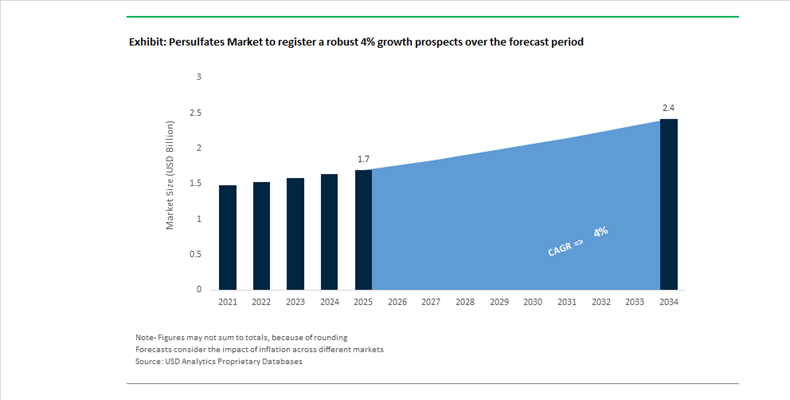

Persulfates Market Size 2025–2034: $1.7 Billion to $2.4 Billion at 4% CAGR Shaped by Trade Enforcement, Electronics Demand, and Sustainable Oxidation Technologies

The global persulfates market is projected to grow from $1.7 billion in 2025 to $2.4 billion by 2034, registering a CAGR of 4%. Market stability is supported by steady demand for sodium persulfate, ammonium persulfate, and potassium persulfate across polymerization initiators, printed circuit board etching, cosmetics, oil & gas stimulation, and in-situ chemical oxidation for groundwater remediation. Persulfates remain critical oxidizing agents in advanced materials manufacturing due to their strong free-radical generation capability, high purity grades, and compatibility with water-based systems.

Trade policy developments significantly reshaped North American market dynamics in February 2025 when the U.S. Department of Commerce and the International Trade Commission reaffirmed antidumping duties on persulfates imported from China. The ruling cited the likelihood of material injury to domestic producers if duties were revoked, effectively preserving pricing discipline for U.S.-based manufacturers of sodium and ammonium persulfates. This decision tightened competitive access for Chinese exporters and reinforced regional sourcing strategies among resin producers and electronics manufacturers. In Australia and New Zealand, United Initiators announced in January 2026 a transition to a distribution-led model by appointing Redox Ltd as its authorized distributor. The pivot enhances logistics efficiency and local inventory management for polymer and mining customers, strengthening supply chain resilience in the ANZ region.

Sustainability credentials and operational efficiency are increasingly central to competitive differentiation. In November 2025, United Initiators secured the EcoVadis Silver Medal for the second consecutive year, improving its sustainability score to 76 points and ranking in the 93rd percentile of its industry. Earlier in July 2025, the company was recognized by allnex as Supplier of the Year for reliable delivery of ammonium and potassium persulfates used in industrial resin polymerization. These recognitions reinforce the importance of ethical sourcing, carbon intensity reduction, and supply chain risk management in contract negotiations with coatings and adhesive producers. Evonik, which manages persulfates within its Active Oxygens business, confirmed in February 2026 that its “Tailor Made” restructuring program is stabilizing margins through hierarchy reduction and global workforce optimization. The company also introduced a dynamic dividend policy targeting a 40% to 60% payout ratio, enabling reinvestment into sustainable sodium persulfate production technologies.

Electronics sector expansion continues to support high-purity persulfate demand. In November 2025, Mitsubishi Gas Chemical completed capacity expansion at its overseas electronic materials subsidiary, strengthening supply of high-grade etching agents for next-generation printed circuit board manufacturing. In parallel, Adeka Corporation announced construction of a new specialty plant in October 2025 as part of a broader integration strategy linking commodity chemicals, including persulfates, with functional polymers serving EUV lithography and semiconductor fabrication markets. These moves signal alignment between oxidizing agents and advanced electronics materials ecosystems. In February 2026, Mitsubishi Chemical Group’s strategic withdrawal from its coke and carbon materials business freed capital for reinvestment into performance chemicals and polymer catalyst segments where persulfates function as essential initiators.

Environmental remediation technologies are evolving to extend application depth. In early 2024, environmental engineering firms introduced long-release persulfate gel systems for groundwater treatment. These controlled-release formulations enable sustained oxidation of soil contaminants while reducing the frequency of re-injection, aligning with tightening environmental compliance standards for industrial brownfield sites. Innovation momentum also accelerated in January 2025 when Arxada, integrating PeroxyChem’s persulfate portfolio, reported doubling its patent filings in 2024, focusing on stabilized oxidative formulations for microbial control and wood protection systems.

Structural Trends and Growth Opportunities Reshaping the Global Persulfates Market

Capacity Consolidation and Geographic Realignment Under Green and Safety Mandates

The persulfates market is entering a decisive phase of supply-side restructuring, driven primarily by environmental compliance, process safety regulation, and digital oversight requirements. Across Asia-Pacific, especially in China, persulfate production is no longer viable for small, non-integrated plants operating legacy batch processes. The implementation of China’s GB 45673-2025 national safety standard, effective November 1, 2025, mandates intelligent safety systems, real-time monitoring, and automated risk controls for hazardous chemical manufacturing. These requirements are accelerating the shutdown of sub-scale persulfate units that cannot justify the required capital expenditure, resulting in rapid capacity consolidation among Tier-1, integrated producers.

This regulatory tightening is simultaneously reshaping global trade flows. European producers are repositioning away from commodity-grade persulfates toward high-purity, low-impact products aligned with EU REACH 2024–2025 sustainability thresholds. Companies such as Evonik, following its acquisition of PeroxyChem, and United Initiators are leveraging this transition to differentiate European supply as the preferred option for ESG-driven polymer, electronics, and specialty chemical customers. Rather than competing on volume, European capacity is increasingly optimized for consistency, traceability, and regulatory certainty.

In parallel, Asia is undergoing selective capacity realignment rather than outright contraction. Expansion plans announced by United Initiators during 2024–2025 in India and China are focused on high-purity persulfates for specialty polymerization and semiconductor applications. This reflects a clear bifurcation of the market: bulk oxidation-grade persulfates face margin pressure, while specialty grades benefit from tighter supply and premium pricing. As a result, geographic production is becoming more polarized, with specialty-grade capacity clustering near advanced manufacturing hubs rather than low-cost export zones.

Shift Toward Engineered Initiators for Precision Polymerization

Demand-side dynamics in the persulfates market are shifting decisively from bulk oxidizing agents to engineered initiator systems designed for advanced polymer architectures. Persulfates are increasingly specified as precision redox initiators in emulsion polymerization processes, particularly for water-based coatings, adhesives, specialty elastomers, and high-performance plastics. Polymerization now represents the single largest application segment, accounting for approximately 40% of global persulfate consumption in 2024–2025.

This transition is being reinforced by the growing need for ultra-clean chemistries in electronics and semiconductor manufacturing. In 2024, PeroxyChem under Evonik introduced semiconductor-grade sodium persulfate products engineered to maintain metal-ion contamination at sub-parts-per-billion levels. These grades are critical for wafer etching and cleaning processes, where even trace impurities can compromise yields at advanced logic nodes. The premium attached to such specifications is materially higher than that of conventional industrial persulfates, improving overall market value even as volumes remain controlled.

Collaborative R&D is also reshaping how persulfates are sold and applied. Rather than supplying standardized initiators, producers are co-developing tailored redox systems with downstream customers to fine-tune molecular weight distribution, reaction kinetics, and end-use performance. In 2024, AkzoNobel launched a new portfolio of low-impact persulfates designed specifically for waterborne polymer systems. This reflects a broader shift toward application-driven chemistry, where persulfates are positioned as enabling materials for VOC reduction, regulatory compliance, and advanced material performance rather than interchangeable oxidants.

In-Situ Chemical Oxidation for Publicly Funded Environmental Remediation

One of the most structurally attractive opportunities for the persulfates market lies in environmental remediation, particularly In-Situ Chemical Oxidation (ISCO). Regulatory agencies are increasingly moving away from excavation-based remediation toward subsurface treatment technologies that permanently destroy contaminants. Sodium persulfate has emerged as the preferred oxidant for ISCO due to its stability in groundwater and its ability to generate highly reactive sulfate radicals when activated.

In the United States, the expansion of the Superfund program by the U.S. Environmental Protection Agency in July 2025, including new additions to the National Priorities List, has significantly expanded the pipeline of funded groundwater cleanup projects. Field data from 2025 remediation sites confirm that activated sodium persulfate can achieve up to 95% removal of chlorinated VOCs such as chlorobenzene and trichloroethylene, making it a core reagent in modern remediation strategies.

Technological innovation is further strengthening this opportunity. Sustained-release persulfate delivery systems, such as sodium persulfate rods evaluated in NIH-funded studies during 2025, enable long-term contaminant oxidation in low-permeability soils. These systems reduce the need for repeated injections, lowering total project costs and improving treatment reliability. In Europe, the IMPEL Water and Land Remediation initiative is actively promoting ISCO over pump-and-treat methods, creating a steady, regulation-backed demand base for bulk sodium persulfate across multiple EU member states.

Enabling High-Performance Acrylic Fibers for Carbon and Protective Textiles

The persulfates market is also benefiting from structural growth in advanced fiber applications, particularly acrylic fibers used as carbon fiber precursors and flame-resistant textiles. Carbon fiber production requires exceptional control over polymer chain length and composition, with acrylonitrile content typically ranging from 93% to 99.4%. Patent and process data from 2024 confirm that persulfate-based redox initiation systems remain the industry standard for achieving the molecular uniformity needed to prevent filament fusion during high-temperature carbonization.

Growth in flame-resistant and modacrylic textiles is reinforcing this demand. Persulfates enable the controlled copolymerization of acrylonitrile with vinyl monomers, imparting UV resistance, dimensional stability, and decay resistance to protective fabrics used in industrial workwear and outdoor applications. Recent innovations in polymer precursor design have also leveraged water-soluble persulfate initiators to achieve hot-wet elongation below 9% at 70°C, a critical performance metric for filtration media and technical textiles.

As global investment in carbon fiber capacity accelerates across aerospace, wind energy, and hydrogen infrastructure, persulfate consumption linked to acrylic precursor production is expected to grow disproportionately relative to overall market volumes. This positions persulfates not only as a mature industrial chemical but as a strategic enabler of next-generation materials with long-term demand visibility.

Persulfates Market Share and Segmentation Insights

Sodium Persulfate Leads Market Demand in Polymer Initiation and Environmental Oxidation Processes

Sodium persulfate accounted for 42.80% of the Persulfates Market by type in 2025, reflecting its strong adoption across polymer manufacturing and environmental remediation applications. This persulfate salt provides high solubility, stable storage characteristics, and cost efficiency that support large-scale use in emulsion polymerization processes for synthetic rubber, latex, and specialty polymers. Sodium persulfate also serves as a powerful oxidizing agent used in groundwater and soil treatment technologies. In 2025, the growing use of sodium persulfate in in-situ chemical oxidation for contaminated site remediation is driving additional demand, as environmental engineers deploy activated persulfate systems to break down persistent organic pollutants in industrial soil and groundwater cleanup projects.

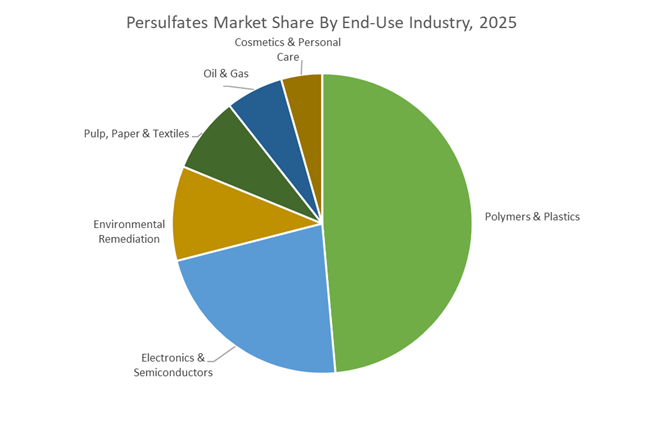

Polymers and Plastics Sector Drives Persulfate Consumption in Emulsion Polymerization Systems

The polymers and plastics sector represented 48.60% of the Persulfates Market by end-use industry in 2025, making polymerization processes the dominant outlet for persulfate oxidizing agents. Persulfates function as free-radical initiators in emulsion polymerization systems used to manufacture synthetic rubber, acrylic latex, styrene-butadiene polymers, and specialty resins for coatings, adhesives, and paper applications. Global polymer production continues to sustain steady consumption of persulfate initiators across chemical manufacturing plants. In 2025, growth in specialty latex polymers used in coatings and adhesives is increasing demand for tailored persulfate initiator systems designed to control polymer particle size distribution and molecular weight in advanced polymer formulations.

Persulfates Market Competitive Landscape

The Persulfates Market is evolving toward high-purity specialization and circular economy applications, driven by semiconductor-grade etchants and battery recycling demand. Competitive intensity is concentrated among a few global players focusing on ultra-low contamination levels, proprietary stabilization technologies, and localized supply chains to ensure resilience amid logistics volatility.

United Initiators strengthens global leadership with full-spectrum persulfates portfolio and diversified supply chain

United Initiators (UI) dominates the persulfates market with its “Total Initiator Solution” model, offering a complete range of sodium, potassium, and ammonium persulfates. The company is advancing high-purity grades for agrochemical synthesis and analytical applications, showcased across major Asian markets in 2026. Its optimized sodium persulfate formulations incorporate silica additives to enhance flowability and prevent agglomeration in automated dosing systems. UI’s geographically diversified manufacturing footprint ensures strong supply chain resilience amid ongoing geopolitical disruptions. The company is also expanding into soil and groundwater remediation, positioning persulfates as key agents for in-situ chemical oxidation (ISCO). This combination of product breadth and global reach reinforces UI’s leadership.

Evonik leverages hydrogen peroxide integration to lead sustainable oxidation and battery recycling applications

Evonik Industries AG is a major force in the persulfates market through its Active Oxygens segment, supported by full integration with hydrogen peroxide production. The company reported €1.87 billion in EBITDA in 2025 and continues to focus on high-margin specialty persulfates. Its strategic pivot toward sustainable oxidation emphasizes hydrometallurgical battery recycling, where persulfates are used to extract lithium and cobalt from spent batteries. Despite pricing pressure in some divisions, Evonik maintained stable demand in semiconductor and water treatment sectors. Its feedstock integration provides a structural cost advantage over competitors. This positioning enables Evonik to capture growth in circular economy-driven applications.

Mitsubishi Gas Chemical leads ultra-high-purity persulfates for advanced semiconductor etching applications

Mitsubishi Gas Chemical (MGC) is a key player in the Asian persulfates market, specializing in ultra-high-purity (UHP) grades for semiconductor manufacturing. Its proprietary purification technologies achieve sub-ppb contamination levels required for 2nm and 3nm chip fabrication. MGC is prioritizing its Functional Chemicals segment, directing capital toward high-performance etching agents for advanced electronics. The company is also advancing decarbonization initiatives through green energy integration in production processes. Its ammonium persulfate products are widely used in acrylics and synthetic rubber for next-generation mobility applications. This focus on precision chemistry and semiconductor integration strengthens MGC’s competitive positioning.

Ak-Kim Kimya expands EMEA footprint with integrated chemical solutions and customized persulfate applications

Ak-Kim Kimya is leveraging its strategic geographic position to serve as a bridge between European and Middle Eastern persulfates markets. The company operates one of the most advanced production facilities in the region, compliant with 2026 REACH safety standards. Its expansion into epoxy resins enhances its ability to offer integrated solutions for coatings and composites industries. Ak-Kim differentiates itself through proprietary process know-how, enabling customized persulfate formulations for oilfield stimulation and textile bleaching. It plays a critical role in enhanced oil recovery (EOR) applications, where persulfates are used for downhole oxidation. This engineering-driven approach strengthens its regional competitiveness.

Adeka focuses on low-residual persulfate systems for electronics and sustainable polymer applications

Adeka Corporation is a niche innovator in the persulfates market, focusing on high-performance polymer additives and IT-related materials. The company is developing low-residual initiator systems that enable compliance with strict toxicity standards in food-contact and medical-grade plastics. Its persulfate blends are critical for fine-line etching in 5G electronics and advanced device packaging. Adeka is actively promoting its solutions at global exhibitions, highlighting applications in water-borne coatings and sustainable materials. Under its ADK plus-2026 strategy, the company is prioritizing recyclability-enhancing additives. This focus on high-value applications and environmental compliance positions Adeka as a specialty leader.

Japan – Electronics-Grade Differentiation and Capital Reallocation

Japan’s persulfates industry is increasingly defined by precision manufacturing and electronics-driven demand. In October 2025, Mitsubishi Gas Chemical launched a new line of high-purity ammonium persulfates engineered specifically for advanced-node semiconductor fabrication and fine chemical synthesis. This move reinforces Japan’s leadership in electronics-grade oxidizers, where impurity control and batch consistency are critical for etching, surface treatment, and photoresist processing. Japanese producers are deliberately moving away from commodity-grade volumes toward grade-specific formulations, a trend underscored by Adeka Corporation and Mitsubishi Gas Chemical showcasing next-generation persulfate-based etchants at SEMICON Japan and SEMICON China 2025, aligned with the miniaturization needs of next-generation PCB and semiconductor manufacturing.

Sustainability and capital discipline are reshaping operational strategy. In 2025, leading Japanese firms integrated ISCC PLUS certification across their peroxygen value chains, emphasizing renewable electricity sourcing for the energy-intensive electrolytic production of persulfates. Mitsubishi Gas Chemical’s September 2025 decision to suspend select European construction projects reflects a broader capital reallocation toward high-growth Asian electronics-grade chemical hubs. Parallel research initiatives launched in late 2025 are also exploring persulfate-initiated polymers and PDI-linked systems for emerging 6G telecommunications infrastructure, where low dielectric loss and material stability are non-negotiable performance parameters.

United States – Trade Protection and Remediation-Led Demand Expansion

The U.S. persulfates market is operating under a structurally protected trade environment combined with expanding downstream applications. In February 2025, the U.S. Department of Commerce and the International Trade Commission reaffirmed the continuation of the antidumping duty order on Chinese persulfate imports, extending tariff protection for domestic producers through the next five-year review cycle. This policy certainty has allowed U.S.-based suppliers to invest confidently in capacity utilization and logistics optimization, reinforcing a local-for-local supply model that reduces lead times for industrial and environmental applications.

Demand-side momentum is increasingly driven by environmental remediation and energy sector pilots. By early 2026, peroxide-based groundwater remediation projects using activated sodium persulfate have accelerated, particularly for in-situ treatment of PFAS and chlorinated solvent plumes. Companies such as United Initiators and Evonik (via PeroxyChem) optimized North American supply chains in 2025 to capture market share vacated by restricted Chinese imports. In parallel, enhanced oil recovery pilots in the Permian Basin reported in mid-2025 demonstrated that monophasic persulfate packages remained stable above 120°C, outperforming traditional peroxide systems in high-temperature reservoirs and opening a niche but technically demanding energy application segment.

China – Capacity Expansion Under Tighter Controls

China remains a volume-intensive producer of persulfates, but 2025 marked a clear tightening of regulatory and strategic oversight. Fujian ZhanHua Chemical advanced its third-phase expansion project, targeting a total ammonium persulfate capacity of 80,000 tons per year by the end of 2025. This scale-up underscores China’s role as a global supply anchor, particularly for industrial and polymerization-grade persulfates, even as export conditions become more complex.

Policy direction is increasingly shaped by dual-use controls and semiconductor self-sufficiency goals. In October 2025, the Ministry of Commerce introduced stricter export control requirements, including the so-called “50% Rule,” forcing persulfate exporters to implement enhanced end-user verification. At the same time, incentives under the Big Fund Phase III and the MIIT Work Plan (2025–2026) are accelerating domestic production of semiconductor-grade sodium persulfate to reduce reliance on Japanese and German imports. Environmental governance is also tightening, with regional authorities in Ningxia and Shanxi mandating closed-loop catalytic processes for all new peroxide and persulfate facilities from 2025 onward to minimize sulfate discharge and improve compliance transparency.

Germany – R&D-Centric Consolidation and Low-Carbon Positioning

Germany’s persulfates industry is positioned as a technology and formulation hub rather than a volume leader. United Initiators, headquartered in Pullach, operates the only global network supplying both peroxodisulfates and organic peroxides, with its German sites functioning as the central R&D base for encapsulated persulfate technologies such as the CUROX® BRK range. These encapsulated systems are increasingly relevant for controlled radical polymerization and specialty polymer processing where safety and reaction control are critical.

Decarbonization considerations are shaping product strategy. In 2025, German producers began commercial rollouts of peracetic acid and persulfate blends using low-PCF aluminum and hydrogen peroxide precursors, aligning with EU Green Deal transparency and reporting requirements. Structural change has also followed ownership realignment. After acquiring RheinPerChemie from Evonik, Calibre Chemicals successfully integrated the Rheinfelden site in 2025, establishing a notable Indian-owned manufacturing footprint within the European persulfates market and reinforcing cross-regional supply linkages.

India – Cluster-Based Scale-Up and Textile-Led Consumption

India’s persulfates industry is benefiting from policy-driven infrastructure development and robust downstream demand. Under the Petroleum, Chemicals and Petrochemical Investment Regions policy, integrated clusters in Gujarat and Andhra Pradesh are streamlining access to sulfuric acid, hydrogen peroxide, and power infrastructure, reducing input volatility for persulfate manufacturers. These clusters are improving cost competitiveness while supporting faster project commissioning timelines.

On the demand side, the September 2025 update from the Ministry of Chemicals and Fertilizers highlighted the Production Linked Incentive scheme’s role in building domestic capacity for critical chemical intermediates used in specialty peroxide applications. Sodium persulfate demand in particular reached new highs in 2025, driven by its use as a bleaching and sizing agent in the textile sector. The expansion of Mega Integrated Textile Regions and Apparel parks has structurally increased consumption, anchoring persulfates as a core input in India’s growing textile and polymer processing ecosystem.

Comparative Snapshot – Persulfates Industry by Country

Persulfates Market County Level Snapshot

|

Country

|

Strategic Focus

|

Key Demand Driver

|

Structural Character

|

|

Japan

|

Electronics-grade purity

|

Semiconductors, PCBs, 6G R&D

|

High-margin, precision-led

|

|

United States

|

Trade-protected supply

|

Remediation, energy pilots

|

Policy-shielded, application-driven

|

|

China

|

Capacity with controls

|

Polymers, semiconductors

|

Scale with regulatory tightening

|

|

Germany

|

R&D and encapsulation

|

Specialty polymers

|

Technology-centric hub

|

|

India

|

Cluster-based growth

|

Textiles, polymers

|

Demand-led domestic scale-up

|

Persulfates Market Report Scope

Persulfates Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.7 Billion

|

|

Market Size (2034)

|

$2.4 Billion

|

|

Market Growth Rate

|

4%

|

|

Segments

|

By Type (Ammonium Persulfate, Sodium Persulfate, Potassium Persulfate, Potassium Peroxymonosulfate), By Grade (Technical Grade, Electronics Grade, Cosmetic Grade, Pharmaceutical Grade), By Application (Polymer Initiator, Etching & Cleaning, Oxidizing Agent, Bleaching & Sizing, Down-hole & Oilfield, Disinfectant & Sanitizer), By End-Use Industry (Polymers & Plastics, Electronics & Semiconductors, Cosmetics & Personal Care, Environmental Remediation, Oil & Gas, Pulp, Paper & Textiles)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

United Initiators GmbH, Mitsubishi Gas Chemical Company Inc., Evonik Industries AG, Calibre Chemicals Private Limited, Adeka Corporation, Fujian ZhanHua Chemical Co. Ltd., Hebei Jiheng Group, VR Persulfates, Yatai Electrochemistry Co. Ltd., Ak-Kim Kimya, San Yuan Chemical Co. Ltd., Shaoxing Shangyu Jiehua Chemical, Stars Chemical, M Chemical Company, Peroxide Chemicals Proprietary Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Persulfates Market Segmentation

By Type

- Ammonium Persulfate

- Sodium Persulfate

- Potassium Persulfate

- Potassium Peroxymonosulfate

By Grade

- Technical Grade

- Electronics Grade

- Cosmetic Grade

- Pharmaceutical Grade

By Application

- Polymer Initiator

- Etching & Cleaning

- Oxidizing Agent

- Bleaching & Sizing

- Down-hole & Oilfield

- Disinfectant & Sanitizer

By End-Use Industry

- Polymers & Plastics

- Electronics & Semiconductors

- Cosmetics & Personal Care

- Environmental Remediation

- Oil & Gas

- Pulp, Paper & Textiles

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Persulfates Industry

- United Initiators GmbH

- Mitsubishi Gas Chemical Company Inc.

- Evonik Industries AG

- Calibre Chemicals Private Limited

- Adeka Corporation

- Fujian ZhanHua Chemical Co. Ltd.

- Hebei Jiheng Group

- VR Persulfates

- Yatai Electrochemistry Co. Ltd.

- Ak-Kim Kimya

- San Yuan Chemical Co. Ltd.

- Shaoxing Shangyu Jiehua Chemical

- Stars Chemical

- M Chemical Company

- Peroxide Chemicals Proprietary Limited

*- List not Exhaustive