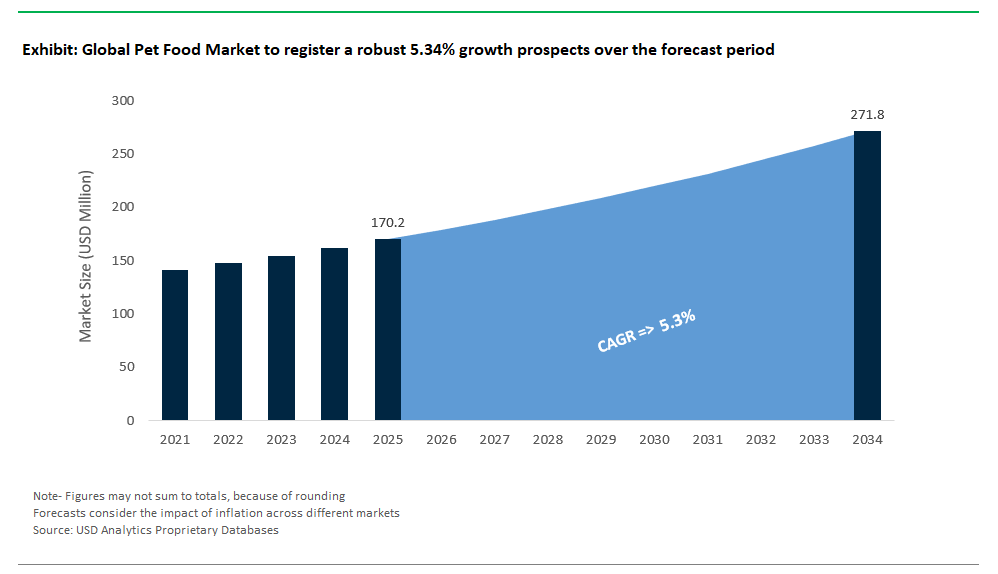

Pet Food Market Size Outlook

USD Analytics forecasts the global Pet Food market size to increase from $170.2 Billion in 2025 to $271.8 Billion in 2034, registering a CAGR of 5.34% during the forecast period

The global pet food market is undergoing a dynamic transformation, marked by bold acquisitions, sustainability initiatives, and a growing emphasis on health-driven innovation. In July 2025, WH Group, one of the world’s leading food conglomerates, announced a major strategic move by acquiring Pupil Foods, a top Polish manufacturer specializing in both wet and dry pet foods for cats and dogs. This acquisition signals WH Group’s determined entry and rapid expansion in the competitive European pet food landscape, positioning the company to capitalize on rising pet ownership and premiumization trends across the region.

Sustainability and environmental responsibility are at the forefront of recent industry developments. In August 2024, Mars Petcare a global industry heavyweight teamed up with Big Idea Ventures to launch a pioneering initiative supporting sustainable pet food startups. This collaboration underscores the pet food sector’s commitment to tackling environmental challenges through innovation, particularly in alternative proteins, upcycled ingredients, and eco-friendly packaging. By fostering a new generation of startups focused on green solutions, Mars Petcare is helping set industry standards for responsible manufacturing and product development.

Financial performance remains robust among major pet food manufacturers. In June 2025, General Mills reported a 4% increase in its pet food segment revenues, reaching an impressive US$2.5 billion for FY25. The company highlighted a growing market share in dog food, reinforcing the strength and resilience of established brands in an increasingly competitive market. This performance is supported by continuous product innovation, portfolio expansion, and targeted marketing strategies that address evolving consumer preferences.

Humanization of pets continues to drive new product categories and innovation. Early 2025 saw a strong trend of health and wellness companies such as NetNutri entering the pet supplement segment with specialized products targeting joint health, digestion, and immunity. This “humanization” trend where pet owners seek out products mirroring human health and nutrition standards for their animals has resulted in a surge of premium supplements, functional treats, and holistic formulations, further segmenting and elevating the global pet food market.

Ingredient innovation is also accelerating with industry consolidation. The February 2025 merger of Novozymes and Chr. Hansen led to the formation of Novonesis, a global biosolutions provider dedicated to advancing food, health, and nutrition. Novonesis is poised to play a pivotal role in the pet food industry by supplying innovative ingredients, such as tailored enzymes and probiotics, that enhance functionality, palatability, and health benefits of pet food products. Their expertise is expected to fuel the next wave of functional, health-oriented pet food formulations.

Pet Food Market Trends, and Opportunities

Prescription Renal Diets for Aging Cats

The rising prevalence of chronic kidney disease (CKD), affecting approximately 40% of felines aged ten years or older, represents a compelling opportunity in the pet food market through prescription renal diets. Despite their proven therapeutic benefits, fewer than 15% of cats diagnosed with CKD consistently consume these specialized diets, primarily due to palatability concerns and perceived high costs among pet owners. Innovations addressing these barriers offer significant potential for market growth, as evidenced by recent formulation advancements designed to enhance taste, digestibility, and nutritional efficacy.

Cutting-edge developments, including novel phosphate-binding agents and more palatable, nutrient-rich ingredients, are transforming prescription renal diets, significantly increasing feline acceptance rates in clinical trials. Such advancements facilitate broader adoption, ensuring more aging cats receive critical nutritional interventions to effectively manage CKD, ultimately improving health outcomes and extending life expectancy. This growing acceptance among pet owners, driven by improved product formulations, presents a notable growth opportunity for companies capable of innovating within this niche. As consumer awareness around pet healthcare continues to expand, brands effectively overcoming traditional adoption barriers stand to benefit substantially, positioning prescription renal diets as a vital and profitable segment within the pet food market.

High quality ingredients as a key buying criterion in the pet food industry

The nutrient content of pet foods emerges as a pivotal factor influencing consumer preferences and purchase decisions. Pet owners, driven by an unwavering commitment to the well-being of their animal companions, have developed a strong penchant for high-quality pet products. A prominent trend in the industry is the formulation and introduction of pet foods enriched with an appropriate blend of functional ingredients. These include vital components such as essential amino acids, complex carbohydrates, linoleic acid, and dietary fibers.

Essential amino acids, for instance, play a pivotal role in bolstering pets' growth and development. Complex carbohydrates serve as a valuable source of sustained energy, ensuring the longevity of active and happy pets. Linoleic acid is recognized for its positive impact on skin and coat health, while dietary fibers promote optimal digestive functionality. The introduction of pet foods enriched with essential functional ingredients represents a concerted effort by manufacturers to align their offerings with the discerning tastes of pet owners.

Strong prospects for fishmeal ingredients in pet food

The prospects for fishmeal ingredients in pet food appear promising, driven by potential benefits including high protein content, rich in essential amino acids, vitamins, and minerals, palatability, source of omega-3 fatty acids, highly digestible, and other benefits. Fishmeal is renowned for its exceptional protein content and quality. As pet owners increasingly seek high-protein diets for their pets, particularly in response to the growing trend of grain-free and high-meat diets, fishmeal provides an excellent protein source that meets these demands.

Further, fishmeal is rich in essential amino acids, vitamins, and minerals, making it a nutritionally dense ingredient. These nutrients are vital for promoting the health and vitality of pets, including muscle development, skin and coat health, and overall immune function. Menhaden fish, particularly Gulf menhaden, are a common source of fishmeal in pet food. Further, Salmon, Tuna, Whitefish, Sardines, Anchovies, Herring, Mackerel, and others are widely being used in the industry.

Precision Fermentation for Allergen-Free Protein

Precision fermentation is rapidly transforming the pet food market, emerging as a critical solution for producing novel, highly digestible proteins designed specifically for pets with food sensitivities. This innovative technology leverages fermentation-derived ingredients, such as insect-based and yeast proteins, to substantially reduce allergic responses often triggered by conventional proteins like chicken. Recent peer-reviewed studies validate these benefits, demonstrating significant reductions in immune-mediated reactions among canines exposed to precision-fermented proteins compared to traditional protein sources. Commercial adoption has accelerated notably, exemplified by Bond Pet Foods’ delivery of two metric tons of precision-fermented animal protein to Hill’s Pet Nutrition in early 2024, underscoring growing industry confidence in fermentation-based ingredients.

Advancements in bioreactor technologies further amplify this trend, enabling more efficient, scalable, and rapid production compared to conventional plant-based or animal-derived alternatives. For instance, FeedKind’s fermented protein, which gained approval across the EU, UK, and Canada, showcases exceptional digestibility and gut health benefits in adult dogs, reinforcing its safety and effectiveness. Startups like Ten Lives, based in San Francisco, leverage precision fermentation to produce rabbit proteins that precisely replicate the nutritional profile of wild prey, offering allergen-free nutrition and significantly reducing livestock-associated disease risks. These developments highlight precision fermentation’s critical role in meeting consumer demand for allergen-free, sustainable pet food ingredients, positioning it as a primary growth driver in the market.

Pet Food Market Share Insights

Among Pet Food Types, Dry Pet Food account for 62.3% market share in 2024.

Dry pet food is typically kibble or biscuit-like in texture, offering a crunchy consistency that can help with dental health by reducing tartar buildup. It is easy to store, handle, and measure, making it a convenient option for pet owners. It has a longer shelf life compared to wet food. Further, Dry pet food is often more cost-effective per serving than wet food, making it an attractive option for budget-conscious pet owners. It also allows for precise portion control, making it suitable for pets with specific dietary needs or those prone to overeating.

.png)

Pet Food Market Revenue Share

Among Pet Food Applications, Dogs are projected to be the largest revenue generator with a 45.9% revenue share.

The dog food market is a dynamic and evolving sector within the broader pet food industry, accounting for 45.9% market share in 2024. In recent years, there has been a notable shift towards premium and specialized dog food products, reflecting the growing awareness among pet owners about the importance of their dogs' nutrition and overall well-being.

Over 400 million pet dogs are estimated worldwide, with over 85 million in the US, 95 million in Europe, 75 million in China. An increasing demand for natural and organic ingredients is widely observed across the segment. Companies are introducing new product lines that emphasize real meat and high-quality, sustainably sourced ingredients. These launches often feature grain-free, limited-ingredient, and novel protein recipes, catering to dogs with specific dietary requirements or allergies.

Competitive Landscape: Pet Food Market

The global pet food market is characterized by strong competition among established multinational corporations and emerging premium brands, driven by evolving consumer expectations around health, sustainability, and convenience. The market is being shaped by three major trends: premiumization, humanization of pets, and technology-driven innovations in formulation and distribution. Players are investing in research, e-commerce strategies, and emerging segments such as fresh, natural, and functional diets to capture diverse consumer needs. With a surge in pet ownership and heightened attention to animal wellness, leading brands are expanding manufacturing capacities, leveraging AI for health insights, and strengthening omnichannel presence to sustain competitive advantages in this rapidly growing industry.

Mars Petcare – Market Leader with Unmatched Brand Portfolio

Mars Petcare is the global frontrunner in the pet food industry, offering an extensive portfolio of trusted brands spanning all major segments, including everyday nutrition, specialty diets, and treats. Its leading brands include Pedigree, Whiskas, Royal Canin, IAMS, Eukanuba, Sheba, Cesar, Temptations, and Greenies, catering to multiple price tiers and specific health needs. Mars invests heavily in science-backed innovation through the Waltham Petcare Science Institute, advancing formulations for life-stage nutrition, breed-specific diets, and therapeutic solutions. Recent strategic moves include multi-million-dollar investments in expanding production capacity across Europe and Asia-Pacific to meet rising demand, alongside digital transformation and e-commerce initiatives to strengthen omnichannel engagement. Mars is also pioneering the use of AI-powered health prediction tools to improve preventive care, positioning itself as a technology-driven leader in the global pet nutrition landscape.

Nestlé Purina PetCare – Science-Driven Innovation and Global Reach

Nestlé Purina PetCare stands out as a major competitor with its strong commitment to scientifically formulated diets and innovative product development. Key brands such as Purina Pro Plan, Purina ONE, Friskies, Fancy Feast, and Dog Chow dominate in both premium and mass-market segments, supported by veterinary-exclusive therapeutic diets under Purina Pro Plan Veterinary Diets. The company is aggressively expanding production, with a £159.9 million investment in its Jefferson, Wisconsin plant in 2025, part of a £1.64 billion global capital expansion strategy aimed at scaling wet pet food production. Purina continues to drive organic growth through emerging market penetration and innovative launches like GOURMET REVELATIONS and Fancy Feast Gems, aligning with premiumization and indulgence trends. With robust research capabilities and a strong distribution network, Nestlé Purina maintains its leadership by delivering tailored nutrition, from everyday meals to specialized therapeutic diets.

Hill’s Pet Nutrition (Colgate-Palmolive) – Leader in Therapeutic and Preventive Care

Hill’s Pet Nutrition commands a prominent position in the premium pet food category, focusing on science-based, veterinarian-recommended diets that address health-specific needs. Its core offerings include Hill’s Prescription Diet, a leader in therapeutic nutrition for conditions like kidney disease and obesity, and Hill’s Science Diet, designed for life-stage and preventative health benefits. The company’s strong clinical research foundation and partnerships with veterinarians reinforce its reputation as a trusted health-driven brand. Recent developments include double-digit sales growth, a major manufacturing expansion with the opening of the Tonganoxie, Kansas facility, and a strategic exit from private-label production to focus exclusively on premium and veterinary lines. By integrating innovation with clinical efficacy, Hill’s Pet Nutrition remains a top choice for pet parents seeking specialized, medically endorsed solutions for long-term wellness.

Blue Buffalo (General Mills) – Pioneer in Natural and Fresh Pet Nutrition

Blue Buffalo has cemented its position as a leading natural pet food brand, distinguished by its “Feed Them Like Family” philosophy and ingredient transparency. Its flagship lines BLUE Life Protection Formula, BLUE Wilderness, BLUE Basics, and BLUE Freedom focus on grain-free, limited-ingredient, and high-protein formulations catering to sensitive dietary needs. Blue Buffalo recently entered the fresh pet food segment with “Love Made Fresh”, marking a significant expansion into the fastest-growing category of minimally processed pet diets. In addition, General Mills introduced Edgard & Cooper to the U.S. market, bringing more premium, ingredient-focused offerings through exclusive partnerships. Strategic marketing collaborations, such as campaigns with actor Taylor Lautner for the BLUE Wilderness range, reinforce Blue Buffalo’s active, nature-inspired positioning. These moves underscore its commitment to innovation and consumer-driven trends in health-focused and fresh pet food solutions.

J.M. Smucker (Big Heart Pet Brands) – Strength in Treats and Mainstream Nutrition

The J.M. Smucker Company maintains a stronghold in the pet treats and mainstream food segments through brands such as Milk-Bone, Meow Mix, Kibbles ‘n Bits, Nature’s Recipe, and Rachael Ray Nutrish. Known for accessibility and affordability, Smucker’s pet portfolio spans dry kibble, wet food, and treats, appealing to cost-conscious consumers while addressing demand for natural and wholesome options. Recent strategic initiatives include leadership restructuring to strengthen execution, divestiture of its private-label pet food business to streamline focus, and continued innovation in its dominant treats category. By leveraging the strong equity of brands like Milk-Bone and expanding premium offerings through Nature’s Recipe, J.M. Smucker positions itself as a key player balancing affordability with evolving consumer preferences for quality and variety in pet nutrition.

North America is set to be the largest market for Pet Food vendors during the forecast period with a 55.4% Market Share.

The US is the largest market for Pet Food in the North American region and the world. The market growth is driven by the rising pet ownership rates, focus on pet health and wellness, and the launch of premium and specialized pet food products. In particular, products tailored for specific dietary needs are gaining significant demand in the US and North America.

Nestlé Purina, Mars Petcare, Hill's Pet Nutrition, and others are increasingly focusing product launches focused on niche consumer segments. As of 2024, 66% of U.S. households (86.9 million homes) own a pet according to the American Pet Products Association. In particular, Millennials make up the largest percentage of current pet owners (33%), followed by Gen X (25%) and baby boomers (24%). Accordingly, companies are strategizing their marketing campaigns focused on these segments. In addition to well-established offline distribution channels, the sales through e-commerce portals are rapidly growing raipidly.

United States Pet Food Market Thrives on Premiumization and Digital Expansion

The United States continues to lead the global pet food market through substantial investments and ongoing premiumization trends. In March 2024, The Crump Group Inc. unveiled plans for an $85 million expansion of its premium pet treat manufacturing facility in Nashville, North Carolina, signaling robust growth in the premium pet food segment. This premium focus is mirrored by JustFoodForDogs, which in April 2025 significantly expanded its fresh-frozen dog food products to over 900 PetSmart locations nationwide, reflecting a consumer shift towards minimally processed, human-grade pet diets. Furthermore, the rising demand for sustainable and alternative-protein pet foods was underscored by PawCo Foods' January 2024 launch of its innovative plant-based dog food products, "InstaBites" and "LuxBites," demonstrating an increasing trend toward eco-friendly, health-conscious choices among pet owners.

In parallel, digital transformation and innovation by major brands further propel market expansion. Mars Petcare announced in October 2024 a massive $1 billion investment in enhancing its global digital infrastructure, significantly boosting its U.S. e-commerce capabilities, AI integration, and consumer data management. Complementing these advancements, Purina PetCare announced in April 2024 its ambitious goal of launching over 100 new pet food products within the year, emphasizing advanced nutrition and microbiome health. The American Pet Products Association (APPA) identified pet humanization as the central driver for these trends, with 75% of pet owners treating pets as integral family members, profoundly shaping purchasing behaviors towards premium, nutritious, and personalized pet food offerings.

China Pet Food Market Expands Rapidly with Rising Domestic Brands and Urban Growth

China's pet food market exhibits remarkable growth, driven by robust domestic production, rising consumer preference for local brands, and substantial investment inflows. The urban pet market alone exceeded 300.2 billion yuan ($41.1 billion) in 2024, marking a significant 7.5% year-on-year growth. Reflecting this surge, Mars opened a state-of-the-art, 110,000 square meter pet food manufacturing plant in Tianjin in May 2024, underlining the substantial commitment global brands are making toward localized Chinese production. This was further supported by Advent International’s notable private equity investment in Seek Pet Food, China's prominent kibble manufacturer boasting 66 nutritional patents, demonstrating investor confidence and fueling domestic innovation.

Simultaneously, consumer preferences in China are evolving rapidly, with a distinct shift toward domestic brands; in 2024, approximately 32.9% of dog owners and 34.8% of cat owners exclusively purchased Chinese pet food products. Cat ownership has notably outpaced dog ownership, with urban pet cats increasing by 2.5% to 71.53 million in 2024, accelerating the cat food segment’s growth. This changing pet ownership landscape is prompting manufacturers to diversify and innovate, catering specifically to cat-specific dietary needs and preferences. The combined effect of consumer preference shifts, significant investments, and manufacturing expansions positions China as a leading market for pet food globally.

India's Pet Food Market Booms with Strategic Investments and Premiumization

India’s pet food market is witnessing accelerated growth through strategic corporate investments and evolving consumer preferences towards premium and specialized nutrition. Godrej Pet Care notably launched its premium dog food brand "Godrej Ninja" in April 2025, supported by an ambitious investment plan of Rs 500 crore ($60 million USD) over five years, highlighting increased corporate confidence in the domestic pet food industry. Additionally, Avanti Pet Care diversified into the cat food market in March 2025, introducing "Avant Furst" through a strategic collaboration with Thailand's Bluefalo Group, catering to India's rapidly expanding cat-owner base.

Consumer preferences across India are distinctly shifting towards convenient, commercial pet diets, particularly in major urban centers like Pune and Mumbai, where packaged diets are increasingly favored over homemade meals. Pet owners now seek specialized formulations rich in omega fatty acids, probiotics, glucosamine, and high-quality proteins, creating a surge in premium product demand. The significant rise in cat ownership, which grew by 88.2% between 2017 and 2022, continues to drive innovation and product development, particularly within the wet food segment. Furthermore, Avanti Pet Care’s announcement to establish a new state-of-the-art pet food manufacturing facility in Hyderabad underscores sustained market optimism and the strategic direction towards quality-driven, specialized pet food production in India.

Germany Pet Food Market Driven by Sustainability and Functional Nutrition Demand

Germany’s pet food market is increasingly shaped by strong consumer demand for sustainability, organic ingredients, and functional nutrition. Reflecting heightened consumer environmental consciousness, organic pet food sales have grown consistently by approximately 15% annually over the past five years, driven by pet owners prioritizing natural and ethically sourced ingredients. This sustainability trend aligns closely with the broader humanization of pets in Germany, as consumers increasingly seek high-quality, premium diets mirroring their own dietary standards.

Simultaneously, functional pet foods that provide targeted health benefits have emerged as a key growth area. German pet owners prioritize foods fortified with probiotics, omega-3 fatty acids, and specialized nutrients for digestion, joint health, and immune support. Dry pet food, particularly appreciated for convenience, affordability, and extended shelf life, continues to dominate the market with a substantial 59.5% revenue share as of 2024. This multifaceted approach, combining sustainability, premium quality, and functional nutrition, firmly positions Germany’s pet food market for sustained growth and innovation.

United Kingdom Pet Food Market Embraces Eco-friendly and Specialized Diet Trends

The United Kingdom pet food market continues its upward trajectory, driven by increasing consumer preferences for eco-friendly products and specialized dietary solutions. UK pet food brands are proactively adopting sustainable practices, incorporating environmentally responsible packaging and ethically sourced ingredients to meet consumer expectations. This heightened focus on sustainability aligns closely with a pronounced trend towards pet humanization, with the majority of UK pet owners considering pets as family members and therefore prioritizing premium, natural, and human-grade diets.

Moreover, niche dietary options such as grain-free, hypoallergenic, and raw/BARF (Biologically Appropriate Raw Food) diets have gained considerable traction, reflecting growing health-consciousness among pet owners. Local and independent brands have particularly benefited from this shift, attracting consumers seeking transparent sourcing, unique formulations, and ethical production practices. Concurrently, e-commerce remains a dominant distribution channel, driven by convenience, subscription services, and extensive product availability. This dynamic combination of sustainable practices, specialized diets, and strong e-commerce presence ensures continued robust growth in the UK pet food market.

Brazil Pet Food Market Expands with Premiumization and Strategic Sustainability Efforts

Brazil's pet food market continues its rapid expansion, achieving significant revenue of approximately R$ 68.7 billion ($12.5 billion USD) in 2024, with food products alone accounting for 55.5% of this total. Major manufacturing expansions, such as Adimax's May 2025 launch of a $140 million production facility in Mandirituba, demonstrate sustained industry investment and increased production capacity, positioning the company as Brazil's leading pet food producer. Simultaneously, Brazilian pet owners overwhelmingly perceive pets as family members (92%), fueling significant demand for premium, specialized pet nutrition tailored to specific life stages and breeds.

Sustainability initiatives have also become integral to Brazil’s pet food sector. In September 2024, PremieRpet introduced limited-edition packaging for its Nattu pet food line, donating proceeds to Onçafari's Pantanal Recovery Fund, aligning brand identity with environmental conservation efforts. Concurrently, demand for functional ingredients addressing joint health, digestion, and coat care remains strong, pushing manufacturers to innovate in breed-specific and grain-free formulations. This convergence of premiumization, sustainable practices, and functional nutrition solidifies Brazil’s pet food market's robust growth trajectory.

Japan Pet Food Market Adapts to Aging Pet Demographics and Compact Living Spaces

Japan’s pet food market is responding dynamically to unique demographic and lifestyle factors, particularly the aging pet population. There is an increased demand for specialized senior pet foods that address age-related issues, such as joint support, kidney health, and cognitive wellness. Japanese consumers highly value premium and functional ingredients, emphasizing natural and organic formulations known for specific health benefits, reinforcing Japan's reputation for meticulous pet care standards.

Moreover, given Japan’s compact urban living spaces, pet food manufacturers have adapted by offering smaller, single-serving packages, optimizing freshness, reducing waste, and enhancing convenience. Concurrently, technological integration, including the growing adoption of smart pet feeders, indirectly influences product development and packaging decisions. These factors collectively position Japan’s pet food market as uniquely attuned to demographic and lifestyle requirements, ensuring steady demand for premium, functional, and suitably packaged products.

Australia Pet Food Market Thrives with Innovative Diets and Sustainability Focus

Australia’s pet food market continues to flourish, reaching AUD 6.05 billion in 2024, largely propelled by premiumization and health-conscious consumer trends. Innovations such as Tuckers Natural’s biologically appropriate raw diet line and Natural Pet Food Co.’s plant-based dog food illustrate the market’s adaptability to diverse dietary preferences and growing demand for alternative, sustainable pet nutrition.

Furthermore, the market increasingly addresses specific health concerns, notably obesity in pets, exemplified by Hill's Science Diet's new weight-management formula introduced in July 2024. Sustainability remains paramount, with Australian consumers favoring brands that utilize regenerative agriculture, recyclable packaging, and alternative low-impact protein sources. These diverse yet focused strategies underscore Australia’s dynamic and evolving pet food landscape, characterized by innovation, premiumization, and environmental consciousness.

Pet Food Market Share and Leaders

The global Pet Food market is fragmented with the presence of both local and global players. Leading companies in the Pet Food industry are The J.M. Smucker Company, Nestle Purina, Mars, Incorporated, LUPUS Alimentos, Total Alimentos, Hill’s Pet Nutrition, Inc., General Mills Inc., WellPet LLC, The Hartz Mountain Corporation, and others.

Pet Food Market Recent product launches and market news

- Growel Group announced the launch of premium category 'Carniwel'. The product category caters to the growing demand of pet nutrition

- Big Idea Ventures and Mars launch Next Generation Pet Food Program pilot in collaboration with AAK and Bühler

- Pawco Launches AI-Powered Dog Food. The products- LuxBites, InstaBites. PawCo Foods uses AI for nutrition optimization and palatability improvement

- HelloFresh announced the launch of their new premium pet food brand, The Pets Table in 2023

- Nestlé Purina launched pet food with plant and insect proteins in 2020

- US-based Wild Earth announced it has developed a cell-based chicken broth topper for dogs.

- Mankind Pharma Limited announced the launch of PetStar Dog Food as it forays into the pet food industry

- Go! Solutions Announces Launch of New Functional Pet Food and Treats in Canada

Pet Food Market Report Scope

|

Parameter

|

Details

|

|

Market Size (2025)

|

$170.2 Billion

|

|

Market Size (2034)

|

$271.8 Billion

|

|

Market Growth Rate

|

5.34%

|

|

Largest Segment- Type

|

Dry Pet Food (62.3% Market Share)

|

|

Fastest Growing Market- Region

|

North America (55.4% Market Share)

|

|

Largest Segment- Application

|

Dogs (45.9% Market Share)

|

|

Segments

|

Types, Applications, Forms, Products, Sales Channels

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The J.M. Smucker Company, Nestle Purina, Mars, Incorporated, LUPUS Alimentos, Total Alimentos, Hill’s Pet Nutrition, Inc., General Mills Inc., WellPet LLC, The Hartz Mountain Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Pet Food Market Segmentation

By Animal Type

By Form

- Dry Food (Kibble)

- Wet Food (Canned/Pouch)

- Treats & Snacks

- Semi-Moist Food

- Raw Food

- Veterinary Diets

- Pet Nutraceuticals

By Source

- Animal-Based Ingredients

- Plant-Based Ingredients

- Specialty Ingredients

By Quality

- Mass Market/Economy

- Premium/Super Premium

- Veterinary/Therapeutic

By Distribution Channel

- Supermarkets/Hypermarkets

- Specialty Pet Stores

- Veterinary Clinics/Pharmacies

- Independent Retailers.

- Online Channels (E-commerce)

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Pet Food Companies Profiled in the Study

- The J.M. Smucker Company

- Nestle Purina

- Mars, Incorporated

- LUPUS Alimentos

- Total Alimentos

- Hill’s Pet Nutrition, Inc.

- General Mills Inc.

- WellPet LLC

- The Hartz Mountain Corporation

*- List Not Exhaustive

Research Coverage

This USDAnalytics report presents a comprehensive analysis of the global pet food market from 2025 to 2034, examining industry size, CAGR, and the forces reshaping the sector including strategic acquisitions, premiumization, humanization of pets, sustainability, and technology-driven innovation.

The study covers detailed segmentation by animal type (dogs, cats, other pets), form (dry, wet, treats, raw, semi-moist, veterinary, nutraceuticals), source (animal-based, plant-based, specialty ingredients), quality (economy, premium, veterinary), and distribution channel (supermarkets, specialty pet stores, veterinary clinics, independent retailers, e-commerce).

Regional and country-specific insights span North America, Europe, Asia Pacific, South America, and the Middle East & Africa, with focused profiles on leading pet food markets including the United States, China, India, Germany, United Kingdom, Brazil, Japan, and Australia.

The report evaluates key trends such as precision fermentation, sustainability initiatives, premiumization, and the digitalization of pet food retail. Competitive landscape coverage highlights the strategic positioning and product innovation of top companies like Mars Petcare, Nestlé Purina, Hill's Pet Nutrition, and Blue Buffalo.

This USDAnalytics research provides actionable intelligence for manufacturers, retailers, investors, and stakeholders seeking to capitalize on the evolving global pet food industry.

Deliverables:

- Full Market Research Report (PDF, Excel): Complete data tables, market charts, and visual insights.

- Country-Level Forecasts & Analysis.

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis.

- Recent Developments & News Tracker

- Executive Summary & Analyst Insights.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

About USD Analytics

Table of Contents

- List of Charts and Exhibits

- List of Tables

1. Executive Summary

What’s New in 2024?

Top 10 Takeaways from the Industry

Potential Opportunities for Industry Stakeholders

Strategic Imperatives

Company Market Positioning

Industry Benchmarking Matrix

2. Research Scope and Methodology

Market Definition

Market Segments

Companies Profiled

Research Methodology

- Bottom-Up Method

- Top-Down Method

- Data Triangulation

- Forecast Methodology

Data Sources

- USDA Proprietary Databases

- External Sources

- Primary Research and Interviews

Conversion Rates for USD

Abbreviations

3. Strategic Landscape: Key Insights and Implications

Spotlight: Key Strategies Opted by Business Leaders

Competitive Landscape

- Market Size ($ Million) and Share (%) by Company, 2023

SWOT Analysis

- Key Market Strengths

- Key Market Weaknesses

- Potential Opportunities

- Potential Threats

Porter’s Five Force Analysis

- Summary

- Bargaining Power of Buyers- Impact Analysis

- Bargaining Power of Suppliers- Impact Analysis

- Threat of New Entrants- Impact Analysis

- Intensity of Competitive Rivalry- Impact Analysis

Macro-Environmental Analysis

- Economic Forecasts by Country, 2010- 2032

- Population Forecasts by Country, 2010- 2032

- Inflation Outlook by Country, 2010-2032

- Impact of Russia-Ukraine Conflict, Sluggish China Growth, US Developments

4. Growth Opportunity Analysis

Trends at a Glance

- What are the most noteworthy trends in the market

- Where should leaders pay attention?

- What industries are likely to be affected by the growth?

Market Dynamics

- Charting a path forward

- Growth Drivers

- Growth Barriers

Key Industry Stakeholders

- Suppliers

- Manufacturers and Service Providers

- Distribution Channels

- End-Users and Applications

- Regulators

- Investors, Traders, and R&D Institutes

Regulatory Landscape

5. Market Size Outlook to 2032

Global Pet Food Market Size Forecast, USD Million, 2018- 2032

- Historic Market Size, 2018- 2023

- Forecast Market Size, 2024- 2032

Scenario Analysis

- Low Growth Scenario: Definition and Outlook to 2032

- Reference Case: Definition and Outlook to 2032

- High Growth Scenario: Definition and Outlook to 2032

Pricing Analysis and Outlook

- Pet Food Average Price Forecast, 2021- 2032

- Key Factors Shaping the Pricing Patterns

6. Historical Pet Food Market Size by Segments, 2018- 2023

Key Statistics, 2024

Pet Food Market Size Outlook by Type, USD Million, 2018-2023

Growth Comparison (y-o-y) across Pet Food Types, 2018-2023

Pet Food Market Size Outlook by Application, USD Million, 2018-2023

Growth Comparison (y-o-y) across Pet Food Applications, 2018-2023

7. Pet Food Market Size Outlook by Segments, 2024- 2032

Pet Food Market Size Outlook by Type, USD Million, 2024-2032

Growth Comparison (y-o-y) across Pet Food Types, 2024-2032

- Dry

- Wet

- Snacks and Treats

Pet Food Market Size Outlook by End-User, USD Million, 2024-2032

Growth Comparison (y-o-y) across Pet Food End-Users, 2024-2032

Pet Food Market Size Outlook by Product, USD Million, 2024-2032

Growth Comparison (y-o-y) across Pet Food Products, 2024-2032

Pet Food Market Size Outlook by Source, USD Million, 2024-2032

Growth Comparison (y-o-y) across Pet Food Sources, 2024-2032

- Animal-Derived

- Plant-Derived

- Synthetic

8. Pet Food Market Size Outlook by Region

North America

- Key Market Dynamics

- North America Pet Food Market Size Outlook by Type, USD Million, 2021-2032

- North America Pet Food Market Size Outlook by Application, USD Million, 2021-2032

- North America Pet Food Market Size Outlook by Sales Channel, USD Million, 2021-2032

- North America Pet Food Market Size Outlook by Country, USD Million, 2021-2032

Europe

- Key Market Dynamics

- Europe Pet Food Market Size Outlook by Type, USD Million, 2021-2032

- Europe Pet Food Market Size Outlook by Application, USD Million, 2021-2032

- Europe Pet Food Market Size Outlook by Sales Channel, USD Million, 2021-2032

- Europe Pet Food Market Size Outlook by Country, USD Million, 2021-2032

Asia Pacific

- Key Market Dynamics

- Asia Pacific Pet Food Market Size Outlook by Type, USD Million, 2021-2032

- Asia Pacific Pet Food Market Size Outlook by Application, USD Million, 2021-2032

- Asia Pacific Pet Food Market Size Outlook by Sales Channel, USD Million, 2021-2032

- Asia Pacific Pet Food Market Size Outlook by Country, USD Million, 2021-2032

South America

- Key Market Dynamics

- South America Pet Food Market Size Outlook by Type, USD Million, 2021-2032

- South America Pet Food Market Size Outlook by Application, USD Million, 2021-2032

- South America Pet Food Market Size Outlook by Sales Channel, USD Million, 2021-2032

- South America Pet Food Market Size Outlook by Country, USD Million, 2021-2032

Middle East and Africa

- Key Market Dynamics

- Middle East and Africa Pet Food Market Size Outlook by Type, USD Million, 2021-2032

- Middle East and Africa Pet Food Market Size Outlook by Application, USD Million, 2021-2032

- Middle East and Africa Pet Food Market Size Outlook by Sales Channel, USD Million, 2021-2032

- Middle East and Africa Pet Food Market Size Outlook by Country, USD Million, 2021-2032

9. United States Pet Food Market Analysis and Outlook, 2021- 2032

Key Statistics

United States Pet Food Market Size Outlook by Type, 2021- 2032

United States Pet Food Market Size Outlook by Application, 2021- 2032

United States Pet Food Market Size Outlook by End-User, 2021- 2032

10. Canada Pet Food Market Analysis and Outlook, 2021- 2032

Key Statistics

Canada Pet Food Market Size Outlook by Type, 2021- 2032

Canada Pet Food Market Size Outlook by Application, 2021- 2032

Canada Pet Food Market Size Outlook by End-User, 2021- 2032

11. Mexico Pet Food Market Analysis and Outlook, 2021- 2032

Key Statistics

Mexico Pet Food Market Size Outlook by Type, 2021- 2032

Mexico Pet Food Market Size Outlook by Application, 2021- 2032

Mexico Pet Food Market Size Outlook by End-User, 2021- 2032

12. Germany Pet Food Market Analysis and Outlook, 2021- 2032

Key Statistics

Germany Pet Food Market Size Outlook by Type, 2021- 2032

Germany Pet Food Market Size Outlook by Application, 2021- 2032

Germany Pet Food Market Size Outlook by End-User, 2021- 2032

13. France Pet Food Market Analysis and Outlook, 2021- 2032

Key Statistics

France Pet Food Market Size Outlook by Type, 2021- 2032

France Pet Food Market Size Outlook by Application, 2021- 2032

France Pet Food Market Size Outlook by End-User, 2021- 2032

14. United Kingdom Pet Food Market Analysis and Outlook, 2021- 2032

Key Statistics

United Kingdom Pet Food Market Size Outlook by Type, 2021- 2032

United Kingdom Pet Food Market Size Outlook by Application, 2021- 2032

United Kingdom Pet Food Market Size Outlook by End-User, 2021- 2032

15. Spain Pet Food Market Analysis and Outlook, 2021- 2032

Key Statistics

Spain Pet Food Market Size Outlook by Type, 2021- 2032

Spain Pet Food Market Size Outlook by Application, 2021- 2032

Spain Pet Food Market Size Outlook by End-User, 2021- 2032

16. Italy Pet Food Market Analysis and Outlook, 2021- 2032

Key Statistics

Italy Pet Food Market Size Outlook by Type, 2021- 2032

Italy Pet Food Market Size Outlook by Application, 2021- 2032

Italy Pet Food Market Size Outlook by End-User, 2021- 2032

17. Benelux Pet Food Market Analysis and Outlook, 2021- 2032

Key Statistics

Benelux Pet Food Market Size Outlook by Type, 2021- 2032

Benelux Pet Food Market Size Outlook by Application, 2021- 2032

Benelux Pet Food Market Size Outlook by End-User, 2021- 2032

18. Nordic Pet Food Market Analysis and Outlook, 2021- 2032

Key Statistics

Nordic Pet Food Market Size Outlook by Type, 2021- 2032

Nordic Pet Food Market Size Outlook by Application, 2021- 2032

Nordic Pet Food Market Size Outlook by End-User, 2021- 2032

19. Rest of Europe Pet Food Market Analysis and Outlook, 2021- 2032

Key Statistics

Rest of Europe Pet Food Market Size Outlook by Type, 2021- 2032

Rest of Europe Pet Food Market Size Outlook by Application, 2021- 2032

Rest of Europe Pet Food Market Size Outlook by End-User, 2021- 2032

20. China Pet Food Market Analysis and Outlook, 2021- 2032

Key Statistics

China Pet Food Market Size Outlook by Type, 2021- 2032

China Pet Food Market Size Outlook by Application, 2021- 2032

China Pet Food Market Size Outlook by End-User, 2021- 2032

21. India Pet Food Market Analysis and Outlook, 2021- 2032

Key Statistics

India Pet Food Market Size Outlook by Type, 2021- 2032

India Pet Food Market Size Outlook by Application, 2021- 2032

India Pet Food Market Size Outlook by End-User, 2021- 2032

22. Japan Pet Food Market Analysis and Outlook, 2021- 2032

Key Statistics

Japan Pet Food Market Size Outlook by Type, 2021- 2032

Japan Pet Food Market Size Outlook by Application, 2021- 2032

Japan Pet Food Market Size Outlook by End-User, 2021- 2032

23. South Korea Pet Food Market Analysis and Outlook, 2021- 2032

Key Statistics

South Korea Pet Food Market Size Outlook by Type, 2021- 2032

South Korea Pet Food Market Size Outlook by Application, 2021- 2032

South Korea Pet Food Market Size Outlook by End-User, 2021- 2032

24. Australia Pet Food Market Analysis and Outlook, 2021- 2032

Key Statistics

Australia Pet Food Market Size Outlook by Type, 2021- 2032

Australia Pet Food Market Size Outlook by Application, 2021- 2032

Australia Pet Food Market Size Outlook by End-User, 2021- 2032

25. South East Asia Pet Food Market Analysis and Outlook, 2021- 2032

Key Statistics

South East Asia Pet Food Market Size Outlook by Type, 2021- 2032

South East Asia Pet Food Market Size Outlook by Application, 2021- 2032

South East Asia Pet Food Market Size Outlook by End-User, 2021- 2032

26. Rest of Asia Pacific Pet Food Market Analysis and Outlook, 2021- 2032

Key Statistics

Rest of Asia Pacific Pet Food Market Size Outlook by Type, 2021- 2032

Rest of Asia Pacific Pet Food Market Size Outlook by Application, 2021- 2032

Rest of Asia Pacific Pet Food Market Size Outlook by End-User, 2021- 2032

27. Brazil Pet Food Market Analysis and Outlook, 2021- 2032

Key Statistics

Brazil Pet Food Market Size Outlook by Type, 2021- 2032

Brazil Pet Food Market Size Outlook by Application, 2021- 2032

Brazil Pet Food Market Size Outlook by End-User, 2021- 2032

28. Argentina Pet Food Market Analysis and Outlook, 2021- 2032

Key Statistics

Argentina Pet Food Market Size Outlook by Type, 2021- 2032

Argentina Pet Food Market Size Outlook by Application, 2021- 2032

Argentina Pet Food Market Size Outlook by End-User, 2021- 2032

29. Rest of South America Pet Food Market Analysis and Outlook, 2021- 2032

Key Statistics

Rest of South America Pet Food Market Size Outlook by Type, 2021- 2032

Rest of South America Pet Food Market Size Outlook by Application, 2021- 2032

Rest of South America Pet Food Market Size Outlook by End-User, 2021- 2032

30. United Arab Emirates Pet Food Market Analysis and Outlook, 2021- 2032

Key Statistics

United Arab Emirates Pet Food Market Size Outlook by Type, 2021- 2032

United Arab Emirates Pet Food Market Size Outlook by Application, 2021- 2032

United Arab Emirates Pet Food Market Size Outlook by End-User, 2021- 2032

31. Saudi Arabia Pet Food Market Analysis and Outlook, 2021- 2032

Key Statistics

Saudi Arabia Pet Food Market Size Outlook by Type, 2021- 2032

Saudi Arabia Pet Food Market Size Outlook by Application, 2021- 2032

Saudi Arabia Pet Food Market Size Outlook by End-User, 2021- 2032

32. Rest of Middle East Pet Food Market Analysis and Outlook, 2021- 2032

Key Statistics

Rest of Middle East Pet Food Market Size Outlook by Type, 2021- 2032

Rest of Middle East Pet Food Market Size Outlook by Application, 2021- 2032

Rest of Middle East Pet Food Market Size Outlook by End-User, 2021- 2032

33. South Africa Pet Food Market Analysis and Outlook, 2021- 2032

Key Statistics

South Africa Pet Food Market Size Outlook by Type, 2021- 2032

South Africa Pet Food Market Size Outlook by Application, 2021- 2032

South Africa Pet Food Market Size Outlook by End-User, 2021- 2032

34. Rest of Africa Pet Food Market Analysis and Outlook, 2021- 2032

Key Statistics

Rest of Africa Pet Food Market Size Outlook by Type, 2021- 2032

Rest of Africa Pet Food Market Size Outlook by Application, 2021- 2032

Rest of Africa Pet Food Market Size Outlook by End-User, 2021- 2032

35. Key Companies

Market Share Analysis

- The J.M. Smucker Company

- Nestle Purina

- Mars, Incorporated

- LUPUS Alimentos

- Total Alimentos

- Hill’s Pet Nutrition, Inc.

- General Mills Inc.

- WellPet LLC

- The Hartz Mountain Corporation

Company Benchmarking

SWOT Analysis

36. Recent Market Developments

Appendix

Looking Ahead

Research Methodology

Legal Disclaimer