Passive Fire Protection Coatings Market Size, Intumescent Technology Adoption, and Infrastructure Safety Mandates

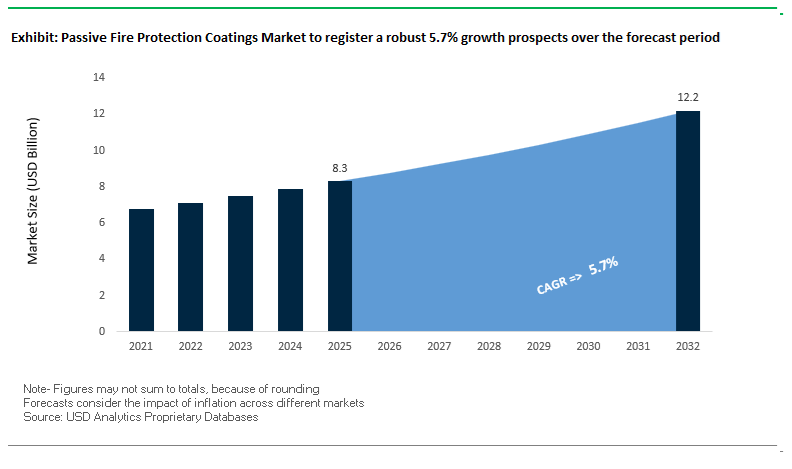

The global Passive Fire Protection (PFP) Coatings Market was valued at $8.3 billion in 2025 and is projected to expand at a CAGR of 5.7% through 2032, reaching $12.2 billion by 2032. This growth trajectory reflects the increasing prioritization of fire safety compliance, asset integrity, and risk mitigation across industries such as oil and gas, construction, transportation, and high-tech manufacturing.

A primary growth driver is the tightening of global fire safety regulations and building codes, particularly for high-rise structures, energy infrastructure, tunnels, and industrial facilities. Passive fire protection coatings, especially intumescent and cementitious systems, are essential for protecting structural steel from collapse during fire exposure by providing thermal insulation and load-bearing preservation. This is particularly critical in hydrocarbon fire scenarios, where temperatures escalate rapidly and demand specialized high-performance coatings.

Technological advancements are accelerating the adoption of epoxy-based and waterborne intumescent coatings, offering improved durability, reduced application thickness, and enhanced environmental performance. Modern PFP systems are increasingly designed to deliver multi-functional benefits, including corrosion resistance, mechanical strength, and simplified application processes. The shift toward high-build, single-coat systems is also reducing installation time and lifecycle costs, which is a critical factor in large-scale infrastructure and energy projects.

Additionally, the market is benefiting from rising investments in LNG terminals, offshore platforms, renewable energy infrastructure, data centers, and EV manufacturing facilities, all of which require stringent fire protection measures. Regional demand is particularly strong in the Middle East and Asia-Pacific, where rapid industrialization and urbanization are driving large-scale construction and energy projects.

Market Analysis: Epoxy PFP Innovation, Faster Application Systems, and Regulatory Compliance Driving Market Evolution

Recent developments in the Passive Fire Protection Coatings Market highlight a strong focus on advanced epoxy technologies, application efficiency, and regulatory alignment. In October 2025, AkzoNobel launched Chartek® ONE, a next-generation epoxy PFP coating designed as a single-coat, mesh-free solution for high-risk energy infrastructure. This innovation significantly reduces installation complexity and labor requirements while maintaining stringent fire protection standards for LNG and offshore assets.

Building on this, AkzoNobel introduced Chartek® 2218E (November 2025), engineered to halve application time compared to conventional systems while meeting rigorous hydrocarbon fire protection requirements. These developments underscore the industry’s shift toward high-efficiency, labor-saving coating technologies.

Performance enhancement remains a key competitive focus. Jotun’s Jotachar 1709XT, certified to the UL 1709 standard, is specifically designed for extreme environments, offering enhanced durability and mechanical strength for steel infrastructure in energy-intensive regions. Similarly, PPG’s expanded PITT-CHAR® NX product line (January 2026) introduces faster-curing intumescent coatings with improved corrosion resistance, addressing the dual challenges of fire protection and harsh marine exposure.

Sustainability and environmental compliance are increasingly influencing product development. Hempel’s Hempafire Extreme 550, launched in March 2025, is a solvent-free, high-build epoxy PFP coating that reduces embedded carbon by up to 40% while delivering up to four hours of fire resistance. In parallel, Nippon Paint’s water-based intumescent coating (February 2026) targets urban markets in Asia, aligning with stricter regulations on solvent-based materials in densely populated regions.

Application-specific innovation is also expanding the market scope. Sherwin-Williams’ advanced FIRETEX® coatings enable thinner film applications for complex architectural steel designs, while Isolatek’s FireSolve SB addresses the unique requirements of data centers and EV battery facilities, combining high fire ratings with smooth finishes. Meanwhile, Carboline’s enhanced cementitious fireproofing solutions improve application efficiency for large-scale commercial construction projects.

Market Trend: Clear Intumescent Coatings Enabling Fire-Safe Mass Timber Construction with Aesthetic Preservation

The passive fire protection coatings industry is evolving rapidly with the emergence of clear intumescent coatings tailored for mass timber construction, particularly cross-laminated timber high-rise structures. As architectural trends emphasize biophilic design and exposed wood aesthetics, traditional opaque fireproofing systems are being replaced by transparent, waterborne intumescent coatings that deliver both fire resistance and visual clarity.

Advanced clear intumescent coatings now achieve Euroclass B-s1, d0 classification under EN 13501-1 at application rates around 350 g/m², ensuring minimal contribution to flame spread and smoke generation. This level of performance is critical for meeting stringent fire safety regulations in modern timber buildings while preserving design intent. In structural fire testing, treated CLT panels demonstrate a 25% reduction in charring rates, decreasing from approximately 0.65 mm per minute to below 0.5 mm per minute during the first hour of fire exposure. This reduction significantly enhances load-bearing retention, providing crucial time for evacuation and emergency response.

Durability and long-term appearance have also improved. New-generation formulations exhibit a Yellowing Index below 2 after extended UV exposure of 1,000 hours, addressing a key limitation of earlier clear coatings that suffered from discoloration in sunlit environments. These advancements are enabling broader adoption of timber-based construction in urban settings, positioning clear intumescent coatings as a critical technology in sustainable building design and fire safety compliance.

Market Trend: Epoxy Intumescent Coatings Advancing Jet Fire Protection in LNG and Energy Infrastructure

In the energy sector, passive fire protection coatings are undergoing a shift toward high-performance systems designed to withstand jet fire scenarios in liquefied natural gas facilities and hydrocarbon processing environments. Unlike conventional pool fires, jet fires generate extreme localized heat flux levels exceeding 250 to 300 kilowatts per square meter, requiring coatings with superior thermal insulation and mechanical stability.

Epoxy-based intumescent coatings are engineered to maintain structural steel temperatures below the critical threshold of 400°C for durations exceeding 120 minutes under jet fire exposure conditions. This capability is essential for preventing structural collapse in high-risk environments such as LNG terminals, offshore platforms, and gas processing facilities.

Mechanical integrity under stress is equally important. Next-generation jet fire-rated coatings, including J60 and J120 classifications, must demonstrate pull-off adhesion strength greater than 3 MPa after environmental aging, ensuring that the coating remains intact under the erosive forces of high-pressure gas jets. This performance requirement is driving innovation in binder chemistry and reinforcement technologies within epoxy intumescent systems.

Weight optimization is also a key trend. Modern formulations achieve a 15% to 20% reduction in dry film thickness while maintaining equivalent fire resistance ratings, reducing the overall dead load on large infrastructure components such as storage tanks and piping systems. These advancements are enhancing both safety and structural efficiency, reinforcing the role of advanced intumescent coatings in critical energy infrastructure protection.

Market Opportunity: FEMA BRIC Funding Accelerating Adoption of Fire-Resistant Coatings in Wildfire-Prone Infrastructure

The expansion of funding under the Building Resilient Infrastructure and Communities program is creating a significant opportunity for passive fire protection coatings in wildfire mitigation applications. With a funding pool of approximately 1 billion dollars announced in 2026, and a dedicated allocation of around 81 million dollars for building code adoption and enforcement, the program is driving investment in fire-resistant infrastructure across high-risk regions.

The availability of a 75% federal cost-share significantly reduces financial barriers for municipalities and public agencies, encouraging the adoption of intumescent coatings for critical assets such as wooden utility poles, bridges, and government buildings located in wildland-urban interface zones. These coatings play a crucial role in reducing ignition risk and slowing fire propagation, contributing to overall community resilience.

This funding framework is also influencing specification standards, with increased emphasis on coatings that demonstrate proven fire resistance performance under real-world wildfire conditions. Manufacturers that can provide validated testing data and compliance with evolving fire safety codes are well positioned to benefit from increased demand in publicly funded infrastructure projects.

Market Opportunity: China GB 50016-2026 Code Driving High-Performance Fire Protection Coatings in High-Rise Construction

China’s updated building fire code is creating a large-scale demand shift in the passive fire protection coatings market, particularly for high-rise steel structures. The revised GB 50016-2026 standard mandates that buildings exceeding 50 meters in height must utilize coatings capable of delivering a minimum of three hours of fire resistance for primary load-bearing elements.

This requirement significantly raises performance expectations and drives the adoption of advanced intumescent coatings with reliable expansion characteristics and consistent thermal insulation properties. The introduction of mandatory third-party ultrasonic thickness testing for a portion of the coated area further reinforces quality control, ensuring uniform application and eliminating the use of substandard low-build coatings.

Environmental compliance is also integrated into the regulatory framework. Coatings must meet VOC limits below 200 g/L for waterborne systems, aligning fire protection requirements with broader green building initiatives. This dual requirement is accelerating the development of high-solids epoxy and waterborne intumescent coatings that combine fire performance with environmental sustainability.

The scale of urban development in China, combined with stricter enforcement mechanisms, is creating substantial growth opportunities for manufacturers of high-performance passive fire protection coatings capable of meeting both safety and environmental standards.

Passive Fire Protection Coatings Market Share and Segmentation Insights

Repair and Retrofit Segment Captures 58.6% Share Driven by Aging Infrastructure and Fire Safety Upgrades

The passive fire protection (PFP) coatings market by project type is led by the repair and retrofit segment, accounting for 58.6% of market share in 2025, primarily due to the widespread need to upgrade aging infrastructure and ensure compliance with modern fire safety standards. Buildings constructed prior to the 2000s often lack adequate intumescent coatings or cementitious fireproofing systems, necessitating upgrades to meet regulations such as IBC (International Building Code) and Eurocode fire resistance requirements. Additionally, post-fire and water damage remediation projects require the removal and reapplication of passive fire protection coatings, generating consistent demand regardless of new construction cycles. As global focus intensifies on structural fire resistance, occupant safety, and regulatory compliance, retrofit applications remain the primary growth driver in the fireproof coatings and structural steel protection market.

Certified Applicators Hold 62.5% Share Due to Regulatory Requirements and Performance Assurance

In the passive fire protection coatings market by sales channel, certified PFP contractors and applicators dominate with a 62.5% market share in 2025, reflecting the critical importance of precision application and regulatory compliance. Passive fire protection coatings must meet strict specifications for dry film thickness (DFT), adhesion, and fire resistance ratings, which can only be reliably achieved by trained and certified professionals. Building owners, regulatory bodies, and insurers mandate certified applicators to mitigate liability risks and ensure compliance with safety codes, as improper application can lead to failed inspections and voided warranties. Furthermore, these contractors provide essential documentation and traceability, including DFT reports, environmental condition logs, and material certifications, which are required for occupancy permits and insurance underwriting. This makes certified contractors indispensable in the global fire protection coatings industry, reinforcing their dominant position in the distribution landscape.

Competitive Landscape of the Passive Fire Protection Coatings Market

AkzoNobel Leads Hydrocarbon Fire Protection with Advanced Intumescent Coating Technologies

AkzoNobel N.V., through its International® Protective Coatings brand, remains a global leader in hydrocarbon passive fire protection coatings, particularly for offshore and petrochemical industries. In 2026, the company launched Chartek 2218E, a boron-free epoxy intumescent coating capable of delivering a 2-hour hydrocarbon pool fire rating in a single-coat, mesh-free application, significantly reducing labor requirements. The company continues to optimize its portfolio by divesting non-core assets and focusing on high-growth marine and protective coatings markets. Its integrated “Total Asset Protection” approach combines anti-corrosive primers with fire protection coatings, ensuring C5-level corrosion resistance alongside fire safety performance.

PPG Expands Cellulosic Fire Protection Market with Sustainable Waterborne Coatings

PPG Industries, Inc. is a technological leader in cellulosic passive fire protection coatings, targeting high-rise construction and infrastructure projects. In 2026, the company launched PPG STEELGUARD® 652, a waterborne intumescent coating designed for interior structural steel, achieving UL 263 certification for up to two hours of fire resistance. This low-VOC formulation supports LEED and BREEAM certifications, aligning with global sustainability goals. PPG is focusing on improving construction efficiency through enhanced coating durability and faster application processes. Its strong performance in protective coatings, particularly in data centers and battery plants, reinforces its position in the global fire protection coatings market.

Sherwin-Williams Strengthens Global PFP Leadership with High-Solids Epoxy Systems

The Sherwin-Williams Company holds a dominant position in the passive fire protection coatings market, with 15% global market share. Its Firetex® and Phoenix™ product lines are widely used in construction and industrial applications. In 2026, the company expanded its Kentucky facility to increase production capacity for fire-rated building components. Its Firetex® M90 series is considered an industry benchmark for jet fire and cryogenic spill protection, offering up to 120 minutes of resistance in harsh oil and gas environments. Sherwin-Williams continues to benefit from strong growth in its Performance Coatings Group, driven by increasing global demand for high-performance fire-resistant coatings.

Hempel Drives Efficiency in Fire Protection Coatings with Reduced Thickness and Fast Curing Systems

Hempel A/S is a key innovator in the epoxy passive fire protection coatings market, focusing on efficiency and sustainability. Its Hempafire Extreme 550 system delivers up to 4 hours of fire resistance while reducing paint consumption by 40% compared to traditional coatings. The company’s 2026 product range is fully solvent-free, significantly lowering VOC emissions and carbon footprint. Hempel’s HEET Dynamic software enables engineers to optimize coating thickness in real time, improving project efficiency. Its coatings are designed for rapid handling, becoming service-ready within 24 hours, making them ideal for large-scale industrial projects requiring fast turnand high-performance fire protection.

Jotun Advances Offshore Fire Protection with Mesh-Free and High-Durability Intumescent Coatings

Jotun is a leading player in the hydrocarbon fire protection coatings market, particularly in offshore and marine applications. With a global market share of 12%, the company is focusing on advanced mesh-free coating technologies. Its Jotachar 1709 XT system is a high-build epoxy intumescent coating designed to withstand hydrocarbon pool and jet fires, featuring enhanced flexibility to resist mechanical and thermal stress. Jotun has expanded its presence in Asia-Pacific, which accounts for a significant share of global demand. Its coatings have been tested in extreme arctic conditions, ensuring consistent performance and fire resistance even after severe thermal cycling.

United States: E-Mobility Safety and Data Infrastructure Expansion

The United States is the global leader in advanced PFP coatings, driven by rapid investments in data centers, EV infrastructure, and energy storage systems (ESS). Tech giants such as Google and Amazon are collectively investing over $17 billion (2024–2026) in fire-resistant infrastructure, boosting demand for epoxy intumescent coatings that protect structural steel under extreme thermal conditions.

Regulatory transformation is accelerating innovation. The PFAS phase-out (2026) is driving a shift toward bio-based, halogen-free fire-retardant chemistries, while strict VOC regulations—especially in California—are pushing adoption of waterborne PFP coatings.

Technological advancements include integrated fire detection and suppression systems, highlighted by Honeywell’s acquisition of Li-ion Tamer, enabling enhanced safety for lithium-ion battery storage. Additionally, infrastructure investments under the IIJA are fueling demand for durable intumescent coatings in tunnels and transit hubs. New product innovations, such as Sherwin-Williams’ FIRETEX® FX7002, are combining low-VOC performance with architectural aesthetics, reinforcing U.S. leadership in high-performance fire protection solutions.

China: Industrial Scale and Smart Infrastructure Integration

China remains the largest global market for PFP coatings, supported by extensive industrialization and government-driven infrastructure expansion. The market is dominated by cementitious coatings, which accounted for nearly 48.87% of revenue, favored for their cost efficiency and high fire resistance in heavy industrial applications.

Regulatory reforms such as GB 30981.1-2025 are enforcing strict VOC limits, accelerating the shift toward waterborne and HEUR-modified PFP systems. China is also integrating plasma-enhanced coatings (PACVD) into semiconductor manufacturing, enabling fire-resistant thin films for advanced fabrication equipment.

The push toward green building certifications and smart city infrastructure is increasing adoption of PFP coatings in energy-efficient construction. With projections indicating the market could reach $1.5 billion by 2033, China continues to lead in both production capacity and technological adoption.

Germany: Circular Economy and Hydrogen Safety Innovation

Germany is the European leader in PFP coatings, driven by strict regulatory frameworks and a strong focus on circular economy principles. The transition to BS EN 13501 standards, fully implemented by 2026, is providing standardized fire performance metrics across construction projects.

The country’s energy transition is creating demand for PFP coatings in offshore wind infrastructure, requiring durability in C5-M corrosive environments with lifespans exceeding 25 years. Additionally, the PFAS foam ban (2026) is accelerating adoption of recyclable and low-impact intumescent systems.

Emerging applications include hydrogen infrastructure, where conductive fire-resistant coatings are being developed for fuel cell components. Innovations such as bio-based polyaspartic resins (e.g., Desmophen CQ NH) are further advancing sustainable fire protection technologies, reinforcing Germany’s leadership in environmentally compliant coatings.

India: Infrastructure Boom and Regulatory Alignment Driving Growth

India is a high-growth PFP coatings market, fueled by rapid urbanization and government initiatives such as the Smart Cities Mission and PMAY-U 2.0. These programs are driving widespread adoption of cost-effective water-based fire-retardant coatings in residential and commercial infrastructure.

Infrastructure expansion, particularly in metro rail systems and logistics corridors, is boosting demand for intumescent coatings offering up to 120 minutes of fire protection for structural steel. The Delhi-Mumbai Industrial Corridor is further driving demand for heavy-duty industrial PFP coatings in warehousing and logistics facilities.

Regulatory alignment with NFPA standards via BIS updates is ensuring improved safety compliance across public infrastructure projects. Product innovation, such as cool-roof fire-retardant coatings, is addressing both fire safety and urban heat challenges, positioning India as a rapidly evolving and opportunity-rich market.

United Kingdom: Regulatory Rigor and Digital Traceability Leadership

The United Kingdom is setting global benchmarks in PFP compliance and traceability, driven by post-Grenfell regulatory reforms. The updated Regulation 38 (2025/2026) mandates digital documentation of all fire protection systems, including precise coating specifications and performance data.

The transition from BS 476 to BS EN 13501 standards is reshaping the market, requiring updated testing and certification for all fire protection coatings. Additionally, mandatory integration of sprinkler systems in new care homes is increasing the complexity of fire safety strategies, driving demand for coatings that complement active systems.

Industry initiatives led by the Association for Specialist Fire Protection (ASFP) are improving quality standards and collaboration. Innovations such as advanced cavity fire barriers and increased M&A activity are strengthening the UK’s position as a leader in regulatory-driven fire protection solutions.

Japan: Advanced Materials and EV Thermal Protection

Japan’s PFP coatings market is driven by advanced material science and precision engineering, particularly in EV and infrastructure applications. The development of silicone elastomer coatings capable of withstanding temperatures above 600°C is transforming fire protection for EV battery systems.

Innovations include photocatalytic PFP coatings, which combine fire resistance with pollutant decomposition, improving indoor environmental quality. Japan is also advancing low-temperature curing technologies, reducing energy consumption and enabling application on heat-sensitive substrates.

The country’s aging infrastructure is driving demand for multi-functional coatings, combining fire resistance, seismic reinforcement, and durability. Additionally, the development of ultra-high-purity coatings for 6G infrastructure highlights Japan’s leadership in next-generation fire protection technologies.

South Korea: Semiconductor Safety and High-Tech Fire Protection

South Korea’s PFP coatings market is shaped by its dominance in semiconductors, electronics, and shipbuilding industries, requiring ultra-high-performance fire protection systems.

There is strong demand for anti-static (ESD) and fire-resistant coatings in semiconductor cleanrooms, where flammable gases are processed. Technological advancements include PACVD-based thin-film PFP coatings and low-voltage plasma deposition (<160V), enabling applications on delicate electronic substrates.

South Korea is also a leader in high-barrier retort coatings, adapted for fire protection in extreme thermal environments. In shipbuilding, intumescent epoxy coatings are being integrated into LNG carriers, providing up to four hours of fire protection. Additionally, premium sectors such as cosmetics are adopting fire-retardant sensory coatings, blending safety with aesthetics. These developments position South Korea as a leader in high-tech and precision fire protection solutions.

Passive Fire Protection Coatings Market Report Scope

Passive Fire Protection Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$8.3 Billion

|

|

Market Size (2032)

|

$12.2 Billion

|

|

Market Growth Rate

|

5.7%

|

|

Segments

|

By Product Type (Intumescent Coatings, Cementitious Coatings, Ablative Coatings, Hybrid and Nano-enhanced Coatings), By Technology (Water-borne, Solvent-borne, 100% Solids Epoxy, Reactive Systems), By Fire Scenario (Cellulosic Fire Protection, Hydrocarbon Fire Protection, Cryogenic Spill Protection), By Substrate (Structural Steel, Concrete, Wood and Timber, Specialty Substrates), By End-Use Industry (Building and Construction, Oil and Gas, Industrial and Manufacturing, Transportation and Aerospace, Energy and Power), By Project Type (New Construction, Repair and Retrofit), By Sales Channel (Direct Sales, Specialty Construction Chemical Distributors, Certified PFP Contractors and Applicators)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Sherwin-Williams Company, PPG Industries, Inc., Akzo Nobel N.V., Jotun A/S, Hempel A/S, Sika AG, RPM International Inc., Hilti Group, Etex Group, BASF SE, Kansai Paint Co., Ltd., Nippon Paint Holdings Co., Ltd., Teknos Group, Rudolf Hensel GmbH, Isolatek International

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Passive Fire Protection Coatings Market Segmentation

By Product Type

- Intumescent Coatings

- Cementitious Coatings

- Ablative Coatings

- Hybrid and Nano-enhanced Coatings

By Technology

- Water-borne

- Solvent-borne

- 100% Solids Epoxy

- Reactive Systems

By Fire Scenario

- Cellulosic Fire Protection

- Hydrocarbon Fire Protection

- Cryogenic Spill Protection

By Substrate

- Structural Steel

- Concrete

- Wood and Timber

- Specialty Substrates

By End-Use Industry

- Building and Construction

- Oil and Gas

- Industrial and Manufacturing

- Transportation and Aerospace

- Energy and Power

By Project Type

- New Construction

- Repair and Retrofit

By Sales Channel

- Direct Sales

- Specialty Construction Chemical Distributors

- Certified PFP Contractors and Applicators

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Passive Fire Protection Coatings Industry

- The Sherwin-Williams Company

- PPG Industries, Inc.

- Akzo Nobel N.V.

- Jotun A/S

- Hempel A/S

- Sika AG

- RPM International Inc.

- Hilti Group

- Etex Group

- BASF SE

- Kansai Paint Co., Ltd.

- Nippon Paint Holdings Co., Ltd.

- Teknos Group

- Rudolf Hensel GmbH

- Isolatek International

*- List not Exhaustive