North America Produced Water Treatment for EOR Market: Growth Outlook, Analysis, and Forecast to 2034

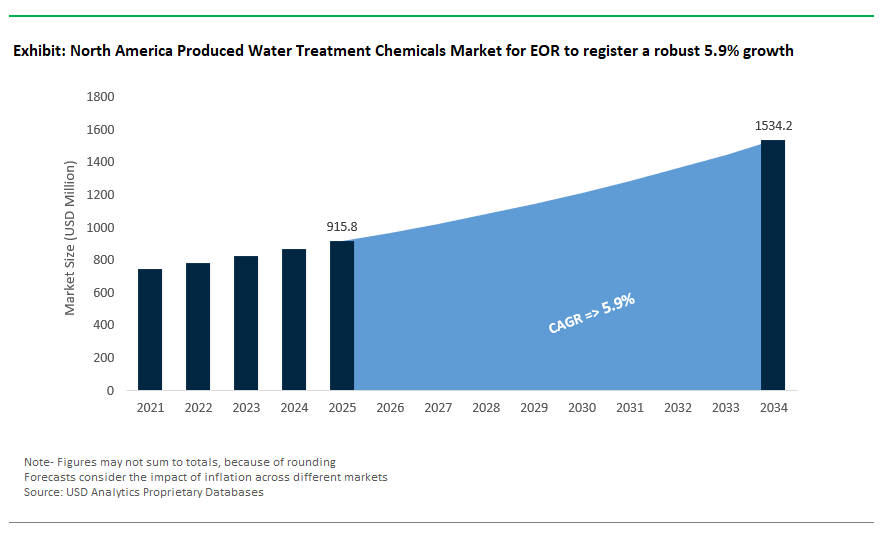

North America Produced Water Treatment Chemicals Market for Enhanced Oil Recovery (EOR) Applications Size is estimated at $915.8 Million in 2025 and is forecast to register an annual growth rate (CAGR) of 5.9% to reach $1534.1 Million by 2034.

The North American produced water treatment market for enhanced oil recovery (EOR) applications is shaped by the dual imperatives of maximizing injection efficiency and protecting high-value equipment in thermally and chemically aggressive environments. Managing scaling and corrosion in recycled water is a top priority, with phosphonate–polycarboxylate inhibitor blends dosed at 5–20 ppm effectively suppressing calcium carbonate at LSI >2.5 and barium sulfate at saturation indices up to 1.8, in accordance with NACE TM0197. These inhibitors exhibit thermal stability above 150°C, making them suitable for high-pressure steam flood operations common in heavy oil plays, as noted by DOE NETL (2023).

Oxygen scavenging is another critical control point carbohydrazide, a non-toxic alternative to hydrazine, is deployed at 2–4x stoichiometric ratios to maintain dissolved oxygen below 10 ppb, aligning with EPA SW-846 waste handling criteria. For oil-water separation, polyol ester and ethoxylated demulsifiers dosed at 10–50 ppm can reduce oil-in-water concentrations to under 10 ppm, per API 19G8 performance standards. Foam control during gas flooding is handled using low-dose (1–5 ppm) silicone-polyether defoamers, which prevent operational disruptions linked to foam carryover, especially in high-CO₂ or methane-rich injectate environments (SPE 206672).

Microbial-induced souring and biofouling are managed through glutaraldehyde and THPS biocide pulses at 50–150 ppm, which suppress sulfate-reducing bacteria (SRB) populations and achieve >90% hydrogen sulfide reduction, as validated by NACE TM0212. Where H₂S persists, triazine-based scavengers provide rapid neutralization while ensuring compliance with OSHA’s 20 ppm ceiling exposure limit. As operators seek to reduce freshwater dependency and chemical OPEX, this segment is seeing rising interest in treatment packages tailored for thermal resilience, microbial selectivity, and high-recovery water reuse in closed-loop EOR systems.

Market Trend: High-Efficiency, Sustainable Chemical Formulations Revolutionize Produced Water Reuse in EOR

The North American produced water treatment chemicals market is undergoing a rapid transformation as oilfield operators prioritize sustainability, operational efficiency, and regulatory compliance in Enhanced Oil Recovery (EOR) operations. With stricter enforcement of the EPA’s 2024 Produced Water Standards capping oil and grease at <10 ppm producers are adopting green chemistry alternatives and AI-enhanced dosing systems. Innovative solutions like Baker Hughes’ H2Zero™ inhibitor deliver 90% scale reduction while slashing freshwater consumption by 30% in the Permian Basin, aligning directly with Occidental’s net-zero goals. Meanwhile, Clariant’s FoamTrol™ ECO, a PFAS-free siloxane defoamer, meets Canada’s CleanBC regulatory requirements for oil sands reuse. The integration of digital platforms like Schlumberger’s AquaConnect™, which optimizes dosing based on real-time salinity and ion profiles, is accelerating cost reductions of 25% or more. As EOR economics increasingly hinge on produced water reuse, the market is shifting toward biodegradable, low-carbon-footprint inhibitors that reduce OPEX and meet ESG targets. The competitive edge lies with suppliers offering non-toxic, field-proven chemistries bundled with smart monitoring tools, unlocking performance in both onshore and offshore fields from the Eagle Ford to the Gulf of Mexico.

Growth Opportunity: Lithium Recovery from Produced Water Sparks $500M+ Chemical Demand Surge

A transformative opportunity is emerging at the intersection of water treatment and battery materials: Direct Lithium Extraction (DLE) from produced water. Oilfield brines once a waste management liability are being tapped for their lithium content, catalyzing a $500M+ demand boom for specialized treatment chemicals by 2030. Projects like Standard Lithium’s Arkansas operation are pioneering the use of selective antiscalants to prevent silica and sulfate fouling in lithium adsorption units, increasing recovery efficiency by 20%. As North America races to localize critical mineral supply chains, especially for EVs and grid storage, lithium-rich oilfield brines represent a double win: sustainable water reuse and mineral monetization. Further enhancing this trend, ExxonMobil’s Permian pilot leverages green scale inhibitors and nanofiltration to enable 90% brine reuse in CO₂-EOR, while Chevron’s water reuse strategy is earning carbon credits valued at $15/ton CO₂. Offshore platforms like Shell’s Vito FPU are deploying compact electrocoagulation units to cut chemical use by 40%, paving the way for DLE-ready water systems in space-constrained environments. As New Mexico’s SB 489 law introduces $100K/day spill fines, and ESG investors demand reduced freshwater dependency, operators and suppliers alike are co-investing in multifunctional, DLE-compatible water treatment chemistries that turn waste into revenue.

Competitive Analysis: North America Produced Water Treatment Chemicals Market for EOR Applications

The North American market for produced water treatment chemicals in Enhanced Oil Recovery (EOR) applications is highly competitive and specialized across different chemical functions, basin requirements, and sustainability goals. Major players like Ecolab (Nalco Champion), Baker Hughes, Schlumberger, and Halliburton dominate this market, holding more than half of it. This sector features proprietary monitoring systems, customized formulations based on reservoir geology, and various commercial models such as chemical leasing and pay-per-barrel pricing. These companies use their technological advantages to implement smart platforms like Ecolab’s 3D TRASAR Oilfield and Baker Hughes’ Altalion nano-inhibitors, focusing on complex formations in the Permian, Bakken, and Marcellus basins. Their use of digital intelligence, such as real-time AI for scale prediction or blockchain for chemical traceability, is changing chemical management in oilfield water treatment.

The Tier 2 segment is becoming more important, representing 35% of the market. It includes specialty providers like Dorf Ketal, Clariant, Innospec, and Solenis, which have established niche positions through targeted innovations. For instance, Dorf Ketal is the only NSF-certified supplier for H₂S scavengers in sour gas fields, while Clariant is taking advantage of ESG trends with its bio-based inhibitors and carbon-reduction platforms. These companies are also exploring carbon credit-linked chemistry and modular, skid-mounted manufacturing, appealing to operators who want flexible and sustainable solutions. Companies like Solenis excel in polymer flooding with shear-resistant polymers that handle reservoir stress, while Innospec improves waterflood operations by generating oxygen scavengers on-site.

Tier 3 regional formulators are fragmented and hold just a 10% market share but are essential in cost-sensitive and decentralized markets, like stripper wells and marginal fields. They offer prices up to 40% lower than larger companies and thrive in regions that multinationals do not serve well. Their success comes from customization, quick delivery, and price flexibility, but their limited R&D capabilities expose them to risks from stricter regulations and the rise of ESG-focused procurement.

In examining application trends, the market is shifting toward high-impact EOR techniques polymer flooding, ASP, and CO₂ injection all of which require innovative and often diverse chemistries. Companies like Solenis and Ecolab are bringing viscosity-modulating and shear-resistant polymers to the market, while Baker Hughes and Clariant are advancing integration of surfactants and alkaline solutions with pH-stable chemicals. Temperature-resistant demulsifiers and enzyme/UV-based biocides are also becoming popular in high-TDS or thermally challenging settings.

Future competitive success will depend on three connected areas: digital integration, green chemistry, and extraction synergies. Companies are adapting by using predictive analytics, cloud-based dosing, and automated compliance reporting, which are crucial for meeting regulations in states like California and New Mexico. Differentiation through sustainability, like Clariant’s plant-based inhibitors and Solenis' closed-loop recycling systems, is helping secure contracts with ESG-focused operators. Additionally, new opportunities such as lithium and boron recovery from flowback water are emerging as competitive areas, with Schlumberger and Baker Hughes testing approaches that extract mineral values beyond just water treatment.

North America Produced Water Treatment Chemicals Market for EOR Applications– Segmentation Insights (2025–2034)

By Type of Chemical: Corrosion Inhibitors Lead, Specialty EOR Chemicals Accelerate Rapidly

In North America’s produced water treatment market for Enhanced Oil Recovery (EOR), corrosion inhibitors are projected to dominate with a 2025 market share of approximately 24.9%, as they play a critical role in safeguarding pipelines, well casings, and separation units exposed to high-salinity water and extreme conditions. These chemicals are particularly indispensable in shale formations like the Permian Basin and Bakken, where elevated chloride and sulfate levels intensify the risk of equipment degradation. The continuous need to extend asset life and maintain flow assurance is driving widespread use of film-forming and neutralizing corrosion inhibitors.

At the same time, specialty chemicals tailored for EOR fluids though a smaller segment are forecast to grow at the fastest CAGR of 6.8% through 2034. These include tailored surfactants, polymers, and emulsion breakers designed to optimize oil recovery efficiency while reducing formation damage. With increasing reuse of produced water in chemical flooding operations, demand for high-performance additives that can maintain viscosity, reduce interfacial tension, and mitigate scaling or microbial fouling is surging. Growth is particularly strong in Canada’s Alberta region and Texas, where operators are scaling up EOR projects with advanced chemical formulations to maximize recovery from mature fields.

.png)

By Application Point in Produced Water Treatment Flow: Upstream Dominates, Centralized Facilities Expand Rapidly

Upstream applications are expected to hold the largest market share at around 43.9% in 2025, owing to the heavy concentration of produced water treatment activities at the wellhead and separation stage. At this early phase, operators deploy a suite of chemicals such as demulsifiers, corrosion inhibitors, and biocides to separate oil from water, protect surface equipment, and reduce microbial contamination. The demand is particularly intense in unconventional plays where high water-to-oil ratios demand aggressive and continuous chemical treatment programs.

On the other hand, centralized treatment facilities are projected to be the fastest-growing segment, with a CAGR of 7.1%, as oilfield operators shift toward more sustainable water reuse strategies for EOR. These centralized hubs treat bulk volumes of produced water for reinjection in polymer flooding or surfactant-based enhanced recovery methods, reducing freshwater demand and improving operational economics. Growth is particularly notable in regions such as Texas and Saskatchewan, where tight regulatory frameworks and water scarcity are driving investment in closed-loop water systems. The integration of membrane technologies and chemical treatment at these facilities is fostering long-term demand for advanced water conditioning agents tailored for EOR performance.

North America Produced Water Treatment Chemicals Market for Enhanced Oil Recovery (EOR) Applications Report Scope

North America Produced Water Treatment Chemicals Market for Enhanced Oil Recovery (EOR) Applications

|

Parameter

|

Details

|

|

Market Size (2025)

|

$915.8 Million

|

|

Market Size (2034)

|

$1534.1 Million

|

|

Market Growth Rate

|

5.9%

|

|

Segments

|

By Type of Chemical (Corrosion Inhibitors, Scale Inhibitors, Biocides, Flocculants and Coagulants, Demulsifiers, Oxygen Scavengers, H2S Scavengers, Defoamers and Antifoaming Agents, Specialty Chemicals for EOR Fluids, Adsorbents), By EOR Technology Application (Polymer Flooding, Surfactant-Polymer (SP) Flooding / Alkaline-Surfactant-Polymer (ASP) Flooding, Thermal EOR (Steam Flooding, SAGD - Steam-Assisted Gravity Drainage), Chemical EOR in Unconventional Plays), By Application Point in Produced Water Treatment Flow (Upstream (Wellhead/Separation), Midstream (Pipelines/Storage), Centralized Treatment Facilities), By Operation Type (Onshore EOR Operations, Offshore EOR Operations

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ecolab Inc. (U.S.), Solenis LLC (U.S.), Baker Hughes Company (U.S.), SLB (formerly Schlumberger) (U.S.), Halliburton (U.S.), Kemira Oyj (Finland), BASF SE (Germany), The Dow Chemical Company (U.S.), Nouryon (The Netherlands), Albemarle Corporation (U.S.), Buckman (U.S.),

|

|

Countries

|

US, Canada, Mexico

|

North America Produced Water Treatment Chemicals Market for Enhanced Oil Recovery (EOR) Applications Market Segmentation

By Type of Chemical

- Corrosion Inhibitors

- Scale Inhibitors

- Biocides

- Flocculants and Coagulants

- Demulsifiers

- Oxygen Scavengers

- H2S Scavengers

- Defoamers and Antifoaming Agents

- Specialty Chemicals for EOR Fluids

- Adsorbents

By EOR Technology Application

- Polymer Flooding

- Surfactant-Polymer (SP) Flooding / Alkaline-Surfactant-Polymer (ASP) Flooding

- Thermal EOR (Steam Flooding, SAGD - Steam-Assisted Gravity Drainage)

- Chemical EOR in Unconventional Plays

By Application Point in Produced Water Treatment Flow

- Upstream (Wellhead/Separation)

- Demulsification

- Corrosion/Scale Inhibition in flowlines

- Biocide dosing

- Midstream (Pipelines/Storage)

- Corrosion/Scale Inhibition

- Biocide dosing

- H2S Scavenging

- Centralized Treatment Facilities

- Coagulation/Flocculation

- Filtration aids

- Disinfection

- Membrane Cleaning

- Sludge dewatering

By Operation Type

- Onshore EOR Operations

- Offshore EOR Operations

By Country

- United States

- Canada

- Mexico

Top Companies in North America Produced Water Treatment Chemicals Market for Enhanced Oil Recovery (EOR) Applications

- Ecolab Inc. (U.S.)

- Solenis LLC (U.S.)

- Baker Hughes Company (U.S.)

- SLB (formerly Schlumberger) (U.S.)

- Halliburton (U.S.)

- Kemira Oyj (Finland)

- BASF SE (Germany)

- The Dow Chemical Company (U.S.)

- Nouryon (The Netherlands)

- Albemarle Corporation (U.S.)

- Buckman (U.S.)

* List Not Exhaustive

Research Coverage

This report investigates the North America Produced Water Treatment Chemicals Market for Enhanced Oil Recovery (EOR) Applications, delivering comprehensive analysis reviews on corrosion inhibitors, scale control, demulsifiers, and biocides, alongside emerging segments such as specialty EOR additives and green chemistries. It highlights breakthroughs in produced water reuse, PFAS-free inhibitors, and AI-based dosing platforms, providing actionable intelligence on operational efficiency, ESG compliance, and digital transformation in oilfield water management. This report is an essential resource for operators, chemical suppliers, and strategic planners seeking insights into sustainability trends and market shifts across upstream, midstream, and centralized treatment facilities. USDAnalytics ensures industry professionals access data-driven projections, competitive strategies, and innovation roadmaps to navigate a rapidly evolving EOR landscape.

Key Research Details:

- Segmentation:

- By Type of Chemical: Corrosion Inhibitors, Scale Inhibitors, Biocides, Flocculants and Coagulants, Demulsifiers, Oxygen Scavengers, H₂S Scavengers, Defoamers, Specialty Chemicals for EOR Fluids, Adsorbents.

- By EOR Technology Application: Polymer Flooding, ASP Flooding, Thermal EOR, Chemical EOR in Unconventional Plays.

- By Application Point: Upstream (Wellhead/Separation), Midstream (Pipelines/Storage), Centralized Treatment Facilities.

- By Operation Type: Onshore EOR, Offshore EOR.

- Geographic Scope: United States, Canada, Mexico.

- Study Period: Historic data from 2021–2024 and forecast data from 2025–2034.

- Top Companies: Ecolab Inc. (U.S.), Solenis LLC (U.S.), Baker Hughes Company (U.S.), SLB (U.S.), Halliburton (U.S.), Kemira Oyj (Finland), BASF SE (Germany), Dow Chemical (U.S.), Nouryon (The Netherlands), Albemarle (U.S.), Buckman (U.S.).

Methodology

USDAnalytics applies a multi-tier research methodology combining extensive primary interviews with oilfield operators, EOR project managers, and chemical engineers, along with secondary research from SPE journals, NACE guidelines, and regulatory frameworks (EPA, API). Market size estimations follow a bottom-up approach based on chemical consumption intensity per barrel of produced water, EOR activity levels, and adoption rates of advanced treatment technologies. Forecast models incorporate econometric trend analysis and scenario-based modeling reflecting sustainability mandates, lithium recovery opportunities, and ESG-driven procurement strategies. Data triangulation across company disclosures, procurement databases, and pilot-scale studies ensures accuracy and credibility for strategic decision-making.

Deliverables

- Complete Market Research Report (PDF, Excel): data tables, market charts, and visual insights.

- Country-Level Forecasts & Analysis

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis

- Recent Developments & News Tracker

- Executive summary and key takeaway slides for boardroom presentations

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements