Parking Deck Coatings Market Size, Infrastructure Modernization, and High-Durability Coating Demand

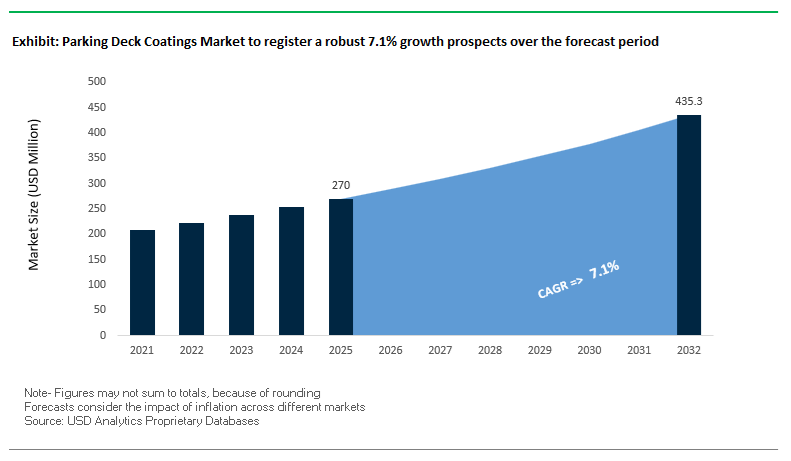

The global Parking Deck Coatings Market was valued at $270 million in 2025 and is projected to expand at a CAGR of 7.1% through 2032, reaching $436.4 million by 2032. This above-average growth rate reflects the increasing prioritization of infrastructure durability, lifecycle cost optimization, and safety compliance across commercial, residential, and mixed-use parking structures.

A primary market driver is the global surge in urban infrastructure development and refurbishment of aging parking facilities, particularly in North America, Europe, and rapidly urbanizing regions in Asia-Pacific and the Middle East. Parking decks are exposed to severe mechanical stress, water ingress, de-icing salts, UV radiation, and thermal cycling, making advanced coating systems essential for preventing concrete deterioration, corrosion of reinforcing steel, and structural failures.

Technological advancements in polyurethane, epoxy, and PMMA-based coating systems are enabling superior performance characteristics such as crack-bridging capability, rapid curing, skid resistance, and chemical protection. In addition, the increasing adoption of low-VOC and high-solids formulations is aligning with stringent indoor air quality standards, especially in enclosed or mixed-use parking environments.

Another critical trend is the shift toward integrated waterproofing and protective systems, where coatings are designed not only for surface protection but also for long-term structural preservation and reduced maintenance cycles. Regional manufacturing expansion and localized production strategies are further enhancing supply chain resilience, enabling faster deployment of coating solutions in infrastructure-intensive markets.

Market Analysis: Capacity Expansion, Regional Infrastructure Investments, and Low-VOC Innovation Driving Market Growth

Recent developments in the Parking Deck Coatings Market highlight strong momentum in capacity expansion, regional market penetration, and advanced material innovation. In March 2026, BASF inaugurated its $10 billion Verbund site in Zhanjiang, China, significantly boosting the production of performance chemicals, including precursors for polyurethane and epoxy-based coating systems. This facility strengthens supply capabilities for high-growth infrastructure markets across China and Southeast Asia.

Strategic acquisitions are reinforcing market positioning in emerging regions. Master Builders Solutions’ acquisition of Arkaz (March 2026) enhances its footprint in the Middle East, particularly in Saudi Arabia and the UAE, where large-scale infrastructure programs such as Vision 2030 are driving demand for advanced waterproofing and deck protection systems.

Localization strategies are proving critical in mature markets. Sika AG reported record revenues in the Americas (February 2026), with nearly all of its U.S. products, including Sikafloor® parking deck systems, now manufactured domestically. This “local-for-local” approach improves supply chain efficiency and aligns with government-backed infrastructure investments and refurbishment initiatives.

Product innovation is focused on durability and application efficiency. Tremco CPG’s acquisition of a specialized coatings manufacturer (June 2025) strengthens its portfolio in fast-curing, cold-applied waterproofing membranes, reducing downtime for commercial parking operators. Meanwhile, Sto Corp’s StoPrime Deck systems introduce high-build, crack-bridging primers designed to withstand freeze-thaw cycles and salt exposure, addressing a key challenge in North American climates.

Sustainability and regulatory compliance are also shaping product development. Sika’s rollout of low-VOC polyurethane coating systems, fully deployed in 2026, meets stringent indoor air quality standards in mixed-use developments. Additionally, Master Builders Solutions’ bio-identical material R&D initiative signals a shift toward lower-carbon alternatives for traditional petroleum-based coatings.

Regional production expansion is further supporting market growth. Mapei’s expansion of Mapefloor™ production in Southeast Asia (November 2025) enhances capacity for skid-resistant and chemical-resistant coatings, tailored for humid and tropical environments.

Market Trend: Polyaspartic Coatings Driving Rapid Return-to-Service and Lifecycle Efficiency in Parking Deck Applications

The parking deck coatings industry is undergoing a decisive transition toward fast-cure polyaspartic coating systems as asset owners prioritize return-to-service metrics and revenue continuity. Traditional epoxy-based systems, while historically dominant, are increasingly being replaced due to their extended curing timelines and susceptibility to UV degradation in exposed environments.

Polyaspartic coatings deliver a substantial improvement in curing speed, achieving approximately 90% faster cure rates compared to conventional epoxy systems. Industry benchmarks indicate that treated surfaces can be reopened to vehicular traffic within 24 hours, compared to the typical 3 to 5 day downtime associated with epoxy coatings. This rapid turnaround is critical for commercial parking structures, where prolonged closures directly impact revenue generation and operational efficiency.

Lifecycle performance advantages further reinforce adoption. Polyaspartic systems exhibit superior UV stability, preventing the yellowing and embrittlement commonly observed in epoxy topcoats exposed to sunlight. This stability translates into a 40% reduction in maintenance requirements over a 15-year lifecycle, lowering total cost of ownership for facility operators. Additionally, these coatings maintain high abrasion resistance and chemical durability, ensuring long-term protection against vehicular traffic, oil exposure, and environmental wear. The combination of fast application, reduced downtime, and extended durability is positioning polyaspartic coatings as a preferred solution in modern parking deck rehabilitation and construction projects.

Market Trend: Polyurea Membrane Technologies Enhancing Cold-Climate Durability and Waterproofing Performance

In regions characterized by extreme temperature fluctuations and heavy use of deicing salts, polyurea-based waterproofing membranes are gaining significant traction in parking deck coatings. These systems are engineered to deliver high elasticity and chemical resistance, addressing the primary causes of structural degradation in reinforced concrete decks.

Polyurea membranes provide exceptional corrosion protection by acting as a barrier against chloride ion ingress, a leading factor in rebar corrosion. Advanced formulations demonstrate resistance exceeding 5,000 hours in Neutral Salt Spray testing, maintaining adhesion and structural integrity under aggressive environmental conditions. This level of performance is essential for infrastructure exposed to repeated freeze-thaw cycles and salt-laden runoff.

Thermal flexibility is another defining characteristic. Modern polyurea coatings maintain elongation properties between 250% and 400% even at temperatures as low as minus 40 degrees Fahrenheit. This allows the membrane to accommodate dynamic cracking caused by thermal contraction and expansion without compromising waterproofing performance. The ability to bridge cracks and maintain continuity under stress makes polyurea systems particularly suitable for cold-climate parking structures.

These coatings also exhibit rapid curing characteristics and high impact resistance, enabling efficient application in challenging environments. As infrastructure owners increasingly focus on durability and long-term asset protection, polyurea membrane technologies are becoming integral to advanced parking deck coating strategies.

Market Opportunity: FHWA Infrastructure Funding Driving Demand for High-Durability Parking Deck Coatings in the United States

The expansion of infrastructure funding through the Federal Highway Administration is creating a substantial growth opportunity for parking deck coatings. The FY 2026 allocation under the Bridge Formula Program, totaling 5.5 billion dollars, combined with targeted funding under the Bridge Investment Program, is accelerating rehabilitation and preservation projects across aging infrastructure networks.

A significant portion of this funding, approximately 2.5 billion dollars, is specifically directed toward preservation and protection initiatives. This includes parking structures that are often integrated within broader transportation infrastructure systems. Coating technologies capable of extending service life to 50 years are receiving priority consideration in state and municipal project proposals, particularly those aligned with durability and sustainability criteria.

This funding environment is encouraging the adoption of high-performance coating systems such as polyaspartic and polyurea technologies, which offer extended lifecycle performance and reduced maintenance requirements. Manufacturers that can demonstrate compliance with federal durability standards and provide validated performance data are well positioned to secure contracts within publicly funded infrastructure projects.

Market Opportunity: China Mandatory Waterproofing Standards Accelerating Adoption of Advanced Deck Coatings in Urban Development Projects

China’s regulatory framework for construction materials is creating a large-scale opportunity for advanced parking deck coatings, driven by mandatory standards introduced by the Ministry of Housing and Urban-Rural Development and the Ministry of Industry and Information Technology. The implementation of updated GB 30981 standards in 2026 imposes stricter limits on hazardous substances in floor coatings, requiring compliance with environmental and safety thresholds related to formaldehyde and heavy metals.

These regulations are particularly impactful in urban renewal and infrastructure development projects, where compliance is mandatory for material approval. Coating manufacturers must now provide formulations that meet stringent emission and toxicity criteria while maintaining high performance in terms of durability and slip resistance.

In parallel, the national urban development strategy for 2026 to 2030 mandates integrated waterproofing and anti-slip coating systems for all new underground parking facilities. This requirement addresses long-standing issues related to groundwater ingress and structural deterioration, creating demand across millions of square meters of new construction in major metropolitan regions.

The scale of urban expansion in Tier 1 and Tier 2 cities, combined with regulatory enforcement, is driving rapid adoption of advanced coating technologies. Suppliers offering compliant, high-performance waterproofing and protective systems are positioned to capture significant growth opportunities in China’s evolving construction and infrastructure market.

Parking Deck Coatings Market Share and Segmentation Insights

Topcoats Capture 38.1% Share Driven by Abrasion Resistance and Safety Requirements

The parking deck coatings market by system layer is led by topcoats, accounting for 38.1% of total market share in 2025, due to their critical role in delivering final surface protection and performance. Parking deck topcoats—primarily based on polyurethane, epoxy, and MMA coatings—are engineered to withstand heavy tire abrasion, oil and gasoline exposure, deicing salts, and continuous UV radiation, making them indispensable for long-term durability. Beyond protection, topcoats serve essential aesthetic and safety functions, including color-coded parking zones, traffic lane markings, and slip-resistant aggregate broadcast systems. These features are crucial for ensuring pedestrian safety and traffic management in high-traffic commercial and residential parking structures. As infrastructure modernization and multi-level parking construction expand globally, demand for high-performance parking deck topcoat systems continues to drive growth in the protective coatings market.

Contractors Hold 58.3% Share Due to Technical Application and Warranty Requirements

In the parking deck coatings market by sales channel, professional coating contractors dominate with a 58.3% market share in 2025, reflecting the complexity of multi-layer coating system application. Parking deck coatings require meticulous surface preparation techniques such as shot blasting, scarifying, moisture testing, and crack repair, followed by precise application of primers, basecoats, and topcoats—processes that demand specialized expertise. Contractors provide end-to-end turnkey solutions, ensuring optimal adhesion, durability, and performance under demanding conditions. Additionally, liability and warranty requirements are a major driver of this segment, as property owners and developers typically require 5–10 year performance guarantees against issues like delamination, blistering, and chemical degradation. This shifts operational risk to certified professionals, reinforcing contractor dominance in the global parking structure coatings market.

Competitive Landscape of the Parking Deck Coatings Market

Sika Leads High-Performance Parking Deck Coatings with Rapid-Cure and Digital Monitoring Technologies

Sika AG remains the global leader in the parking deck coatings market, leveraging its expertise in structural waterproofing and advanced flooring systems. In 2026, the company projected an EBITDA margin of up to 20%, supported by steady growth despite challenging market conditions. Its Sikafloor® systems utilize PMMA-based rapid curing technology, enabling application in under one hour, even in sub-zero temperatures—critical for minimizing downtime in urban garages. Sika’s launch of the CarPark digital twin platform integrates IoT sensors for real-time monitoring of deck wear and chloride penetration. This combination of fast-curing coatings and smart infrastructure solutions positions Sika at the forefront of next-generation parking deck technologies.

Sherwin-Williams Strengthens North American Leadership with High-Durability Deck Systems

The Sherwin-Williams Company is a dominant player in the parking deck coatings market, particularly in North America, through its Resudeck™ portfolio. Its Resudeck™ IV system combines elastomeric urethane and epoxy technologies to deliver superior thermal stability and freeze-thaw resistance, making it ideal for harsh climates. In 2026, the company reinforced its growth outlook with strong Performance Coatings Group expansion. Sherwin-Williams has also integrated Pro-Park™ traffic paints into its deck systems, offering a comprehensive solution for protective membranes and safety markings, including EV charging zones. Its “Success by Design” platform further enhances its competitive edge by providing digitally optimized coating specifications.

Master Builders Solutions Sets Benchmark with Polyaspartic and Hybrid Deck Coating Systems

Master Builders Solutions, now part of the Sika-MBCC integration, continues to lead innovation in polyaspartic and hybrid parking deck coatings. Its MasterSeal® Traffic systems are widely recognized as the industry standard for high-traffic environments, delivering seamless waterproof membranes that protect reinforced concrete from corrosion. In 2026, the company introduced MasterSeal® 6100 FX, a lightweight membrane that reduces material usage by 15% while maintaining performance. Its expansion in China supports growth in high-density residential infrastructure. Known for exceptional chemical resistance, Master Builders Solutions offers coatings capable of withstanding battery acid runoff and industrial fluid exposure, reinforcing its leadership in durable deck protection.

Tremco Expands Integrated Building Envelope Solutions for Parking Deck Protection

Tremco CPG Inc. is a key innovator in the parking deck coatings industry, focusing on integrated building envelope solutions. Its Vulkem® Pro Series coatings, introduced in 2026, feature high-solids, low-VOC formulations that adhere effectively to damp concrete, reducing surface preparation time by 20%. Tremco’s ability to provide a total building envelope warranty ensures seamless integration between deck coatings, air barriers, and waterproofing systems. The company has also expanded its restoration services with thermal imaging technologies to detect hidden moisture issues. Tremco is particularly strong in multi-unit residential developments, where low-odor, fast-curing coatings are essential for occupant convenience.

Mapei Leads Sustainable Parking Deck Coatings with Eco-Friendly and High-Performance Systems

Mapei S.p.A. is a leading player in the sustainable parking deck coatings market, particularly across Europe and the Mediterranean region. In 2026, the company saw a 22% increase in adoption of waterborne coatings due to stringent environmental regulations. Its Mapefloor™ Parking System delivers high slip resistance and abrasion durability, making it ideal for high-traffic applications. Mapei has also completed major infrastructure projects, including airport parking facilities in the Middle East, using UV-stable coatings designed for extreme climates. With a focus on EV infrastructure, the company is developing cool roof deck coatings that reduce heat absorption and improve energy efficiency in outdoor parking environments.

United States: Sun Belt Expansion and VOC-Driven Innovation

The United States leads the parking deck coatings market, driven by rapid urbanization in the Sun Belt region and strict environmental regulations. States such as Texas, Florida, and Arizona account for nearly 35% of national construction activity, fueling demand for heat-reflective and cool-deck coatings that mitigate urban heat island effects in large parking structures.

Regulatory pressure has accelerated the shift toward waterborne technologies, which now represent approximately 87% of the market, replacing solvent-based systems to meet stringent VOC limits. Growth in e-commerce logistics hubs is increasing demand for high-build, abrasion-resistant epoxy coatings in loading docks and high-traffic ramps.

Technological innovation includes the adoption of fast-curing polyaspartic systems, particularly in colder regions, enabling rapid repair cycles with minimal downtime. Additionally, rising residential remodeling expenditure—projected at $509 billion in 2025—is boosting demand for DIY-friendly decorative deck coatings, reinforcing the U.S. position as a leader in performance-driven and regulatory-compliant solutions.

China: Smart City Development and Dual-Carbon Transformation

China remains the largest market for parking deck coatings, driven by large-scale infrastructure expansion and alignment with its “dual-carbon” sustainability goals. The introduction of GB 30981.1-2025 standards, capping VOC levels, is accelerating the shift toward eco-friendly, waterborne coating systems.

Innovation is centered on thermal insulation technologies, such as AkzoNobel’s radiative cooling coating system, which reduces surface temperatures by up to 10%. China is also pioneering liquid stone coatings, offering a lightweight alternative to natural stone and reducing structural weight by up to 75%.

Massive investments in Transit-Oriented Development (TOD) are driving demand for high-performance polyaspartic coatings in multi-modal transit hubs. Additionally, mandates for photovoltaic-ready reflective coatings on parking structures are integrating solar capabilities into infrastructure, reinforcing China’s leadership in sustainable urban development.

Germany: Energy-Efficient Retrofits and Circular Coating Systems

Germany is leading Europe’s transition toward energy-efficient and sustainable parking deck coatings, supported by government funding programs such as BEG and KfW, which allocated over €2.1 billion for building refurbishments. These initiatives are driving demand for thermal-insulating and high-performance deck coatings.

The market is characterized by a strong shift toward waterborne coatings, which now hold over 85% market share, reflecting compliance with strict EU VOC and biocide regulations. Growth in prefabricated construction is also increasing demand for factory-applied UV-curable coatings, improving efficiency and reducing on-site application time.

Emerging applications include hydrogen-resistant coatings for specialized parking facilities supporting fuel-cell infrastructure. Additionally, the integration of AI-driven color visualization platforms is enhancing workflow efficiency in urban redevelopment projects, reinforcing Germany’s leadership in sustainable and technologically advanced coatings.

India: Smart City Expansion and Emerging Premium Segment

India is a high-growth market for parking deck coatings, driven by rapid urbanization and government initiatives such as the Smart Cities Mission and PMAY-U housing programs. The broader coatings market is projected to reach INR 2.29 trillion by 2030, with parking deck coatings emerging as a niche high-margin segment.

Urban consumers are increasingly opting for premium, durable, and easy-to-clean coatings, particularly in metropolitan areas like Mumbai and Bengaluru. Innovations in smart coatings, offering temperature regulation and air purification, are gaining traction in commercial real estate projects.

Infrastructure development, including multi-modal logistics parks along the Delhi-Mumbai Industrial Corridor, is driving demand for heavy-duty industrial deck coatings. At the same time, government housing initiatives continue to support adoption of cost-effective water-based acrylic coatings in residential parking zones, balancing affordability with performance.

South Korea: EV Infrastructure and High-Tech Coating Integration

South Korea is emerging as a key market driven by its leadership in EV infrastructure and advanced materials innovation. The EV charging infrastructure market, projected to reach $704.7 million by 2025, is creating demand for fire-retardant and chemical-resistant coatings in parking facilities.

Technological crossovers from the electronics industry are enabling the adoption of Thin-Film Encapsulation (TFE) techniques in high-performance coatings, enhancing durability and precision. South Korea is also leveraging retort pouch adhesion technologies to develop advanced waterproofing membranes for parking decks exposed to extreme conditions.

Sustainability initiatives include the use of biocide-free coatings in coastal infrastructure, while premium urban projects are incorporating sensory-effect coatings for aesthetic enhancement. Government R&D incentives for next-generation materials are further accelerating innovation in low-voltage plasma-deposited coatings for smart parking systems.

Japan: Infrastructure Renewal and Smart Coating Technologies

Japan’s parking deck coatings market is driven by infrastructure renewal and advanced material science, focusing on extending asset life and improving environmental performance. Advanced coatings are capable of extending concrete deck lifespans by up to 30 years, reducing long-term maintenance costs.

Innovations include reflective thermal coatings designed to reduce ambient temperatures in parking garages, minimizing thermal stress on EV batteries. Japan is also leading in photocatalytic coatings, which actively decompose pollutants such as NO₂ in enclosed parking environments.

The market is characterized by a strong preference for low-VOC, water-based coatings, supported by government policies promoting sustainable construction. Additionally, nano-silica reinforced coatings are improving durability in high-traffic areas, while smart city initiatives are integrating predictive maintenance sensors beneath coating layers, enhancing operational efficiency.

Canada: Cold Climate Innovation and Sustainable Construction Growth

Canada’s parking deck coatings market is shaped by extreme climate conditions and a strong renovation sector. The adoption of low-temperature curing coatings, capable of application at temperatures as low as -5°C, is extending construction seasons in northern regions.

The country is also experiencing growth in mass-timber construction, following updates to the National Building Code allowing taller wood structures. This is driving demand for fire-resistant and breathable coatings that protect timber aesthetics in integrated parking facilities.

Strict VOC regulations, with limits of 150 g/L or lower, are accelerating the adoption of environmentally friendly formulations. Additionally, increasing renovation activity—where average household spending has doubled—has boosted demand for surface-tolerant primers and durable coatings for aging infrastructure. Emerging projects involving Indigenous-led construction are further supporting the adoption of bio-based coatings, reinforcing sustainability trends in the Canadian market.

Parking Deck Coatings Market Report Scope

Parking Deck Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$270 Million

|

|

Market Size (2032)

|

$436.4 Million

|

|

Market Growth Rate

|

7.1%

|

|

Segments

|

By Resin Type (Polyurethane, Epoxy, Polyaspartic, Methyl Methacrylate, Polyurethane-Methacrylate, Acrylic, Polyurea, Cementitious and Hybrid Systems), By Technology (Single-Component, Double-Component, Triple-Component), By System Layer (Primers, Basecoats, Intermediate, Topcoats), By Application Area (Internal, Exposed, Ramps and Turning Circles, Walkways and Pedestrian Areas), By Project Type (New Construction, Renovation and Maintenance), By Substrate (Concrete, Asphalt, Metal), By End-Use Sector (Commercial, Residential, Municipal and Infrastructure, Industrial, Specialty), By Performance Property (Crack-Bridging Ability, Slip Resistance, Chemical and Oil Resistance, Thermal Stability, Fire Resistance), By Sales Channel (Direct Sales, Specialty Construction Chemical Distributors, Professional Coating Contractors)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sika AG, Tremco Incorporated, The Sherwin-Williams Company, BASF SE, MAPEI S.p.A., Stonhard, PPG Industries, Inc., Akzo Nobel N.V., LATICRETE International, Inc., Jotun A/S, Tennant Coatings, Dur-A-Flex, Inc., Fosroc International Ltd., Sto SE and Co. KGaA, KCC Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Parking Deck Coatings Market Segmentation

By Resin Type

- Polyurethane

- Epoxy

- Polyaspartic

- Methyl Methacrylate

- Polyurethane-Methacrylate

- Acrylic

- Polyurea

- Cementitious and Hybrid Systems

By Technology

- Single-Component

- Double-Component

- Triple-Component

By System Layer

- Primers

- Basecoats

- Intermediate

- Topcoats

By Application Area

- Internal

- Exposed

- Ramps and Turning Circles

- Walkways and Pedestrian Areas

By Project Type

- New Construction

- Renovation and Maintenance

By Substrate

By End-Use Sector

- Commercial

- Residential

- Municipal and Infrastructure

- Industrial

- Specialty

By Performance Property

- Crack-Bridging Ability

- Slip Resistance

- Chemical and Oil Resistance

- Thermal Stability

- Fire Resistance

By Sales Channel

- Direct Sales

- Specialty Construction Chemical Distributors

- Professional Coating Contractors

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Parking Deck Coatings Industry

- Sika AG

- Tremco Incorporated

- The Sherwin-Williams Company

- BASF SE

- MAPEI S.p.A.

- Stonhard

- PPG Industries, Inc.

- Akzo Nobel N.V.

- LATICRETE International, Inc.

- Jotun A/S

- Tennant Coatings

- Dur-A-Flex, Inc.

- Fosroc International Ltd.

- Sto SE & Co. KGaA

- KCC Corporation

*- List not Exhaustive