Market Overview: Optical Films Are Becoming Yield, Power, and Form-Factor Enablers for the Display Industry

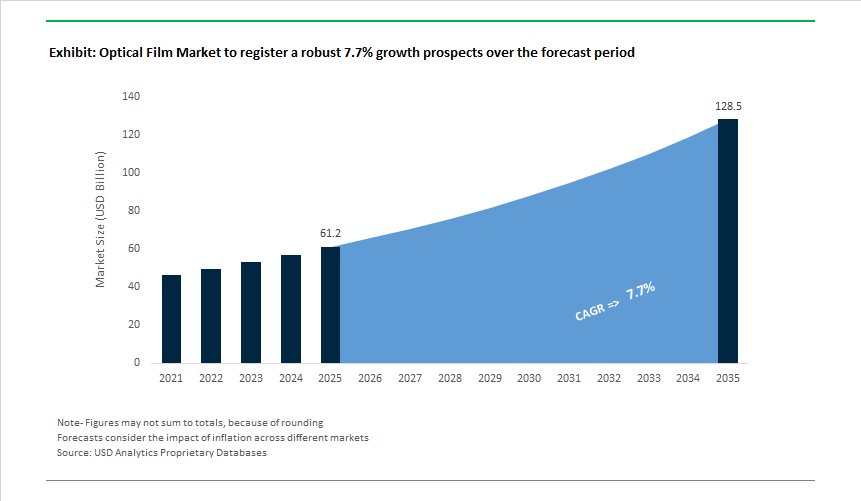

The Optical Film Market is valued at USD 61.2 billion in 2025 and is projected to reach USD 128.5 billion by 2035, expanding at a 7.7% CAGR as display manufacturers shift from pixel-centric innovation to system-level optical optimization. In mature display technologies where panel resolution gains are incremental, optical films increasingly determine brightness efficiency, device thickness, outdoor readability, durability, and manufacturing yield-making them strategic components rather than interchangeable consumables.

Growth is anchored in the economics of luminance and power efficiency. Brightness Enhancement Films (BEFs) enable axial luminance improvements of up to ~30%, allowing panel makers and device OEMs to either lower backlight power consumption or deliver higher peak brightness without increasing energy draw. This directly supports battery-life extension in smartphones, tablets, and laptops, while reducing thermal load in large-format TVs and monitors. As energy efficiency standards tighten globally, BEFs and related light-management films function as power-saving tools embedded at the optical stack level.

At the same time, form-factor pressure is reshaping polarizer and protective film design. Polarizer thickness reduction-from roughly ~200 µm toward ~130 µm-is enabling thinner, lighter devices without sacrificing contrast or color performance. This trend is particularly pronounced in premium mobile devices and OLED panels, where stack height and mechanical flexibility are tightly constrained. Anti-glare (AG) and anti-reflection (AR) films further enhance perceived display quality by improving outdoor visibility and reducing eye strain, attributes that increasingly influence consumer purchasing decisions even when underlying panel specifications are similar.

Flexible and foldable displays represent a structurally different demand driver. Here, optical films must maintain optical clarity, adhesion, and mechanical integrity under extreme cyclic strain, with next-generation films engineered to preserve >99% transparency after hundreds of thousands of folding cycles. These requirements elevate material science, coating uniformity, and adhesion chemistry to qualification gates, lengthening supplier lock-in once a film system is approved for a device platform.

From a competitive standpoint, margin resilience depends on differentiation above raw polymer inputs. Volatility in key feedstocks such as PVA and TAC-evidenced by significant price movement over recent years-has pushed film suppliers to emphasize value-added layers and functional integration, including optical adhesives, modified optical films (MOFs), and cyclo-olefin polymer (COP) substrates. Suppliers able to deliver system-level performance gains, manufacturing compatibility, and stable long-term supply are best positioned as display OEMs prioritize yield, power efficiency, and platform continuity over lowest-cost sourcing.

Market Analysis: Recent Product Launches, Capacity Moves and Technology Pivots

The last 18 months have been characterised by product innovation targeting next-generation displays and capacity reallocation toward high-value segments. In March 2025, Zeon Corporation completed a USD 50 million COP film capacity expansion (ZeonorFilm®) to serve large automotive displays and medical screens, reflecting upstream material substitution away from cellulose acetate toward cyclo olefin polymers for superior dimensional stability and near-glass transparency. March 2025 also saw Toray Industries launch a UV-blocking protective film for outdoor signage ( >99.9% UV filtration, >7-year durability), which directly addresses outdoor readability and lifetime issues for transit and retail signage.

Throughout 2025 the push toward flexible, MicroLED and automotive applications accelerated. June 2025 brought a high-profile research collaboration (Sumitomo Chemical / Institute of Science Tokyo) aimed at ultra-low power display films, signalling upstream materials R&D to cut display energy budgets. September 2025 Nitto Denko declared a technology focus on ultra-thin optical adhesives for AR/VR bonding (<1 µm), a response to the critical optical-distortion tolerance demanded by headset optics. October-November 2025 LG Display and LG Chem demonstrated a next-gen OLED panel using a customised flexible polarizer (Oct 2025) while LG Chem announced a production capacity ramp for advanced polarizer film (Nov 2025) - both moves show OEMs and materials houses aligning to supply rollable/transparent and automotive display programs. The year closed with December 2025 DuPont commercialising a flexible substrate film for MicroLED mass-transfer processes, emphasising the immediate addressable opportunity in microLED tooling and yield improvement.

Optical Film Market Trends and Opportunities

Trend 1: High-Precision Microstructure Films for AR Waveguides

The commercialization of consumer-grade augmented reality glasses is fundamentally constrained by the manufacturability of nano-structured optical films used in waveguide combiners. These films must manipulate light paths with sub-wavelength accuracy while remaining thin, lightweight, and scalable at consumer volumes.

In November 2025, Morphotonics launched its Cypris nanoimprint platform, designed to industrialize waveguide film production at scale. With a stated throughput capacity of 6 million waveguide sets annually and yield targets of 90–95%, the system directly addresses one of the biggest barriers to AR adoption: high scrap rates and cost volatility in nano-patterned films. This shift signals that waveguide optics are moving from bespoke pilot lines into repeatable, high-volume manufacturing.

Material innovation is also accelerating. Research published in Photonics (October 2025) demonstrated ultra-thin silicon carbide (SiC) diffractive waveguide films fabricated using Period-Limited Theory. These films achieved a 55° field of view at a lens weight of 2.12 grams, while mitigating chromatic “rainbow” artifacts that have plagued glass-based waveguides. For OEMs, this translates directly into lighter headsets, improved visual comfort, and longer battery life.

Downstream readiness is evident as well. As of late 2025, micro-LED manufacturers such as Aledia have entered production-phase fabs exceeding $200 million in capital commitment, driving parallel demand for optical films capable of managing monolithic RGB emission. This has enabled AR optical engines to shrink from 5–6 cc to below 0.4 cc, a prerequisite for all-day wearable devices.

Trend 2: Spectrally Selective Films for Agrivoltaics and Building Integration

Optical films are increasingly central to dual-use energy and land strategies, particularly in agrivoltaics and building-integrated photovoltaics (BIPV). The technical inflection point lies in spectral selectivity—films that transmit photosynthetically active radiation (PAR) while redirecting or reflecting near-infrared (NIR) wavelengths for energy generation or thermal management.

In May 2025, research from Fraunhofer Institute for Solar Energy Systems highlighted a decisive shift toward semi-transparent PV modules incorporating spectrally selective thin films. These films channel NIR light—unused by crops—toward crystalline silicon cells, while maintaining high average visible transmittance for plant growth. This approach reframes optical films as yield-optimization tools.

Controlled-environment trials are reinforcing this trend. In October 2025, researchers at the University of Naples Federico II demonstrated that thin-film silicon structures embedded in greenhouse covers preserved biomass output in leafy crops such as Lactuca sativa, while simultaneously generating on-site electricity. This validates optical films as infrastructure-grade materials for dense urban agriculture, where land efficiency and energy autonomy are equally critical.

Policy alignment is accelerating adoption. The Indo–German Cooperation on Agrivoltaics convened large-scale stakeholder consultations in August 2025, pushing standardization of spectrally selective films under programs such as PM-KUSUM. With participation spanning 15 Indian states and over 1,700 stakeholders, these initiatives are moving optical film demand beyond pilots into regulated deployment frameworks.

Opportunity 1: Advanced Polarizers for High-Brightness Automotive Micro-LED Displays

The rapid shift toward immersive, pillar-to-pillar automotive displays is creating a high-value opportunity for advanced polarizer and retarder films engineered for extreme brightness and thermal stress. Unlike consumer electronics, automotive environments impose sustained exposure to sunlight, vibration, and temperature cycling from –40°C to 105°C.

At Display Week 2025, next-generation micro-LED panels demonstrated 3,000 nits full-screen brightness and localized peaks above 10,000 nits, performance levels that are only viable with optical films capable of suppressing glare while maintaining color fidelity. These films are now integral to achieving sunlight readability without excessive backlight power, directly influencing EV range and cockpit energy efficiency.

The aviation segment underscores the upper performance ceiling. In May 2025, BOE showcased a micro-LED head-up display exceeding 300,000 nits for cockpit applications. Such brightness levels require optical films with exceptional thermal stability and minimal polarization loss, reinforcing their role as mission-critical safety components rather than aesthetic layers.

Market penetration is accelerating. By late 2024, over 34% of new vehicles featured curved or large-format displays exceeding 10 inches. This is driving demand for flexible polarizer films that resist delamination and optical distortion, positioning advanced optical film suppliers at the core of next-generation automotive UX platforms.

Opportunity 2: Security Optical Films for Pharmaceutical Brand Protection

Pharmaceutical counterfeiting has evolved into a technologically sophisticated threat, prompting regulators to mandate embedded optical security features rather than surface-level packaging elements. Optical films are emerging as a preferred solution due to their ability to integrate overt and covert identifiers directly into material structures.

In February 2025, the EU enacted Legislative Decree 10/2025, tightening anti-counterfeiting requirements for medicinal products. This regulation mandates anti-tamper devices and unique identifiers, triggering a surge in demand for optical films incorporating diffractive optical variable image devices (DOVIDs) and holographic elements that are extremely difficult to replicate.

Academic reviews published in AAPS PharmSciTech (November 2025) point to the growing use of carbon dots and microstructural optical markers embedded within films. These features enable multi-layer authentication—combining visible color-shift effects with machine-readable forensic markers—creating a security stack that scales across global supply chains.

A notable 2025 development is the integration of blockchain traceability with holographic films. By embedding unique optical signatures that correspond to blockchain records, pharmaceutical manufacturers can establish a verifiable chain of custody from production to dispensing. As enforcement of the Falsified Medicines Directive intensifies, optical films are transitioning from packaging enhancements to regulatory compliance infrastructure.

Market Share Analysis: Optical Film Market

Market Share by Film Type: Backlight Unit (BLU) Films as the Efficiency Multiplier in Modern Displays

Backlight Unit (BLU) films account for around 30% of the Optical Film Market because they sit at the economic and performance core of display manufacturing, directly influencing brightness, power consumption, and bill-of-materials efficiency. As display OEMs push for higher luminance in thinner form factors, BLU films such as Brightness Enhancement Films (BEF) and Dual Brightness Enhancement Films (DBEF) have become non-negotiable components rather than optional upgrades. Reflective polarizer technologies introduced by leading suppliers enable 30–40% gains in light efficiency, allowing manufacturers to achieve higher nits without increasing LED count or energy draw—an essential advantage for battery-powered devices and energy-labeled TVs. The segment’s dominance is further reinforced by near-total visible light recycling, with advanced ESR films reflecting up to 98% of visible wavelengths, effectively reducing wasted photons inside the optical stack. In parallel, aggressive film-thinning trends to 65–82 microns support ultra-slim TV profiles and foldable device architectures without sacrificing optical gain, aligning BLU films with premium industrial design requirements. With this sub-segment projected to grow at an 8.32% CAGR through 2032, BLU films represent the highest value-density layer in the optical stack, explaining their outsized share in a market increasingly defined by efficiency-led differentiation.

Market Share by Application: Displays as the Structural Demand Anchor for Optical Films

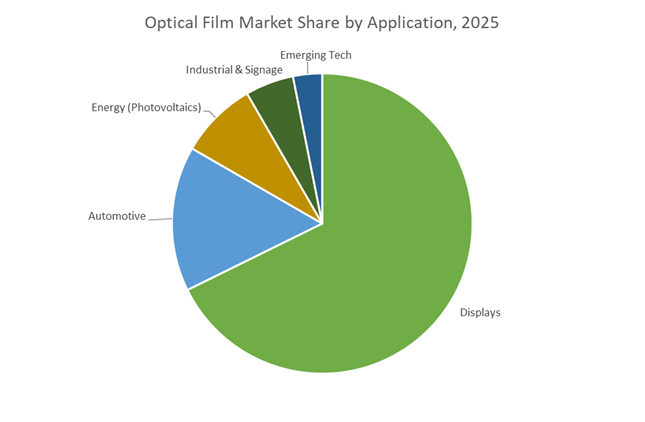

Displays dominate the Optical Film Market with a commanding 65% application share, reflecting their role as the primary commercialization platform for advanced optical materials. This leadership is structurally driven by the global shift from conventional LCDs toward high-resolution OLED, QLED, and Mini-LED displays, all of which require multi-layer optical architectures to manage reflection, polarization, color purity, and ambient light interference. In premium OLED panels alone, over 70% adoption of advanced polarizing and functional films highlights how optical films have transitioned from passive layers to active performance enablers. Smartphones remain the single largest device category within displays, contributing around 41% of demand, with rapid uptake of polymer-based window and polarizer films in foldable and rollable form factors accelerating material innovation cycles. Regionally, the concentration of 88% of global demand across China, South Korea, and Taiwan underscores how tightly optical film consumption is coupled to the Asian display manufacturing ecosystem, making supply chain proximity a competitive necessity. Finally, the industry-wide move toward “zero-defect” optical film production, driven by 8K resolution sensitivity and ultra-fine pixel densities, elevates homogeneity and contamination control as decisive procurement criteria—cementing displays as the dominant, quality-driven application segment in the global optical film market.

Competitive Landscape: Supplier Positioning, Technical Moats and Application Plays

The optical film market is concentrated around companies that combine polymer science, precision coating/microreplication and optical assembly expertise. Leading suppliers differentiate by film function (brightness, polarizing, adhesive, COP), integration with OEM display stacks, and targeted verticals (automotive, microLED, AR/VR).

3M - Multilayer Optical Engineering and System-Level Brightness Optimization

3M remains the benchmark supplier for brightness enhancement and optical efficiency through its proprietary multilayer optical film (MOF) and DBEF™ platforms, which are widely integrated into LCD and mini-LED backlight units. Rather than competing on film count, 3M’s value proposition centers on system-level luminance gains-allowing panel makers to reduce LED density, cut power consumption, and manage thermal loads without sacrificing brightness. Beyond traditional displays, 3M is extending its optical stack into optical clear adhesives (OCAs), light management films for near-eye displays, and films compatible with under-display sensors, reinforcing its position as a system enabler for AR/VR and advanced consumer devices. Its internal capability to design, coat, microreplicate, and scale multilayer structures at tight tolerances remains a major barrier to entry.

Nitto Denko - Polarizer Leadership and Adhesive-Film Integration for Automotive Displays

Nitto Denko’s competitive strength lies in its unique integration of polarizer manufacturing with high-reliability optical adhesive technologies, making it a preferred supplier for automotive infotainment, instrument clusters, and head-up displays. Automotive OEMs increasingly require films that survive wide temperature swings, UV exposure, vibration, and long service lifetimes, and Nitto’s product roadmap is explicitly aligned to these requirements. By supplying polarizers, pressure-sensitive optical adhesives, and functional surface films as a matched system, Nitto reduces assembly risk and defect propagation for Tier-1 display integrators. This system-level approach has positioned the company strongly in mobility displays, where qualification cycles are long and switching costs are high.

Sumitomo Chemical - Vertically Integrated Polarizer Chemistry and Flexible Display Materials

Sumitomo Chemical differentiates itself through vertical control of polymer synthesis, dye chemistry, and film processing, enabling tight control over optical performance and long-term stability. Following the restructuring of its China LCD polarizer operations in late 2024, Sumitomo has reallocated capital and R&D toward OLED polarizers, flexible display materials, and automotive-grade films, where margins and technical barriers are higher. Its development focus includes low-stress polarizers for curved and foldable displays, as well as materials designed to support energy-efficient panels with lower light loss. This repositioning reflects a strategic shift away from commoditized LCD volume toward application-specific, high-performance optical films.

LG Chem - Display-Adjacent Scale with a Pivot Toward Premium and Automotive Films

LG Chem’s position is shaped by its proximity to Korean display ecosystems and long-standing relationships with panel manufacturers. Historically a high-volume supplier of display materials, the company is increasingly focusing on premium polarizers, functional films for OLED, and automotive-qualified optical materials, where reliability and consistency outweigh pure scale. Investments in pilot-scale flexible film lines and advanced polymer R&D signal a move toward higher-value applications, including large-format vehicle displays and next-generation OLED stacks. LG Chem’s ability to coordinate material development closely with downstream panel makers gives it an advantage in time-to-qualification and iterative design cycles.

ZEON Corporation (ZeonorFilm®) - COP Platform for Glass Replacement and Precision Optics

ZEON occupies a differentiated niche as a cyclo-olefin polymer (COP) specialist, with ZeonorFilm® positioned as a glass-alternative optical substrate. The material’s exceptionally low birefringence, high transparency, low moisture uptake, and dimensional stability make it well-suited for retardation films, compensation layers, medical displays, MicroLED modules, and optical components where glass is too heavy or fragile. ZEON’s extrusion-based film technology allows consistent production across ultra-thin to thicker gauges, supporting applications ranging from precision optics to emerging transparent and functional display concepts. As display architectures diversify beyond flat glass-based stacks, ZEON’s COP platform gives it a strategic foothold in next-generation and non-traditional optical film applications.

China: Polarizer Sovereignty and Vertical Integration Acceleration

China has decisively shifted from downstream display assembly to upstream dominance in optical films, making polarizers a cornerstone of its broader display sovereignty strategy. By 2025, Chinese manufacturers control 65% of global polarizer production capacity, with projections pointing toward 80% by 2027, fundamentally reshaping pricing power and supplier dependencies across LCD, OLED, and automotive display ecosystems. This expansion is not incremental—it is driven by state-backed consolidation and aggressive vertical integration into critical sub-films such as triacetyl cellulose (TAC) and PET protective layers.

Strategic acquisitions by domestic leaders—including Shanjin, Heongmei Optoelectronics, and Sunnypol—have reduced reliance on Japanese imports and tightened control over precursor availability. However, this rapid consolidation caused localized polarizer shortages in early 2025, exposing coordination gaps across the supply chain. In response, Ministry of Industry and Information Technology (MIIT) intensified incentives for “all-in-one” optical film manufacturing clusters, reinforcing China’s long-term objective of end-to-end domestic display material independence.

South Korea: Premium Optical Films for Foldables and EV Cockpits

South Korea’s optical film strategy in 2025 is sharply focused on high-margin, technology-intensive segments, particularly foldable OLED displays and electric vehicle (EV) interiors. In December 2025, Hyosung Advanced Materials completed a major expansion that doubled specialty fiber and film capacity, directly addressing surging demand for EV-grade thermal barriers and high-durability optical layers capable of withstanding prolonged heat and UV exposure.

Policy support under the government’s ₩360.6 billion advanced display and packaging mandate has enabled firms such as LG Chem and Kolon Industries to scale ultra-thin colorless polyimide (CPI) films, a critical enabler for foldable smartphones and rollable displays. Simultaneously, new AI-driven smart factory inspection systems commissioned in 2025 have pushed Optically Clear Adhesives (OCA) adoption up by ~40%, as zero-defect bonding becomes essential for curved and flexible display architectures.

Japan: GX 2040, Traceability, and Chemical Purity Leadership

Japan continues to command the highest-value segments of the optical film market, underpinned by chemical precision, traceability, and sustainability leadership. The GX 2040 Vision, approved by the Japanese Cabinet on January 18, 2025, is channeling R&D subsidies toward recycled, bio-based, and low-carbon optical films, reinforcing Japan’s differentiation from volume-driven competitors.

A key milestone came in April 2025, when Teijin Limited launched a Digital Product Passport (DPP) platform for optical films, enabling blockchain-based tracking to meet the EU’s Ecodesign for Sustainable Products Regulation (ESPR). On the technology front, Fujifilm is leveraging semiconductor-display convergence: its ¥20 billion (~$140 million) investment in Shizuoka and Oita supports production of WAVE CONTROL MOSAIC™ color filters, with operations commencing in Fall 2025, targeting OLED, Micro-LED, and advanced sensor modules.

Taiwan: Micro-LED Scaling and ESG Glass Commercialization

Taiwan is translating its semiconductor manufacturing depth into leadership in Micro-LED optical films and large-format display (LFD) solutions. The Touch Taiwan 2025 exhibitions highlighted breakthroughs in quantum dot (QD) films, diffuser sheets, and ultra-uniform brightness enhancement films tailored for medical imaging and industrial signage, where optical precision directly impacts diagnostic accuracy.

By mid-2025, Taiwanese manufacturers had scaled anti-reflective (AR) and brightness enhancement films (BEF) aligned with the 2nm semiconductor roadmap, where light management is critical not only for displays but also for sensors and lithography-adjacent applications. Commercial momentum is extending into architecture: Vastalent ESG Technology debuted nano-ceramic ESG glass coatings that block 95% of solar infrared while maintaining ~80% electromagnetic transmittance, positioning Taiwan as a first mover in signal-friendly smart city glazing.

United States: CHIPS Act Pull-Through and LiDAR Optics

The U.S. optical film market is increasingly shaped by autonomous systems, defense optics, and reshoring priorities rather than mass consumer displays. The Investment Accelerator Office, established in March 2025 by the U.S. Department of Commerce, is fast-tracking domestic projects focused on interference filters, decorative optical films, and LiDAR-grade coatings essential for AV perception stacks and aerospace sensing.

Supply chain resilience is reinforced by the U.S. Department of Energy, which committed $134 million in December 2025 to commercialize rare earth recovery from e-waste, securing domestic feedstocks for lanthanide-doped optical coatings. In parallel, U.S. automotive suppliers reported heightened 2025 investment in scratch-resistant, anti-fingerprint, and matte films for digital cockpits, reflecting the shift toward touch-centric human–machine interfaces (HMIs).

Germany: Photonics 2025 and PFAS-Free Optical Films

Germany anchors Europe’s optical film ecosystem through a blend of photonics R&D, regulatory compliance, and sustainability-driven innovation. Under Bavaria’s €5.5 billion High-Tech Agenda, Photonics 2025 initiatives are supporting custom optics and multi-layer functional polymer films used in medical diagnostics, rail HUDs, and industrial vision systems.

Regulation is a key market driver. In July 2025, German majors including BASF and Covestro launched PFAS-free, recyclable optical films, aligning with evolving REACH and EU zero-pollution mandates. German manufacturers are also prioritizing high-precision light-diffusion films, where micron-level uniformity is critical for medical-grade displays and high-speed rail heads-up displays, reinforcing Germany’s reputation for precision optics.

2025 Strategic Matrix: Optical Film Market Developments

Optical Film Market Developments Matrix

|

Country

|

Primary Market Driver

|

2025 Strategic Milestone

|

Key Material Focus

|

|

China

|

Display panel proximity

|

Polarizer capacity reaches 65% global share

|

Polarizers, TAC sub-films

|

|

South Korea

|

OLED & foldables

|

Hyosung capacity expansion (Dec 2025)

|

OCA, colorless polyimide

|

|

Japan

|

Sustainability & GX 2040

|

Teijin DPP launch for traceability

|

Bio-based films, color filters

|

|

Taiwan

|

Micro-LED & smart cities

|

Nano-ceramic ESG glass debut

|

QD films, AR/BEF coatings

|

|

United States

|

LiDAR & automotive

|

$134M DOE REE recovery funding

|

Interference & matte films

|

|

Germany

|

Circular economy

|

PFAS-free optical film launch (Jul 2025)

|

Recyclable optical resins

|

Optical Film Market Report Scope

Optical Film Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$61.2 Billion

|

|

Market Size (2035)

|

$128.5 Billion

|

|

Market Growth Rate

|

7.7%

|

|

Segments

|

By Type (Polarizing Films, BLU Films, ITO Films, OCA & OCF, Functional Films), By Material (PET, TAC, COP, PC, PI, Bio-based/Recycled Polymers), By Application (Displays, Automotive, Energy, Industrial & Signage, Emerging Technologies)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Nitto Denko Corporation, 3M Company, Sumitomo Chemical Co. Ltd., LG Chem, Toray Industries Inc., Samsung SDI Co. Ltd., Eastman Chemical Company, SKC Co. Ltd., Toyobo Co. Ltd., Mitsubishi Chemical Group, Kolon Industries Inc., Chi Mei Corporation, Sanritz Co. Ltd., Dexerials Corporation, Zeon Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Optical Film Market Segmentation

By Type

- Polarizing Films

- Backlight Unit (BLU) Films

- Indium Tin Oxide (ITO) Films

- Optically Clear Adhesives (OCA) & OCF

- Functional Films

By Material

- Polyethylene Terephthalate (PET)

- Triacetyl Cellulose (TAC)

- Cyclic Olefin Copolymer (COP)

- Polycarbonate (PC)

- Polyimide (PI)

- Bio-based / Recycled Polymers (rPET)

By Application

- Displays

- Automotive

- Energy

- Industrial & Signage

- Emerging Tech

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Optical Film Market

- Nitto Denko Corporation

- 3M Company

- Sumitomo Chemical Co., Ltd.

- LG Chem

- Toray Industries, Inc.

- Samsung SDI Co., Ltd.

- Eastman Chemical Company

- SKC Co., Ltd.

- Toyobo Co., Ltd.

- Mitsubishi Chemical Group

- Kolon Industries, Inc.

- Chi Mei Corporation

- Sanritz Co., Ltd.

- Dexerials Corporation

- Zeon Corporation

*- List not Exhaustive