North American Water Treatment Chemicals Market: Value Analysis, Growth Trends, and Forecast to 2034

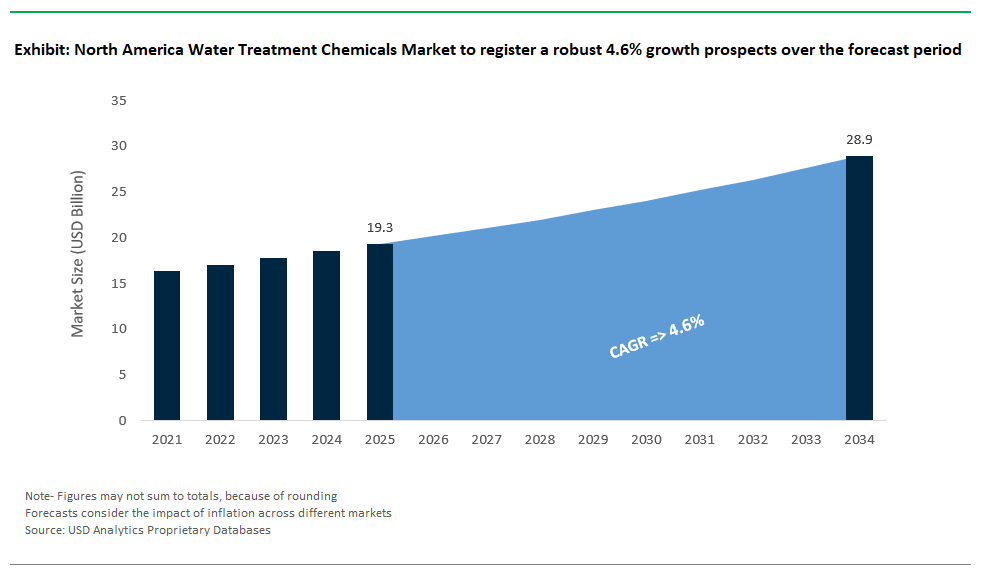

North America Water Treatment Chemicals Market Size is estimated at $19.3 Billion in 2025 and is forecast to register an annual growth rate (CAGR) of 4.6% to reach $28.9 Billion by 2034.

The North American water treatment chemicals market continues to evolve at the intersection of stringent regulatory mandates, aging infrastructure, and rising public health expectations, especially within municipal systems. Lead control remains a national priority, with orthophosphate dosing demonstrated to reduce lead leaching below 3 µg/L, aligning with the 2024 Lead and Copper Rule Improvements (LCRI), which emphasize proactive corrosion control and lower trigger levels. In parallel, PFAS contamination is prompting widespread adoption of hybrid systems combining granular activated carbon (GAC) and anion exchange resins typically offering PFOS/PFOA capacities of 1.0–1.5 mmol/g resin optimized for breakthrough delays and regeneration efficiency.

Disinfection strategies are shifting toward advanced oxidation processes (AOPs); UV-AOP units utilizing ultraviolet light (typically at 254 nm or UV-A range) and hydrogen peroxide have been validated for >6-log virus inactivation and certified under NSF/ANSI 55 Class A standards. In shale-dominated industrial zones like the Permian Basin, electrocoagulation systems especially when integrated with polyacrylamide (PAM)-based flocculants are increasingly deployed to treat high-TDS produced water, in line with EPA recommendations (600-R-20-006). Cooling water circuits are also transitioning to phosphate-free programs to meet REACH SVHC restrictions, with polymers like polyepoxysuccinic acid (PESA) and polyaspartic acid (PASP), dosed at 4–12 ppm, proving effective in scale inhibition at LSI values above 2.5.

Meanwhile, rising awareness about microplastics has prompted the integration of dissolved air flotation (DAF) with high-charge-density cationic polymers, achieving removal rates exceeding 85% for particles below 5 µm, consistent with ASCE 68-21 findings. As both public and private sectors face tightening environmental limits, the region’s water treatment chemicals market is rapidly being redefined by multifunctional, regulatory-compliant, and environmentally resilient chemistries.

Market Trend: Convergence of Sustainability and AI Redefines Water Treatment Chemistry in North America

The market is undergoing a transformation driven by the convergence of sustainability, regulatory compliance, and digital optimization. A growing shift toward PFAS-free and biodegradable chemistries such as Ecolab’s EnviroTru® BIO, currently operational at Denver’s Robert W. Hite wastewater plant is eliminating legacy toxics like alum while also reducing sludge production by up to 30%. In Canada, federal initiatives targeting single-use plastic bans are accelerating demand for plant-derived polymers in industrial scale control applications, particularly in energy and chemical manufacturing.

Simultaneously, AI-enabled water treatment platforms are optimizing chemical dosing in real time across sectors like power generation and food & beverage. These systems have shown reductions of up to 20% in chemical consumption, with payback periods of less than one year, while also supporting compliance with EPA's 2024 PFAS National Primary Drinking Water Regulations (NPDWR) and Canada’s CEPA Part 5. Advanced treatment programs are now emphasizing circular economy gains, such as struvite recovery (valued at ~$500/ton as a fertilizer feedstock), contributing both to revenue streams and to ESG performance. With PFAS-related fines potentially reaching $56,000/day, chemical suppliers are repositioning themselves as digital and ESG enablers offering integrated solutions that are safer, smarter, and scalable across utilities, industrial clusters, and data centers.

Growth Opportunity: Industrial Water Reuse and Critical Mineral Recovery Fuel Multi-Billion Dollar Chemical Demand

North America's water treatment chemicals market is capitalizing on two transformative megatrends: the push for industrial water reuse and the strategic recovery of critical minerals. Sectors like green hydrogen, lithium-ion battery recycling, and hyperscale data infrastructure are leading demand for ultra-pure water (UPW) solutions and novel reuse-enabling formulations. Siemens Energy’s HyPure™ ion exchange system, used in electrolyzer feedwater treatment, reduces regeneration cycles by up to 50%, improving system uptime in green hydrogen hubs like California’s Central Valley.

In battery recycling, Li-Cycle and other innovators are deploying proprietary chelating agents and metal-selective polymers to purify acidic lithium leachate, recovering over 90% of water for reuse and qualifying for IRA-linked sustainability credits. At the same time, Microsoft’s Zero Water Cooling initiative across its North American data centers demonstrates how Legionella-safe, non-toxic biocides can prevent contamination while saving more than 2 million gallons of water per facility annually.

These chemical solutions are not merely enabling compliance they are becoming essential for access to tax credits, ESG funding, and sustainable certification schemes. The U.S. Geological Survey (USGS) anticipates lithium demand to quadruple by 2030, while the Department of Energy’s Hydrogen Shot initiative pushes for $1/kg clean hydrogen by mid-decade. In this landscape, water treatment chemicals that facilitate resource recovery and operational circularity will command a strategic premium positioning this market for high-impact growth driven by innovation, policy alignment, and cross-sector value unlocking.

Competitive Landscape: Strategic Positioning in a Transforming Market

The North America water treatment chemicals market has a competitive structure that combines global reach, regional strength, and new digital developments. Big companies like Ecolab, Solenis, BASF, and Kemira dominate the market, holding about 55% of the market share. These firms act as full-service providers or technology specialists, offering complete water management services and innovative chemical solutions to meet increasing regulatory and environmental needs. Ecolab leads with an estimated 18% share, thanks to its IoT-enabled Nalco solutions and proprietary digital tools like the 3D TRASAR and Water Risk Monetizer. Solenis has established a strong second position in the industrial water treatment segment, recently growing its portfolio by acquiring Diversey’s chemical business and moving into closed-loop water reuse systems. BASF remains at the forefront of technology with sustainable, bio-based inhibitors under its GreenChemistry initiative, while Kemira maintains a strong presence in municipal water treatment, utilizing AI-powered coagulation dosing and securing a significant contract in Chicago that highlights its credibility in the municipal sector.

Regional players account for about 30% of the market. They focus on local delivery, low-cost chemicals, and personalized customer service to stand out in a price-sensitive market. USALCO, the largest blue alum producer in the U.S., has built its competitive strength through regional leadership in the Northeast and Midwest, allowing for quick supply and customer responsiveness. Chemtrade, a key producer of chlorine in Canada and the northern U.S., is increasingly focusing its operations on environmentally responsible production, while PVS Chemicals has become a leader in on-site chemical generation, especially valued for disaster response and emergency treatment contracts across the Great Lakes region.

A third group of market participants disruptive technology firms now makes up 15% of the market and is growing fast due to the need for digital integration and sustainability. Firms like AquaHawk, ClearAqua, and Fracta are creating AI- and ML-powered platforms that change how water utilities and industrial facilities manage leak detection, dosing precision, and asset management. AquaHawk recently closed a $20M Series B funding round and targets mid-sized utilities with its predictive analytics-based platforms. ClearAqua, supported by grants from the U.S. Department of Energy, is pioneering electrochemical treatment technologies for industrial water users, while Fracta, backed by Sequoia Capital, offers AI-driven pipe failure prediction solutions to municipalities.

From an application perspective, competition in municipal water treatment is becoming more intense, particularly in disinfection, coagulation, and corrosion control. The conversion to chloramine is speeding up, with chloramine-based systems expected to grow by 15% as utilities move away from free chlorine due to regulatory and taste issues. Organic polymers are gaining traction in coagulation, with a projected 20% CAGR, because they generate less sludge and have better environmental profiles than traditional alum. In corrosion control, lead service line replacements are driving demand for orthophosphates. The main areas of competition in municipal applications now focus on PFAS removal chemistry, smart infrastructure integration, and developing climate-resilient treatment chemicals.

In the industrial sector, companies differentiate themselves with solutions tailored to specific industries. In power generation, Ecolab and ChemTreat concentrate on cycle chemistry management. The food and beverage industry, which emphasizes hygiene, prefers sanitizers and biofilm control from BASF and Solenis. Suez and Veolia dominate ultra-pure water systems for pharmaceutical applications, while microelectronics manufacturers increasingly rely on Kurita and Entegris for ultrapure and nanoparticle-sensitive treatment solutions.

The competitive advantage is also being enhanced by new strategies that use digital transformation and sustainability. Ecolab’s PFAS destruction technology and its financial modeling tool, Water Risk Monetizer, show how digital tools are incorporated into chemical programs for better risk assessments. BASF has introduced a virtual plant operator that helps with real-time chemical dosing and performance optimization using AI. Similarly, AquaHawk’s leak-detection algorithms are being used by utilities aiming for predictive, rather than reactive, control systems. On the sustainability front, Kemira produces coagulants using biogas energy for carbon-neutrality, while Solenis is pursuing water circularity through recycling partnerships. BASF has further strengthened its position with a range of plant-derived, biodegradable chemical alternatives.

New business models are also changing how value is delivered. Ecolab’s Chemical-as-a-Service model through Nalco Water turns water treatment into a recurring revenue service. Solenis offers performance-based contracts linking chemical usage to measurable outcomes, allowing customers to share risk and savings. Xylem is taking this further with a Water Resilience-as-a-Service model designed to help cities and companies respond to climate-related water stress with bundled technologies and consulting services.

Looking ahead to 2025–2030, several trends are likely to transform the competitive landscape. Digital adoption is expected to reach 60% in the industrial segment as companies seek efficiency and real-time control. Green chemistry, currently a value-add, may capture over 35% of the market as regulations and customer preferences unify around non-toxic, sustainable formulations. Additionally, consolidation among regional players is probable, especially for those lacking digital capabilities or advanced environmental, social, and governance alignment. Success in this changing market will require companies to adopt integrated digital-chemical platforms, focus on regulatory-first innovation pipelines, embrace circular economy principles, and offer climate-resilient solutions as essential elements of their portfolios.

North America Water Treatment Chemicals Market – Segmentation Insights (2025–2034)

By Type of Chemical: Corrosion Inhibitors Lead, Membrane Cleaners Grow Fastest

In the North America water treatment chemicals market, corrosion and scale inhibitors are expected to dominate with a 2025 market share of approximately 29.1%, driven by their essential role in maintaining the integrity of aging pipelines, boilers, and cooling systems. The region’s industrial sectors including power generation, refineries, and manufacturing continue to rely on these inhibitors to prevent fouling and equipment degradation, especially in areas with hard water or high-salinity feedstocks. The demand is further boosted by retrofitting programs in older utilities and compliance with water quality standards that require optimized system performance.

Meanwhile, membrane cleaning chemicals are projected to be the fastest-growing category, with a CAGR of 6.1% through 2034, fueled by the widespread adoption of reverse osmosis (RO) and nanofiltration (NF) in both municipal and industrial sectors. As RO becomes integral for desalination, wastewater recycling, and ultrapure water systems, there is rising demand for effective membrane maintenance to prevent scaling, biofouling, and organic fouling. This trend is especially strong in U.S. water-scarce states like California and Arizona, where municipal reuse and industrial zero-liquid discharge initiatives are accelerating.

.png)

By Application: Industrial Sector Dominates, Municipal Demand Grows with PFAS Regulation

Industrial water treatment is projected to hold the largest market share at approximately 47.8% in 2025, driven by robust demand across oil & gas, energy generation, food processing, and chemical manufacturing. These sectors increasingly face regulatory pressure to optimize water usage and minimize environmental impact, pushing up demand for chemical solutions tailored to cooling towers, boilers, and process water streams. Complex chemistries for corrosion control, scaling prevention, and biofilm mitigation are becoming essential in process-intensive industries.

Municipal water treatment follows closely with an estimated 36.7% share, as utilities upgrade treatment systems to address contaminants like PFAS (per- and polyfluoroalkyl substances) and comply with stricter U.S. EPA rules including the Lead and Copper Rule Revisions (LCRR). Investment in advanced treatment infrastructure, including granular activated carbon and membrane systems, is driving growth in disinfectants, coagulants, and specialty formulations. The commercial segment covering hospitals, hospitality, and institutional buildings also maintains steady growth, with increased biocide demand for Legionella prevention in HVAC and water distribution systems.

North America Water Treatment Chemicals Report Scope

North America Water Treatment Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$19.3 Billion

|

|

Market Size (2034)

|

$28.9 Billion

|

|

Market Growth Rate

|

4.6%

|

|

Segments

|

By Type of Chemical (Coagulants and Flocculants, Corrosion and Scale Inhibitors, Biocides and Disinfectants, pH Adjusters and Softeners, Oxygen Scavengers, Defoamers and Antifoaming Agents, Membrane Cleaning Chemicals, Other Specialty Chemicals), By Application (Industrial Water Treatment, Municipal Water Treatment, Commercial Water Treatment), By End-User Industry (Refined from Applications) (Municipal (Water and Wastewater Utilities), Industrial), By Form of Chemical (Liquid, Powder/Solid, Gas

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ecolab Inc. (U.S.), Solenis LLC (U.S.), Kemira Oyj (Finland), SNF Holding Company (U.S.), BASF SE (Germany), Veolia Water Technologies (France), SUEZ Water Technologies and Solutions (France), The Dow Chemical Company (U.S.), Kurita Water Industries Ltd. (Japan), ChemTreat, Inc. (U.S.), Nouryon (The Netherlands), Buckman (U.S.)

|

|

Countries

|

US, Canada, Mexico

|

North America Water Treatment Chemicals Market Segmentation

By Type of Chemical

- Coagulants and Flocculants

- Corrosion and Scale Inhibitors

- Biocides and Disinfectants

- pH Adjusters and Softeners

- Oxygen Scavengers

- Defoamers and Antifoaming Agents

- Membrane Cleaning Chemicals

- Other Specialty Chemicals

By Application

- Industrial Water Treatment

- Cooling Water Treatment

- Boiler Water Treatment

- Process Water Treatment

- Industrial Wastewater Treatment

- Produced Water Treatment

- Water Reuse and Recycling

- Water Desalination

- Municipal Water Treatment

- Drinking Water Treatment

- Municipal Wastewater Treatment

- Commercial Water Treatment

By End-User Industry (Refined from Applications)

- Municipal (Water and Wastewater Utilities)

- Industrial

- Power Generation

- Oil and Gas

- Chemical Manufacturing

- Food and Beverage

- Pulp and Paper

- Mining and Metallurgy

- Pharmaceutical

- Electronics and Semiconductors

- Other Manufacturing Industries

By Form of Chemical

By Country

- United States

- Canada

- Mexico

Top Companies in North America Water Treatment Chemicals Market

- Ecolab Inc. (U.S.)

- Solenis LLC (U.S.)

- Kemira Oyj (Finland)

- SNF Holding Company (U.S.)

- BASF SE (Germany)

- Veolia Water Technologies (France)

- SUEZ Water Technologies and Solutions (France)

- The Dow Chemical Company (U.S.)

- Kurita Water Industries Ltd. (Japan)

- ChemTreat, Inc. (U.S.)

- Nouryon (The Netherlands)

- Buckman (U.S.)

* List Not Exhaustive

Research Coverage

This report investigates the North America Water Treatment Chemicals Market, delivering an in-depth analysis review of chemical categories such as corrosion and scale inhibitors, coagulants, membrane cleaners, biocides, and advanced formulations for PFAS and microplastics mitigation. It highlights breakthroughs in AI-driven dosing optimization, sustainable chemistries, and resource recovery technologies that are redefining municipal and industrial water treatment strategies. The study also reviews digital transformation trends and regulatory dynamics, providing actionable insights into ESG-driven procurement and emerging zero-liquid-discharge models. This report is an essential resource for utilities, industrial operators, and policymakers aiming to balance compliance, sustainability, and cost efficiency in water management. Published by USDAnalytics, this comprehensive study equips decision-makers with data-backed intelligence for navigating the fast-evolving North American water treatment chemicals landscape.

Key Research Details:

- Segmentation:

- By Type of Chemical: Coagulants & Flocculants, Corrosion & Scale Inhibitors, Biocides & Disinfectants, pH Adjusters & Softeners, Oxygen Scavengers, Defoamers & Antifoaming Agents, Membrane Cleaning Chemicals, Other Specialty Chemicals.

- By Application: Industrial Water Treatment (Cooling, Boiler, Process Water, Industrial Wastewater, Produced Water, Water Reuse, Desalination), Municipal Water Treatment (Drinking Water, Wastewater), Commercial Water Treatment.

- By End-User: Industrial (Power, Oil & Gas, Chemicals, Food & Beverage, Pulp & Paper, Mining, Pharmaceuticals, Electronics), Municipal Utilities.

- By Form: Liquid, Powder/Solid, Gas.

- Geographic Scope: North America (U.S., Canada, Mexico).

- Study Period: Historic data from 2021–2024 and forecast data from 2025–2034.

- Top Companies: Ecolab Inc., Solenis LLC, Kemira Oyj, SNF Holding Company, BASF SE, Veolia Water Technologies, SUEZ, The Dow Chemical Company, Kurita Water Industries, ChemTreat Inc., Nouryon, Buckman.

Methodology

USDAnalytics applies a structured methodology combining primary interviews with utilities, EPC contractors, and chemical suppliers, alongside secondary research from regulatory frameworks (EPA, ASTM, NSF), trade associations, and technical literature. Market sizing uses a bottom-up approach leveraging dosage norms, installed treatment capacities, and project pipelines across municipal and industrial sectors. Forecasting employs advanced statistical modeling that factors in CAPEX trends, regulatory shifts, ESG mandates, and digital adoption rates. Rigorous data triangulation ensures accuracy, while scenario analysis evaluates the impact of sustainability policies and PFAS regulations on market dynamics. This methodology guarantees actionable insights for stakeholders targeting long-term growth and compliance in the North American water treatment chemicals sector.

Deliverables

- Complete Market Research Report (PDF, Excel): data tables, market charts, and visual insights.

- Country-Level Forecasts & Analysis

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis

- Recent Developments & News Tracker

- Executive summary and key takeaway slides for boardroom presentations

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements