North America Municipal Water Treatment Chemicals Market: Growth Analysis, Value Projections, and Industry Forecast

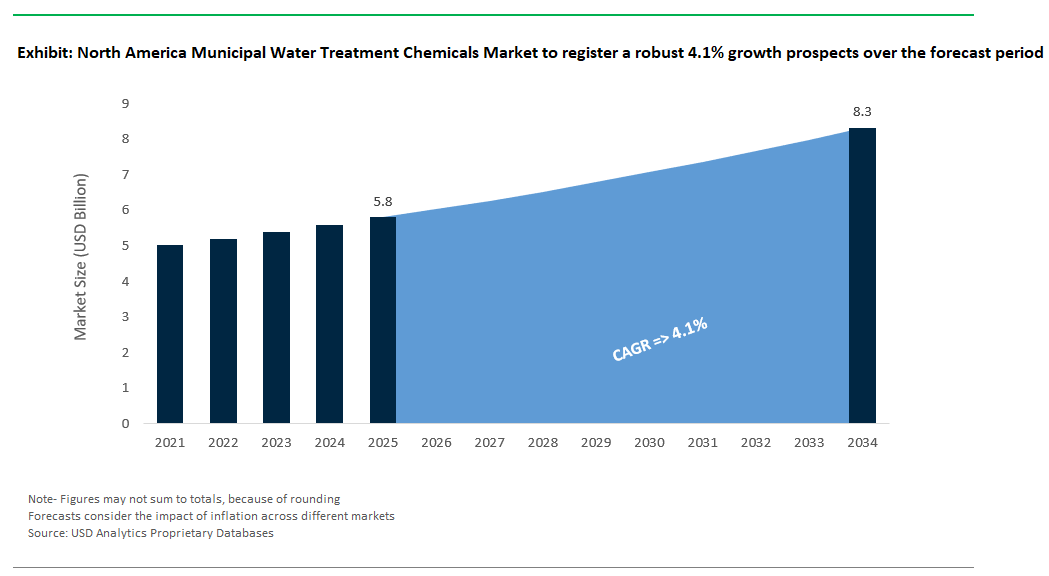

North America Municipal Water Treatment Chemicals Market Size is estimated at $5.8 Billion in 2025 and is forecast to register an annual growth rate (CAGR) of 4.1% to reach $8.3 Billion by 2034.

The municipal water treatment chemicals market in North America is fundamentally shaped by stringent regulatory frameworks, aging infrastructure, and a growing emphasis on sustainable, cost-effective operations. Core chemical treatment processes particularly coagulation and flocculation remain essential in both surface water and groundwater treatment systems. Aluminum sulfate (alum) continues to be the most widely used primary coagulant, typically applied at dosages ranging from 10–50 mg/L, though actual rates vary based on raw water quality. Alternative coagulants such as polyaluminum chloride (PACl) are gaining traction due to their effectiveness over a broader pH range, higher charge density, and generally lower sludge production. Utilities frequently conduct jar tests and pilot-scale studies to optimize chemical selection and dosage, balancing treatment performance with cost and residuals management.

Disinfection remains a critical focus under U.S. EPA rules such as the Stage 1 and Stage 2 Disinfectants and Disinfection Byproducts Rules (D/DBPR). Many systems have transitioned to chloramine as a secondary disinfectant to reduce regulated byproducts like trihalomethanes (THMs) and haloacetic acids (HAAs), especially in systems with extended distribution networks. Chlorine dioxide is selectively used as a pre-oxidant in certain facilities, though its application is more limited due to operational complexity and residual concerns. Granular activated carbon (GAC) is widely employed in surface water systems for control of taste, odor, and synthetic organic compounds. Typical empty bed contact times (EBCT) range from 10 to 20 minutes, and media regeneration or replacement cycles are generally determined by site-specific breakthrough curves often spanning 12 to 24 months in full-scale systems.

For corrosion control, orthophosphate is the standard additive used to form protective scales inside pipes and mitigate lead and copper release, as required by the EPA's Lead and Copper Rule (LCR). Silicates are also applied in some systems as supplementary corrosion inhibitors, particularly where phosphate-based formulations are not preferred due to potential nutrient loading concerns. Corrosion control strategies are routinely reassessed during infrastructure upgrades and in response to revised regulatory guidance, such as the forthcoming Lead and Copper Rule Improvements (LCRI).

Market Trend: PFAS Regulation and Digitized Chemical Management

The evolving regulatory environment around per- and polyfluoroalkyl substances (PFAS) is a defining trend in the North American municipal water treatment market. In 2024, the U.S. EPA finalized Maximum Contaminant Levels (MCLs) for six PFAS compounds, including PFOA and PFOS at 4 ppt each. These regulations have prompted widespread evaluation of advanced treatment technologies, including high-efficiency ion exchange resins, nanofiltration membranes, and next-generation adsorbents designed specifically for PFAS capture. While GAC remains a frontline solution, its effectiveness for short-chain PFAS and regeneration limitations are prompting utilities to explore complementary or replacement technologies.

At the same time, utilities are increasingly deploying digital tools to enhance chemical dosing accuracy and reduce operational costs. AI- and sensor-enabled platforms are being piloted and adopted to provide real-time adjustments in coagulant and disinfectant dosing based on influent turbidity, pH, and chlorine demand. These platforms contribute to chemical cost savings, improved regulatory compliance, and data transparency making them attractive under funding programs such as the Bipartisan Infrastructure Law (BIL) and the Drinking Water State Revolving Fund (DWSRF). Many utilities now prioritize suppliers offering transparent sustainability metrics, including product carbon footprint data and green chemistry certifications.

Growth Opportunity: Advanced Disinfection and Nutrient Recovery

Opportunities for market growth are increasingly tied to innovation in disinfection and nutrient recovery. Utilities facing elevated pathogen risks such as Legionella are evaluating ultraviolet (UV) and ozone-based disinfection systems as primary or supplementary treatments, particularly in large urban centers and facilities with vulnerable populations. Monochloramine remains a preferred choice for distribution system stability, while oxidants like peracetic acid are used selectively in low-THM applications or where contact time is limited.

On the nutrient front, phosphorus recovery is becoming a strategic priority, particularly in regions with water quality-sensitive receiving watersheds. State-led mandates in places like Wisconsin are pushing utilities to recover phosphorus from biosolids and sidestreams. Technologies such as Ostara’s Pearl® process, deployed at facilities like DC Water’s Blue Plains Advanced Wastewater Treatment Plant, enable recovery of phosphorus as marketable struvite fertilizer, turning a regulatory burden into a revenue opportunity.

Additionally, decentralized water systems including tribal and remote communities are increasingly turning to modular, solar-powered treatment units integrating natural coagulants (e.g., chitosan) and low-energy reverse osmosis (RO) for contaminant removal, including arsenic and uranium. These technologies are particularly impactful in underserved areas, offering compliance-level water quality at a fraction of the lifecycle cost of centralized systems. Collectively, these developments represent significant commercial potential for chemical suppliers that offer high-performance, regulation-compliant products integrated with digital and modular delivery solutions.

Competitive Analysis: North America Municipal Water Treatment Chemicals Market

The North American municipal water treatment chemicals market features a strong competitive structure. Tier 1 players, which include multinational water companies, hold over 60% of the market. They achieve this through long-term contracts, regulatory insight, and a wide range of capabilities. Ecolab (Nalco Water) leads in disinfection by integrating digital solutions into municipal systems. A recent example is its smart chemical dosing project with the Chicago MWRD, supported by its own IoT platforms and extended operation and maintenance agreements. Kemira maintains a strong position in coagulation with its aluminum-based chemicals and low-carbon PAC products. It takes advantage of pre-approved EPA formulations to move faster than slower rivals. Chemtrade’s integration in the chlor-alkali sector strengthens its chlorine supply across North America. This further benefits from its strategic acquisition of Basic Chemicals. Solvay, focusing on biofilm control through specialty polymers, has partnered with Xylem to use AI for dosing. This reflects a growing trend where chemical formulation and digital optimization come together.

Tier 2 players are agile within specific regions, often winning by providing local service, closeness, and fast delivery. Companies such as USALCO and PVS Chemicals have established their places in the Northeast and Great Lakes regions by using local emergency response capabilities and cooperative purchasing programs to secure their positions. Westlake Chemical utilizes its logistics advantage with its own rail tank car fleet to rapidly deliver chlorine derivatives across the South. This capability is especially necessary during emergencies or supply chain issues. These companies play a vital role in meeting the needs of mid-sized municipalities with cost-effective and adaptable service options.

Tier 3 disruptors are introducing new technology into niche but fast-growing sectors like PFAS remediation and lead service line treatment. Startups such as AquaHawk and ClearAqua are using AI and electrochemical disinfection methods to assist utilities adapting to new regulations. With backing from the U.S. Department of Energy and venture capital firms like Kleiner Perkins, these disruptors are poised to bring innovative methods to market, challenging established chemical companies especially where new infrastructure funding opens doors for innovative firms.

The competitive landscape is also shaped by three main areas: regulatory responsiveness, infrastructure partnerships, and sustainability focus. Market leaders like Ecolab and Kemira are closely following stricter EPA requirements through tech-driven traceability and next-generation chemical products. Collaborations, such as the USALCO-Ferguson strategy for combining pipe and chemical services, yield noticeable cost savings. Sustainability is becoming a key differentiator. PVS's solar-powered chlorine production, Kemira’s aim for carbon-neutral PAC by 2026, and Nexom’s USDA-certified biobased inhibitors are increasingly important for winning large contracts with environmentally conscious municipalities.

Looking to the future, the competitive edge may depend on the capacity to provide climate-resilient, digitally integrated chemical solutions that tackle complicated regulatory, operational, and environmental issues. As chloramine starts to take the place of traditional chlorine and alternative coagulants gain traction over aluminum-based ones, the ability to offer modular, circular, and disaster-ready treatment solutions will distinguish future leaders from traditional players. M&A activities, including expected moves by 3M and DuPont into PFAS treatment, along with digital water initiatives (where 60% of utilities are anticipated to seek cloud-based dosing systems by 2027), indicate a shift in the market from chemical commoditization to comprehensive municipal water solutions.

North America Municipal Water Treatment Chemicals Market– Segmentation Insights (2025–2034)

By Type of Chemical: Coagulants Lead, Adsorbents Gain Rapid Momentum

In the North American municipal water treatment chemicals market, coagulants and flocculants are set to lead with a projected market share of 35.2% in 2025, reflecting their foundational role in both drinking water and wastewater treatment. Chemicals like aluminum sulfate (alum), ferric chloride, and polyDADMAC are widely used for removing turbidity, color, suspended solids, and dissolved organic matter. These coagulants are vital for ensuring safe, visually clear drinking water and for enhancing sludge dewatering in municipal wastewater plants.

Meanwhile, adsorbents are expected to be the fastest-growing segment with a CAGR of 5.9% through 2034, driven by emerging contaminant regulations, especially around PFAS (per- and polyfluoroalkyl substances), pharmaceuticals, and microplastics. Granular activated carbon (GAC), ion exchange resins, and new-generation synthetic adsorbents are increasingly deployed to comply with EPA mandates and state-level drinking water standards. Municipalities across the United States and Canada are upgrading their treatment infrastructure to incorporate advanced adsorptive filtration especially in regions like Michigan, New Jersey, and Ontario where PFAS contamination has made national headlines.

.png)

By Application: Drinking Water Treatment Dominates, Wastewater Gains Focus on Nutrient Removal

Drinking water treatment is projected to remain the dominant application, accounting for 59.6% of the market in 2025, largely due to regulatory compliance under the U.S. Safe Drinking Water Act (SDWA) and Canada’s Guidelines for Canadian Drinking Water Quality. Utilities rely heavily on coagulants, disinfectants, and corrosion inhibitors to maintain water clarity, kill pathogens, and reduce lead leaching from aging infrastructure. The use of chloramine and chlorine dioxide is expanding, offering long-lasting residuals while minimizing disinfection byproducts (DBPs).

On the other hand, municipal wastewater treatment is forecast to grow at a steady CAGR of 6.3%, with heightened attention to nutrient removal (nitrogen and phosphorus) to prevent eutrophication in receiving water bodies. This segment also sees increasing use of advanced treatment chemicals to control emerging pollutants, such as endocrine disruptors and pharmaceutical residues. With initiatives like the U.S. EPA’s Effluent Guidelines Program and stricter NPDES permit requirements, municipalities are investing in both chemical and biological enhancements to meet effluent discharge standards across North America.

North America Municipal Water Treatment Chemicals Report Scope

North America Municipal Water Treatment Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.8 Billion

|

|

Market Size (2034)

|

$8.3 Billion

|

|

Market Growth Rate

|

4.1%

|

|

Segments

|

By Type of Chemical (Coagulants and Flocculants, Biocides and Disinfectants, pH Adjusters and Neutralizers, Scale and Corrosion Inhibitors, Adsorbents, Other Specialty Chemicals), By Application (Drinking Water Treatment, Municipal Wastewater Treatment), By Form of Chemical (Liquid, Powder/Solid, Gas

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ecolab Inc. (U.S.), Solenis LLC (U.S.), Kemira Oyj (Finland), SNF Holding Company (U.S.), BASF SE (Germany), Veolia Water Technologies (France), SUEZ Water Technologies and Solutions (France), The Dow Chemical Company (U.S.), Nouryon (The Netherlands), Kurita Water Industries Ltd. (Japan), ChemTreat, Inc. (U.S.), Axiall Corporation (Westlake Chemical Corporation - U.S.),

|

|

Countries

|

US, Canada, Mexico

|

North America Municipal Water Treatment Chemicals Market Segmentation

By Type of Chemical

- Coagulants and Flocculants

- Biocides and Disinfectants

- Oxidizing Biocides

- Non-Oxidizing Biocides

- pH Adjusters and Neutralizers

- Scale and Corrosion Inhibitors

- Phosphates

- Silicates

- Zinc compounds

- Adsorbents

- Other Specialty Chemicals

By Application

- Drinking Water Treatment

- Raw Water Clarification

- Filtration Aids

- Disinfection

- Taste and Odor Control

- Fluoridation

- Corrosion Control in Distribution Systems

- Municipal Wastewater Treatment

- Primary Treatment

- Secondary Treatment

- Tertiary Treatment

- Sludge Treatment and Dewatering

- Odor Control

By Form of Chemical

By Country

- United States

- Canada

- Mexico

Top Companies in North America Municipal Water Treatment Chemicals Market

- Ecolab Inc. (U.S.)

- Solenis LLC (U.S.)

- Kemira Oyj (Finland)

- SNF Holding Company (U.S.)

- BASF SE (Germany)

- Veolia Water Technologies (France)

- SUEZ Water Technologies and Solutions (France)

- The Dow Chemical Company (U.S.)

- Nouryon (The Netherlands)

- Kurita Water Industries Ltd. (Japan)

- ChemTreat, Inc. (U.S.)

- Axiall Corporation (Westlake Chemical Corporation - U.S.)

* List Not Exhaustive

Research Coverage

This report investigates the North America Municipal Water Treatment Chemicals Market, offering detailed analysis reviews on regulatory drivers, chemical innovations, and digital dosing trends that define this critical sector. It highlights breakthroughs such as PFAS-targeted adsorbents, advanced coagulant formulations, and AI-enabled dosing platforms, positioning the report as an essential resource for decision-makers across utilities and chemical suppliers. USDAnalytics delivers actionable insights on market dynamics, competitive benchmarking, and technology adoption shaping municipal water systems across the U.S., Canada, and Mexico, ensuring a robust understanding of both regulatory compliance and sustainability imperatives for 2025–2034.

Key Research Details:

- Segmentation:

- By Type of Chemical: Coagulants & Flocculants, Biocides & Disinfectants (Oxidizing & Non-Oxidizing), pH Adjusters & Neutralizers, Scale & Corrosion Inhibitors, Adsorbents, Other Specialty Chemicals.

- By Application: Drinking Water Treatment (Raw Water Clarification, Filtration Aids, Disinfection, Taste & Odor Control, Fluoridation, Corrosion Control), Municipal Wastewater Treatment (Primary, Secondary, Tertiary, Sludge Dewatering, Odor Control).

- By Form: Liquid, Powder/Solid, Gas.

- Geographic Scope: United States, Canada, Mexico.

- Study Period: Historic: 2021–2024; Forecast: 2025–2034

- Top Companies: Ecolab Inc. (U.S.), Solenis LLC (U.S.), Kemira Oyj (Finland), SNF Holding Company (U.S.), BASF SE (Germany), Veolia Water Technologies (France), SUEZ Water Technologies & Solutions (France), The Dow Chemical Company (U.S.), Nouryon (The Netherlands), Kurita Water Industries Ltd. (Japan), ChemTreat, Inc. (U.S.), Axiall Corporation (Westlake Chemical Corporation – U.S.).

Methodology

USDAnalytics applies a structured research methodology combining primary interviews with water utility managers, municipal regulators, and chemical suppliers alongside secondary research from U.S. EPA, Environment Canada, and ASTM standards. Market size estimations employ a bottom-up modeling approach validated with capex patterns under programs like the Bipartisan Infrastructure Law (BIL) and NPDES compliance initiatives. Forecasting integrates macroeconomic indicators, water treatment upgrade cycles, and regulatory changes into advanced econometric models. The study applies rigorous data triangulation across financial disclosures, government databases, and case studies from municipal water and wastewater facilities across North America.

Deliverables

- Complete Market Research Report (PDF, Excel): data tables, market charts, and visual insights.

- Country-Level Forecasts & Analysis

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis

- Recent Developments & News Tracker

- Executive summary and key takeaway slides for boardroom presentations

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements