N-Methyl Pyrrolidone (NMP) Market 2025–2034: Battery-Grade Solvents, Regulatory Realignment, and Closed-Loop Recovery Systems

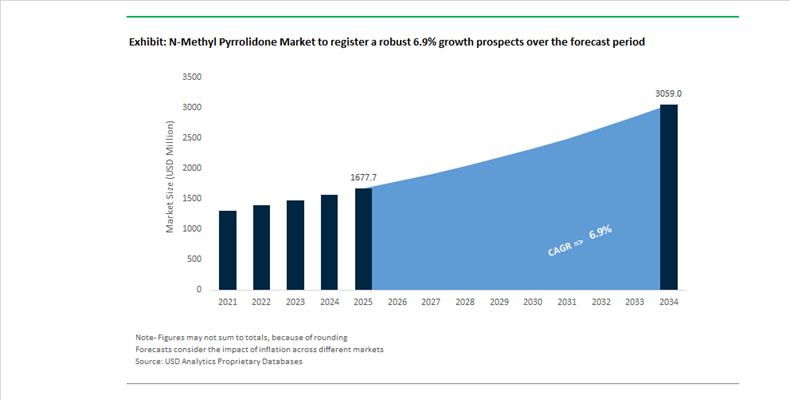

The N-Methyl Pyrrolidone (NMP) Market is projected to expand from $1,677.7 Million in 2025 to $3,058.5 Million by 2034, reflecting a CAGR of 6.9%. NMP remains a mission-critical polar aprotic solvent across lithium-ion battery cathode processing, electronics cleaning, petrochemical extraction, and specialty coatings. However, the market is undergoing structural realignment as regulatory scrutiny intensifies in North America and Europe while Asia-Pacific consolidates its dominance in electronic-grade supply. The result is a bifurcated landscape: shrinking industrial-grade applications in regulated markets and accelerating growth in ultra-high-purity battery solvent demand tied to gigafactory expansions.

In May 2025, the U.S. Environmental Protection Agency advanced its final risk management rule under TSCA, introducing a Workplace Chemical Protection Program (WCPP) for industrial users and setting a 45% concentration cap for consumer applications such as adhesives. The rule formalized prohibitions on NMP use in automotive care products, degreasers, fertilizers, and certain metal-cleaning operations where alternatives are deemed viable. These restrictions have triggered portfolio rationalization among Western producers. In early 2026, Dow Inc. intensified its “Transform to Outperform” restructuring, shifting focus toward high-margin electronic-grade NMP while phasing out lower-value industrial solvent lines.

Simultaneously, Asia-Pacific capacity continues to scale. Throughout 2025, China strengthened its position as the global leader in 99.9% purity electronic-grade NMP, integrating production near major battery manufacturers such as CATL and LG New Energy. This vertical alignment lowers logistics costs and secures solvent supply for high-nickel cathode chemistries. In February 2026, BASF SE announced expansion of its production footprint in Mangalore, India, reinforcing its intermediates and dispersion capabilities that rely on NMP-based solvent systems. The move aligns with India’s January 2025 launch of the National Critical Minerals Mission, which targets 50 GWh of domestic battery capacity under the Production-Linked Incentive scheme and emphasizes secure solvent supply chains.

Technological adaptation is redefining operational efficiency. Between 2025 and 2026, gigafactories across Europe and North America installed advanced solvent recovery units capable of reclaiming over 99.5% of NMP from electrode coating lines. These closed-loop purification systems reduce virgin solvent consumption, stabilize operating costs amid energy volatility, and ensure compliance with occupational exposure thresholds. High-purity NMP suppliers have also entered strategic partnerships with battery material producers to tailor solvent rheology and viscosity characteristics for solid-state and advanced cathode slurry systems.

Substitution pressure is intensifying. In April 2025, technical data for JEFFSOL® MEOX (3-Methyl-2-oxazolidinone) positioned it as a safer, high-boiling alternative lacking NMP’s reprotoxic classification. Parallel trials of bio-based γ-Valerolactone (GVL) in agrochemical and membrane applications highlight emerging renewable solvent pathways. Meanwhile, 2026 ECHA microplastic reporting mandates indirectly affect NMP demand because it remains integral to polymer and resin processing that must now undergo lifecycle audits.

The NMP market through 2034 will be defined by electronic-grade solvent premiums, recovery-system integration, regulatory displacement in consumer applications, and continued Asian capacity consolidation. Demand growth is increasingly tethered to battery manufacturing scale, advanced electronics fabrication, and solvent circularity engineering rather than traditional industrial cleaning segments.

N-Methyl-2-Pyrrolidone (NMP) Market Trends and Opportunities

Trend: Accelerated Regulatory Phase-Out and Semiconductor Process Reformulation

The N-Methyl-2-Pyrrolidone market is undergoing a structural reset as regulatory authorities tighten controls on reproductive and occupational exposure risks. Following the EU REACH Annex XVII restrictions, the United States has moved decisively under TSCA Section 6, reframing NMP from a manageable industrial solvent to a regulated high-risk substance. This shift is particularly disruptive for semiconductor fabrication, where NMP has historically been the solvent of choice for photoresist stripping, wafer cleaning, and advanced node defect remediation.

In June 2024, the U.S. EPA proposed a federal rule that would prohibit NMP use in automotive care products, cleaning and degreasing, and fertilizer applications within one year of finalization. For semiconductors and batteries, the rule does not immediately ban NMP but mandates the implementation of a Workplace Chemical Protection Program with sharply reduced exposure thresholds. Compliance requires enclosed tools, automated handling, real-time vapor monitoring, and upgraded ventilation systems. For many fabs, the cumulative compliance cost is exceeding the economics of continued NMP use, accelerating reformulation decisions at the process level.

The consumer and retail channel has already collapsed. Large home-improvement and coatings retailers have fully withdrawn NMP-based paint strippers and cleaners, effectively eliminating discretionary demand. This has reoriented the market toward highly controlled industrial environments where NMP survives only if embedded in closed systems. In parallel, semiconductor manufacturers are piloting aqueous-based and nano-chemistry strippers that replace volatile organic solvents with high-purity, lower-toxicity chemistries. By 2025, industry benchmarks indicate that advanced aqueous systems can meet critical linewidth and residue-removal requirements at mature nodes, signaling a long-term structural decline in open-use NMP demand even in high-tech manufacturing.

Trend: Strategic Capacity Rationalization and Eastward Production Rebalancing

On the supply side, NMP production is being reshaped by energy economics, litigation risk, and proximity to downstream demand. Europe has become the epicenter of capacity contraction. Persistently high natural gas prices, tightening environmental permits, and exposure to “forever chemical” class-action risks have undermined the viability of solvent production in the region. By December 2025, industry leaders warned that between 2022 and 2027 nearly 90 chemical plants across Europe would close or idle, removing roughly 25 million tonnes of capacity from the market. NMP, as an energy-intensive and compliance-heavy solvent, is disproportionately affected by this de-industrialization.

Capital is moving eastward. Integrated chemical producers are reallocating investment toward Asia-Pacific, where energy costs are lower and demand is anchored by lithium-ion battery manufacturing. In early 2025, BASF commissioned a new commercial facility at its Caojing Verbund site in Shanghai, reinforcing a broader strategy to colocate solvent production with cathode, binder, and electrolyte manufacturing. This geographic realignment reflects the reality that Asia now dominates EV battery output and therefore captive NMP consumption.

At the same time, excess Chinese capacity is being exported aggressively, placing downward pressure on merchant prices in Europe and North America. In response, the United States introduced targeted tariffs in early 2025 on NMP and related battery precursors to protect domestic supply chains and support localization under the Inflation Reduction Act. The result is a bifurcated market: regulated, high-cost closed-loop NMP use in the West versus scale-driven, price-competitive production in Asia tied directly to battery ecosystems.

Opportunity: Closed-Loop Recovery Systems in Battery Gigafactories

Despite regulatory headwinds, NMP remains indispensable in lithium-ion battery manufacturing, particularly for dissolving PVDF binders used in cathode electrode slurries. As battery output scales, the economic and environmental burden of solvent losses has turned recovery from a best practice into a non-negotiable operational requirement. Closed-loop NMP recovery and purification systems are now central to gigafactory design.

State-of-the-art recovery units deployed in 2025 are achieving solvent recovery rates approaching 99%. For a typical gigafactory, this level of circularity can reduce cathode production costs by up to 30% while simultaneously cutting solvent-related carbon emissions by nearly the same margin. These systems also mitigate regulatory exposure by minimizing operator contact and reducing fugitive emissions, aligning with the strict expectations of the EU Battery Regulation.

With more than 200 gigafactories planned or operating globally, investment in solvent circularity has become a scale opportunity. European players such as Northvolt and BASF are integrating dedicated NMP recycling modules directly into cathode lines to meet zero-waste manufacturing targets. In the United States, IRA incentives and tariff protections are accelerating localized “hub-and-spoke” purification models, enabling spent NMP to be upgraded back to battery-grade purity without reliance on imported virgin solvent. This transforms NMP from a consumable cost into a managed asset within battery value chains.

Opportunity: High-Performance NMP-Alternative Solvent Blends

The most strategically attractive growth avenue lies not in defending legacy NMP demand, but in replacing it. Regulatory restrictions have created a solvency gap across coatings, polyurethane processing, electronics cleaning, and refinery maintenance. Developing drop-in alternatives that replicate NMP’s exceptional solvency and thermal stability without its reproductive toxicity has become a central innovation priority.

Next-generation dipolar aprotic solvents are gaining traction as near-functional substitutes. Products such as safer NxG-class solvents are being adopted in photoresist stripping, cookware coatings, and industrial cleaning with minimal reformulation, offering immediate regulatory relief to users. At the same time, bio-based and ester-derived solvent blends are moving from niche to mainstream. In late 2025, expanded portfolios of dimethyl ester-based formulations entered polyurethane cleaning and line-flushing applications, delivering low volatility, strong resin-softening performance, and Prop 65-free safety profiles.

Field data from 2025 industrial trials demonstrate that specialty ester blends can achieve performance parity with NMP in soaking and heavy-duty maintenance processes, albeit with longer dwell times. For many industrial users, this trade-off is acceptable when balanced against compliance certainty and workforce safety. As a result, the long-term growth narrative of the NMP market is increasingly defined not by volume expansion, but by technology substitution, circular recovery, and the monetization of safer, regulation-aligned solvent systems.

N-Methyl Pyrrolidone Market Share and Segmentation Insights

Industrial Grade N-Methyl Pyrrolidone Dominates Market Due to High-Volume Industrial and Battery Manufacturing Demand

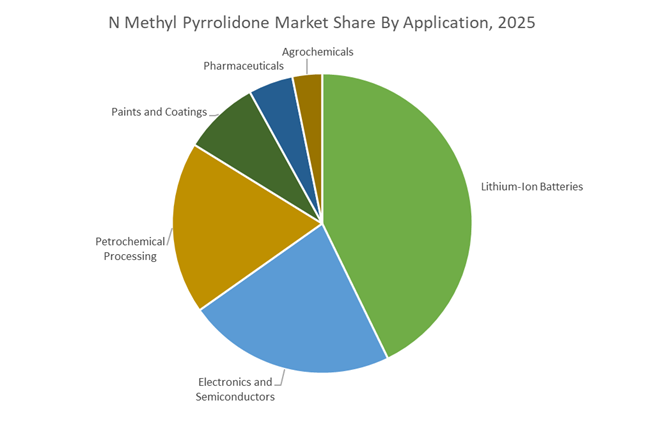

Industrial grade N-methyl pyrrolidone (NMP) accounted for 58.60% of the N-Methyl Pyrrolidone Market share in 2025, making it the most widely used grade across large-scale industrial solvent applications. Industrial grade NMP typically contains purity levels above 99.5%, which is sufficient for demanding applications such as lithium-ion battery electrode manufacturing, petrochemical extraction processes, industrial cleaning formulations, and coatings production. The solvent is valued for its excellent solvency power, high boiling point, and strong compatibility with polar polymers, enabling efficient dissolution of resins, binders, and chemical intermediates in complex manufacturing processes. Because these industries operate at high production volumes, industrial grade NMP offers the most cost-effective balance between purity and price. In 2025, increasing demand from battery manufacturing has altered product specifications across the market. Lithium-ion battery producers are now specifying higher purity solvent grades approaching electronic-grade standards, creating a premium segment within the industrial grade category as battery manufacturers seek improved process consistency and electrode quality.

Lithium-Ion Battery Manufacturing Drives the Largest Demand for N-Methyl Pyrrolidone

Lithium-ion batteries accounted for 42.80% of the N-Methyl Pyrrolidone Market share in 2025, making battery manufacturing the largest application segment for this high-performance solvent. NMP plays a critical role in the production of lithium-ion battery electrodes, where it is used to dissolve polyvinylidene fluoride (PVDF) binders during the slurry preparation process for cathode and anode coating. The solvent enables uniform dispersion of active materials and conductive additives, ensuring consistent electrode structure and battery performance. The rapid expansion of electric vehicle (EV) battery production, energy storage systems, and consumer electronics batteries has significantly increased demand for high-purity NMP used in electrode fabrication lines. In 2025, battery manufacturers have intensified efforts to improve solvent efficiency due to rising production volumes and solvent price volatility. Large-scale gigafactories increasingly implement closed-loop NMP recovery and recycling systems, capturing solvent vapors from electrode coating processes and purifying them for reuse. These systems can recover 80–90% of the NMP used in battery manufacturing, reducing raw solvent consumption while maintaining the purity levels required for high-performance lithium-ion battery production.

N-Methyl Pyrrolidone Market Competitive Landscape

The N-Methyl-2-Pyrrolidone (NMP) market in 2026 is driven by electronic-grade purity (≥99.9%), lithium-ion battery demand, and closed-loop solvent recovery (>98%). Competitive advantage centers on ultra-low moisture control, circular economy models, and regionalized supply chains supporting EV battery and semiconductor manufacturing.

BASF advances low-carbon electronic-grade NMP with verified reduced product carbon footprint solutions

BASF SE is reinforcing its leadership in the NMP market through sustainable, high-purity solvent innovation tailored for lithium-ion batteries and electronics. Its rPCF NMP, launched in 2026, delivers at least a 10% lower product carbon footprint, aligning with Scope 3 emissions reduction goals for automotive and semiconductor OEMs. Produced at the Ludwigshafen Verbund site, the solvent benefits from integrated feedstock efficiency and low-emission utilities. BASF ensures compliance with ISO 14067 and TfS standards, providing verified ESG credentials to global customers. With approximately €60 billion in 2025 sales, the company is prioritizing high-margin intermediates and green solvents. Its focus on carbon-efficient production and regulatory compliance strengthens its position in electronic-grade NMP.

LyondellBasell optimizes asset utilization and feedstock integration to sustain NMP competitiveness amid market volatility

LyondellBasell Industries is maintaining its NMP market presence through operational efficiency and disciplined capital management. Its expanded $1.3 billion Cash Improvement Plan is focused on optimizing asset utilization across its Intermediates & Derivatives segment. The Channelview expansion enhances upstream integration, securing propylene feedstock and improving downstream solvent economics. LYB is targeting an 80% operating rate in 2026, balancing supply-demand dynamics amid global overcapacity. Despite 2025 financial pressures, the company retained strong liquidity with $3.4 billion in cash reserves. Its “value over volume” strategy ensures profitability while maintaining a stable supply of industrial and specialty solvents.

Mitsubishi Chemical aligns high-purity NMP with semiconductor recovery and circular economy initiatives

Mitsubishi Chemical Group is repositioning toward specialty materials, with high-purity NMP playing a critical role in semiconductor and electronics manufacturing. Its Medium-Term Management Plan 2029 targets ¥460 billion in operating income, driven by growth in EV mobility and wafer processing chemicals. The company’s withdrawal from low-margin carbon materials enables reinvestment into high-value solvent technologies. Strategic partnerships focused on chemical recycling and circular economy infrastructure reinforce its sustainability agenda. Investments in carbon fiber and advanced films further complement NMP demand in lightweight automotive applications. Mitsubishi’s integration of specialty chemicals with advanced materials strengthens its position in high-growth electronics markets.

Ashland focuses on high-purity NMP for pharmaceutical and battery applications with disciplined portfolio optimization

Ashland Inc. is strengthening its position in the NMP market by focusing on specialty applications in pharmaceuticals and lithium-ion battery manufacturing. The company reported $58 million adjusted EBITDA in early 2026, maintaining margins through cost optimization and strategic divestitures. Its NMP portfolio supports critical applications such as parenteral drug formulations and cathode slurry preparation for domestic US battery plants. Stabilization of operations at its Calvert City facility ensures reliable supply for high-purity solvent demand. With $125 million in operating cash flow, Ashland is investing in process improvements and supply chain resilience. Its targeted focus on high-value applications enhances competitiveness in specialty solvent markets.

Eastman drives circular NMP value through molecular recycling and high-margin specialty chemical strategy

Eastman Chemical Company is differentiating itself in the NMP market through its circular economy and molecular recycling platforms. Its Kingsport methanolysis facility significantly increased recycled content output, supporting a targeted $75–$100 million EBITDA contribution by 2026. The company is implementing cost reduction initiatives of up to $150 million to protect margins in its Chemical Intermediates segment. Eastman’s strategy emphasizes defending price and prioritizing high-value specialty markets over commoditized volume segments. Plans for a second methanolysis facility in Texas will expand its recycled feedstock capabilities. Its focus on sustainability, recycling integration, and premium product positioning strengthens its long-term market competitiveness.

China: Battery-Driven Scale, Centralized Solvent Parks, and Export Leadership

China continues to define the global operating center of the N-Methyl Pyrrolidone market, anchored by its overwhelming dominance in lithium-ion battery manufacturing. With more than 75% of global Li-ion cell capacity located domestically in 2025, NMP demand is structurally embedded in the coating of Lithium Iron Phosphate cathodes. This demand concentration has driven the formation of large, vertically integrated NMP production clusters aligned with battery supply chains. A key milestone was achieved when Ganzhou Zhongneng Industrial Co. Ltd. commissioned an additional 100,000-ton capacity expansion across late 2024 and 2025, materially strengthening solvent availability for domestic EV battery producers.

Industrial policy is reinforcing scale with environmental discipline. Under the 2026 Green Manufacturing roadmap issued by the Ministry of Industry and Information Technology, provincial governments in Shandong and Jiangsu are incentivizing the migration of NMP assets into centralized chemical parks. These parks deploy shared high-efficiency distillation and recovery units, reducing per-ton emissions while improving solvent reuse economics. Technologically, Chinese producers achieved stable 99.9% electronic-grade NMP at scale in 2025, supporting 12-inch wafer cleaning and photoresist stripping in the domestic semiconductor industry. Export momentum remains strong, with May 2025 customs data indicating more than 50 outbound shipments per month, primarily serving Vietnam and India.

United States: Regulatory Convergence, Battery Belt Recovery Systems, and High-Purity Pivot

The United States NMP market is undergoing a structural recalibration driven by regulation, reshoring of battery manufacturing, and a strategic pivot toward high-purity applications. In 2025, BASF expanded specialty pyrrolidone production at its Geismar, Louisiana site, reinforcing North American supply security for inks, automotive coatings, and agricultural formulations through 2026. At the same time, accelerated rulemaking under the Toxic Substances Control Act is tightening exposure standards. By mid-2026, finalized Workplace Chemical Protection Programs are expected to impose lower Existing Chemical Exposure Limits, compelling industrial users to invest in enclosed handling and recovery infrastructure.

Battery manufacturing is reshaping solvent flows. Gigafactory investments across Georgia, Tennessee, and Kentucky are incorporating on-site NMP recovery systems designed to achieve solvent recovery rates approaching 90%, materially lowering operating costs for cathode slurry preparation. Strategic repositioning is also visible among specialty players. Ashland has focused its 2025–2026 portfolio on pharmaceutical-grade NMP and derivatives for biopharma applications, aligning with rapid growth in advanced drug delivery and formulation. Concurrently, import tariff adjustments in 2025 are encouraging closed-loop domestic recycling, reducing dependence on imported solvent volumes.

Germany: REACH Enforcement, Ultra-Low Emissions Engineering, and Battery Circularity

Germany’s NMP market is shaped by regulatory precision, engineering leadership, and circular economy mandates tied to batteries and semiconductors. As of September 30, 2025, updated ECHA registration requirements under REACH Annex XVII introduced stricter transparency obligations for NMP, which is registered in the 10,000–100,000 tonnes per annum band. These requirements are accelerating investments in solvent containment and recovery across professional and industrial uses.

German engineering firms such as Brofind and DEC Group are deploying advanced multi-stage distillation and rotor concentrator systems capable of reducing atmospheric emissions below 2 mg/Nm³, meeting the EU’s most stringent DNEL thresholds. Circularity is becoming a binding requirement rather than a strategic option. Under the EU Battery Regulation taking effect through 2026, recycling one ton of NMP is documented to save up to six tons of CO₂ compared with virgin production. Demand for ultra-pure NMP is also rising in the Silicon Saxony semiconductor cluster, supported by federal subsidies aimed at strengthening domestic microelectronics manufacturing.

India: Import Exposure, Policy-Led Localization, and Academic Process Innovation

India remains the world’s largest NMP importer, with more than 750 inbound shipments annually as of May 2025, underscoring acute supply dependence. This exposure is catalyzing both industrial investment and policy intervention. In May 2025, Gujarat Alkalies and Chemicals Limited approved an ₹81 crore investment at Dahej to expand downstream feedstock units, creating foundational infrastructure to support domestic NMP synthesis through 2026. NMP has been identified as a priority intermediate for India’s agrochemical sector, which continues to expand steadily alongside broader ambitions to grow the national chemical industry from $220 billion toward $300 billion by 2030.

At the innovation layer, academic institutions are contributing process efficiency gains. Researchers at IIT Guwahati patented membrane-based purification techniques in 2025 that materially reduce energy intensity for NMP recovery, particularly suited to small and mid-scale pharmaceutical formulators. These advances complement emerging policy discussions around production-linked incentives aimed at accelerating local solvent manufacturing and reducing structural import reliance.

South Korea: Contracted Stability, Closed-Loop Battery Systems, and Pharma-Grade Demand

South Korea’s NMP market is increasingly characterized by predictability and circularity rather than spot procurement. By 2026, major battery manufacturers have shifted toward long-term volume locking, with confirmed dedicated procurement of 80 tons for H1 2026 by a leading domestic battery client to manage currency volatility and cost visibility. This contractual stability supports upstream planning across the solvent value chain.

At the operational level, Samsung SDI and SK On finalized the rollout of integrated condensation-adsorption-distillation systems in 2025. These systems establish near-closed-loop NMP supply chains, lowering raw material costs by up to 20%. Beyond batteries, pharmaceutical-grade NMP demand rose in 2025 alongside the expansion of domestic biosimilar production, where high-purity solvent is essential for solubilizing hydrophobic active ingredients.

Comparative Snapshot: Country Positioning in the N-Methyl Pyrrolidone Market

N-Methyl Pyrrolidone Market County Level Snapshot

|

Country

|

Primary Demand Engine

|

Strategic Focus

|

Structural Impact

|

|

China

|

Li-ion batteries and electronics

|

Scale, centralized parks, exports

|

Cost leadership and global supply dominance

|

|

United States

|

Batteries, biopharma, coatings

|

Regulation-driven recovery, purity shift

|

Closed-loop systems and specialty positioning

|

|

Germany

|

Batteries, semiconductors

|

REACH compliance, solvent recycling

|

Ultra-low emissions and circular leadership

|

|

India

|

Agrochemicals, pharma

|

Import substitution, academic innovation

|

Localization pathway with policy support

|

|

South Korea

|

EV batteries, biosimilars

|

Long-term contracts, recovery systems

|

Cost stability and circular supply chains

|

N-Methyl Pyrrolidone Market Report Scope

N-Methyl Pyrrolidone Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1677.7 Million

|

|

Market Size (2034)

|

$3058.5 Million

|

|

Market Growth Rate

|

6.9%

|

|

Segments

|

By Grade (Electronic Grade, Pharmaceutical Grade, Industrial Grade), By Application (Electronics and Semiconductors, Lithium-Ion Batteries, Pharmaceuticals, Agrochemicals, Paints and Coatings, Petrochemical Processing), By Recovery and Service Model (Virgin Solvent Supply, Solvent Recycling Services, On-Site Recovery Systems), By End-Use Industry (Automotive, Consumer Electronics, Energy Storage, Chemical and Petrochemical, Biopharma and Healthcare)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF, Ashland, Dow, Eastman Chemical, Mitsubishi Chemical Group, SABIC, Huntsman, LyondellBasell Industries, Nouryon, Balaji Amines, Gujarat Alkalies and Chemicals, Zhejiang Wansheng, Ganzhou Zhongneng Industrial, Hebei Chengxin, Shin-Etsu Chemical

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

N-Methyl Pyrrolidone Market Segmentation

By Grade

- Electronic Grade

- Pharmaceutical Grade

- Industrial Grade

By Application

- Electronics and Semiconductors

- Lithium-Ion Batteries

- Pharmaceuticals

- Agrochemicals

- Paints and Coatings

- Petrochemical Processing

By Recovery and Service Model

- Virgin Solvent Supply

- Solvent Recycling Services

- On-Site Recovery Systems

By End-Use Industry

- Automotive

- Consumer Electronics

- Energy Storage

- Chemical and Petrochemical

- Biopharma and Healthcare

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the N-Methyl Pyrrolidone Market

- BASF

- Ashland

- Dow

- Eastman Chemical

- Mitsubishi Chemical Group

- SABIC

- Huntsman

- LyondellBasell Industries

- Nouryon

- Balaji Amines

- Gujarat Alkalies and Chemicals

- Zhejiang Wansheng

- Ganzhou Zhongneng Industrial

- Hebei Chengxin

- Shin-Etsu Chemical

*- List not Exhaustive