Market Overview: Advanced Microphase-Engineered Copolymers Driving High-Performance Applications

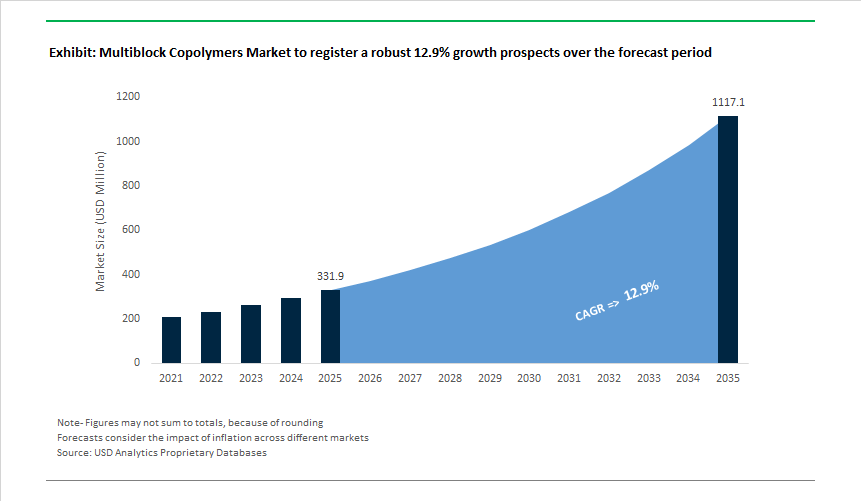

The Global Multiblock Copolymers Market is valued at USD 331.9 million in 2025 and is projected to reach USD 1,116.7 million by 2035, expanding at a 12.9% CAGR as multiblock architectures move from specialty polymer science into commercially scaled, application-critical materials. Market growth is being shaped less by generic polymer demand and more by end-use sectors that require precise mechanical behavior, durability under stress, and compliance with tightening sustainability and regulatory frameworks.

Multiblock copolymers sit at the intersection of performance engineering and material efficiency. Unlike traditional polymers, they allow manufacturers to dial in properties at the molecular level, balancing elasticity, strength, toughness, and processability within a single material system. This capability is becoming increasingly valuable as OEMs seek to reduce part counts, simplify assemblies, and replace multi-material solutions with single, high-function polymers.

Demand is accelerating across thermoplastic elastomers (TPEs), styrenic block copolymers (SBCs), biomedical polymers, adhesives, and specialty automotive components, where predictable performance under cyclic load, temperature variation, and long service life is essential. For these applications, multiblock copolymers are not substitutes-they are enablers of new product design.

Key End-Market Forces Driving Adoption

- Automotive and Mobility: Lightweighting, vibration damping, and durability requirements are pushing OEMs toward advanced TPEs and SBCs that combine high elongation with structural integrity. Multiblock copolymers enable soft-touch, flexible components that withstand long-term mechanical stress without creep or fatigue.

- Biomedical and Drug Delivery: Controlled-release systems, resorbable implants, and drug carriers increasingly rely on engineered multiblock architectures to achieve predictable degradation and high payload efficiency. These applications are structurally insulated from price volatility and benefit from long qualification cycles.

- Adhesives, Sealants, and Consumer Goods: Pressure-sensitive adhesives, flexible packaging, and high-performance consumer products require materials that deliver consistent elasticity, adhesion, and surface feel-attributes that multiblock copolymers can tailor more precisely than conventional elastomers.

Sustainability is also becoming a market access requirement. The integration of renewable and mass-balance-certified feedstocks into multiblock copolymers is accelerating adoption, particularly in Europe and among global brand owners. Renewable-content SBCs and recyclable TPEs allow manufacturers to meet carbon-reduction targets and circular plastics regulations without sacrificing performance, reinforcing long-term demand.

Over the forecast period, the multiblock copolymers market is transitioning from an advanced materials niche into a core platform for next-generation elastomers and functional polymers. Growth through 2035 will be above-average and high quality, supported by durable end-use demand, sustainability mandates, and the need for materials that combine multiple performance attributes in a single polymer system. Companies that align polymer architecture innovation with scalable manufacturing and sustainability certification will be best positioned to capture disproportionate value as this market matures.

Market Analysis: Sustainability Leadership, M&A Expansion, and Compounding Investments Redefine Global Competitiveness

The global multiblock copolymers industry is experiencing strong strategic momentum as leading manufacturers place sustainability, advanced compounding, and application diversification at the center of growth strategies. In December 2025, Industrie Polieco’s international acquisition of The Compound Company expanded its presence across high-performance adhesive resins and thermoplastic compounds, signaling consolidation across Europe’s performance polymer segment. On the other hand, sustainability commitments intensified across the industry: Kraton Corporation announced long-term 2032 climate and resource-efficiency targets in November 2025, strengthening its leadership in renewable SBCs and circular polymer technologies. The same month, ICIS established a new PP block copolymer price index in South Korea (August 2025), providing essential transparency for automotive and industrial markets in Asia-Pacific where block copolymer demand is accelerating.

Infrastructure and automotive investments continued driving demand for specialized block copolymer formulations. Borealis’ €100+ million expansion of PP compounding capacity in September 2025 aims to meet the rising need for lightweight automotive materials incorporating multiblock additives for impact resistance and flexibility. Sustainability credentials further strengthened when Kraton received the EcoVadis Platinum Award (September 2025) for the fifth consecutive year, reinforcing best-in-class ESG performance in specialty polymer manufacturing. In April 2025, the company launched its CirKular+™ Paving Circularity Series, demonstrating how advanced block copolymers significantly improve reclaimed asphalt pavement (RAP) reuse efficiency for low-carbon infrastructure.

Earlier milestones also shaped the strategic landscape. In March 2025, Kraton’s France facility achieved ISCC PLUS certification, enabling commercial-scale production of renewable SBCs, expanding on its June 2023 investment that began producing 100% renewable SBCs capable of reducing carbon footprints by up to 85%.

Multiblock Copolymers Market Trends and Opportunities

Trend 1: Multiblock Copolymer Electrolyte Membranes Enabling Long-Duration Energy Storage

The acceleration of long-duration energy storage (LDES) deployment is reshaping membrane material requirements, positioning multiblock copolymers as a structurally superior alternative to perfluorinated ion-exchange membranes. Grid-scale flow batteries, particularly vanadium redox flow batteries (VRFBs) and emerging non-aqueous systems, demand membranes that simultaneously deliver high ionic conductivity, low active-species crossover, and long mechanical life under continuous cycling. Multiblock architectures based on polysulfone (PSU), polyphenylsulfone (PPSU), and sulfonated PEEK derivatives are gaining traction because they spatially separate hydrophilic ion-conducting domains from mechanically robust hydrophobic blocks. Peer-reviewed studies from late 2024–2025 show that this phase-segregated morphology reduces vanadium crossover rates by up to 60–70% compared with random copolymers, directly extending stack efficiency and electrolyte lifetime. This materials shift aligns with hard demand signals from national grid planners: India’s Central Electricity Authority has formally projected 336 GWh of storage requirements by 2030, while Viability Gap Funding programs launched in 2024–2025 are already catalyzing multi-gigawatt-hour flow battery deployments. Importantly, multiblock copolymers also tolerate higher operating temperatures, which lowers electrolyte viscosity and pumping losses in next-generation redox systems. As utilities prioritize lifetime cost per delivered kilowatt-hour over upfront capex, membrane durability and chemical selectivity—rather than raw conductivity alone—are becoming decisive procurement criteria, structurally favoring engineered multiblock copolymer systems.

Trend 2: Styrenic Multiblock Copolymers Replacing Epoxies in Advanced Electronics Assembly

In advanced electronics and semiconductor packaging, styrenic multiblock copolymers (SBCs) are emerging as a critical materials solution to the mechanical and thermal stresses introduced by device miniaturization. Hydrogenated SBCs such as SEBS and SEPS are increasingly displacing rigid epoxies in die-attach adhesives, underfills, and thermal interface materials because they provide elastic compliance without sacrificing thermal and chemical stability. As chip architectures move toward fan-out wafer-level packaging (FOWLP), heterogeneous integration, and higher I/O densities, managing coefficient-of-thermal-expansion mismatch has become a yield-limiting factor. Industry data from 2025 indicates that SBC-modified adhesive systems can reduce package-level stress concentrations sufficiently to improve manufacturing yields by approximately 15%, while also shortening cure cycles and cutting overall assembly time by nearly 30%. This performance advantage is especially relevant in automotive electronics and 5G infrastructure, where components are exposed to repeated thermal ramps, vibration, and oxidative environments. With global 5G connections approaching 1.8 billion by 2025, OEMs are prioritizing materials that maintain adhesion and elasticity across thousands of thermal cycles. Hydrogenated SBCs meet this requirement while remaining compatible with high-throughput, low-temperature processing—making them structurally aligned with both cost-down pressures and reliability mandates in advanced electronics manufacturing.

Opportunity 1: Olefin Block Copolymers as the Backbone of Monomaterial Flexible Packaging

Global regulatory pressure on plastic waste and recyclability is creating a powerful growth window for olefin block copolymers (OBCs) in flexible packaging. Brand owners are actively dismantling multi-material laminate structures that are incompatible with mechanical recycling, replacing them with monomaterial polyethylene-based films that still require toughness, sealability, and heat resistance. OBCs uniquely enable this transition by combining rigid polyethylene crystallites with elastomeric soft segments in a single molecular architecture. In 2025, the commercialization of next-generation OBC resins allowed biaxially oriented polyethylene (BOPE) films to meet demanding packaging performance standards—such as hot-fill resistance and high-speed printing—without introducing incompatible polymer layers. This capability directly supports emerging policy frameworks, including extended producer responsibility schemes and national “circular economy” mandates in Asia and Europe. Closed-loop collaborations between resin producers and consumer brands are reinforcing demand, with early programs already incorporating double-digit percentages of post-consumer recycled content into fully recyclable packaging. Beyond packaging, OBCs are also gaining traction in hygiene and footwear applications, where their superior elastic recovery and low compression set outperform legacy elastomers while remaining recyclable within polyolefin streams. As recyclability shifts from a marketing claim to a regulatory requirement, OBCs are positioned as a structural enabler of compliant, scalable packaging redesign.

Opportunity 2: RAFT-Engineered Multiblock Copolymers for Precision Biomaterials

Controlled radical polymerization—particularly Reversible Addition–Fragmentation Chain Transfer (RAFT)—is unlocking a high-value opportunity for multiblock copolymers in biomedical and pharmaceutical applications. Unlike conventional polymer synthesis, RAFT enables precise control over block sequence, molecular weight, and end-group functionality, which is increasingly essential for medical devices, drug delivery systems, and biointerfaces. Research published during 2024–2025 demonstrates that optimized RAFT pathways can achieve exceptionally low dispersity (Đ ≈ 1.1–1.2) while preserving end-group fidelity, reducing cytotoxic side reactions that have historically limited synthetic polymer use in vivo. This precision allows engineers to design copolymers that respond predictably to biological triggers such as pH shifts or enzyme presence. The opportunity is expanding rapidly as AI-guided synthesis platforms automate RAFT experimentation, enabling the rapid screening of thousands of polymer architectures for poorly soluble drugs and targeted therapies. In parallel, multiblock copolymers incorporating bioactive sequences are being developed to mimic natural peptide assemblies, allowing controlled release of therapeutic payloads within hours in response to disease-specific enzymes. As pharmaceutical pipelines increasingly focus on complex biologics and precision oncology, RAFT-derived multiblock copolymers are transitioning from academic novelty to enabling infrastructure for next-generation drug delivery and implantable medical technologies.

Market Share Analysis: Multiblock Copolymers Market

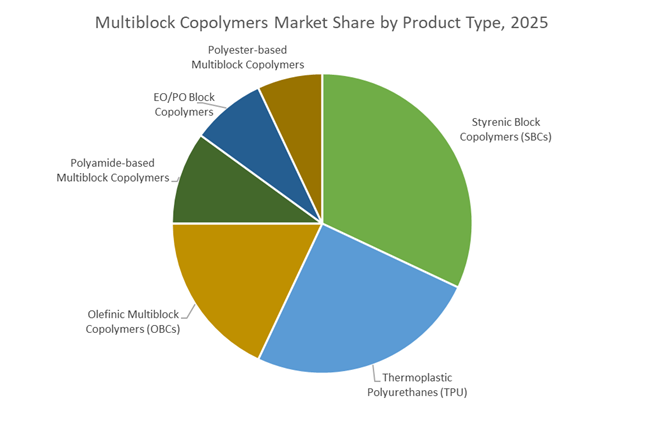

Market Share by Product Type: Styrenic Block Copolymers as the Volume Anchor of Flexible Polymers

Styrenic Block Copolymers (SBCs) hold the largest share of the multiblock copolymers market at ~32% in 2025, primarily because they deliver the lowest cost-to-performance ratio across high-volume flexible applications. Global SBC production has reached ~3.11 million tons, with Styrene-Butadiene-Styrene (SBS) accounting for 72.1% of total SBC tonnage, according to 2025 disclosures from Kraton and Sinopec. SBS dominance is structurally linked to asphalt modification and footwear, where procurement decisions are driven by price stability, rheological consistency, and large-scale availability rather than niche performance differentiation. At the same time, hydrogenated SBCs (SEBS/SEPS) are emerging as the value engine within this segment, expanding at a ~4.53% CAGR as they replace conventional rubber in high-temperature and regulatory-sensitive applications such as automotive wire & cable insulation and medical tubing. A decisive 2025 buying trigger is the “zero-phthalate” transition, with SBCs increasingly specified as PVC alternatives that deliver comparable softness while complying with tightened EU and US health regulations—an advantage highlighted by Dynasol. Additionally, near-95% compatibility with polyolefin recycling streams, validated by Kraton, positions SBCs as the default choice for ESG-aligned manufacturers, reinforcing their leadership in both volume and regulatory resilience.

Market Share by End-User Industry: Industrial Demand Drives Scale, Productivity, and Electrification Adoption

The industrial sector accounts for ~45% of total multiblock copolymer demand in 2025, reflecting a decisive shift from discretionary consumer uses toward infrastructure, heavy manufacturing, and electrification-linked applications. Within this segment, asphalt and roofing modification alone represents ~35.5% of SBC consumption, underpinned by large-scale road and urban infrastructure programs across Asia-Pacific—an anchor demand stream consistently cited by Kraton and Sinopec. Beyond volume, industrial OEMs are increasingly selecting multiblock copolymers for measurable productivity gains: Dow reports that its INFUSE™ olefin block copolymers enable ~40% faster injection-molding cycle times, a material advantage in high-throughput manufacturing environments. Durability is another decisive factor—BASF and Lubrizol highlight TPU-based multiblock systems delivering up to 3× higher abrasion resistance than conventional elastomers, directly reducing downtime in mining, oil & gas, and material-handling equipment. In parallel, automotive electrification is accelerating industrial uptake: Lubrizol’s 2025 EV-focused multiblock solutions for charging cables and robotic automation achieve ~20% weight reduction, aligning material selection with EV efficiency and automation requirements. Together, infrastructure scale, productivity economics, and electrification-driven redesign make industrial applications the most structurally entrenched demand pillar for multiblock copolymers.

Competitive Landscape: High-Performance Polymers, Renewable Sbcs, and Advanced Elastomer Technologies

The competitive landscape of the Multiblock Copolymers Market is defined by a blend of global specialty polymer leaders and diversified chemical producers investing heavily in renewable feedstocks, advanced microstructural control, and application-specific high-performance copolymer engineering. Market leadership is shifting toward companies with strong hydrogenation chemistry, metallocene control technologies, and integrated circular economy initiatives. The industry's evolution is centered on sustainability, high-functionality polymer design, and high-value application diversification across automotive, electronics, adhesives, coatings, biomedical, and sports performance sectors.

Kraton Corporation - Global Leader in Renewable Styrenic Block Copolymers

Kraton remains the dominant global supplier of SBS, SIS, SEBS, and SEPS multiblock copolymers, assisting the transition toward high-performance thermoplastic elastomers. The company’s expansion in June 2023 to produce SBCs with up to 100% ISCC PLUS-certified renewable content underscores its leadership in biobased TPE innovation. Its CirKular+™ line (launched April 2025) is positioned at the forefront of polymer circularity and asphalt upcycling. Kraton’s strong hydrogenation expertise enables SEBS/SEPS materials with enhanced weatherability and durability, supplying critical applications in automotive, healthcare, and engineered adhesives.

BASF SE - Integrated Specialist in EO/PO Multiblock Systems and Functional Additives

BASF provides a broad portfolio of multiblock copolymers including Poloxamers and specialized EO/PO systems used as surfactants, dispersants, and rheology modifiers. Its Lupasol and Sokalan technologies enable high-performance polymer additives for detergents, coatings, water treatment, and personal care. BASF’s sustainability strategy focuses on biodegradability metrics and product carbon footprint (PCF) reduction, ensuring compliance with OECD standards. Its massive integration capabilities allow it to deliver multiblock copolymers as components of full chemical solution ecosystems.

LG Chem - Advanced TPE-E Solutions For Automotive and Electronics

LG Chem delivers advanced multiblock copolymer-based materials, particularly through its KEYFLEX BT TPE-E lineup, designed for flexibility, toughness, and automotive-grade mechanical performance. The company leverages proprietary metallocene catalyst technology to precisely control polymer architecture, enabling superior elasticity and heat resistance. LG Chem’s portfolio extends into EV battery insulation materials, automotive interiors, and impact-resistant adhesives, supporting safety and lightweighting trends across next-generation electric mobility.

Arkema S.A. - Leader in Lightweight PEBA Performance Materials

Arkema specializes in PEBA (Polyether Block Amide) multiblock copolymers under its widely recognized Pebax® brand, known for exceptional lightness, flexibility, and energy return. These polymers cater to elite sportswear, medical tubing, and precision industrial applications. With its Pebax® Rnew® grades, Arkema is an early leader in bio-derived performance polymers sourced from castor oil. Its materials are also optimized for advanced manufacturing, including 3D printing and extrusion coating.

Covestro Ag - High-Durability Tpu Block Copolymer Innovator

Covestro commands a strong position with its thermoplastic polyurethane (TPU) block copolymers, delivering industry-leading abrasion resistance-up to 10× greater than standard TPEs. The company invests heavily in CO₂-based polymer feedstocks and chemical recycling technologies to achieve circularity in polyurethane systems. Covestro’s TPU materials are widely used in automotive parts, industrial equipment, medical devices, and athletic footwear, where durability and flexibility are mission-critical.

India has positioned itself as a strategic growth engine for the multiblock copolymers market by embedding advanced polymer science directly into its national bio-economy agenda. The rollout of the BioE3 (Biotechnology for Economy, Environment and Employment) policy has elevated bio-based multiblock copolymers from niche R&D materials to nationally prioritized industrial outputs. By explicitly targeting high-performance biopolymers and specialty copolymers, India is encouraging domestic scale-up of thermoplastic polyurethanes, styrenic block copolymers, and biodegradable multiblock systems that can replace fossil-derived elastomers in medical devices, packaging, and mobility applications. The DBT–BIRAC joint initiatives further reinforce this trajectory by funding biofoundries and biomanufacturing hubs capable of translating lab-scale block fidelity into commercial volumes. From a market perspective, India’s emphasis on LC³-compatible materials and net-zero-aligned polymer systems is creating long-term demand visibility for sustainable multiblock copolymers while reducing import dependence on specialty resins.

South Korea’s Automotive and Electronics-Centric Copolymer Pricing and Capacity Expansion

South Korea’s multiblock copolymers market is defined by precision manufacturing and tight integration with downstream automotive and electronics supply chains. The launch of a domestic polypropylene block copolymer price index has introduced unprecedented transparency for high-flow resins critical to lightweight EV components. This pricing benchmark is strategically important for OEMs and Tier-1 suppliers seeking predictable input costs as vehicle architectures shift toward polymer-intensive designs. Capacity expansions by leading producers are tightly aligned with EV battery demand, where multiblock copolymers function as binders, separators, and impact-modifying agents under high thermal and electrochemical stress. In parallel, South Korean manufacturers are accelerating low-VOC multiblock formulations to meet stringent indoor air quality norms for smart cabins and consumer electronics. This combination of price discovery, application-specific capacity, and regulatory alignment strengthens South Korea’s role as a regional hub for high-spec multiblock copolymers.

United States Re-shoring Strategy and Baroplastics Innovation Redefining Processing Economics

The United States multiblock copolymers market is undergoing a structural reset driven by trade policy and advanced materials research. Strategic tariff recalibrations have shifted procurement behavior toward domestically produced EO- and PO-based block copolymers, particularly for adhesives, oilfield chemicals, and specialty elastomers. This re-shoring momentum is complemented by rapid progress in baroplastics-pressure-processable multiblock copolymers that eliminate energy-intensive thermal processing. Such materials are attracting strong interest from aerospace and defense manufacturers seeking lower-carbon manufacturing routes without compromising mechanical performance. Regional polymer innovation clusters, especially in legacy rubber and plastics hubs, are also leveraging multiblock compatibilizers to improve the recyclability of mixed polyolefin waste streams. Collectively, these developments position the U.S. as a leader in processing innovation and circular-economy-enabled multiblock systems.

Germany’s Circular Economy Focus and High-Load Multiblock Specialization

Germany continues to anchor Europe’s multiblock copolymers market through deep R&D capabilities and circular economy integration. Material innovation is centered on sustainable copolymer polyols engineered for high-load automotive and furniture applications, where durability, low emissions, and process efficiency are non-negotiable. Industrial leaders such as BASF SE have advanced waste-reducing production routes for high-performance polyols, while Covestro AG has accelerated low-VOC multiblock launches aligned with EU indoor safety standards. Government-backed circular bioeconomy grants are further catalyzing the transition toward bio-derived feedstocks for polyurethane and elastomer systems. This policy–industry synchronization reinforces Germany’s leadership in premium, regulation-compliant multiblock copolymers rather than commodity-scale production.

China’s Infrastructure-Led Scale-Up of Styrenic Block Copolymers

China’s multiblock copolymers market is characterized by scale, infrastructure intensity, and policy-driven demand creation. Under the 14th Five-Year Plan, styrenic block copolymers-particularly SBS-are prioritized for asphalt modification to support expansive road, roofing, and smart city projects. The mandated shift toward prefabricated buildings has further amplified demand for flexible, weather-resistant multiblock copolymers used in sealants and structural adhesives. Capacity expansions by state-backed producers such as Sinopec in hydrogenated SBCs signal China’s intent to move up the value chain into medical tubing and specialty footwear applications. This dual focus on infrastructure scale and selective high-end substitution underpins China’s dominant volume position in the global market.

Japan’s Medical-Grade Precision and Advanced Biocompatible Multiblock Systems

Japan’s multiblock copolymers market is defined by uncompromising quality standards and leadership in medical-grade materials. Producers such as Mitsui Chemicals emphasize ultra-high purity copolymer polyols to serve global medical device manufacturers, where traceability and consistency are critical. At the innovation frontier, Japanese research institutions and specialty chemical firms are commercializing thermo-sensitive triblock copolymers for 3D bioprinting, enabling tissue engineering applications in cartilage and cardiac repair. The anticipated launch of thermally stable specialty copolymers by Honeywell for industrial sensors and AI hardware further reinforces Japan’s position as a premium market for technologically demanding multiblock applications rather than volume-driven growth.

2025 National Strategic Development Matrix: Multiblock Copolymers Market

2025 National Strategic Development Matrix: Multiblock Copolymers Market

|

Country

|

Primary Strategic Driver

|

2025 Key Milestone

|

Primary Application Focus

|

|

India

|

Bio-economy (BioE3 Policy)

|

National Biomanufacturing Hubs operationalized

|

Bio-based chemicals and biopolymers

|

|

South Korea

|

Automotive & electronics resins

|

Domestic PP block copolymer price index

|

EV components and high-flow resins

|

|

United States

|

Re-shoring and energy efficiency

|

Tariff-driven sourcing shift and baroplastics R&D

|

Baroplastics and oilfield chemicals

|

|

Germany

|

Circular economy leadership

|

High-load sustainable copolymer polyols

|

Automotive seating and low-VOC interiors

|

|

China

|

Infrastructure scale-up

|

SBS asphalt modification expansion

|

Paving, roofing, and prefab buildings

|

|

Japan

|

Medical precision and quality

|

Triblock copolymers for 3D bioprinting

|

Medical devices and tissue engineering

|

Multiblock Copolymers Market Report Scope

Multiblock Copolymers Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$331.9 Million

|

|

Market Size (2035)

|

$1116.7 Million

|

|

Market Growth Rate

|

12.9%

|

|

Segments

|

By Product Type (Styrenic Block Copolymers, Thermoplastic Polyurethanes, Polyamide-Based Multiblock Copolymers, Polyester-Based Multiblock Copolymers, Olefinic Multiblock Copolymers, EO/PO Block Copolymers), By Synthesis Methodology (RAFT, ATRP, NMP, Anionic/Cationic Polymerization), By Application (Automotive, Electronics, Healthcare & Medical, Consumer Goods, Industrial & Construction, Packaging), By End-User (Industrial, Commercial, Residential)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Kraton Corporation, Arkema, Evonik Industries AG, BASF SE, Dow Inc., LyondellBasell Industries N.V., SABIC, Covestro AG, DuPont de Nemours Inc., HMC Polymers, Sumitomo Chemical Co. Ltd., Solvay S.A., Eastman Chemical Company, Asahi Kasei Corporation, INEOS Group Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Multiblock Copolymers Market Segmentation

By Product Type

- Styrenic Block Copolymers (SBCs)

- Thermoplastic Polyurethanes (TPU)

- Polyamide-based Multiblock Copolymers

- Polyester-based Multiblock Copolymers

- Olefinic Multiblock Copolymers (OBCs)

- EO/PO Block Copolymers

By Synthesis Methodology

- Reversible Addition–Fragmentation Chain-Transfer (RAFT)

- Atom Transfer Radical Polymerization (ATRP)

- Nitroxide-Mediated Polymerization (NMP)

- Anionic/Cationic Polymerization

By Application

- Automotive

- Electronics

- Healthcare & Medical

- Consumer Goods

- Industrial & Construction

- Packaging

By End-User

- Industrial

- Commercial

- Residential

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Multiblock Copolymers Market

- Kraton Corporation

- Arkema

- Evonik Industries AG

- BASF SE

- Dow Inc.

- LyondellBasell Industries N.V.

- SABIC

- Covestro AG

- DuPont de Nemours, Inc.

- HMC Polymers

- Sumitomo Chemical Co., Ltd.

- Solvay S.A.

- Eastman Chemical Company

- Asahi Kasei Corporation

- INEOS Group Limited

*- List not Exhaustive