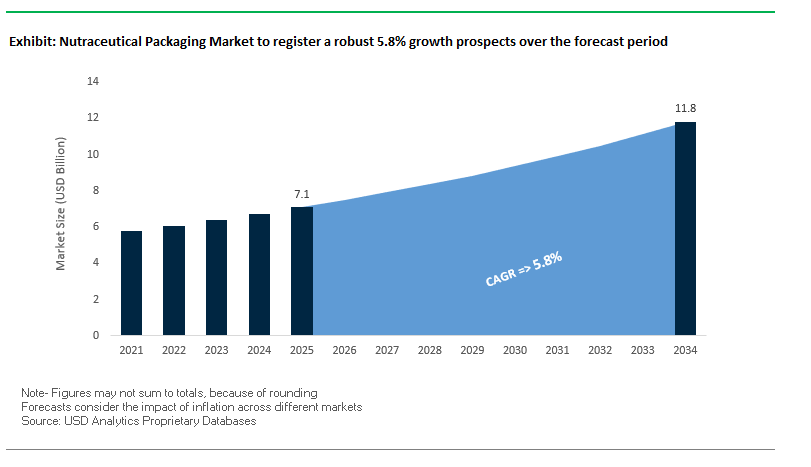

Nutraceutical Packaging Market Set to Reach $11.8 Billion by 2034 at 5.8% CAGR

The global nutraceutical packaging market is projected to grow from $7.1 billion in 2025 to $11.8 billion by 2034, reflecting a CAGR of 5.8%. Growth is driven by increasing consumer demand for high-quality, safe, and sustainable nutraceutical products, as well as innovations in rigid and flexible packaging formats that preserve potency and ensure product authenticity. The industry is increasingly adopting eco-friendly packaging materials, tamper-evident features, and connected technologies, aligning with stringent regulatory requirements and evolving market expectations.

Key Insights for Industry Professionals:

- Protecting product integrity: Packaging innovations prevent exposure to moisture, oxygen, and UV light, maintaining stability and efficacy of dietary supplements, powders, and herbal formulations.

- Rigid packaging dominance: Bottles and blister packs, particularly in HDPE and PET, remain preferred formats for dosing convenience and barrier protection.

- Safety and security focus: Tamper-evident seals, child-resistant closures, QR codes, and digital watermarks ensure authenticity and enhance consumer trust.

- Sustainable material adoption: Transition to recycled plastics (PCR) and paper-based alternatives reduces environmental footprint while complying with regulatory mandates.

- Integration of smart packaging: Digital touchpoints such as NFC tags and QR codes provide consumer engagement and anti-counterfeiting capabilities.

Market Analysis: Recent Industry Developments Shaping Nutraceutical Packaging Innovation

The nutraceutical packaging industry has seen strategic moves and technological innovations aimed at enhancing product safety, sustainability, and consumer engagement. In September 2025, Siegwerk showcased its circular packaging innovations at a flexible packaging summit, emphasizing sustainable solutions tailored for the nutraceutical sector. Graphic Packaging International launched the PaperSeal® Pressed MAP Tray in August 2025, reducing plastic use by up to 85% in modified atmosphere packaging applications, relevant to nutraceutical powders and tablets.

In the same month, Mondi ramped up production of its FunctionalBarrier Paper Ultimate, an ultra-high barrier paper solution providing an alternative to conventional plastics. In July 2025, Gerresheimer AG refocused on growth after ending potential takeover discussions, highlighting its commitment to biologics and nutraceutical systems. Additionally, Constantia Flexibles expanded its portfolio with the acquisition of a majority stake in Aluflexpack, reinforcing its position in food, beverage, and pharma packaging markets.

Earlier initiatives include Keystone Folding Box’s paperboard blister for medical tablets in June 2025, Berry Global’s lightweight protein powder packages in April 2025, and Gerresheimer’s Connected Packaging platform debut at Paris Packaging Week in January 2025, integrating QR codes and NFC tags for consumer engagement and anti-counterfeiting measures.

Trends and Opportunities Transforming the Nutraceutical Packaging Market

Accelerated Adoption of Integrated Anti-Counterfeiting and Serialization Technologies

The nutraceutical packaging market is witnessing a rapid shift toward advanced anti-counterfeiting and serialization solutions as counterfeit supplements and vitamins threaten consumer safety and brand credibility. With counterfeit seizures in the U.S. alone surpassing $2 billion in 2022, including over $20 million in counterfeit drugs, the urgency for robust packaging security features has never been greater. Inspired by pharmaceutical models such as the EU Falsified Medicines Directive (FMD)—which mandates 2D barcodes and anti-tamper devices—nutraceutical companies are proactively adopting similar track-and-trace technologies. By implementing serialization and unique identifiers, brands are not only preparing for potential regulatory expansion but also strengthening consumer trust in product authenticity. Corporate initiatives are also driving momentum: in October 2022, Gerresheimer and Merck collaborated on a “digital twin” packaging solution that assigns each unit a unique digital ID for full lifecycle traceability. Similarly, Covectra’s StellaGuard smart label provides mobile-based authentication, empowering consumers to verify product legitimacy instantly. These developments are positioning serialization as a competitive necessity in nutraceutical packaging, turning packaging into a frontline defense against counterfeiting.

Strategic Material Science Shift Towards Post-Consumer Recycled (PCR) and Marine Plastics

Sustainability imperatives are reshaping material sourcing strategies in nutraceutical packaging, with post-consumer recycled (PCR) and marine plastics taking center stage. Global leaders are setting ambitious recycled content goals, with PepsiCo incorporating 15% recycled plastic in primary packaging as of 2024, and targeting 40% or higher recycled content by 2035. This trend is not limited to beverages but extends to their nutraceutical brands, showcasing the cross-portfolio push for circularity. Companies such as K.P. Films are pioneering the use of Prevented Ocean Plastic (POP) in blister films, preventing over 3,600 tons of plastic from entering oceans—a quantifiable impact that strengthens brand sustainability credentials. On the regulatory front, the momentum is undeniable: by August 2024, five U.S. states had passed minimum PCR content laws, mandating between 15% and 50% recycled plastic in packaging. This dual force of regulatory push and corporate sustainability commitment is making PCR content a baseline expectation rather than a voluntary initiative. At the same time, advances in resin processing are improving the quality and availability of recycled plastics, ensuring that functional and aesthetic performance is not compromised.

Development of High-Barrier, Monomaterial Flexible Pouches

One of the most significant opportunities in nutraceutical packaging lies in the development of high-barrier, mono-material flexible pouches for powders, tablets, and soft gels. The industry’s reliance on multi-layer laminates creates recycling challenges, as most cannot be processed in existing infrastructure. By shifting toward all-PE or all-PP structures, manufacturers can unlock recyclability without compromising barrier properties against moisture and oxygen. Innovations from companies like Toppan have already demonstrated that mono-material packaging can maintain product integrity while achieving end-of-life recyclability. Collaborative efforts, such as those led by Mondi Group, have resulted in NIR-recognizable pouches optimized for recycling streams, ensuring circularity without disrupting functionality. For nutraceutical brands, adopting mono-material pouches not only enhances sustainability credentials but also reduces compliance risks as more regions implement extended producer responsibility (EPR) laws. This evolution addresses one of the sector’s critical sustainability gaps and positions brands to lead in eco-friendly, high-performance flexible packaging.

Integration of Smart Labels for Dose Compliance and Personalization

The convergence of nutraceutical packaging with digital health and IoT technologies represents another game-changing opportunity. Smart labels and NFC-enabled caps are evolving packaging from a passive container to an active compliance and engagement tool. These technologies help track supplement intake, providing real-time data that can improve consumer adherence—a challenge well-documented in clinical trials for pharmaceuticals. By linking QR codes or NFC tags to mobile apps, brands can deliver personalized dosage instructions, product authentication, and digital health content, deepening consumer trust and engagement. This personalization is particularly relevant in nutraceuticals, where consumers often seek tailored solutions for wellness. Moreover, healthcare providers and insurers are beginning to recognize the value of such adherence-tracking technologies, opening pathways for nutraceuticals to be integrated into preventive health strategies. For brands, the adoption of smart packaging not only supports better consumer outcomes but also differentiates products in a crowded market by offering value-added digital health functionality.

Competitive Landscape of Global Nutraceutical Packaging Market

The nutraceutical packaging market is highly competitive, with leading players focusing on high-barrier protection, sustainability, and connected technologies. Companies are innovating in rigid and flexible packaging, tamper-evident features, and smart packaging solutions, catering to growing consumer and regulatory demands.

Amcor plc: Innovating Recyclable and High-Barrier Packaging Solutions

Amcor offers high-barrier films for stick packs and sachets, recycle-ready blister systems, and paper-based solutions for vitamins and supplements. In April 2025, it introduced the AmSky™ recyclable polyethylene-based thermoform blister, a major innovation for the nutraceutical and healthcare sectors. Amcor combines advanced material science with sustainability, delivering lightweight, recyclable, and high-barrier packaging for environmentally conscious consumers. Its portfolio includes the HealthCare™ AmSky™ Blister System and High-Shield Pharma Laminates, designed for carbon reduction and recyclability.

Gerresheimer AG: Pioneering Connected and Sustainable Packaging

Gerresheimer specializes in primary packaging glass and plastic solutions for nutraceuticals, including bottles, jars, and containers for powders, liquids, and solids. In January 2025, the company showcased its Connected Packaging platform, integrating QR codes and NFC tags for personalized engagement and anti-counterfeiting. Gerresheimer focuses on sustainable materials, such as sugarcane-based plastics, while ensuring compliance with global production and regulatory standards.

Constantia Flexibles: Leading High-Barrier Flexible Packaging Innovations

Constantia Flexibles provides high-barrier films, foils, and laminates for blister packs, pouches, and sachets. In August 2025, it expanded its portfolio following the Aluflexpack acquisition, and earlier in January 2025, received the WorldStar Global Packaging Award for EcoPeelCover and EcoLamHighPlus. The company emphasizes sustainable, mono-material, and aluminum-free solutions, catering to nutraceutical tablets, capsules, powders, and gels with heat- and pressure-resistant flexible packaging.

Huhtamaki Oyj: Driving Circularity in Flexible Nutraceutical Packaging

Huhtamaki offers a variety of films, laminates, and pouches with a growing focus on nutraceuticals. In July 2025, it launched recyclable and compostable packaging solutions, reinforcing its commitment to circularity and sustainability. Its blueloop™ brand represents eco-friendly flexible packaging, aligning with the company’s 2030 sustainability strategy.

CCL Industries Inc.: Advanced Labeling and Smart Packaging Solutions

CCL Industries, through CCL Healthcare, provides innovative labeling and packaging for nutraceuticals, including pressure-sensitive labels, folding cartons, and specialty packaging. Leveraging a global network of 43 cGMP-compliant facilities, the company offers smart packaging solutions with RFID, NFC, and 2D barcodes for authentication and supply chain security. CCL’s solutions combine brand promotion, product safety, and regulatory compliance for global nutraceutical brands.

Nutraceutical Packaging Market Share Insights

Tablets and Capsules Lead Market Share by Nutraceutical Form in the Nutraceutical Packaging Industry

Tablets and capsules dominate the nutraceutical packaging market with 55% share in 2025, reflecting their unmatched stability, convenience, and consumer trust. Packaging for this segment is concentrated in HDPE and PP bottles with tamper-evident seals and desiccant integration to protect potency, alongside the rising use of blister packs that enhance compliance, portability, and pharmaceutical-grade positioning. Powders hold 20% share, largely protein powders and meal replacements, requiring high-barrier multilayer pouches with zippers and scoops to protect against moisture and clumping. Sustainability is a defining driver here, with a transition towards monomaterial PE-based recyclable pouches with barrier coatings. Liquids, accounting for 15% share, are packaged primarily in amber glass bottles and UV-inhibited PET bottles, balancing premium presentation with protection against oxidation and nutrient loss. Gels hold 5% share, with softgels and gel shots relying on blister packs and HDPE bottles for stability. The remaining 5% share is from emerging forms like gummies and effervescent tablets, requiring specialized moisture-barrier tubs and pouches to protect texture and prevent microbial growth in this fast-growing niche.

Dietary Supplements Hold the Largest Share by Application in the Nutraceutical Packaging Industry

Dietary supplements account for 50% of nutraceutical packaging demand in 2025, making them the foundation of the industry. This segment is defined by strict regulatory compliance, with packaging designed to ensure potency, safety, and consumer trust, typically through HDPE bottles, PET bottles, and blister packs with tamper-evidence and UV protection. Sports nutrition, with 20% share, is highly brand-driven, using large-format foil pouches, single-serve sachets, and durable shaker bottles that reinforce active lifestyle positioning while delivering functional portability. Functional foods hold 15% share, where packaging requirements go beyond conventional food packaging to incorporate enhanced barriers protecting probiotics, vitamins, and bioactive compounds in cereals, bars, and dairy products. Functional beverages, at 10%, leverage PET bottles, aluminum cans, and amber glass to protect sensitive live cultures in probiotics while aligning with recyclability mandates. Herbal extracts, a premium niche representing 5% share, are dominated by amber glass dropper bottles, valued for their inertness and precision dosing. Across applications, the nutraceutical packaging market is shaped by the dual imperatives of regulatory compliance and sustainability, making innovation in recyclable, tamper-proof, and barrier-optimized formats central to maintaining consumer confidence.

United States: Smart and Sustainable Packaging Transform Dietary Supplement Delivery

The United States nutraceutical packaging market is navigating a complex regulatory environment, with oversight from the FDA ensuring accurate labeling and safety compliance. State-level Extended Producer Responsibility (EPR) laws further drive the adoption of recyclable and high-recycled-content materials, positioning sustainability as a key differentiator.

Technological advancements are redefining the sector through smart packaging solutions, including NFC and RFID-enabled bottles, which provide dosage reminders, authenticity verification, and consumer education via connected apps. Robotics and automation in dispensing and filling improve accuracy and operational efficiency. Corporate investments, such as Berry Global Inc.’s launch of fully recyclable clarified polypropylene (PP) bottles, demonstrate a commitment to eco-friendly nutraceutical packaging. Key applications include dietary supplements, functional foods, and beverages, where tamper-evident and child-resistant packaging enhances safety and consumer trust, particularly in e-commerce channels.

Germany: Regulatory Compliance and Circular Economy Principles Drive Advanced Packaging

Germany’s nutraceutical packaging market is heavily influenced by the EU Packaging and Packaging Waste Regulation (PPWR), effective in early 2025, which enforces ambitious recyclability and recycled content targets. This encourages the adoption of mono-material designs and returnable systems. Germany’s deposit-return system for containers also supports sustainable packaging practices.

German manufacturers are leveraging advanced materials, automated packaging systems, and R&D expertise to meet complex nutraceutical requirements. For instance, SIRIO Pharma’s €16 million investment in a fully automated facility underscores the commitment to precision and efficiency. The country’s strong circular economy infrastructure and the Green Dot system incentivize sustainable production. Key applications include geriatric care products and functional foods, where convenient formats like stick packs and resealable pouches cater to health-conscious consumers seeking on-the-go solutions.

China: Government Support and E-Commerce Growth Accelerate Premium Packaging Adoption

China’s nutraceutical packaging market benefits from government initiatives supporting high-end manufacturing and regulatory oversight from the National Medical Products Administration (NMPA). Recent guidelines for pharmaceutical and excipient packaging also extend to nutraceuticals, requiring a comprehensive quality management system.

Manufacturers are investing in automation, AI, and domestic high-quality production facilities to meet rising demand in the e-commerce and food processing sectors. Consumer trends favor premium and functional products, driving demand for innovative, visually appealing, and sustainable packaging formats. The combination of government support, technological innovation, and expanding online retail channels positions China as a rapidly growing market for smart and eco-friendly nutraceutical packaging.

India: Policy Initiatives and VC Investments Spur Growth in Sustainable Packaging

India’s nutraceutical packaging market is propelled by Make in India and the Production Linked Incentive (PLI) scheme, which encourage domestic manufacturing and investment in recyclable, circular-economy-aligned packaging solutions. The Food Safety and Standards (Health Supplements, Nutraceuticals, Food for Special Dietary Use) Regulations, 2022 provide clear labeling and packaging guidelines for nutraceuticals.

Technological adoption is increasing, exemplified by Ahlstrom and The Paper People’s fiber-based, food-safe packaging, adaptable to nutraceutical products. Venture capital investments in the sector have surged 2.5x between 2020–2023, funding innovation in both product and packaging development. Key applications include dietary supplements, functional foods, vitamins, and probiotics, with packaging playing a pivotal role in brand differentiation, product protection, and consumer convenience across retail and online channels.

Japan: Regulatory Oversight and Eco-Friendly Innovations Strengthen Market Leadership

Japan’s nutraceutical packaging sector is governed by a well-defined regulatory framework for Foods with Health Claims, with oversight by the MHLW and Consumer Affairs Agency. Packaging must meet safety, efficacy, and quality standards, influencing design and material choices.

Technological innovations focus on durable, functional, and environmentally sustainable packaging, with advanced coatings and finishes enhancing protection and aesthetics. Initiatives such as Suntory Group’s 2R+B (Reduce, Recycle + Bio) strategy to achieve 100% sustainable PET bottles by 2030 highlight the integration of eco-conscious practices across the supply chain, including nutraceuticals. The market is driven by Japan’s aging population, necessitating convenient and protective packaging that preserves product efficacy by shielding supplements from moisture, light, and other degrading factors.

Nutraceutical Packaging Market Report Scope

Nutraceutical Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$7.1 Billion

|

|

Market Size (2034)

|

$11.8 Billion

|

|

Market Growth Rate

|

5.8%

|

|

Segments

|

By Packaging Type (Bottles & Jars, Bags & Pouches, Blister Packs, Stick Packs, Cans), By Material (Plastic, Glass, Metal, Paper & Paperboard), By Nutraceutical Form (Tablets & Capsules, Powders, Liquids, Gels, Others), By Application (Dietary Supplements, Functional Foods, Functional Beverages, Sports Nutrition, Herbal Extracts)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Berry Global Inc., WestRock Company, Huhtamaki Oyj, Sonoco Products Company, AptarGroup, Inc., Mondi Group, Gerresheimer AG, Constantia Flexibles, International Paper Company, SGD Pharma, TCPL Packaging, Keystone Folding Box Co., TricorBraun LLC, Comar, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Nutraceutical Packaging Market Segmentation

By Packaging Type

- Bottles & Jars

- Bags & Pouches

- Blister Packs

- Stick Packs

- Cans

By Material

- Plastic

- Glass

- Metal

- Paper & Paperboard

By Nutraceutical Form

- Tablets & Capsules

- Powders

- Liquids

- Gels

- Others

By Application

- Dietary Supplements

- Functional Foods

- Functional Beverages

- Sports Nutrition

- Herbal Extracts

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Nutraceutical Packaging Market

- Amcor plc

- Berry Global Inc.

- WestRock Company

- Huhtamaki Oyj

- Sonoco Products Company

- AptarGroup, Inc.

- Mondi Group

- Gerresheimer AG

- Constantia Flexibles

- International Paper Company

- SGD Pharma

- TCPL Packaging

- Keystone Folding Box Co.

- TricorBraun LLC

- Comar, Inc.

* List Not Exhaustive

Methodology

USDAnalytics employs a robust and multi-faceted research methodology to provide actionable insights into the global nutraceutical packaging market. Our approach integrates primary research, including interviews with packaging engineers, regulatory specialists, sustainability managers, and supply chain experts, with secondary research derived from corporate filings, industry publications, patent analysis, and regulatory documents. Market sizing and forecasts are based on historical trends, adoption rates of sustainable materials such as post-consumer recycled (PCR) plastics, marine plastics, and paper-based alternatives, as well as innovations in high-barrier flexible pouches, bottles, blister packs, and connected packaging solutions. USDAnalytics evaluates technological advancements, including anti-counterfeiting measures, serialization, NFC-enabled smart labels, and digital watermarks, while considering regional regulations such as the EU Packaging and Packaging Waste Regulation (PPWR), U.S. FDA standards, and country-specific mandates for recyclability and safety. Competitive intelligence focuses on strategic initiatives, acquisitions, and product innovations by key players such as Amcor, Gerresheimer AG, Constantia Flexibles, Huhtamaki Oyj, and CCL Industries, highlighting their sustainable, high-performance, and digitally enabled packaging solutions. This methodology ensures USDAnalytics delivers professional-grade, data-driven insights to help industry stakeholders optimize product protection, consumer engagement, and regulatory compliance in nutraceutical packaging.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.