Paints and Varnishes Market Size, Decorative Demand Expansion, and Industrial Coating Transformation

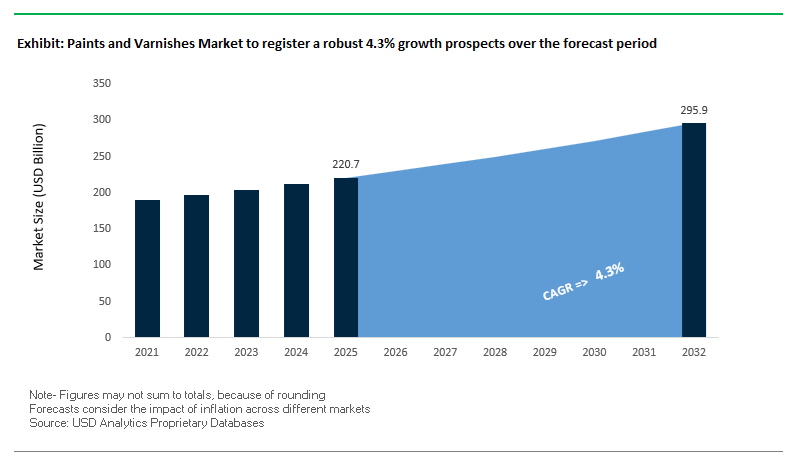

The global Paints and Varnishes Market was valued at $220.7 billion in 2025 and is projected to grow at a CAGR of 4.3% through 2032, reaching $296.3 billion by 2032. This expansion reflects sustained demand across residential construction, infrastructure development, automotive manufacturing, marine coatings, and industrial maintenance, where paints and varnishes serve as both protective and aesthetic surface solutions.

A fundamental growth driver is the continued expansion of urbanization and infrastructure investments, particularly across Asia-Pacific, Africa, and Latin America. Decorative paints and varnishes remain volume-dominant, but increasing demand for premium finishes, long-life coatings, and weather-resistant formulations is shifting value toward higher-margin segments. Additionally, varnishes are gaining traction in wood coatings, furniture, and specialty architectural applications, where durability, gloss retention, and environmental resistance are critical performance attributes.

Simultaneously, the industry is undergoing a transition toward waterborne, low-VOC, and bio-based coating technologies, driven by tightening environmental regulations and sustainability commitments. Innovations in biosurfactants, waterborne primers, and advanced resin systems are enabling manufacturers to deliver high-performance coatings with reduced environmental impact. This shift is particularly relevant in industrial varnishes and protective coatings, where regulatory compliance and lifecycle performance are increasingly interconnected.

Another key trend is the rise of localized product development and regional customization, particularly in emerging markets. Manufacturers are aligning product portfolios with regional climate conditions, cultural preferences, and application requirements, while also strengthening distribution networks and retail presence. At the same time, the integration of smart coatings, advanced additives, and digital color technologies is enhancing product differentiation and customer engagement across both professional and consumer segments.

Market Analysis: Regional Expansion Strategies, and Waterborne Innovation Reshaping Market Dynamics

Recent developments in the Paints and Varnishes Market indicate a period of significant consolidation, regional expansion, and technology-driven innovation. The most prominent event is the November 2025 merger agreement between AkzoNobel and Axalta, forming a global coatings leader valued at $25 billion, with strong capabilities across automotive OEM, refinish, and industrial coatings. This merger, expected to close in late 2026, underscores the increasing importance of scale, portfolio diversification, and global reach in the coatings industry.

Strategic divestments are also reshaping the competitive landscape. BASF’s €7.7 billion sale of its global coatings division, finalized in March 2026, creates a standalone coatings entity backed by Carlyle and QIA, while allowing BASF to focus on upstream chemical operations. This move reflects a broader industry trend of portfolio optimization and specialization.

Product innovation remains a central competitive lever. PPG’s launch of AQUACRON® waterborne shop primers (March 2026) introduces low-VOC, fast-curing solutions for structural steel, addressing historical performance limitations of water-based industrial coatings. Meanwhile, Evonik’s bio-based biosurfactants, including TEGO® Wet 570 Terra and 580 Terra, enable the formulation of renewable, high-performance varnishes without compromising wetting and flow characteristics.

Regional expansion and market penetration strategies are accelerating growth. Jotun’s expansion into Africa, supported by new manufacturing facilities in Algeria and Ethiopia, targets rapidly growing construction markets, while Sherwin-Williams’ integration of Suvinil has driven strong performance in Latin America. In India, Kansai Nerolac’s launch of Excel Everlast 20 reflects increasing demand for long-duration exterior coatings with extended warranties and enhanced weather resistance.

At the same time, companies are leveraging data-driven and culturally tailored marketing strategies. Nippon Paint’s “Year Shade Cards” initiative demonstrates a shift toward hyper-localized color palettes, aligning product offerings with regional design preferences and cultural aesthetics. Additionally, Hempel’s strong marine segment performance, driven by advanced hull coatings that reduce CO2 emissions, highlights the growing importance of sustainability-driven innovation in industrial varnishes.

Market Trend: Ultra-Low VOC “Day-Zero” Paints Enabling Immediate Occupancy and Indoor Air Quality Compliance

The paints and varnishes industry is undergoing a decisive shift toward ultra-low VOC interior coatings designed for immediate occupancy environments. Professional contractors and facility managers are increasingly specifying formulations with VOC levels below 5 g/L to meet the growing demand for odor-free, health-compliant indoor spaces across commercial offices, healthcare facilities, and high-density residential projects. This transition reflects a broader alignment with indoor air quality standards and green building certifications.

Operational efficiency is a primary driver of adoption. Ultra-low VOC paints enable a 30% to 40% reduction in project downtime, as they eliminate the need for extended ventilation cycles and specialized air purification systems typically required with conventional coatings. This is particularly valuable in commercial retrofit projects where rapid turnaround directly impacts revenue and occupancy schedules.

Emission performance has improved significantly with next-generation formulations. While traditional low-VOC paints in the 50 g/L range can continue emitting detectable odors for up to 72 hours, advanced “Day-Zero” coatings achieve non-detectable total volatile organic compound levels within four hours of application. This rapid emission stabilization is critical for environments requiring immediate usability, such as offices, schools, and hospitality spaces.

Consumer behavior is reinforcing this trend. Recent market data indicates that approximately 47% of homeowners prioritize eco-friendly and low-emission finishes, driving a 41% expansion in premium interior paint offerings focused on indoor air quality. This shift is encouraging manufacturers to invest in zero-emission technologies and certification-driven product development to meet evolving customer expectations.

Market Trend: UV-Curable Polyurethane-Acrylate Hybrids Transforming Marine and High-Traffic Wood Coatings

UV-curable polyurethane-acrylate hybrid coatings are redefining performance standards in marine varnishes and high-traffic wood finishing applications. These advanced systems offer near-instantaneous curing through ultraviolet cross-linking, replacing traditional multi-day curing cycles associated with oil-based and moisture-cure urethane coatings.

The most significant advantage lies in application speed. UV-curable hybrid systems allow recoating within approximately 45 minutes, enabling complete multi-coat systems to be applied within a single work shift. This represents a major efficiency gain compared to conventional systems that require four to six hours between coats, significantly reducing labor time and project duration.

Mechanical performance is also enhanced through improved cross-linking density. Experimental data from controlled studies shows that UV curing increases cross-cut adhesion ratings from 3B to 5B, while tensile strength doubles from approximately 4.1 MPa to 8.8 MPa. This improved adhesion and mechanical integrity are critical for coatings exposed to high mechanical stress and environmental conditions.

Water resistance is another key performance metric. UV-cured polyurethane-acrylate coatings demonstrate a 60% to 70% reduction in water absorption after prolonged immersion compared to standard waterborne urethanes. This hydrophobic performance makes them particularly suitable for marine environments and exterior wood applications where moisture resistance is essential. These combined attributes are positioning UV-curable hybrid coatings as a high-growth segment in advanced varnish technologies.

Market Opportunity: GSA P100 Sustainability Mandates Driving Demand for Certified Low-Emission Coatings in Federal Projects

The updated GSA P100 Facilities Standards are creating a large-scale opportunity for manufacturers of low-emission paints and varnishes. Federal construction and renovation projects are now required to meet LEED Gold certification standards, which effectively mandate the use of coatings with verified low-emission profiles, such as UL GREENGUARD Gold certification.

This requirement is driving procurement shifts across a portfolio exceeding 370 million square feet of federal workspace. Coating suppliers must provide comprehensive documentation demonstrating compliance with stringent emission criteria, including screening for thousands of volatile organic compounds. This level of regulatory rigor is favoring manufacturers with advanced testing capabilities and certified product lines.

Institutional purchasing behavior is also evolving. Approximately 55% of large-scale buyers are willing to pay a premium for coatings that contribute to improved indoor environmental quality and regulatory compliance. This willingness to invest in higher-performance, sustainable products is creating a strong value proposition for premium low-VOC and zero-VOC coatings in government and commercial sectors.

Market Opportunity: China Indoor Air Quality Regulations Accelerating Adoption of Low-Emission Architectural Coatings

China’s implementation of GB 30981.1-2025 is establishing a new regulatory baseline for indoor air quality in architectural coatings, creating substantial opportunities for compliant paint and varnish technologies. The standard introduces stricter limits on harmful substances, aligning coating performance with national indoor air quality guidelines and broader environmental targets.

One of the most significant changes is the tightening of formaldehyde limits, now capped at 0.08 mg/m³. This requires manufacturers to reformulate coatings using low-emission raw materials and advanced binder technologies that minimize formaldehyde release. In addition, the regulation enforces stricter limits on heavy metals such as lead, cadmium, and mercury, ensuring that coatings meet international safety benchmarks.

The regulatory framework is further supported by broader environmental objectives, including reduced particulate matter targets. The national roadmap for 2026 to 2030 aims to lower average PM2.5 levels to 25 micrograms per cubic meter, driving a 15% to 20% reduction in solvent emissions across the coatings supply chain. This is accelerating the transition toward waterborne, high-solids, and zero-VOC coating systems.

These regulatory developments are reshaping the competitive landscape, creating strong demand for advanced low-emission coatings that meet both performance and compliance requirements. Manufacturers capable of delivering high-performance, environmentally compliant products are positioned to benefit from China’s rapidly evolving coatings market.

Paints and Varnishes Market Share and Segmentation Insights

Decorative Paints Capture 58.4% Share Driven by Repainting Cycles and Surface Area Coverage

The paints and varnishes market by product type is dominated by decorative paints, accounting for a substantial 58.4% market share in 2025, fueled by their extensive use in residential, commercial, and infrastructure applications. These coatings cover the largest surface areas, including interior walls, exterior facades, ceilings, and trims, making them the primary revenue driver in the global architectural coatings market. A key growth catalyst is the consistent repainting cycle of 3–7 years, ensuring recurring demand across both developed and emerging economies. Additionally, the rise of low-VOC waterborne decorative paints, combined with ease of application via brush, roller, and spray, has significantly expanded adoption among both DIY consumers and professional painters. With increasing urbanization, renovation activity, and demand for aesthetic finishes and sustainable coatings, decorative paints continue to anchor growth in the global paints and varnishes industry.

Trade (Contractor/Professional) Segment Holds 45.3% Share Through Bulk Procurement and Project Specifications

In the paints and varnishes market by distribution channel, the trade (contractor/professional) segment leads with a 45.3% market share in 2025, highlighting the dominance of professional painters and large-scale project procurement. Contractors typically purchase coatings in bulk volumes (5–20L containers) for residential, commercial, and industrial applications, benefiting from trade discounts, credit terms, and dedicated supplier support. A critical factor driving this segment is specification control, where architects, builders, and project managers mandate specific branded paint systems to ensure uniform color consistency, durability, and performance across projects. This structured procurement process reinforces reliance on established trade distribution networks. As construction activity and renovation projects accelerate globally, the contractor channel remains the backbone of the global paints and varnishes supply chain, ensuring steady volume growth and strong brand loyalty among industry professionals.

Competitive Landscape of the Paints and Varnishes Market

Sherwin-Williams Leads Global Paints and Varnishes Market with Strong Retail and Industrial Presence

The Sherwin-Williams Company remains the dominant force in the global paints and varnishes market, leveraging its extensive retail network and high-performance industrial coatings portfolio. In Q1 2026, the company reported net sales of $5.67 billion, reflecting a 6.8% year-over-year increase, with strong double-digit growth in its automotive refinish segment. Sherwin-Williams reaffirmed its 2026 EPS guidance of $11.50 to $11.90, supported by effective price/mix strategies amid raw material volatility. Continued investment in its Paint Stores Group drove a 2.4% increase in same-store sales. With 14% market share in North America, the company is focusing on low-VOC varnish formulations and digital specification tools for contractors.

PPG Strengthens Market Position with PFAS-Free Packaging Coatings and Energy-Efficient Technologies

PPG Industries, Inc. is a key player in the paints and varnishes market, leading innovation in aerospace, packaging, and protective coatings. In Q1 2026, the company achieved organic sales growth despite challenging conditions, with its packaging coatings segment delivering double-digit gains. PPG’s launch of a PVC-free, one-component coating for food packaging highlights its focus on safety and regulatory compliance. The company has also achieved 12 consecutive quarters of growth in protective and marine coatings, particularly in Asia-Pacific. With nearly 11% global market share, PPG is advancing low-bake clearcoat technologies that reduce energy consumption by up to 35%, strengthening its sustainability leadership.

AkzoNobel Advances Sustainable Coatings Leadership Through Strategic Merger and Portfolio Optimization

AkzoNobel N.V. continues to lead the European paints and varnishes market, focusing on sustainability and high-margin product segments. The company is progressing toward its merger with Axalta, expected to close by late 2026 or early 2027, creating a global coatings leader. AkzoNobel has achieved a 47% reduction in carbon emissions compared to its 2018 baseline and expanded its EBITDA margin to 14.2% through efficiency improvements. Its strong portfolio includes Interpon powder coatings and Dulux decorative paints, with increasing focus on antimicrobial and self-cleaning varnish technologies. The company is also divesting non-core assets to streamline operations and enhance profitability.

Nippon Paint Drives APAC Growth with Eco-Friendly Varnish Innovations and Localized Strategy

Nippon Paint Holdings is a dominant player in the Asia-Pacific paints and varnishes market, leveraging a decentralized “Lean for Growth” model to capture regional demand. In 2026, the company increased its market share in Indonesia to 20%, supported by localized production and competitive pricing strategies. It is guiding for steady revenue growth, anticipating recovery in construction activity. Nippon Paint leads in photocatalytic and self-cleaning varnish technologies, particularly in China, where eco-friendly products dominate new launches. 58% of its 2026 product portfolio focuses on low-odor and sustainable coatings, reinforcing its leadership in environmentally friendly solutions.

BASF Expands High-Performance Varnish Technologies with Advanced Color and Sustainable Solutions

BASF SE is a global leader in high-performance paints and varnishes, particularly in automotive OEM and industrial clearcoat segments. The company’s “Driving the Proxy” color collection showcases advanced interference pigment technologies that create multi-dimensional, liquid-metal finishes. BASF has integrated renewable and recycled raw materials into over 40% of its 2026 product range, significantly reducing VOC emissions through waterborne technologies. Its expansion of specialty amine production in China supports the development of advanced curing agents for epoxy and polyurethane varnishes. With a strong presence in the global refinish coatings market, BASF continues to lead in low-VOC, fast-curing varnish solutions.

China: Advanced Functional Coatings and Maritime Leadership

China has transitioned into the global hub for advanced functional paints and varnishes, driven by its dominance in shipbuilding and a strategic shift toward high-value industrial coatings. The country’s maritime leadership is fueling strong demand for anti-fouling and anti-corrosive coatings, aligned with GB 4806.10-2025 standards and international environmental compliance.

Innovation is accelerating across multiple fronts. Investments such as Evonik’s specialty amine expansion in Nanjing are strengthening curing agent supply for polyurethane and epoxy systems, while Covestro’s bio-based polyaspartic resins are enabling sustainable applications in wind energy and flooring. Technological advancements include radiative cooling coatings by AkzoNobel, capable of reducing surface temperatures by up to 10%, supporting urban heat management.

China is also advancing in automotive coatings, with PPG’s Tianjin design center enabling rapid customization for NEVs, and BASF’s Jiangmen technical hub enhancing real-time process optimization. These developments reinforce China’s evolution from a volume producer to a global innovation leader in coatings.

United States: Regulatory Transformation and Infrastructure-Led Demand

The United States paints and varnishes market is undergoing a structural transformation driven by low-VOC regulations, PFAS restrictions, and infrastructure investment. The Infrastructure Investment and Jobs Act (IIJA) continues to generate significant demand for high-build epoxy and polyurethane coatings, particularly in bridges, rail systems, and industrial refurbishment.

Technological innovation is centered on sustainability and efficiency. AI-optimized reflective coatings developed in 2025 can reduce building surface temperatures by up to 20°C, delivering substantial energy savings. The market is also shifting toward PFAS-free formulations, with silicone-based and bio-wax alternatives gaining traction in packaging and industrial coatings.

Manufacturing investments, such as PPG’s $300 million expansion in North America, are strengthening domestic supply chains. Additionally, breakthroughs like DURANEXT energy-curable coatings are eliminating traditional curing ovens, improving efficiency in coil coating applications. Growth in pharmaceutical cold-chain logistics is further driving demand for antimicrobial and anti-fog varnish additives, reinforcing the U.S. position as a leader in high-performance coatings.

Germany: Green Chemistry and Circular Economy Leadership

Germany continues to lead Europe’s paints and varnishes market through its focus on sustainability, circular economy integration, and regulatory compliance. Approximately 40% of coating facilities are undergoing VOC retrofits, reflecting strong alignment with EU Green Deal targets.

The country is driving innovation in bio-based polyols and polyurethane systems, supported by Covestro’s €1.5 billion investment in sustainable materials. Growth in offshore wind infrastructure is creating demand for coatings capable of withstanding 25-year C5-M corrosive environments.

Germany is also pioneering digital tracer technologies embedded in varnishes, enabling recycling systems to achieve 99.5% sorting accuracy. BASF’s €200 million investment in waterborne production lines in Münster signals a decisive shift away from solvent-based systems. Additionally, the launch of biosurfactants like TEGO Wet Terra is advancing sustainable waterborne formulations, reinforcing Germany’s leadership in green coatings innovation.

India: Fastest-Growing Decorative and Infrastructure Coatings Market

India is the fastest-growing paints and varnishes market globally, driven by urbanization and large-scale housing initiatives such as PMAY-U 2.0. This program is significantly boosting demand for architectural acrylics, emulsions, and decorative coatings.

The market is witnessing rapid consolidation, highlighted by JSW Paints’ acquisition of Akzo Nobel India, strengthening domestic capabilities. Innovations in nanotechnology-based self-cleaning coatings, offering “lotus-effect” performance, are gaining traction in high-rise residential projects.

Infrastructure projects under the Smart Cities Mission are driving adoption of anti-carbonation coatings for public assets. Meanwhile, rising imports of titanium dioxide (TiO₂)—a critical pigment—are pushing the government to encourage local production. The growth of solar-reflective coatings, capable of reducing indoor temperatures by 5°C, aligns with India’s sustainability goals and positions the country as a high-growth innovation market.

Japan: Precision Materials and EV-Driven Coating Innovation

Japan’s paints and varnishes market is defined by advanced material science and precision engineering, particularly in automotive and electronics applications. The development of thermal-reflective coatings for EVs is enhancing battery efficiency by reducing cabin heat load.

Innovations such as ARITERAS KPC photocatalytic coatings are enabling pollutant decomposition in indoor environments, while biocide-free marine coatings are advancing environmentally safe anti-fouling technologies. Japan’s strict Positive List System is driving the development of ultra-low-migration coatings for medical and food-contact applications.

The country is also investing in high-purity coatings for 6G optical fiber infrastructure, alongside innovations in seismic-reinforcement coatings for aging buildings. These advancements reinforce Japan’s leadership in high-performance, precision coatings.

Brazil: Industrial Expansion and Bio-Based Coating Leadership

Brazil is emerging as a key market driven by industrial growth, agribusiness, and bio-based innovation. Expansion projects such as PPG’s Sumaré plant upgrade and WEG’s increased production capacity are strengthening domestic coating supply.

The country’s aerospace sector, led by Embraer, is driving demand for lightweight, high-performance coatings, while agriculture is fueling demand for protective coatings in heavy machinery. Brazil is also a global leader in bio-based binders derived from sugarcane, supporting sustainable coating solutions.

With high solar exposure, R&D is focused on UV-resistant coatings using HALS and specialized absorbers. The market reached a milestone of 1.98 billion liters in sales (2024/2025), reflecting strong growth across industrial and decorative segments.

South Korea: Semiconductor-Driven High-Purity Coating Technologies

South Korea’s paints and varnishes market is shaped by its leadership in semiconductors, electronics, and display technologies, requiring ultra-high-purity coatings. The country leads in anti-static (ESD) and EMI-shielding coatings, critical for cleanroom environments and electronic packaging.

Technological advancements include Thin-Film Encapsulation (TFE) for OLED displays and low-voltage PACVD coatings (<160V) for flexible electronics. South Korea is also advancing high-barrier retort coatings for food packaging, capable of withstanding extreme sterilization conditions.

Sustainability innovation is evident in biotechnological marine coatings, such as Selektope-based solutions, while the K-Beauty industry is driving demand for premium tactile coatings with enhanced aesthetics. These factors position South Korea as a leader in high-tech and precision coating applications.

Paints and Varnishes Market Report Scope

Paints and Varnishes Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$220.7 Billion

|

|

Market Size (2032)

|

$296.3 Billion

|

|

Market Growth Rate

|

4.3%

|

|

Segments

|

By Product Type (Decorative Paints, Varnishes, Stains and Wood Preservatives, Primers and Undercoats, Specialty Coatings), By Resin Type (Acrylic, Polyurethane, Alkyd, Epoxy, Nitrocellulose, Polyester, Vinyl and Vinyl-Acrylic), By Technology (Water-borne, Solvent-borne, Powder Coatings, Radiation-Cured), By End-Use Application (Architectural and Construction, Industrial Wood and Furniture, Automotive and Transportation, General Industrial, Marine and Protective), By Substrate (Wood, Metal, Concrete and Masonry, Plastics and Composites), By Component Type (One-Component, Two-Component), By Distribution Channel (Direct Sales, Trade, Retail, E-commerce and Digital Platforms)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Sherwin-Williams Company, PPG Industries, Inc., Akzo Nobel N.V., Nippon Paint Holdings Co., Ltd., RPM International Inc., Axalta Coating Systems Ltd., BASF SE, Kansai Paint Co., Ltd., Asian Paints Limited, Jotun A/S, Hempel A/S, Masco Corporation, Berger Paints India Limited, Beckers Group, KCC Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Paints and Varnishes Market Segmentation

By Product Type

- Decorative Paints

- Varnishes

- Stains and Wood Preservatives

- Primers and Undercoats

- Specialty Coatings

By Resin Type

- Acrylic

- Polyurethane

- Alkyd

- Epoxy

- Nitrocellulose

- Polyester

- Vinyl and Vinyl-Acrylic

By Technology

- Water-borne

- Solvent-borne

- Powder Coatings

- Radiation-Cured

By End-Use Application

- Architectural and Construction

- Industrial Wood and Furniture

- Automotive and Transportation

- General Industrial

- Marine and Protective

By Substrate

- Wood

- Metal

- Concrete and Masonry

- Plastics and Composites

By Component Type

- One-Component

- Two-Component

By Distribution Channel

- Direct Sales

- Trade

- Retail

- E-commerce and Digital Platforms

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Paints and Varnishes Industry

- The Sherwin-Williams Company

- PPG Industries, Inc.

- Akzo Nobel N.V.

- Nippon Paint Holdings Co., Ltd.

- RPM International Inc.

- Axalta Coating Systems Ltd.

- BASF SE

- Kansai Paint Co., Ltd.

- Asian Paints Limited

- Jotun A/S

- Hempel A/S

- Masco Corporation

- Berger Paints India Limited

- Beckers Group

- KCC Corporation

*- List not Exhaustive