Market Analysis: Advanced Imaging, Strategic Acquisitions, and Radioisotope Innovation Drive the Nuclear Medicine Equipment Market

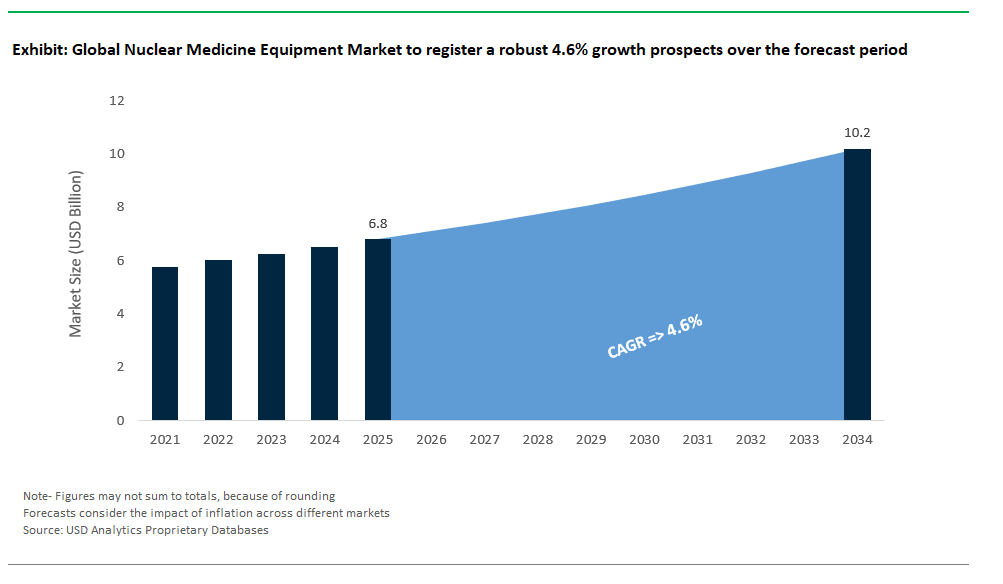

The Global Nuclear Medicine Equipment Market Size is estimated at $6.8 Billion in 2025 and is forecast to register an annual growth rate (CAGR) of 4.6% to reach $10.2 Billion by 2034.

The nuclear medicine equipment market is witnessing rapid advancements, driven by cutting-edge technology launches, strategic acquisitions, and growing collaborations across the globe. In May 2025, Hermes Medical Solutions introduced a suite of CE-marked tools designed for Selective Internal Radiation Therapy (SIRT) planning, featuring advanced segmentation, dose optimization, and multimodal image registration bringing new levels of precision to nuclear medicine procedures. This spirit of innovation is echoed by Siemens Healthineers, which strengthened its European leadership in molecular imaging and PET diagnostics by acquiring the molecular imaging business of Advanced Accelerator Applications (AAA) in December 2024. This acquisition bolsters Siemens’ portfolio in diagnostic radiopharmaceuticals and enhances its theranostics capabilities for targeted cancer care.

Strategic alliances and geographic expansions are further shaping the market’s landscape. In June 2024, Canon Medical Systems and Hermes Medical Solutions announced a key sales agreement to integrate and distribute Hermes’ vendor-neutral molecular imaging and dosimetry software, offering comprehensive solutions for nuclear medicine departments. Curium, another global radiopharmaceutical leader, expanded its presence in Turkey and neighboring regions by acquiring Eczacıbaşı-Monrol Nuclear Product Co. in April 2024, boosting its PET and SPECT infrastructure and accelerating the development of new radionuclides. Curium’s progress is also highlighted by the February 2024 acceptance of its PYLCLARI (18F-PSMA PET tracer) marketing application by Swissmedic, signaling a breakthrough in advanced prostate cancer imaging solutions.

Innovation in therapeutic radioisotopes and research partnerships is accelerating, with a focus on improving patient outcomes. In January 2024, Lantheus Holdings entered into strategic agreements with Perspective Therapeutics, obtaining an exclusive option for Pb212-VMT-α-NET, a clinical-stage alpha therapy targeting neuroendocrine tumors. The company’s commitment to imaging innovation is further seen in its February 2024 collaboration with the CLARiTI study, which will use Lantheus’ F18-labeled PET agent, MK-6240, to advance Alzheimer’s disease research. Meanwhile, Bayer AG signed a supply agreement with Ionetix in November 2023 for actinium-225 (Ac-225), ensuring a steady supply of this therapeutic radioisotope for developing targeted alpha therapies. Collectively, these developments reflect a vibrant and competitive nuclear medicine equipment market, characterized by high-value innovation, strategic growth, and a commitment to transforming diagnostic and therapeutic capabilities worldwide.

Technological Advancements in the Nuclear Medicine Equipment Market

Trend: Rise of Theranostic Cyclotrons for Alpha/Beta-Emitter Production

The nuclear medicine equipment market is undergoing a major transformation with the rising adoption of theranostic cyclotrons, specifically designed for localized production of alpha and beta-emitting isotopes. These compact systems are crucial for generating therapeutic isotopes like Actinium-225, which is essential in advanced cancer treatments such as PSMA-targeted therapies for prostate cancer. By enabling on-demand production, these cyclotrons support the industry’s shift toward personalized medicine, allowing for same-day preparation and administration of targeted radiopharmaceuticals. This not only improves patient outcomes but also enhances operational efficiency for healthcare providers by reducing dependency on distant production facilities.

Regulatory frameworks are accelerating this trend through fast-track approval programs for theranostic technologies, facilitating quicker deployment of new cyclotron systems across healthcare institutions. These initiatives are instrumental in addressing the growing global demand for therapeutic radiopharmaceuticals, especially as cancer incidence rises and precision oncology becomes mainstream. The combination of advanced cyclotron technology and favorable regulatory policies positions theranostic isotope production as a critical growth driver, enabling hospitals and imaging centers to deliver cutting-edge nuclear medicine therapies efficiently and reliably.

Opportunity: Modular Microreactors for On-Site Mo-99 Production

Modular microreactors represent a game-changing opportunity in nuclear medicine, particularly for the decentralized production of Molybdenum-99 (Mo-99), the parent isotope for Technetium-99m (Tc-99m) the most widely used diagnostic isotope in nuclear imaging. Historically, Mo-99 supply has been plagued by shortages due to reliance on aging, centralized reactors and complex international logistics. By enabling on-site or near-site production within hospitals or regional centers, modular microreactors can drastically improve supply chain stability, ensuring continuous availability of Tc-99m for critical diagnostic procedures.

The economic advantages of decentralized isotope production are equally compelling. Eliminating transportation and associated regulatory hurdles reduces operational costs and minimizes delays, leading to improved efficiency and lower per-patient imaging costs. Furthermore, the implementation of modular systems aligns with sustainability goals by reducing waste and improving safety through advanced reactor designs. As healthcare providers increasingly prioritize reliability and cost-effectiveness in nuclear imaging services, modular microreactors are poised to become a cornerstone technology, unlocking significant growth opportunities across the global nuclear medicine equipment market.

Competitive Landscape: Nuclear Medicine Equipment Market

The global nuclear medicine equipment market is being reshaped by the convergence of hybrid imaging systems, theranostics, and AI-powered diagnostic tools that support personalized treatment strategies. With rising adoption of SPECT/CT and PET/CT platforms, companies are focusing on faster scans, low-dose protocols, and improved anatomical-functional integration. Innovations in CZT detectors, automated workflows, and sustainability measures like reduced helium usage are becoming key differentiators. Leading manufacturers are accelerating development in precision imaging, AI-enabled reconstruction, and patient-centric design, positioning themselves to meet the growing demand for oncology, cardiology, and neurology imaging solutions.

Siemens Healthineers – Next-Generation PET/CT with AI-Enhanced Precision

Siemens Healthineers stands at the forefront of the nuclear medicine equipment market with its highly integrated portfolio of SPECT/CT and PET/CT systems under the Symbia and Biograph series. The company has been a key enabler of hybrid imaging trends, offering tools that combine functional and anatomical imaging for superior diagnostic accuracy. The Biograph Vision Quadra, a long axial field-of-view PET/CT scanner, delivers industry-leading sensitivity, facilitating faster scans, lower radiation doses, and dynamic whole-body imaging. Siemens is also leading in AI integration, with solutions that automate patient positioning, image reconstruction, and workflow orchestration through its syngo.via platform. In line with the shift toward precision oncology, the company is actively developing BIOGRAPH One, a next-generation PET/CT system aimed at extending capabilities in theranostics and research imaging. Sustainability is also embedded in Siemens’ strategy, with initiatives that target green imaging practices and improved energy efficiency in radiology departments. These advancements, combined with their expertise in oncology and image-guided therapies, firmly position Siemens Healthineers as a top-tier innovator in molecular imaging.

GE HealthCare – Pioneering CZT Technology and Deep Learning in SPECT/CT

GE HealthCare has cemented its leadership in nuclear medicine through its continuous evolution of CZT-based SPECT/CT systems and deep learning-enabled PET/CT technologies. With devices like StarGuide and NM/CT 870 CZT, GE is addressing the rising need for multi-tracer imaging and dynamic quantification, particularly in oncology and cardiovascular applications. Their Omni Legend PET/CT system showcases Precision DL, a deep learning-based reconstruction algorithm that enhances image clarity and quantification accuracy, enabling earlier disease detection and more accurate therapy response assessments. Their Xeleris AI platform plays a pivotal role in enabling real-time decision support and automated processing, helping improve diagnostic confidence and productivity. The company has also introduced dedicated cardiac imaging systems like MyoSPECT, tailored for advanced cardiovascular diagnostics. As theranostics gains traction globally, GE HealthCare is designing its systems to support dual-purpose diagnostic and therapeutic workflows, ensuring scalability and regulatory readiness. With a strong record of FDA approvals for AI-enabled systems and ongoing investment in quantitative imaging solutions, GE continues to lead the market through clinical impact and operational excellence.

Philips Healthcare – Digital PET and Enterprise Imaging for Precision Medicine

Philips Healthcare’s approach to nuclear medicine revolves around precision, digital transformation, and patient-centricity, anchored by innovations like the Vereos Digital PET/CT system. Utilizing fully digital Silicon Photomultiplier (SiPM) detectors, Vereos sets a new standard for sensitivity, quantitative accuracy, and low-dose performance across oncology, neurology, and cardiology applications. Their BrightView SPECT/CT further complements their nuclear imaging portfolio by delivering robust performance for multi-specialty clinical use. Philips' vision extends beyond hardware, with platforms like IntelliSpace Portal integrating advanced visualization, informatics, and AI-powered quantification tools to deliver actionable insights across diagnostic workflows. The company’s strategic direction is deeply rooted in enterprise imaging and interoperability, enabling a seamless exchange of imaging data across hospital systems. With their Future Health Index 2025 report emphasizing AI and telehealth integration, Philips is shaping the conversation around trust in AI-driven diagnostics and workforce sustainability. Their Circular Edition systems, part of a broader sustainability initiative, help reduce environmental impact without compromising performance, ensuring that Philips remains a responsible and forward-looking leader in molecular imaging.

Canon Medical – Mobile TOF PET and Workflow-Centric Innovation

Canon Medical is making strategic advancements in the nuclear medicine equipment space through its digital Time-of-Flight (TOF) PET/CT systems, exemplified by the Cartesion Prime SP Mobile Digital PET-CT. Known for compact design and transportability, this platform facilitates early disease detection and rapid clinical decision-making, particularly in oncology. Canon’s focus on workflow intelligence is reflected in its AI-powered automation tools that streamline scanning protocols, minimize human error, and optimize diagnostic pathways. Their recent launches in CT, such as the award-winning Aquilion ONE / INSIGHT Edition, incorporate features that are expected to be mirrored in PET/CT development, including AI-powered dose optimization and precision targeting. With a reputation for patient comfort and low-dose performance, Canon emphasizes a holistic imaging ecosystem that includes interventional guidance, multi-modality integration, and personalized care. The company's investments in clinical research, collaboration grants, and advanced post-processing ensure it remains a competitive force in the PET/CT modality while exploring avenues to enter the theranostics-enabled market segment.

United Imaging Healthcare – Total-Body PET and AI-First Molecular Imaging

United Imaging Healthcare is emerging as a global disruptor in the nuclear medicine market with its total-body PET/CT platform and AI-enhanced image processing technologies. The flagship uEXPLORER system, featuring a 2-meter axial field-of-view, enables ultra-fast, ultra-low-dose dynamic imaging of the entire body, redefining diagnostic and research capabilities. Building on this foundation, the newly launched uMI Panvivo and uMI Panorama GS PET/CT systems integrate precision imaging with AI-assisted acquisition and reconstruction, offering exceptional time-of-flight resolution (180 ps) and patient throughput. Their uAI Oncology Suite, CE-marked and FDA-cleared, provides automated lesion detection, segmentation, and quantification, assisting physicians in complex oncology cases. United Imaging is also addressing market gaps in accessibility by scaling PET/MR and PET/CT systems for high- and mid-tier hospitals, ensuring broader adoption of precision diagnostics. At ECR 2025 and EANM 2024, the company showcased its next-generation imaging innovations and sustainability-first product design, reinforcing its dual focus on technology differentiation and global market expansion. With strong academic collaborations and regulatory momentum, United Imaging is poised to transform nuclear medicine imaging standards worldwide.

Market Share and Segmentation Insights: Nuclear Medicine Equipment Market

By Product: SPECT Systems Lead, PET Systems Grow Fastest

Single-Photon Emission Computed Tomography (SPECT) systems hold the largest market share at 40.1% in 2025, owing to their cost-effectiveness, versatility, and dominant role in cardiac imaging for myocardial perfusion studies. Planar scintigraphy systems (gamma cameras) and ancillary devices like dose calibrators support basic nuclear medicine imaging needs but see slower adoption. Cyclotrons, although smaller in market share, are becoming increasingly relevant for on-site radioisotope production in advanced hospitals and research centers. Positron Emission Tomography (PET) systems represent the fastest-growing segment with a CAGR of 5.8%, driven by their critical role in oncology for accurate cancer detection and staging through FDG-PET and hybrid imaging solutions (e.g., PET/CT and PET/MRI).

.png)

By Application: Oncology Dominates, Driving PET Adoption

Oncology accounts for the largest market share at 44.5% in 2025, fueled by the rising global cancer burden and the shift toward personalized medicine using PET/CT scans for early detection and treatment monitoring. Cardiology remains a significant application area, particularly for SPECT-based myocardial perfusion imaging, which continues to be widely adopted for diagnosing coronary artery disease. Neurology applications are expanding with innovations like amyloid PET scans for Alzheimer’s disease and dopamine transporter imaging for Parkinson’s disease. Oncology also drives the fastest growth, with an estimated CAGR of 5.5%, as demand for precision imaging and radioisotope-based therapies accelerates across developed and emerging markets.

United States: Theranostics, AI Integration, and Advanced PET Imaging Lead U.S. Nuclear Medicine Equipment Market

The United States remains at the forefront of the nuclear medicine equipment market, driven by rapid innovation and early adoption of cutting-edge technologies. The country is a global leader in theranostics, an approach that combines diagnostic imaging, such as PET, with targeted radionuclide therapy. Industry analysis published by Elsevier in August 2024 predicts that by 2034, up to 60% of all nuclear medicine procedures in the U.S. will incorporate theranostic principles, indicating a substantial shift towards integrated, precision-guided care. This move is supported by the FDA’s robust regulatory framework, which continues to accelerate the market entry of new radiopharmaceuticals and imaging agents. A major example is Telix Pharmaceuticals’ Gozellix a PSMA-PET imaging agent approved in March 2025 and launched in June which offers extended shelf life and distribution flexibility for prostate cancer diagnostics.

AI and machine learning are rapidly transforming nuclear medicine in the U.S., with the FDA approving 191 new AI/ML-enabled medical devices in radiology in 2024 alone. Leading vendors such as GE HealthCare are also driving progress, evidenced by the May 2025 FDA clearance of the Clarify DL deep-learning reconstruction technology for bone SPECT imaging. This solution, alongside their StarGuide digital SPECT/CT platform, is setting new standards for noise reduction and image contrast. Meanwhile, companies like United Imaging Healthcare have expanded their PET/CT installations to cover over 70% of U.S. states, highlighting robust adoption by renowned institutions such as Yale and UC Davis. With a strong ecosystem of innovation, regulatory agility, and investment in theranostics and AI-powered solutions, the U.S. nuclear medicine equipment market continues to set global benchmarks for clinical excellence and technological advancement.

Germany: Strategic Acquisitions and AI-Driven Image Reconstruction Elevate Nuclear Medicine Sector

Germany is a powerhouse in the European nuclear medicine equipment market, with a strong focus on innovation, precision, and strategic growth. A landmark move was Siemens Healthineers’ acquisition of the molecular imaging business from Advanced Accelerator Applications (AAA) in December 2024, significantly strengthening its diagnostic radiopharmaceutical portfolio for PET imaging across Europe. German hospitals and research centers are at the vanguard of theranostics, leveraging advanced imaging and targeted therapy to address the rising burden of cancer and cardiovascular diseases. This integration of diagnosis and therapy is leading to earlier, more personalized interventions and better patient outcomes.

The German market is also witnessing significant advances in AI-powered image reconstruction, which are enhancing image clarity, reducing scan times, and minimizing radiation exposure for patients. Companies like United Imaging Healthcare are expanding their market footprint, having installed digital PET/CT systems in leading academic centers like Kliniken Essen-Mitte. Germany’s commitment to research and local production, combined with a highly skilled clinical and scientific community, ensures its ongoing leadership in both the adoption and development of next-generation nuclear medicine equipment.

Canada: Next-Generation PET/CT Technology and Cancer Research Define Canadian Nuclear Medicine Market

Canada’s nuclear medicine equipment market is experiencing transformative growth, driven by investments in next-generation PET/CT technology and advanced cancer research capabilities. In June 2025, BC Cancer and the University of British Columbia introduced the country’s first Quadra PET/CT scanner, offering the largest field of view among Canadian scanners, higher image quality, faster scans, and lower radiation doses. This system enables whole-body imaging from head to pelvis in a single scan, greatly improving patient throughput and diagnostic accuracy.

Beyond clinical use, this advanced technology will empower researchers to develop new radiopharmaceuticals for cancer therapy at lower doses and with unprecedented precision. Canada’s long-term commitment to nuclear medicine infrastructure is evident in British Columbia’s 10-Year Cancer Care Action Plan, which includes several additional PET/CT installations across new and expanding cancer centers. These efforts position Canada as a leader in both innovative equipment deployment and clinical research in the nuclear medicine space.

Japan: High-Resolution PET Systems and Collaborative R&D Expand Nuclear Medicine Capabilities

Japan is reinforcing its leadership in nuclear medicine equipment through a combination of domestic innovation and international research partnerships. In July 2025, Shimadzu Corporation launched its high-resolution PET system "PositView" for dementia diagnosis and research, showcasing Japan’s commitment to neurological and early-disease detection. Major players like Canon Medical Systems are also pioneering the development of photon-counting CT (PCCT) technology in collaboration with leading U.S. research institutions, enhancing hybrid imaging modalities that benefit nuclear medicine.

Japanese manufacturers maintain strong R&D pipelines focused on delivering systems with high precision, faster scan speeds, and improved patient comfort. United Imaging Healthcare has also made significant market inroads, further consolidating Japan’s position as a hub for advanced, high-end medical imaging. These innovations are underpinned by Japan’s broader strategic focus on precision medicine, digital health, and quality of care.

United Kingdom: Rising Cardiac Disease and AI-Powered Imaging Propel UK Nuclear Medicine Equipment Market

The United Kingdom is seeing rising demand for nuclear medicine equipment, primarily due to an increase in cardiac and circulatory disease prevalence impacting over 7.6 million people as reported by the British Heart Foundation in 2024. This drives the need for sophisticated SPECT and PET technologies to improve early detection and treatment planning. UK healthcare providers are increasingly adopting AI-powered quality control solutions to improve the accuracy and consistency of both diagnostics and therapeutic procedures.

Homegrown companies like Mirada Medical and LabLogic Systems are playing pivotal roles in developing molecular imaging software, image fusion, quantitative analysis tools, and workflow optimization systems for nuclear medicine departments. This combination of clinical demand, software innovation, and investment in advanced imaging technology ensures the UK market remains dynamic and responsive to the evolving needs of modern healthcare.

China: Domestic Innovation, AI-Enabled Devices, and R&D Investment Transform Chinese Nuclear Medicine Market

China’s nuclear medicine equipment market is surging, powered by a national focus on domestic innovation, high R&D spending, and government support for local manufacturing. United Imaging Healthcare, a Shanghai-based global leader, recorded CNY 10.3 billion in revenue and introduced over 140 innovative products globally in 2024, with a heavy emphasis on AI-enabled radiology devices. These technologies including over 20 FDA-approved AI devices are elevating the capabilities of Chinese nuclear medicine and radiology.

China’s expansion of molecular imaging centers and procurement of PET/CT and SPECT/CT systems reflects a commitment to meeting the growing needs for advanced diagnostics in cancer, neurology, and cardiology. With ongoing public and private investment and an emphasis on regulatory self-sufficiency, China is poised to become a global powerhouse not only in manufacturing but also in the innovation of nuclear medicine equipment.

India: Infrastructure Expansion and “Make in India” Initiatives Drive Nuclear Medicine Equipment Growth

India’s nuclear medicine equipment market is on an upward trajectory, propelled by government-backed investments in both nuclear energy and healthcare infrastructure. The 2025-26 Union Budget’s target for expanding nuclear power signifies a national commitment to nuclear technology, which is expected to benefit medical imaging and treatment. The proliferation of nuclear medicine departments in major hospitals is a direct response to the increasing prevalence of non-communicable diseases, particularly cancer and cardiovascular conditions.

United Imaging Healthcare is rapidly growing its market share in India, supported by a shift toward local manufacturing and skills development through the “Make in India” initiative. These efforts aim to boost the domestic production of high-end medical equipment and build a skilled workforce in nuclear medicine technology, reinforcing India’s ambitions to become a regional leader in this critical healthcare sector.

Switzerland: Compact Brain PET Innovation and Accessible Diagnostics Elevate Swiss Nuclear Medicine Market

Switzerland stands out for pioneering compact and affordable nuclear medicine imaging technologies, exemplified by Positrigo’s NeuroLF® brain PET system. Having secured both CE Mark and FDA clearance by October 2024, NeuroLF is the world’s first ultra-compact PET scanner dedicated to brain imaging and is designed to assist in the diagnosis and monitoring of Alzheimer’s and other brain disorders. Its reduced size and cost aim to democratize access to high-quality brain PET imaging for hospitals and clinics that could not previously afford full-scale systems.

Switzerland’s strong ecosystem for medical device innovation is supported by government and European Innovation Council funding, fostering the rapid development, testing, and commercialization of next-generation nuclear medicine equipment. As amyloid PET imaging for Alzheimer’s is set to enter a historic growth phase, Swiss companies like Positrigo are well positioned to support the evolving needs of neurology and nuclear medicine communities across Europe and beyond.

Nuclear Medicine Equipment Market Report Scope

Nuclear Medicine Equipment Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$6.8 Billion

|

|

Market Size (2034)

|

$10.2 Billion

|

|

Market Growth Rate

|

4.6%

|

|

Segments

|

By Product (Single-Photon Emission Computed Tomography (SPECT) Systems, Positron Emission Tomography (PET) Systems, Planar Scintigraphy Systems (Gamma Cameras), Cyclotrons, Dose Calibrators & Other Ancillary Equipment), By Application (Oncology, Cardiology, Neurology, Endocrinology, Orthopedics & Pain Management, Other Applications), By End User (Hospitals, Diagnostic Imaging Centers, Academic & Research Institutes, Specialized Radiopharmacies)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Siemens Healthineers AG, GE HealthCare, Koninklijke Philips N.V., Curium, Cardinal Health Inc., Lantheus Holdings, Inc., Eckert & Ziegler AG, Mediso Ltd., Advanced Accelerator Applications (a Novartis company), Bracco Imaging S.p.A., Fujifilm Holdings Corporation, Canon Medical Systems Corporation, Neusoft Medical Systems Co., Ltd., Biodex Medical Systems Inc., DDD-Diagnostic A/S, Digirad Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Nuclear Medicine Equipment Market Segmentation

By Product

- Single-Photon Emission Computed Tomography (SPECT) Systems

- Positron Emission Tomography (PET) Systems

- Planar Scintigraphy Systems (Gamma Cameras)

- Cyclotrons

- Dose Calibrators & Other Ancillary Equipment

By Application

- Oncology

- Cardiology

- Neurology

- Endocrinology

- Orthopedics & Pain Management

- Other Applications

By End User

- Hospitals

- Diagnostic Imaging Centers

- Academic & Research Institutes

- Specialized Radiopharmacies

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Nuclear Medicine Equipment Market

- Siemens Healthineers AG

- GE HealthCare

- Koninklijke Philips N.V.

- Curium

- Cardinal Health Inc.

- Lantheus Holdings, Inc.

- Eckert & Ziegler AG

- Mediso Ltd.

- Advanced Accelerator Applications (a Novartis company)

- Bracco Imaging S.p.A.

- Fujifilm Holdings Corporation

- Canon Medical Systems Corporation

- Neusoft Medical Systems Co., Ltd.

- Biodex Medical Systems Inc.

- DDD-Diagnostic A/S

- Digirad Corporation

* List Not Exhaustive

Research Coverage

The Nuclear Medicine Equipment Market report by USDAnalytics delivers a comprehensive analysis of global market sizing, CAGR, and value projections, while offering in-depth coverage of market dynamics, innovation drivers, and recent developments. The study highlights landmark advancements, such as Siemens Healthineers’ acquisition of AAA, Hermes Medical’s SIRT planning tools, Canon Medical’s workflow-centric PET/CT systems, and Curium’s regional expansion in PET and SPECT infrastructure. Regulatory accelerators, AI-powered imaging, and modular microreactors for isotope production are also covered, underscoring the market’s rapid transformation.

Segmentation includes product types (SPECT systems, PET systems, planar scintigraphy/gamma cameras, cyclotrons, ancillary equipment), applications (oncology, cardiology, neurology, endocrinology, orthopedics & pain management, other clinical uses), and end users (hospitals, diagnostic imaging centers, academic/research institutes, specialized radiopharmacies). The competitive landscape section profiles Siemens Healthineers, GE HealthCare, Philips, Curium, Cardinal Health, Lantheus Holdings, Eckert & Ziegler, Canon Medical, United Imaging Healthcare, Mediso, and other industry leaders, covering strategic partnerships, R&D, and geographic expansion.

The report covers historical data from 2021–2024 and provides forecasts from 2025–2034. Geographic coverage spans North America (US, Canada, Mexico), Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia), South America (Brazil, Argentina, Rest of South America), and Middle East & Africa (Saudi Arabia, UAE, South Africa, Egypt, Rest of Africa).

This report is designed for industry professionals, healthcare providers, manufacturers, and investors delivering actionable insights into growth drivers, regulatory changes, competitive positioning, and future opportunities across the global nuclear medicine equipment sector.

Deliverables:

- Full Market Research Report (PDF, Excel): Complete data tables, market charts, and visual insights.

- Country-Level Forecasts & Analysis.

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis.

- Recent Developments & News Tracker

- Executive Summary & Analyst Insights.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.