Package Boilers Market: Strong Growth Anchored by Industrial Demand and Sustainable Innovation

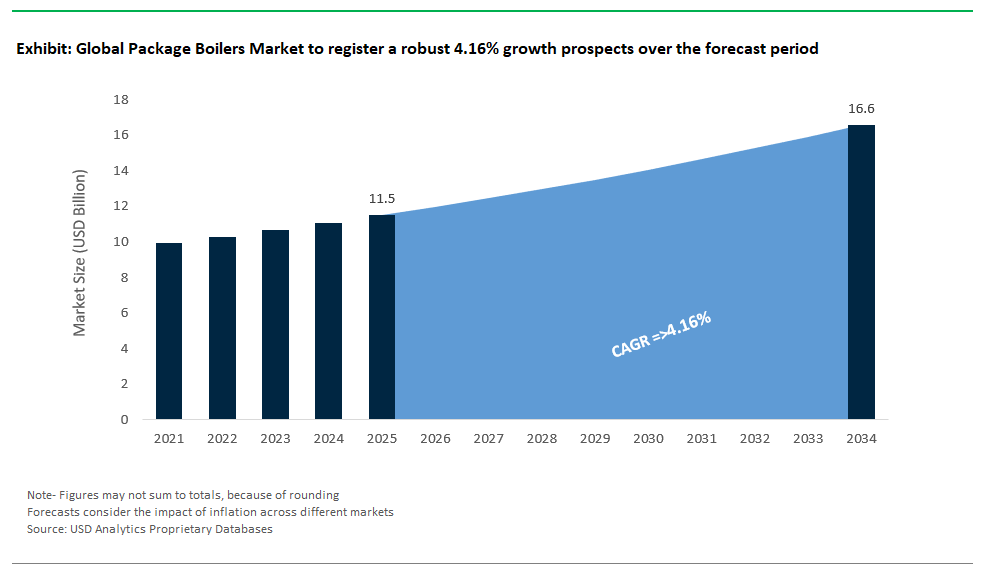

The global package boilers market is on a robust upward trajectory, forecast to expand from $11.5 billion in 2025 to $16.6 billion by 2034, at a steady CAGR of 4.16%. This growth underscores the critical role that package boilers play as the backbone of industrial steam and hot water generation, serving manufacturing, energy, and commercial sectors worldwide. As industries seek space-efficient, cost-effective, and ready-to-install solutions, package boilers pre-assembled, integrated units shipped direct from the factory are favored for their fast deployment, reduced onsite labor, and proven operational reliability.

Industry growth is powered by rising industrialization in emerging markets, tightening environmental regulations, and the global push for energy efficiency and decarbonization. The need for flexible, efficient steam generation spans applications from food processing, chemicals, and pharmaceuticals to power generation and institutional buildings. In response to these demands, manufacturers are driving innovation in cleaner fuels, digital controls, and modular system design. As a result, the package boilers sector is rapidly modernizing to align with the next generation of smart, sustainable industrial infrastructure.

Market Analysis: Digitalization, Clean Energy, and Strategic Expansion Redefine Package Boilers

The package boilers market is in the midst of strategic evolution, defined by digital transformation, clean energy advances, regulatory shifts, and industry consolidation. In February 2025, Cleaver-Brooks launched “myBoilerRoom,” a digital platform centralizing documentation, parts tracking, training, and real-time analytics for boiler room operations a clear reflection of industry-wide digitalization and the growing adoption of IoT-enabled smart boiler systems.

Sustainable development remains a top priority. In September 2024, Babcock Wanson introduced the LV-Pack, a low-voltage electric boiler designed for higher energy efficiency and reduced emissions, targeting customers seeking to meet clean energy mandates. Similarly, strategic partnerships are shaping market reach and service capability, such as Nationwide Boiler Inc.’s March 2024 appointment as Hurst Boiler’s exclusive representative in California and Houston combining regional expertise with an expanded product portfolio.

Regulatory change is also at the forefront: in March 2025, the Indian Parliament passed the Boilers Bill, 2024, modernizing safety standards and streamlining registration/inspection procedures, making it easier for businesses (especially MSMEs) to adopt new boiler technologies in India’s fast-growing market. Meanwhile, global manufacturers are deepening technology collaborations; for example, BHEL’s 2023 technology agreement with Sumitomo SHI FW for CFBC boiler production enhances fuel flexibility and clean emissions indicative of broader industry movement toward low-emission, multi-fuel systems.

Industry consolidation and cross-sector energy expansion are evident in deals like Carrier’s January 2024 acquisition of Viessmann Climate Solutions. While not exclusively in package boilers, such moves illustrate how leading companies are integrating climate solutions, digital controls, and energy management across product lines to maintain competitiveness in a rapidly evolving global market.

Key Trends and Opportunities: Decarbonization and Smart Boiler Technologies Set the Agenda

Shift Towards Cleaner Fuels and Decarbonization Solutions

A defining trend in the package boilers industry is the shift away from coal and oil toward cleaner fuels notably natural gas, biomass, and emerging hydrogen solutions. This change is being driven by global carbon reduction targets, strict emission regulations, and industry commitments to sustainability.

Gas-fired package boilers now dominate due to their high efficiency and lower emissions. Biomass-fired boilers are gaining traction as industries seek low-carbon, circular economy alternatives, while hydrogen-ready and electric boilers are at the frontier of R&D poised to become mainstream as infrastructure and costs align. National and international initiatives, such as the IEA’s Net Zero by 2050 roadmap, are fueling this transition. The market for natural gas package boilers is set to grow at an annual rate of nearly 6.2% through 2034, reflecting global appetite for cleaner, more flexible boiler operations.

Manufacturers are prioritizing the development of flexible, hybrid burner systems, advanced emission control, and boilers capable of seamless fuel switching. The future of the sector will be characterized by rapid uptake of green fuels, digital compliance reporting, and tighter integration with industrial energy management strategies.

Integration of Smart Technologies and Automation

Smart boiler technologies are revolutionizing the package boiler market. The integration of IoT sensors, AI-driven automation, and cloud-based controls allows operators to monitor performance, predict maintenance needs, and optimize energy consumption in real time.

The launch of Cleaver-Brooks’ myBoilerRoom platform is emblematic of this shift, enabling operators to access centralized data, analytics, and diagnostics to reduce downtime and extend equipment life. Modern Boiler Management Systems (BMS) now leverage AI for combustion optimization, while real-time sensors track temperature, pressure, and emissions for maximum efficiency and compliance.

As smart solutions become standard, predictive maintenance, remote diagnostics, and advanced user interfaces will offer new service models and cost efficiencies. This will empower industries to lower energy bills, reduce unplanned outages, and comply with ever-stricter emission standards driving demand for advanced digital boiler platforms and automation-ready designs.

Competitive Landscape: Industry Leaders and Strategic Innovators in the Global Package Boilers Market

The global package boilers market is shaped by established engineering leaders and innovative solution providers, each competing on product reliability, efficiency, digital integration, and sustainability.

Cleaver-Brooks (USA): Digitalization and Integrated Solutions Drive Market Leadership

Cleaver-Brooks stands as a global benchmark for packaged boiler systems, offering a full suite of fire-tube, water-tube, and electric boilers, along with burners, controls, and heat recovery. The 2025 launch of myBoilerRoom signals a new era of digitalized boiler management streamlining operations, maintenance, and analytics. Renowned for its engineering rigor, energy efficiency, and robust service network, Cleaver-Brooks is dedicated to innovation in emission reduction and digital integration.

Babcock & Wilcox Enterprises, Inc. (USA): Broad Portfolio and Clean Energy Focus

Babcock & Wilcox delivers a comprehensive range of boiler technologies and is recognized for its deep engineering expertise and global reach. Operating across renewable, environmental, and thermal segments, B&W is expanding its presence in sustainable and emission-compliant solutions, including advanced package and waste-to-energy boilers. Integration from design to after-market services ensures reliability for complex industrial applications.

Bosch Industriekessel GmbH (Germany): Precision Engineering and Modular Flexibility

Bosch Industriekessel is a global leader in industrial and commercial boiler systems, known for energy efficiency, product reliability, and advanced digital controls. Its modular boiler platforms serve a wide range of applications and fuels, including renewable options. Bosch’s strong international presence and commitment to sustainable, connected boiler systems secure its status in both mature and emerging markets.

Thermax Limited (India): Multi-Fuel Innovation and Emerging Market Strength

Thermax specializes in diverse package boilers, excelling in multi-fuel, waste heat recovery, and biomass-fired solutions. Its August 2022 advances in multi-fuel boilers enable industrial users to optimize for cost and sustainability. With a strong foothold in emerging economies, Thermax prioritizes flexible, energy-efficient products and is driving the shift to greener steam and heat systems.

Miura America Co., Ltd. (USA/Japan): Modular Efficiency and Rapid Response Technology

Miura is known for compact, modular “once-through” steam boilers that combine fast start-up, high efficiency, and a small footprint. These boilers are ideal for facilities seeking scalable solutions and energy savings. Miura’s focus on smart controls, safety, and emission reduction aligns with surging demand for sustainable, automated boiler systems.

Package Boilers Market Share Analysis: Key Segment Insights for 2025

By Type: Fire-Tube Boilers Remain the Backbone, Electric and Hybrid Technologies Surge

Fire-tube boilers are the dominant force in the global package boilers market, holding a commanding 45% share in 2025. Their popularity is driven by their compact footprint, ease of installation, and cost-effectiveness, making them ideal for low to medium-pressure applications across industries. Fire-tube systems are widely adopted in food processing, small-scale chemical production, and institutional facilities, where reliability and ease of maintenance are top priorities. Water-tube boilers, with a 35% share, are essential for high-pressure, high-capacity requirements in sectors like oil & gas, large chemical plants, and power generation. Their ability to handle higher steam pressures and their inherent safety features make water-tube designs a critical choice for demanding industrial environments.

Electric boilers, though a smaller share segment, are experiencing the fastest growth, propelled by stringent emissions regulations, decarbonization efforts, and the push for electrification in process heating. Companies and governments focused on meeting net-zero targets are rapidly adopting electric package boilers, especially in developed markets with cleaner grids. Hybrid boilers combining electric and conventional fuel sources are emerging as a flexible solution, allowing facilities to switch between power sources for cost savings and carbon reduction, marking a significant trend as industries navigate the global energy transition.

.png)

By Application: Chemical & Petrochemical Lead, Food & Beverage Accelerates

Chemical & petrochemical industries are the primary users of package boilers, accounting for 25% of market share in 2025. These sectors rely on package boilers for consistent, high-pressure steam in various processes, including distillation, heating, and chemical reactions. As global chemical output grows and refineries modernize, the demand for efficient, compliant boiler systems rises in tandem. The food & beverage segment follows at 20%, with package boilers essential for critical operations such as sterilization, pasteurization, cooking, and cleaning. The push for food safety, product consistency, and operational efficiency ensures that modern boiler technologies remain at the heart of this industry’s process infrastructure.

Other major application areas include oil & gas (driven by refinery and processing steam needs), paper & pulp (for paper drying and pulping operations), pharmaceuticals (where hygiene and temperature control are paramount), and textiles (steam for dyeing and finishing). While pharmaceuticals and textiles currently represent smaller shares, their growth is accelerating due to stringent regulatory compliance and rising output in emerging economies. Across all segments, the adoption of package boilers is closely linked to trends in industrial modernization, clean energy transition, and automation.

China: Manufacturing Expansion and Environmental Compliance Drive Demand

China’s position as a global manufacturing powerhouse makes it the single largest consumer of package boilers, dominating the Asia Pacific market. Rapid investments in new and upgraded manufacturing infrastructure have driven a surge in demand across chemical & petrochemical, power generation, and general industrial sectors. Environmental regulations are tightening, leading to a major shift toward natural gas, electric, and advanced low-emission boiler systems. Chinese manufacturers, supported by significant R&D, are rapidly upgrading product lines to meet new energy efficiency and emission benchmarks. The combination of fast-paced industrialization, strong government oversight, and relentless modernization ensures that China will remain a pivotal market for both domestic and international boiler suppliers in the years ahead.

The adoption of stricter regulatory policies is not only driving innovation but also opening opportunities for advanced package boiler technologies. Key growth drivers include the scale of ongoing infrastructure projects, continuous updates to manufacturing facilities, and rising demand for reliable steam and hot water systems. China’s focus on cleaner fuels and emission reductions positions it as a critical market for electric and hybrid boilers, especially as factories and municipalities transition toward sustainable operations.

India: Industrial Growth and Policy Support Fuel Rapid Boiler Market Expansion

India’s package boilers market is accelerating rapidly, thanks to robust industrialization across chemicals, pharmaceuticals, food & beverages, and power sectors. Initiatives like “Make in India” and Production Linked Incentive (PLI) schemes have generated over USD 21 billion in new manufacturing investments in 2024 alone, leading to widespread plant expansions and greenfield projects. Package boilers are indispensable in pharmaceuticals (with exports topping USD 25.39 billion), food processing, and textiles, where precise steam quality and operational efficiency are essential.

The new Boilers Bill, 2024, marks a turning point streamlining compliance, improving safety, and encouraging best practices. The adoption of multi-fuel and biomass-fired boilers is growing, reflecting India’s pursuit of sustainability goals and energy security. Expanding output, supportive government policies, and evolving technology are propelling India’s boiler industry into a new era of efficiency and environmental responsibility. The outlook for package boilers is further buoyed by modernization across legacy sectors and a booming export-oriented manufacturing ecosystem.

United States: Modernization, Efficiency Mandates, and Smart Technologies

The United States remains a mature yet highly dynamic market for package boilers, driven by ongoing infrastructure upgrades and a focus on energy transition. The market spans a wide range of applications from food processing and chemicals to institutional and pharmaceutical facilities with modernization efforts targeting increased efficiency and emissions reductions. Regulatory pressure for low-NOx and high-efficiency systems is pushing the adoption of advanced package boilers, including electric and hybrid models.

U.S. manufacturers lead in the development of smart boiler technologies, automation, and cloud-based control systems, with companies like Cleaver-Brooks rolling out solutions such as myBoilerRoom for real-time monitoring and predictive maintenance. The U.S. boiler market is projected to surpass USD 10 billion by 2034, with growth supported by strategic partnerships (e.g., Nationwide Boiler Inc. and Hurst Boiler) and a robust service infrastructure. The U.S. is setting benchmarks for safety, compliance, and operational excellence, making it a focal point for innovation in the global package boilers industry.

Germany: Precision Engineering and Energy Transition at the Core

Germany is a key player within Europe, renowned for its advanced boiler manufacturing, precision engineering, and commitment to sustainability. Stringent EU and national carbon policies are accelerating the transition from traditional fuel-based systems to energy-efficient and low-emission alternatives including electric and hybrid package boilers. German manufacturers like Bosch Industriekessel are at the forefront of R&D, delivering solutions that address both industrial demands and environmental objectives.

The market is driven by diverse industrial applications and significant investments in commercial real estate, supported by a strong emphasis on the circular economy and decarbonization. Germany’s leadership in adopting advanced control systems, waste heat recovery, and digital monitoring sets high standards for operational reliability and sustainability. As the European boiler business experiences a wave of growth, Germany remains central to technology transfer and regulatory advancement in the region.

Japan: Compact Design, Advanced Efficiency, and Global Innovation

Japan’s package boilers market is defined by a focus on compact, highly efficient systems tailored for advanced manufacturing and food processing. Companies such as IHI Corporation, Kawasaki Thermal Engineering, and Miura are global leaders in the development of state-of-the-art thermal engineering solutions. The country’s strict environmental regulations have spurred ongoing R&D in waste heat recovery and alternative fuels, positioning Japanese manufacturers as pioneers in sustainable boiler technology.

Japanese package boilers are widely adopted across chemical, manufacturing, and food industries, valued for their high reliability, compact footprint, and compliance with the world’s toughest emission standards. Continuous innovation and a global export footprint ensure that Japanese firms remain at the cutting edge, influencing boiler markets in Asia and beyond.

United Kingdom: Energy Efficiency and Industrial Decarbonization

The UK is distinguished by its aggressive approach to decarbonization and energy efficiency in industrial processes. Government initiatives supporting the “Green Industrial Revolution” have led to substantial investments in replacing traditional heating systems with modern, eco-friendly package boilers. The UK accounts for over 20% of Europe’s total boiler installations, with significant demand from both legacy industries and new, sustainable manufacturing facilities.

Manufacturers like Babcock Wanson are leading the market with launches of low-voltage industrial electric boilers and other high-efficiency products. The drive toward stringent emission controls and infrastructure upgrades positions the UK as a vital growth market within Europe. Regulatory support and a strong focus on modernization will continue to attract investment in advanced boiler solutions.

Brazil: Biomass Potential and Industrial Demand

Brazil is witnessing strong industrial growth, particularly in food & beverage, chemicals, and paper & pulp sectors all major consumers of package boilers. The abundance of biomass resources gives Brazil a unique edge in adopting sustainable, biomass-fired package boilers, supporting national sustainability and energy diversification efforts.

Growing awareness of energy efficiency and environmental impact is influencing procurement decisions across Brazil’s industrial base. As the nation’s infrastructure and industrialization expand, the demand for efficient, modern steam generation systems will continue to rise, opening significant opportunities for both domestic and international boiler manufacturers.

Australia: Clean Energy Shift and Industrial Expansion

Australia is actively transitioning to a cleaner, more diversified industrial base under national policies like “A future made in Australia.” The drive to reduce carbon emissions and support industrial development is influencing the selection of package boilers, with a clear trend toward high-efficiency, low-emission, and advanced control systems.

Rapid growth in mining and process industries is boosting demand for reliable steam and hot water solutions, while the adoption of high-efficiency units and smart monitoring technologies is on the rise. Australia’s proactive stance on industry support and energy transition will ensure continued market opportunities for innovative package boiler.

Package Boilers Market Report Scope

Package Boilers Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$11.5 Billion

|

|

Market Size (2034)

|

$16.6 Billion

|

|

Market Growth Rate

|

4.16%

|

|

Segments

|

By Type (Fire-Tube Boilers, Water-Tube Boilers, Electric Boilers, Hybrid Boilers)

By Design (D-Type Boilers, O-Type Boilers, A-Type Boilers)

By Fuel Type (Natural Gas, Oil (Diesel, Heavy Fuel Oil, Light Fuel Oil), Biomass (Wood chips, agricultural residues, pellets), Coal, Electric, Multi-fuel / Hybrid, Hydrogen)

By Capacity (10-150 BHP (Boiler Horsepower), 151-300 BHP, 301-600 BHP, Above 600 BHP)

By Application (Chemical & Petrochemical, Food & Beverages, Paper & Pulp, Oil & Gas, Pharmaceuticals, Textiles, Manufacturing, Power Generation, Commercial

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Cleaver-Brooks, Babcock & Wilcox Enterprises, Inc., Bosch Industriekessel GmbH, Thermax Limited, Miura America Co., Ltd. (part of Miura Co. Ltd.), Indeck Power Equipment Company, Rentech Boiler Systems, Inc., Clayton Industries, IHI Corporation, Hurst Boiler & Welding Co., Inc., Johnston Boiler Company, Isgec Heavy Engineering Ltd., Kawasaki Thermal Engineering Co., Ltd., Danstoker A/S, astebo, 1The Fulton Companies

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Type

- Fire-Tube Boilers

- Water-Tube Boilers

- Electric Boilers

- Hybrid Boilers

By Design

- D-Type Boilers

- O-Type Boilers

- A-Type Boilers

By Fuel Type

- Natural Gas

- Oil (Diesel, Heavy Fuel Oil, Light Fuel Oil)

- Biomass (Wood chips, agricultural residues, pellets)

- Coal

- Electric

- Multi-fuel / Hybrid

- Hydrogen

By Capacity

- 10-150 BHP (Boiler Horsepower)

- 151-300 BHP

- 301-600 BHP

- Above 600 BHP

By Application

- Chemical & Petrochemical

- Food & Beverages

- Paper & Pulp

- Oil & Gas

- Pharmaceuticals

- Textiles

- Manufacturing

- Power Generation

- Commercial

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Package Boilers Market

- Cleaver-Brooks

- Babcock & Wilcox Enterprises, Inc.

- Bosch Industriekessel GmbH

- Thermax Limited

- Miura America Co., Ltd. (part of Miura Co. Ltd.)

- Indeck Power Equipment Company

- Rentech Boiler Systems, Inc.

- Clayton Industries

- IHI Corporation

- Hurst Boiler & Welding Co., Inc.

- Johnston Boiler Company

- Isgec Heavy Engineering Ltd.

- Kawasaki Thermal Engineering Co., Ltd.

- Danstoker A/S

- astebo

- 1The Fulton Companies

* List Not Exhaustive

Research Coverage

This report investigates the global package boilers market, delivering in-depth analysis reviews, technological breakthroughs, and strategic insights into the evolution of industrial steam and heating solutions worldwide. USDAnalytics highlights key trends, regulatory dynamics, and competitive benchmarking, positioning this report as an essential resource for manufacturers, investors, engineers, and decision-makers navigating rapid industrial transformation, decarbonization, and energy transition in the boiler industry.

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Segmentation Covered:

- By Type: Fire-Tube Boilers, Water-Tube Boilers, Electric Boilers, Hybrid Boilers

- By Design: D-Type Boilers, O-Type Boilers, A-Type Boilers

- By Fuel Type: Natural Gas, Oil (Diesel, Heavy Fuel Oil, Light Fuel Oil), Biomass (Wood chips, Agricultural Residues, Pellets), Coal, Electric, Multi-fuel / Hybrid, Hydrogen

- By Capacity: 10–150 BHP, 151–300 BHP, 301–600 BHP, Above 600 BHP

- By Application: Chemical & Petrochemical, Food & Beverages, Paper & Pulp, Oil & Gas, Pharmaceuticals, Textiles, Manufacturing, Power Generation, Commercial

- Time Frame: Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Key Companies Profiled: Cleaver-Brooks, Babcock & Wilcox Enterprises, Inc., Bosch Industriekessel GmbH, Thermax Limited, Miura America Co., Ltd. (Miura Co. Ltd.), Indeck Power Equipment Company, Rentech Boiler Systems, Inc., Clayton Industries, IHI Corporation, Hurst Boiler & Welding Co., Inc., Johnston Boiler Company, Isgec Heavy Engineering Ltd., Kawasaki Thermal Engineering Co., Ltd., Danstoker A/S, astebo, The Fulton Companies.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) featuring detailed tables, charts, and interactive visualizations

- Country-Specific Forecasts & Strategic Analysis for all major and emerging markets

- Segment-Wise Revenue Forecasts (2025–2034) by type, design, application, capacity, and region

- Competitive Analysis, Market Benchmarking, and SWOT Profiles of leading package boiler manufacturers

- Recent Developments & Innovation Tracker highlighting product launches, M&A, regulatory updates, and technology adoption

- Executive Summary & Analyst Commentary synthesizing critical findings and actionable insights

- Post-Purchase Analyst Support for client-specific queries, custom data requests, and clarifications

USDAnalytics ensures that this package boilers market report delivers the strategic clarity, deep segmentation, and actionable foresight required to compete, innovate, and lead in the evolving global boiler industry. The report empowers stakeholders to anticipate regulatory changes, benchmark competitors, and formulate data-driven growth strategies across all segments of the package boiler value chain.