capitalize on emerging opportunities. The report highlights case studies, industry milestones, and future projections that capture the ongoing transformation of molded fiber packaging, making it indispensable for decision-makers and investors across global supply chains.

Scope Highlights

- Segmentation: By Product Type (Trays, Clamshells, End Caps, Boxes, Bowls & Cups, Others), By Molded Type (Thick Wall, Transfer Molded, Thermoformed Fiber, Processed Pulp), By Source (Wood Pulp, Non-Wood Pulp), By End-User Industry (Food & Beverage, Electrical & Electronics, Healthcare, Automotive, Personal Care & Cosmetics, Others)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Timeframe: Historic data from 2021–2024 with market forecasts from 2025–2034.

- Companies: Includes analysis and profiles of 15+ leading players such as Huhtamaki Oyj, Brodrene Hartmann A/S, UFP Technologies, PulPac AB, Pactiv Evergreen, DS Smith plc, and others.

Methodology

The research methodology combines primary and secondary approaches to ensure data reliability and market accuracy. Primary research involved interviews with industry executives, packaging engineers, sustainability experts, and supply chain stakeholders across multiple regions. Secondary research included analysis of annual reports, regulatory databases, patents, sustainability disclosures, and verified industry journals. Advanced data triangulation was applied to validate market sizing and growth projections, integrating macroeconomic indicators, raw material pricing trends, and technological adoption models. Forecasts were built using both top-down and bottom-up approaches, while regional insights were contextualized against policy frameworks, consumer trends, and trade flows. This rigorous, multi-layered methodology ensures that the report provides accurate, fact-based insights aligned with real-world industry dynamics.

Deliverables:

• Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

• Country-Specific Forecasts & Analysis.

• Segment-Wise Revenue Forecasts (2025–2034).

• Competitive Analysis, Benchmarking, and SWOT Profiles.

• Recent Developments & Innovation Tracker.

• Executive Summary & Analyst Commentary.

• Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.