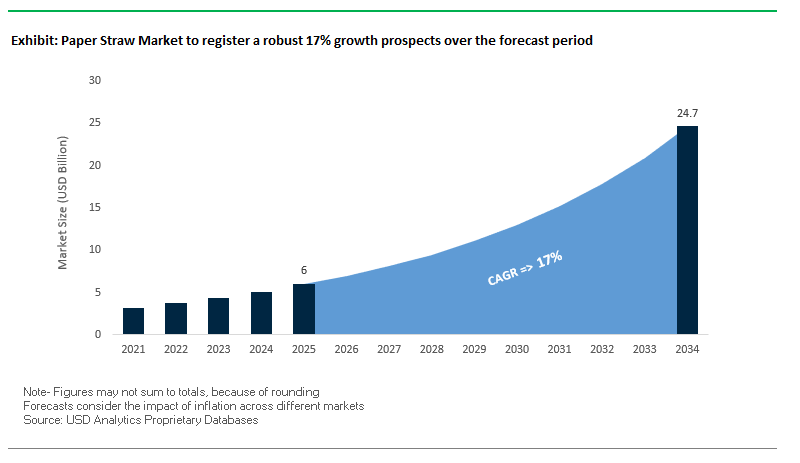

Paper Straw Market Poised to Expand from $6 Billion in 2025 to $24.7 Billion by 2034 with 17% CAGR Driven by Sustainability and Regulatory Pressure

The Global Paper Straw Market is experiencing unprecedented growth, projected to increase from $6 billion in 2025 to $24.7 billion by 2034, at a CAGR of 17%, as governments, corporations, and consumers prioritize eco-friendly alternatives to single-use plastics. Paper straws, made from food-grade paper and adhesives, are integral to quick-service restaurants, hospitality, and food & beverage sectors, serving as both sustainable alternatives and brand engagement tools.

Key Insights for Industry Professionals:

- Government Policies Drive Adoption: Plastic bans and stringent regulations in the EU, UK, US, and India have created a strong, compliant market for paper straws.

- Material Innovation Enhances Durability: Multi-ply designs, advanced adhesives, and coating technologies address the common challenge of straws becoming soggy in liquids.

- Branding and Customization Opportunities: Paper straws are increasingly used for logo printing, color designs, and brand storytelling, enabling companies to showcase sustainability commitments.

- Supply Chain Optimization is Critical: Manufacturers are focusing on sustainable pulp sourcing, high-speed automated production lines, and cost competitiveness versus plastics.

- Circular Economy Alignment: The market is closely linked to broader paper-based packaging trends, promoting renewable and recyclable materials throughout the supply chain.

Recent Developments Illustrate the Industry’s Commitment to Innovation, Sustainability, and Market Expansion

The Paper Straw Industry is rapidly evolving, marked by technological advancements, sustainability initiatives, and strategic investments. In August 2025, Graphic Packaging International added the PaperSeal® Pressed MAP Tray to its portfolio, reflecting the broader industry trend toward fiber-based alternatives to plastic. July 2025 saw the Recycled Materials Association (ReMA) classify paper cups as recyclable, reinforcing the perception of paper straws as part of a sustainable, circular economy solution.

In June 2025, Mondi Group launched the re/cycle PaperPlus Bag Advanced, demonstrating the development of functional, barrier-coated papers suitable for demanding foodservice applications. April 2025 marked International Paper’s $9.9 billion acquisition of DS Smith, strengthening its European presence and indirectly supporting the paper straw supply chain. March 2025 witnessed Billerud’s launch of heat-sealable, fossil-free paper, emphasizing low-carbon and recyclable alternatives to plastics.

Earlier innovations include Huhtamaki’s recyclable single-coated paper cups (February 2025) and Starbucks Japan’s Green Planet™ plant-based straws (December 2024), with a nationwide rollout planned in March 2025. September 2024 featured MJ Global’s single-ply, glue-free paper straw using patented Finnish technology, offering durability of over 30 minutes in liquids, demonstrating the market’s continuous focus on performance, sustainability, and consumer satisfaction.

Trends and Opportunities Transforming the Paper Straw Market

Regulatory-Driven Demand Surge from Single-Use Plastic Bans

The most powerful driver of the global paper straw market is regulation, particularly bans on single-use plastics that leave businesses with no option but to transition to paper-based alternatives. The European Union’s Single-Use Plastics Directive (SUPD), which came into force on July 3, 2021, banned plastic straws along with several other items, immediately creating a non-negotiable demand for paper straws across all EU member states. This mandatory shift has cascaded globally, with countries like India proposing a complete ban on single-use plastics by 2025, ensuring the long-term growth trajectory for paper-based alternatives. In the United States and Asia-Pacific, state- and national-level initiatives are also aligning with this movement, tightening restrictions on plastic straw distribution in foodservice outlets. Corporate alignment is equally critical in reinforcing this trend. Starbucks’ early decision in 2019 to eliminate plastic straws across its 28,000 stores worldwide—effectively cutting over 1 billion straws annually—set a precedent for other major beverage and QSR chains. These regulatory and corporate commitments ensure that the demand for paper straws is not a passing fad but a structural, compliance-driven market transformation.

Performance Innovation to Overcome Consumer Dissatisfaction

While regulatory bans drive adoption, innovation in product performance is addressing long-standing consumer concerns. Early versions of paper straws quickly became soggy and failed to replicate the durability of plastic, leading to dissatisfaction among end users. In response, manufacturers have invested heavily in material science to improve the structural integrity and functional performance of paper straws. Companies such as H.B. Fuller have introduced food-safe, water-based adhesives that allow paper straws to remain intact in liquids for over three hours, solving one of the most significant pain points. Additionally, the widespread adoption of multi-ply construction—typically three layers of tightly wound paper bonded with adhesives—has significantly enhanced sturdiness and resistance to liquid penetration. These innovations not only boost consumer acceptance but also expand the use of paper straws in cold drinks, carbonated beverages, and even certain hot liquid applications. The result is a market that is steadily overcoming the limitations of its early products, positioning paper straws as a credible and scalable alternative to plastics.

Development of Bio-Based, Water-Resistant Coatings

A critical growth opportunity lies in the development and scaling of bio-based coatings to further enhance the durability and performance of paper straws. Polyhydroxyalkanoates (PHA), in particular, are attracting strong interest due to their marine and freshwater biodegradability. Unlike PLA (polylactic acid), which requires industrial composting infrastructure, PHA breaks down naturally in diverse environments, making it highly attractive for regulatory compliance and environmental performance. Specialty chemical companies are actively marketing PHA-based coatings to replace conventional plastic films, targeting applications such as cups, packaging, and straws. Beyond biodegradability, PHA offers superior durability, flexibility, and thermal resistance compared to PLA, enabling paper straws to withstand longer usage times without softening or collapsing. Academic studies confirm that PHA acts as an effective barrier against water, oils, and oxygen, making it suitable for the liquid-contact demands of straws. This innovation creates a pathway for paper straws to move beyond compliance and establish themselves as a high-performance, sustainable solution.

Integration of Digital Printing for Brand Customization and Traceability

Another transformative opportunity for the paper straw market lies in digital printing technologies, which elevate straws from functional items to brand communication tools. Advanced, high-resolution printing enables companies to produce custom straws featuring vibrant, full-color designs, strengthening brand identity in restaurants, cafes, and beverage chains. Beyond visual branding, straws can now incorporate QR codes that connect consumers to digital platforms. These scannable features unlock marketing opportunities such as loyalty program integration, promotional campaigns, and consumer education on sustainability practices. For companies aiming to demonstrate transparency, QR codes can provide details about raw materials, sourcing, and end-of-life recycling or composting pathways. By combining sustainability with consumer engagement, digitally printed paper straws allow brands to differentiate themselves while enhancing customer experience. This convergence of packaging, marketing, and digital traceability is redefining the value proposition of paper straws in a competitive, regulation-driven market.

Leading Paper Straw Manufacturers Are Shaping Sustainability and High-Performance Innovations

The competitive landscape of the Global Paper Straw Market is defined by companies combining materials science expertise, production scale, and sustainable innovation to meet rapidly growing global demand.

Hoffmaster Group Inc. (Aardvark Straws) Leverages Legacy and Domestic Manufacturing to Lead US Paper Straw Supply

Hoffmaster operates Aardvark Straws, known as the Original Paper Straw Company, with a vertically integrated U.S. manufacturing base. The company is expanding its portfolio beyond traditional straws, investing in new machinery and production capabilities to meet the surging demand from national and international foodservice chains. Its offerings include jumbo, bendable, and custom-printed paper straws, designed with FDA-compliant, food-safe materials. Hoffmaster focuses on sustainable, high-performance disposable tableware and leveraging its brand legacy to grow its global market share.

Huhtamaki Oyj Drives Global Expansion Through Innovative Fiber-Based Packaging

Huhtamaki is a leader in sustainable food packaging, with expertise in paperboard converting and global manufacturing operations. In February 2025, the company launched recyclable single-coated paper cups for dairy products, aligning with food safety and recyclability standards. Its portfolio includes paper cups, containers, lids, and other foodservice packaging, using 100% renewable plant-based materials. Huhtamaki aims to accelerate its transformation into a leader in sustainable food packaging, expanding fiber-based product capacity and helping customers achieve sustainability goals.

Transcend Packaging Ltd. Expands European Operations to Support EU Plastic Ban Compliance

Transcend Packaging focuses on 100% plastic-free, recyclable paper straws, catering to major European foodservice brands. The company is scaling its UK and European production to meet EU single-use plastic directives and investing in R&D for higher-performance straw designs. Its offerings are designed for durability and resistance to sogginess, and the company emphasizes leading sustainable packaging innovation for the hospitality sector.

Footprint International Holdings Inc. Develops Compostable Solutions for Global Food Brands

Footprint specializes in fiber-based, compostable alternatives to plastics, with patented technology for custom solutions for major consumer brands. The company is expanding North American manufacturing capacity and partnering with food and beverage companies to launch new sustainable packaging products. Footprint’s straws and trays are plant-based, renewable, and certified compostable, aligning with the circular economy and reducing environmental impact.

Nippon Paper Industries Co., Ltd. Focuses on High-Performance Eco-Friendly Paper Straws in Asia

Nippon Paper leverages R&D capabilities to develop high-performance, durable paper straws, addressing global plastic waste challenges. In March 2019, the company launched a smoother, more durable straw resistant to sogginess. Its portfolio spans containerboard, printing papers, and specialty papers, with a focus on sustainable, circular economy-aligned products. Nippon Paper continues to invest in new technologies to expand eco-friendly, high-performance paper-based solutions across Asia and globally.

United States Paper Straw Market Shaped by Corporate Sustainability and FDA Regulations

The United States paper straw market is undergoing rapid transformation as consumer preference, corporate responsibility, and regulatory frameworks converge to eliminate single-use plastics. A major driver is the FDA ban on PFAS in food-contact materials, which has accelerated the development of fluorine-free barrier coatings that enhance both functionality and safety in paper straws. Leading corporations like Starbucks have been instrumental in shaping market trends, introducing sustainable cold cups and straws across U.S. and Canadian outlets in April 2024. These initiatives highlight the role of major food and beverage players in accelerating paper straw adoption.

The U.S. market is also witnessing innovation in smart and functional straws, with R&D focused on improving durability and addressing common issues like sogginess. Some experimental solutions even integrate interactive features such as QR codes, making straws a branding and engagement tool. While the federal government has sent mixed signals with measures such as the Ending Procurement and Forced Use of Paper Straws executive order, the momentum from corporate sustainability initiatives and rising eco-conscious consumer demand continues to dominate. This positions the U.S. as one of the most important global markets for high-performance and innovative paper straw solutions.

China Paper Straw Market Powered by Plastic Waste Reduction and Mass Manufacturing

The China paper straw market is a global leader in both production and consumption, heavily influenced by strict plastic waste reduction policies and the government’s National Clean Air Programme. With its massive manufacturing and export capabilities, China has become a dominant supplier of paper straws to international markets, leveraging economies of scale to reduce costs while maintaining high output volumes. The country’s booming e-commerce and foodservice sectors further drive demand for disposable straws, particularly in the takeaway and delivery ecosystem.

Domestic manufacturers are rapidly modernizing operations, adopting advanced coating technologies to improve durability and customer satisfaction. A growing niche is the demand for U-shaped paper straws for beverage cartons, especially in dairy and juice packaging. Multinational foodservice and beverage chains expanding in China also amplify demand, ensuring strong growth across both domestic and export markets. The combination of scale, government regulation, and rising consumer eco-awareness makes China a powerhouse in the global paper straw industry.

India Paper Straw Market Driven by Single-Use Plastic Ban and Food Delivery Boom

The India paper straw market is witnessing accelerated adoption following the government’s nationwide ban on single-use plastics, a decisive policy that has transformed consumption patterns across the foodservice and retail industries. With food delivery platforms like Zomato and Swiggy expanding at unprecedented rates, demand for compostable, durable, and spill-resistant paper straws has surged in metropolitan areas.

The Make in India initiative is also creating a fertile ground for domestic manufacturing, with SMEs and large-scale producers receiving financial support and subsidies to scale operations. Local companies have expanded product lines to include flexible and U-shaped paper straws, catering to the beverage and dairy packaging industries. Meanwhile, the country’s quick-service restaurant (QSR) sector and increasing beverage consumption among urban youth are further driving growth. By combining regulatory mandates with strong consumer demand and government-backed manufacturing support, India is emerging as one of the fastest-growing global markets for eco-friendly paper straw solutions.

Germany Paper Straw Market Aligned with EU Sustainability and Advanced Coating Innovation

The Germany paper straw market is at the forefront of Europe’s sustainability shift, heavily shaped by the EU Packaging and Packaging Waste Regulation (PPWR), which bans single-use plastics and mandates recyclable alternatives. German manufacturers are responding with advanced aqueous (water-based) coatings that replace plastic linings, ensuring recyclability within conventional paper mills. This aligns with Germany’s leadership in circular economy practices and its robust recycling infrastructure.

The country’s Blue Angel ecolabel sets stringent benchmarks for environmentally friendly paper products, pushing companies to develop coatings and materials that meet high-performance requirements. With Germany’s strong café and takeaway beverage culture, demand for high-quality, compostable, and recyclable paper straws continues to rise. These regulatory pressures, combined with consumer preference for eco-conscious solutions, are making Germany a benchmark for sustainable innovation in the European paper straw industry.

Japan Paper Straw Market Influenced by Green Innovation and High-Quality Standards

The Japan paper straw market reflects the country’s focus on precision, hygiene, and sustainability. Government policies on plastic waste reduction are driving strong adoption of biodegradable and compostable paper straws, supported by advances in next-generation coating technologies. While companies like Starbucks Japan are experimenting with plant-based alternatives, demand for high-performance paper straws remains resilient.

Leading domestic players such as Nippon Paper Industries and Oji Holdings are spearheading R&D into materials that improve durability, reduce sogginess, and ensure barrier properties for hot and cold beverages. Japan’s foodservice and vending machine culture, coupled with consumer emphasis on convenience and hygiene, makes disposable paper straws a preferred option. With strong innovation pipelines and a balance of sustainability and functionality, Japan is positioning itself as a key player in the Asia-Pacific paper straw industry.

Brazil Paper Straw Market Supported by FMCG Initiatives and Sustainable Packaging Innovation

The Brazil paper straw market is advancing rapidly, led by multinational corporations aligning with global sustainability goals. A landmark example is Nestlé Brazil’s partnership with SIG, which introduced renewable and recyclable paper straws for its NESCAU beverage line. This initiative is expected to eliminate the use of nearly 300 million plastic straws annually, demonstrating the transformative impact of corporate innovation in Brazil.

Beyond multinational players, domestic firms are also responding to growing consumer demand for eco-friendly alternatives, particularly in the beverage and food packaging sectors. Brazil’s regulatory alignment with international food safety and sustainability standards is further encouraging adoption. The introduction of renewable straws for aseptic carton packs highlights the country’s potential to become a hub for sustainable packaging innovation in Latin America, where FMCG demand and environmental awareness are both on the rise.

Paper Straw Market Report Scope

Paper Straw Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$6 Billion

|

|

Market Size (2034)

|

$24.7 Billion

|

|

Market Growth Rate

|

17%

|

|

Segments

|

By Product Type (Straight Straws, Bendable Straws, U-Shaped Straws, Spoon Straws, Other Types), By Material (Virgin Paper, Recycled Paper, Specialty Paper), By Application (Food Service, Institutional, Household Use, Retail), By End-Use Industry (Restaurants & Bars, Coffee Shops, Institutional, Hospitality, Retail), By Length & Diameter (Standard, Custom), By Printing (Printed, Non-Printed)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Huhtamäki Oyj, Transcend Packaging, Hoffmaster Group Inc., Fuling Global Inc., Nippon Paper Industries Co., Ltd., Tetra Pak, Aardvark Straws (Hoffmaster Group Inc.), Paper Straw Co. (Hoffmaster Group Inc.), Footprint, The Paper Straw Company, BillerudKorsnäs AB, Tembo Paper, Charta Global, Transcend Packaging, F. Bender Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Paper Straw Market Segmentation

By Product Type

- Straight Straws

- Bendable Straws

- U-Shaped Straws

- Spoon Straws

- Other Types

By Material

- Virgin Paper

- Recycled Paper

- Specialty Paper

By Application

- Food Service

- Institutional

- Household Use

- Retail

By End-Use Industry

- Restaurants & Bars

- Coffee Shops

- Institutional

- Hospitality

- Retail

By Length & Diameter

By Printing

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Paper Straw Market

- Huhtamäki Oyj

- Transcend Packaging

- Hoffmaster Group Inc.

- Fuling Global Inc.

- Nippon Paper Industries Co., Ltd.

- Tetra Pak

- Aardvark Straws (Hoffmaster Group Inc.)

- Paper Straw Co. (Hoffmaster Group Inc.)

- Footprint

- The Paper Straw Company

- BillerudKorsnäs AB

- Tembo Paper

- Charta Global

- Transcend Packaging

- F. Bender Ltd.

* List Not Exhaustive

Methodology

At USDAnalytics, our approach to analyzing the Global Paper Straw Market integrates comprehensive primary and secondary research, ensuring accurate, data-driven insights for industry professionals. We begin with an extensive review of company reports, regulatory documents, patent filings, and sustainability frameworks to capture the evolving landscape of paper straw adoption, innovations, and regional dynamics. Primary interviews with key stakeholders—including manufacturers, distributors, and end-users—allow us to validate market drivers, challenges, and emerging trends such as bio-based coatings, digital printing, and performance-enhancing multi-ply designs. Advanced quantitative modeling is applied to historical market data, global regulatory impacts, and corporate investment activities to forecast growth trajectories by product type, material, application, and region. Our methodology also emphasizes competitive benchmarking, highlighting strategic initiatives, capacity expansions, and technological innovations among market leaders like Huhtamäki Oyj, Hoffmaster Group Inc., and Nippon Paper Industries. By combining macroeconomic factors, regulatory landscapes, and consumer behavior trends, USDAnalytics delivers an integrated, forward-looking market assessment that supports decision-making for manufacturers, investors, and policymakers in the paper straw industry.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.