Non-Stick Coatings Market Size, PFAS-Free Technologies, and High-Performance Surface Solutions Outlook

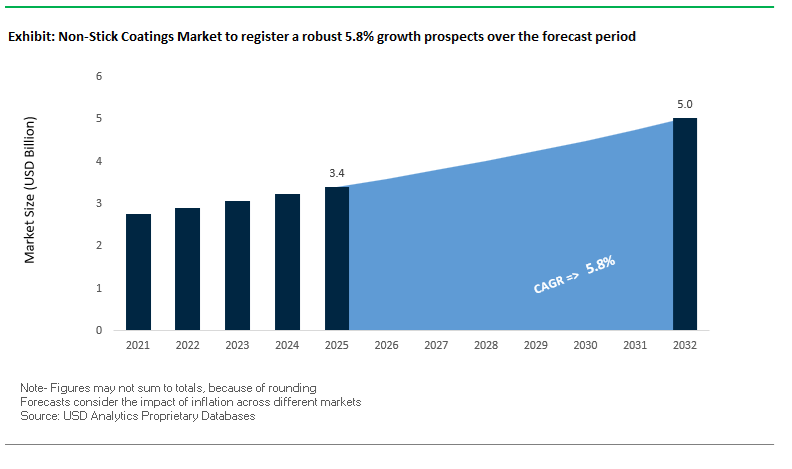

The global non-stick coatings market was valued at $3.4 billion in 2025 and is projected to reach $5 billion by 2032, expanding at a CAGR of 5.8%. Market growth is driven by increasing demand for non-stick coatings, fluoropolymer coatings, ceramic coatings, PTFE-free coatings, and low-friction surface coatings across cookware, food processing equipment, industrial machinery, automotive components, and medical devices. These coatings are critical for delivering easy-release performance, reduced friction, chemical resistance, and enhanced durability in both consumer and industrial applications.

A key growth driver is the global transition toward PFAS-free and environmentally compliant coating systems, as regulatory pressure intensifies around the use of fluorinated chemicals such as PTFE and PFOA. This shift is accelerating innovation in ceramic-based coatings, sol-gel technologies, and hybrid non-stick systems that offer comparable or improved performance without environmental risks. Additionally, the growing demand for premium cookware, induction-compatible surfaces, and high-performance industrial coatings is expanding the application scope of non-stick technologies.

The market is also benefiting from advancements in surface chemistry, nano-coatings, and high-temperature resistant materials, which enhance scratch resistance, thermal stability, and lifecycle durability. Rapid urbanization, evolving consumer lifestyles, and increased demand for convenience-oriented kitchen products are further driving adoption. Regionally, Asia-Pacific dominates due to large-scale cookware manufacturing, while Europe leads in regulatory-driven innovation and PFAS-free product adoption.

Market Analysis: PFAS-Free Transition, Ceramic Coating Innovation, and Strategic Consolidation Driving Market Evolution

The non-stick coatings industry is undergoing a major transformation driven by regulatory shifts, sustainability initiatives, and technological innovation. In February 2026, AkzoNobel announced the opening of a dedicated PFAS-free Innovation Center in Germany, in collaboration with leading appliance manufacturers, focusing on the development of next-generation induction-compatible non-stick coatings. This initiative reflects the industry’s pivot toward environmentally compliant, high-performance coating systems for premium cookware brands.

Strategic consolidation is reshaping the competitive landscape. The February 2026 merger between AkzoNobel and Axalta creates a powerful R&D ecosystem, combining expertise in decorative and industrial coatings to accelerate innovation in non-stick technologies, particularly targeting the rapidly growing Asian cookware market. Similarly, Kansai Helios’ May 2024 acquisition of Weilburger Coatings, owner of the GREBLON® brand, significantly strengthens its global footprint in both consumer cookware and industrial non-stick applications.

Sustainability-driven innovation is becoming a central focus across the value chain. BYK Additives confirmed in December 2025 the complete elimination of PFAS from its additive portfolio, ensuring that critical components such as waxes and surface modifiers meet evolving regulatory requirements. This aligns with broader industry shifts, including 3M’s commitment to exit PFAS manufacturing by the end of 2025, which is driving accelerated development of alternative chemistries.

Product innovation is advancing rapidly toward PFAS-free and high-durability solutions. PPG Industries’ March 2024 showcase of sol-gel and PTFE-free coatings demonstrates the ability to achieve extreme durability and long release life without relying on traditional fluoropolymers. Additionally, Weilburger’s expansion of its Greblon Ceramic production highlights the surge in demand for ceramic-based non-stick coatings, particularly in Europe where PFAS-free labeling is becoming a key purchasing criterion.

Regional expansion and supply chain localization are also shaping market dynamics. The Chemours Company’s January 2026 strategic expansion in India aims to strengthen the supply of high-performance fluoropolymers, ensuring continuity for industrial applications while transitioning toward more responsible manufacturing practices, as outlined in its August 2025 sustainability report.

Industrial applications are also driving innovation. Sherwin-Williams’ November 2025 facility expansion includes dedicated production lines for water-based, low-VOC non-stick coatings targeting food processing and commercial bakeware industries, where durability and compliance with food safety standards are critical.

Market Trend: Waterborne PFAS-Free Ceramic Non-Stick Coatings Transforming Cookware Safety, Durability, and VOC Compliance

The non-stick coatings industry is undergoing a structural transformation as cookware manufacturers transition from solvent-borne PTFE coatings to waterborne ceramic sol-gel coatings. This shift is being accelerated by the European Chemicals Agency PFAS restriction framework, which targets the phase-out of over 10,000 fluorinated substances across consumer and industrial applications. As a result, PFAS-free non-stick coatings are rapidly becoming the standard specification for global cookware brands.

Waterborne ceramic coatings deliver a substantial improvement in thermal stability and safety. These nano-ceramic systems maintain structural integrity at temperatures exceeding 450°C, whereas traditional PTFE coatings begin to degrade at approximately 260°C, releasing fumes associated with polymer fume fever. This high-temperature resilience is a critical differentiator in both consumer cookware and professional kitchen environments, where sustained heating cycles are common.

Mechanical performance is also significantly enhanced. Ceramic sol-gel coatings exhibit a pencil hardness of 9H, compared to the 2H to 3H hardness typical of fluoropolymer-based coatings. This higher hardness profile improves resistance to abrasive wear, extending product lifespan and maintaining non-stick performance under repeated usage. From an environmental perspective, the transition to waterborne coating systems enables up to 80% reduction in VOC emissions compared to solvent-based PTFE lines, supporting compliance with the EU Industrial Emissions Directive and broader sustainability targets. These combined benefits are accelerating the global adoption of ceramic non-stick coatings across premium and mid-range cookware segments.

Market Trend: Diamond-Like Carbon Non-Stick Coatings Enhancing Wear Resistance and Process Efficiency in Food Processing Equipment

Industrial food processing is emerging as a high-growth segment for advanced non-stick coatings, particularly through the adoption of Diamond-Like Carbon coatings. These coatings are replacing traditional chrome plating and electroless nickel systems in applications such as extrusion machinery, conveyor systems, and baking molds, where durability and clean release performance are critical.

DLC coatings provide ultra-low friction characteristics, with coefficients of friction ranging from 0.05 to 0.1. This low-friction surface significantly improves release efficiency in food processing operations. Industrial baking trials show that DLC-coated molds reduce the need for additional release agents by approximately 25%, lowering operational costs and minimizing contamination risks. Wear resistance is another key advantage. In high-speed extrusion environments, DLC coatings demonstrate a 70% reduction in abrasive wear over extended operating periods, enabling longer service life for critical components exposed to abrasive food materials such as grains and starches.

Thermal performance is also advancing with new material innovations. While conventional hydrogenated DLC coatings remain stable up to 350°C, silicon-doped DLC variants extend this threshold to 500°C to 550°C. This enhanced thermal stability supports high-temperature sterilization and baking processes without degradation of coating performance. These attributes position DLC non-stick coatings as a high-performance solution for industrial-scale food manufacturing systems requiring durability, efficiency, and compliance with food safety standards.

Market Opportunity: FDA PFAS Regulatory Actions Creating High-Growth Demand for Ceramic and Bio-Based Non-Stick Coatings

The regulatory environment in the United States is creating a major opportunity for PFAS-free non-stick coatings following the FDA’s 2025 notice and subsequent 2026 updates on food contact substances. The agency’s decision to invalidate 35 PFAS-related food contact notifications has effectively removed a large portion of legacy fluoropolymer-based coatings from regulatory acceptance, triggering a rapid industry-wide reformulation cycle.

Manufacturers are now required to provide validated Total Organic Fluorine testing data for any new food-contact coating, significantly increasing compliance complexity. This requirement has driven a 45% increase in research and development investment toward alternative chemistries, including ceramic, mineral-based, and bio-derived non-stick coatings. Companies with validated PFAS-free technologies are gaining accelerated market entry, as regulatory approval becomes a key barrier to adoption.

In parallel, the EPA’s TSCA Section 8(a)(7) reporting requirement, effective April 2026, mandates disclosure of PFAS usage across manufacturing operations. This is incentivizing companies to transition toward “report-exempt” coating technologies such as ceramic systems to reduce regulatory burden and long-term liability risks. These combined regulatory pressures are creating a strong demand pipeline for advanced non-stick coatings that deliver both performance and compliance in food-contact applications.

Market Opportunity: China GB 4806.7-2025 Standard Driving Large-Scale Replacement of PFAS-Based Non-Stick Coatings

China’s updated GB 4806.7-2025 food contact material standard is creating a large-scale transformation in the non-stick coatings market by introducing strict migration limits and enhanced testing requirements. The regulation establishes a total migration limit of less than 10 mg/dm² for plastic-based coatings, significantly tightening the performance criteria for food-contact safety.

This requirement is effectively limiting the use of traditional PFAS-based coatings, which often struggle to meet low migration thresholds under high-temperature conditions. As a result, manufacturers are shifting toward high-purity polymer systems such as polyethersulfone and polyphenylene sulfide blends, as well as ceramic hybrid coatings that exhibit near-zero migration characteristics. These materials are better suited to meet both thermal and chemical stability requirements under the new regulatory framework.

The enforcement of associated testing standards, including GB 31604.30, has further increased the rigor of compliance, establishing a new benchmark for analytical precision in migration testing. Non-compliant coatings face immediate exclusion from China’s domestic appliance market, which exceeds $150 billion in value. This regulatory shift is driving a large-scale replacement cycle across cookware and food-contact applications, creating substantial opportunities for suppliers offering compliant, high-performance non-stick coating technologies tailored to the Chinese market.

Non-Stick Coating Systems Market Share and Segmentation Insights

Two-Layer Systems Capture 48.3% Share Driven by Balanced Durability, Adhesion, and Release Performance

The non-stick coatings market by number of layers is led by two-layer coating systems, accounting for 48.3% of the global market share in 2025, due to their ideal balance between performance, durability, and cost efficiency. These systems typically consist of a primer layer and a topcoat, where the primer ensures strong adhesion to metal substrates, and the topcoat delivers superior non-stick, low-friction surface properties. Widely used across cookware (frying pans, bakeware), industrial molds, and food processing equipment, two-layer systems provide excellent scratch resistance, heat stability, and release characteristics at a competitive price point. Their compatibility with PTFE, ceramic, and advanced fluoropolymer coatings further enhances their versatility. As demand grows for PFOA-free, high-performance non-stick coatings, two-layer systems continue to dominate as the industry standard.

Direct Sales Hold 45.8% Share Driven by Industrial Scale Demand and Technical Collaboration

In the non-stick coatings market by distribution channel, direct sales dominate with a 45.8% market share in 2025, reflecting the need for customized formulations and close technical collaboration with end-users. Large cookware manufacturers such as SEB, Meyer, and Newell require proprietary coating solutions with precise specifications for release performance, scratch resistance, and compliance with PTFE/PFOA-free standards, making direct supplier relationships essential. Additionally, industrial sectors—including food processing, bakeware manufacturing, and heat press applications—purchase non-stick coatings in bulk volumes, requiring ongoing technical support for application processes, curing parameters, and performance optimization. Direct sales channels provide this level of customization and service, which distributors cannot match. This strong alignment with OEM requirements and industrial-scale demand firmly establishes direct sales as the leading channel in the global non-stick coatings market.

Competitive Landscape of the Non-Stick Coatings Market

Chemours Dominates Fluoropolymer Non-Stick Coatings with Teflon™ Brand Leadership

The Chemours Company continues to set the benchmark in the fluoropolymer non-stick coatings market, leveraging the global recognition of its Teflon™ brand. In 2026, the company commissioned a $35 million PTFE dispersion facility in Texas to meet growing demand for industrial-grade and food-contact non-stick coatings. Its Teflon™ EcoElite platform leads sustainability innovation, offering 60% renewably sourced materials and extending durability with a 7:1 performance ratio over ceramic alternatives. Despite implementing a 6% price increase to counter raw material inflation, Chemours maintains strong market dominance backed by 85% brand awareness. Its integration into aerospace and electronics, including NASA missions, highlights its leadership in high-performance coating applications.

PPG Strengthens Market Leadership with PFAS-Free Ceramic and Advanced PTFE Coatings

PPG Industries, through its Whitford portfolio, is a major force in the global non-stick coatings industry, focusing on PFAS-free innovation and commercial cookware solutions. The launch of PPG Fusion Pro in 2026 marked a significant advancement in ceramic non-stick coatings, delivering over 50,000 abrasion cycles—well above industry standards. By integrating Whitford brands like Eclipse® and Quantanium® into its automated systems, PPG enables manufacturers to reduce coating waste by 15%. Its Eclipse® series remains the gold standard for heavy-duty commercial kitchen applications, achieving up to 60,000 release cycles. With operations in over 70 countries, PPG leads the gourmet and commercial segment, which holds more than 61.6% market share.

AkzoNobel Expands Industrial Non-Stick Coating Capabilities Through Strategic Merger

AkzoNobel N.V. is strengthening its position in the industrial non-stick coatings market by focusing on sol-gel technology and clean cooking solutions. In April 2026, the company announced a transformative merger with Axalta, enhancing its global R&D capabilities in high-performance non-stick powder coatings. The company reported improved profitability in Q1 2026, driven by the expansion of its industrial excellence programs and growing demand for its Resicoat and Interpon product lines. Its innovation in command-based coating removal technology enables efficient recoating with minimal chemical waste, reducing maintenance costs. AkzoNobel’s coatings comply with EU REACH and FDA regulations, reinforcing its leadership in food-safe industrial applications.

GMM Emerges as Asia’s High-Volume Leader in Ceramic Hybrid Non-Stick Coatings

GMM Non-Stick Coatings has established itself as a key player in the Asia-Pacific non-stick coatings market, focusing on high-volume manufacturing and customized ceramic solutions. In 2026, the company expanded its production capacity in India and China to capture the region’s 51% global market share. Its flagship Duraceram® coating offers a PTFE- and PFOA-free alternative, delivering superior hardness for high-heat cooking applications. GMM’s partnerships with e-commerce platforms for "Certified Non-Stick" labeling address the growing dominance of online retail channels, which account for 40% of sales. The company also leverages nano-pigment dispersion technology to create visually appealing finishes, enhancing its presence in the lifestyle cookware segment.

Thermolon Leads the Shift Toward Ceramic-Based Healthy Non-Stick Coatings

Thermolon, developed by The Cookware Company, is a pioneer in the ceramic non-stick coatings segment, driving the “Healthy Home” movement with mineral-based, PFAS-free coatings. In 2026, the company introduced advanced silicon-oxygen (Si-O) matrix technology, improving thermal conductivity by 20% and enabling faster, energy-efficient cooking. Its coatings can withstand temperatures up to 450°C without emitting toxic fumes, offering a critical advantage over traditional PTFE systems. Thermolon is projected to lead the fastest-growing ceramic coating segment, particularly in APAC and North America. By targeting the commercial hospitality sector with dishwasher-safe formulations, the company has reduced failure rates by 35%, strengthening its position in next-generation non-stick coating solutions.

United States Non-Stick Coatings Market: PFAS-Free Transition and Advanced Fluoropolymer Innovation

The United States leads the non-stick coatings market, driven by a strong “compliance-first” approach following tightening environmental regulations between 2025–2026. The implementation of the Non-Stick Safety Act (2025) has accelerated the shift toward water-based, low-VOC fluoropolymer coatings, increasing adoption across both industrial and consumer applications.

Technological advancements include the development of next-generation sol-gel ceramic coatings, which bridge the gap between traditional PTFE performance and the hardness of inorganic materials. Innovations such as nanometre-thin plasma coatings are delivering high hydrophobicity without relying on legacy PFAS chemistries. Strategic investments, including Chemours’ $35 million PTFE dispersion line in Texas, are expanding production capacity for food-contact and industrial applications. The market is also witnessing strong growth in medical device coatings, where non-thrombogenic, low-friction surfaces are critical for guidewires and catheters. Additionally, expansion by companies like PPG in silicone-polyester hybrid coatings is supporting demand in bakeware and industrial food processing sectors.

China Non-Stick Coatings Market: AI-Driven Manufacturing and High-Volume Industrial Expansion

China dominates the global non-stick coatings market in volume, transitioning toward high-quality, AI-integrated manufacturing systems. Government initiatives such as the “AI Plus” strategy (2026–2030) are enabling optimization of coating processes, including molecular alignment and thickness control, significantly improving efficiency and consistency.

Technological innovation includes the scaling of graphene-reinforced non-stick coatings, reducing friction and energy consumption in industrial machinery. The market is also benefiting from large-scale infrastructure investments, including consumer goods replacement programs, which are driving demand for high-performance cookware and appliances. China’s leadership in EV manufacturing is further boosting demand for specialized non-stick coatings used in battery housings and cooling systems. Regulatory enforcement of strict VOC limits is accelerating the shift toward waterborne formulations, particularly among SMEs, reinforcing sustainable production practices.

Germany Non-Stick Coatings Market: Circular Economy and Bio-Based Material Innovation

Germany is a European leader in non-stick coatings, driven by its focus on circular economy principles and sustainable material development. Innovations in bio-based polymers derived from food-industry by-products, such as collagen and chitosan, are enabling high-performance non-stick coatings with reduced environmental impact.

Technological advancements include the use of laser ablation surface preparation, improving adhesion and extending the lifespan of PFA-coated industrial molds by up to 25%. Germany’s regulatory environment, aligned with the EU Green Deal, is enforcing design-for-recycling principles, ensuring compatibility of coatings with recyclable substrates. Key applications include medical and pharmaceutical packaging, where zero-leachable non-stick coatings prevent contamination and product loss. Infrastructure developments such as closed-loop solvent recovery systems are achieving high solvent recapture rates, further enhancing sustainability.

India Non-Stick Coatings Market: Consumer Demand and Solar Infrastructure Driving Growth

India is emerging as a high-growth market for non-stick coatings, supported by rising consumer demand and expanding infrastructure. Government initiatives like the PLI scheme for white goods and electronics are driving domestic manufacturing, increasing the adoption of coated components.

The market is witnessing a shift toward multi-layer ceramic and hard-anodized coatings, as consumers increasingly demand toxin-free and durable cookware solutions. Infrastructure investments under the National Solar Mission are also boosting demand for anti-soiling non-stick coatings on solar panels, improving efficiency in high-dust regions. Strategic collaborations between domestic and global players are establishing advanced coating centers in cities like Pune, strengthening regional capabilities. Additionally, innovations such as high-heat resistant coatings (up to 450°C) are supporting industrial bakery and food processing applications.

Japan Non-Stick Coatings Market: Ultra-Thin Films and Smart Surface Technologies

Japan’s non-stick coatings market is defined by its expertise in precision materials, ultra-thin film technologies, and smart coatings. The development of hybrid inorganic-organic coatings combines ceramic durability with polymer slip properties, enabling applications in advanced electronics such as foldable displays.

Innovations such as hydrophilic self-cleaning coatings are leveraging ambient humidity to prevent adhesion of oils and dust, maintaining optical clarity in sensitive applications. Japan’s strong R&D ecosystem supports the development of coatings for robotics and automated systems, where performance and cleanliness are critical. Government initiatives under Society 5.0 are promoting the adoption of IoT-enabled smart coatings, capable of monitoring wear and signaling maintenance needs. Investments in digital twin coating lines are further enhancing precision and quality control in high-end manufacturing.

South Korea Non-Stick Coatings Market: Electronics and Energy Storage Driving Advanced Applications

South Korea is emerging as a key player in the non-stick coatings market, leveraging its leadership in electronics, EV batteries, and advanced materials engineering. Technological advancements include the development of high-dielectric non-stick coatings, ensuring no conductive residue transfer in EV battery separator manufacturing.

Innovations such as carbon nanotube (CNT)-based coatings are delivering both thermal conductivity and non-stick performance, particularly in high-tech applications. The market is also driven by demand in foldable OLED displays, where coatings must withstand repeated mechanical stress without degradation. Investments in advanced R&D facilities, such as KCC Corporation’s Surface Engineering Excellence Center, are accelerating the development of nano-silicone hybrid coatings. Additionally, the expansion of regional production hubs is strengthening supply chains for global electronics manufacturers like Samsung and LG.

Italy Non-Stick Coatings Market: Premium Cookware Innovation and Design-Led Growth

Italy remains a global leader in premium non-stick coatings, particularly in the cookware and bakeware segments, combining design innovation with advanced material science. The adoption of titanium- and diamond-reinforced coatings is delivering significantly improved scratch resistance compared to traditional systems.

Technological advancements include impact-bonded and sandwich (SAS) base technologies, ensuring compatibility with induction cooking systems. Sustainability initiatives such as the use of squeeze-cast aluminum are reducing material waste and lowering carbon footprints in manufacturing. Italy’s dominance in premium bakeware is supported by silicone-based non-stick coatings that eliminate the need for additional greasing materials. Product innovations such as high-temperature stable “oven-to-table” coatings are enhancing both functionality and aesthetics, reinforcing Italy’s position as a trendsetter in the global non-stick coatings market.

Non-Stick Coatings Market Report Scope

Non-Stick Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.4 Billion

|

|

Market Size (2032)

|

$5 Billion

|

|

Market Growth Rate

|

5.8%

|

|

Segments

|

By Type (Fluoropolymers, Ceramic, Silicone Coatings, Nanotechnology and Hybrid Coatings, Other Specialty Polymeric Coatings), By Formulation Technology (Water-borne, Solvent-borne, Powder Coatings, High-Solids), By Substrate Material (Metals, Non-Metals), By End-Use Industry (Consumer Goods, Food Processing and Bakery, Automotive and Transportation, Medical and Healthcare, Electrical and Electronics, Industrial Machinery, Textiles and Carpets), By Number of Layers (Single-Layer Systems, Two-Layer Systems, Multi-Layer), By Distribution (Direct Sales, Specialty Chemical Distributors, Contract Coating Service Providers, Retail), By Price Tier (Mass Market, Mid-Range, Premium)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Chemours Company, PPG Industries, Inc., Daikin Industries, Ltd., Akzo Nobel N.V., 3M, Solvay S.A., Weilburger Coatings GmbH, The Sherwin-Williams Company, AGC Inc., Pfluon Technology Co., Ltd., GMM Coatings, Industrielack AG, Arkema S.A., Whitford Corporation, Hempel A/S

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Non Stick Coatings Market Segmentation

By Type

- Polytetrafluoroethylene

- Fluorinated Ethylene Propylene

- Perfluoroalkoxy

- Ethylene Tetrafluoroethylene

- Ceramic

- Silicone Coatings

- Nanotechnology and Hybrid Coatings

- Other Specialty Polymeric Coatings

By Formulation Technology

- Water-borne

- Solvent-borne

- Powder Coatings

- High-Solids

By Substrate Material

By End-Use Industry

- Consumer Goods

- Food Processing and Bakery

- Automotive and Transportation

- Medical and Healthcare

- Electrical and Electronics

- Industrial Machinery

- Textiles and Carpets

By Number of Layers

- Single-Layer Systems

- Two-Layer Systems

- Multi-Layer

By Distribution

- Direct Sales

- Specialty Chemical Distributors

- Contract Coating Service Providers

- Retail

By Price Tier

- Mass Market

- Mid-Range

- Premium

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Non Stick Coatings Industry

- The Chemours Company

- PPG Industries, Inc.

- Daikin Industries, Ltd.

- Akzo Nobel N.V.

- 3M

- Solvay S.A.

- Weilburger Coatings GmbH

- The Sherwin-Williams Company

- AGC Inc.

- Pfluon Technology Co., Ltd.

- GMM Coatings

- Industrielack AG

- Arkema S.A.

- Whitford Corporation

- Hempel A/S

*- List not Exhaustive