Pet Hygiene and Care Products Market Outlook – Premiumization, Sustainability, and Technological Evolution

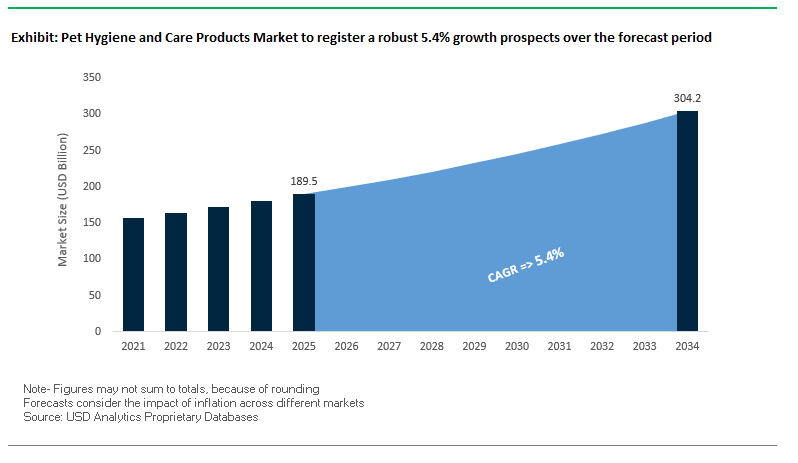

The global pet hygiene and care products market is expected to grow from USD 189.5 billion in 2025 to USD 304.2 billion by 2034, at a CAGR of 5.4%. The market is led by growing pet humanization, premiumization, and the increasing use of sustainable, health-focused products. Customers are looking for innovative, high-end, niche-level solutions offering solutions for skin, dental, and general health, in line with pet humanization overall. Growth is being driven by innovation in organic grooming products, AI grooming products, and smart collars, while sustainability is impacting material choice and packaging solutions. Growing awareness towards preventive pet care and e-commerce channel growth are also further driving market penetration regionally.

Key Insights for Industry Professionals

- Premiumization Driving Growth – Surge in demand for luxury and specialized products like organic shampoos and therapeutic dental chews.

- Humanization of Pets – Owners increasingly treat pets as family members, fueling investment in advanced hygiene and care solutions.

- Eco-Friendly Focus – Strong shift toward biodegradable, plant-based, and chemical-free formulations.

- Technology Integration – Smart grooming devices and health-monitoring accessories entering mainstream retail.

- Preventive Healthcare Demand – Rise in medicated shampoos, probiotics, and dental care products to tackle common pet health issues.

Pet Hygiene and Care Products Market Analysis – Recent Developments and Strategic Shifts

Recent news highlights the shift of the market towards innovation and sustainability. In August 2025, the Pet Innovation Awards included dental care brands such as Pet Honesty and gut health brands such as Brutus Bone Broth, showing high interest in disease prevention. In July 2025, the American Pet Products Association introduced a compliance-oriented series of webinars amidst new tariff deadlines, emphasizing the impact of international trade on supply chains.

Zoetis was approved in May 2025 by the FDA for a new indication for Simparica Trio to protect against flea tapeworm infestation a first for the industry since the EPA review of Seresto collars continues to influence product safety protocols. Leadership changes, such as the April 2025 hiring of Michael Bellingham as CEO of PFMA, are indicative of strategic realignments to address evolving consumer and sustainability demands.

Cross-segment technology mergers and acquisitions are shaping the competitive landscape. Incline Equity Partners' acquisition of Med-Vet International in February 2025 bolstered veterinary distribution, and Perfect Corp.'s acquisition of Wannaby in January 2025 portends future AR-enabling marketing for pet items. Sustainability initiatives, including Mars Petcare's platform for renewable energy and Happy Egg's October 2024 merger with Egg Innovations, are affirming the green-forward direction of the sector.

Innovative Trends and Emerging Opportunities in the Pet Hygiene and Care Products Market

Probiotic Coat Microbiome Reset: Restoring Pet Skin Health Naturally

One of the most significant advances in the pet care and pet hygiene products market is the application of probiotic sprays and topical therapy for the reconstruction of the skin and coat microbiome. The products heal chronic skin disease, allergies, and fungal infections without the application of harsh chemicals. Backed by veterinary research, probiotics remove inflammation, boost immune function, and link gut health with skin health. Industry participants are leveraging dissolvable delivery forms and multi-strain formulas to restore lost microbial diversity from chemical exposure from cleaning products, pest control, and antibiotics. With pet owners increasingly seeking natural, chemical-free products, probiotic therapy is part of a larger holistic pet care movement. Clinical applications, such as "Skin & Coat Relief Kits" based on fecal microbiota transplantation expertise, further drive the market movement toward science-based, non-invasive treatments.

At-Home Cavitron Dental Scaling: Professional-Level Oral Care Without Anesthesia

The increasing popularity of in-home ultrasonic dental scaling units for pets responds to one of the most entrenched obstacles in pet oral health anesthesia risks and steep veterinary expenses. Silent, vibration-free ultrasonic toothbrushes and scalers are finding favor for their capacity to clean interdental and break down plaque and tartar without pain. These units feature gentle, high-frequency technology that maintains gum integrity while enhancing periodontal health. The comfort of in-home dental care is a powerful driver to adoption, especially for preventive care in between professional cleanings. As pet humanization trends raise the value placed on dental hygiene, these units find themselves a cost-effective, stress-free solution for high-end pet oral care.

Post-Pandemic Growth in Pet-Friendly Disinfectants for Hygiene

Pet-friendly disinfectant market has increased as consumers prioritize home cleansing but protect pets from toxic ingredients. Most conventional cleaners contain harmful ingredients such as phenol or pungent essential oils, which pose highly dangerous health risks. This has facilitated the entry of green, non-toxic products containing natural agents, which are safe even when wet. Wiggles has been among the pioneers in launching alcohol-free instant pet sanitizers for fur and paws after a walk, a direct result of the pandemic. New players in this market can leverage greater awareness of health and green trends, making green disinfectants a household necessity for pet-keeping households.

CBD-Infused Wound Care for Therapeutic Pet Recovery

The advent of CBD-based wound care products offers a high-growth opportunity in pet wellness. Cannabidiol's analgesic and anti-inflammatory properties, supported by case reports and early veterinary trials, offer a potential therapy for cuts, abrasions, and postop recovery. Despite regulatory ambiguity and inconsistent product quality studies confirm just 23% of veterinary hemp products meet label claims brands publishing open COAs can build credibility and corner the market. CBD topicals solve both acute wound care and chronic skin conditions, marrying holistic pain management with accelerated recovery. As regulatory infrastructures evolve, CBD wound care will transition from niche to mass in the pet medical care products market.

Pet Hygiene and Care Products Market Share Insights Strategic Insights by Product and Pet Type

Market Share by Product Type: Grooming Leads While Dental Care Gains Momentum

By 2025, the pet care and hygiene products market is led by 30% market share of grooming products, fueled by shampoos, conditioners, and wipes' frequent usage and premiumization. Natural and organic grooming products' focus shows a consumer shift towards chemical-free products. Flea & tick control is a robust 25% market share, with preventive and long-lasting natural repellents becoming popular. Waste management solutions such as biodegradable waste bags and eco-friendly litter are growing in sync with urban pet keeping. Dental care products are experiencing high growth rates as pet humanization fuels demand for oral care products such as water additives, dental chews/dental sticks, and enzymatic toothpastes. Specialty but high-margin categories such as paw/skin care and eye/ear care are gaining due to specialty products addressing sensitive skin and breed-specific requirements.

.png)

Market Share by Pet Type: Dogs Dominate, Cats Drive Specialized Care Growth

Dogs represent 65% of pet grooming and hygiene products, reflecting more intensive grooming, outdoor usage, and owner outlays on premium wellness products. The cat business is increasing vigorously in urban markets with innovation in low-dust cat litter, grooming wipes, and stress-reducing cleaning products for cats. Other pets (birds, fish, small mammals) represent a minor 5%, but the niche is gaining respect with specialist cage cleaners, water conditioners, and dental sticks for small animals. The growth trajectory across segments is such that dogs remain the highest-revenue driver, but cats and niche pets offer opportunities for category extension and brand portfolio growth.

Competitive Landscape – Market Leaders Shaping Global Pet Care

Pet care and hygiene products market is ruled by a set of global conglomerates and specialist innovators competing on brand reputation, research-driven product innovation, and multi-channel distribution approaches. Those businesses that strike the balance between premium product quality and sustainability, technology integration, and veterinarian credibility are best positioned to dominate in the long term. The key players discussed are Mars Petcare, Nestlé Purina PetCare, The J.M. Smucker Company, Colgate-Palmolive Company (Hill's Pet Nutrition), Zoetis Inc., Elanco Animal Health, Hartz, Central Garden & Pet Company, Wahl Clipper Corporation, PetIQ, Virbac, Beaphar, Suprtails, Heads Up for Tails, Royal Canin, Others.

Mars Petcare – Global Leader in Pet Care with Synergistic Veterinary and Hygiene Offerings

Mars Petcare's dog and cat food brand portfolio, including Royal Canin and Iams, spans nutrition, veterinary care, and pet grooming. With over 2,000 U.S. veterinary hospitals and a target of using 100% renewable electricity by 2025, Mars Petcare leverages research from its Waltham Petcare Science Institute in product innovation through the grooming, dental, and wellness categories.

Colgate-Palmolive (Hill's Pet Nutrition) – Science-Driven Diet for Pet Wellness

Hill's Pet Nutrition is focused on clinically formulated products for dental and skin well-being, typically prescribed by veterinarians. Ongoing activity involves a movement away from private-label pet food and focus on branded growth and the acquisition of Prime100 to underpin its fresh pet food business.

Nestlé S.A. (Purina PetCare) – Innovation Leader in Pet Care in the Emerging Markets

Purina has a wide range of products from top brands such as Purina Pro Plan to mass market levels, with cat care being the driver of growth. The company is growing strongly in Greater China and making new product bets in dental care and grooming.

Zoetis Inc. – Global Animal Health and Hygiene Leader Specializing in Veterinary

Zoetis has pharmaceutical, diagnostic, and dermatology solutions, such as cutting-edge technologies like AI-assisted cytologic diagnostics with Vetscan Imagyst. Its diversified portfolio provides veterinarians with efficient hygiene and parasite control solutions, like the new Simparica Trio.

Spectrum Brands Holdings (Global Pet Care Division) – Multidiversified Pet Hygiene and Grooming Solutions Provider

Spectrum Brands markets a wide portfolio of grooming assist, dental care, and accessories, with recent strategic ventures in high-margin consumables. Spectrum Brands is diversifying the supply chain to reduce tariff exposure and innovating in premium pet health categories.

United States: Premiumization, Preventive Care, and Veterinary-Backed Innovation

The U.S. market for pet hygiene and care products is being transformed by the “humanization of pets” trend, where pets are treated as family members and their products mirror human wellness standards. This has led to growing demand for premium, allergen-free, and organic grooming solutions, including biodegradable shampoos, non-toxic conditioners, and hypoallergenic wipes. The market is also seeing growth in specialized categories such as oral care products like pet-specific toothpaste and medicated shampoos for skin health.

Technological innovation is another driver, with smart collars and AI-powered health monitoring tools allowing owners to track their pets’ well-being in real time. This shift from reactive to preventive health management is strengthening consumer trust in products backed by veterinary expertise. Large players, such as Mars Petcare, are integrating veterinary diagnostics and telehealth with product offerings, creating a holistic care ecosystem. The continued rise of e-commerce and subscription models is ensuring convenience and regular replenishment, making it easier for owners to maintain consistent hygiene routines.

China: Large-Scale Production, Domestic Boom, and Digital-First Marketing

China’s position as a global manufacturing hub for pet products gives it the ability to meet both local and international demand with speed and scale. Its domestic market is expanding rapidly, driven by urbanization, rising disposable incomes, and a younger demographic of pet owners seeking high-quality grooming and hygiene solutions.

E-commerce and social media dominate sales channels, with brands using livestreams, influencer marketing, and interactive content to educate consumers and promote new products. These platforms have also enabled niche and premium brands to reach targeted audiences quickly. Many Chinese companies are pursuing global expansion, operating overseas plants and exporting to over 50 countries, ensuring they meet international safety and quality standards.

India: Startup Ecosystem, Government Support, and Sustainability Push

India’s pet hygiene market is benefiting from government support for research, education, and best practices, combined with a surge of venture-backed pet care startups. These young companies are leveraging Direct-to-Consumer (D2C) and e-commerce platforms to deliver grooming, dental care, and skin health solutions across both metro and non-metro areas.

Urban pet owners are increasingly focused on preventive care, driving demand for products targeting skin infections, respiratory health, and oral hygiene. Sustainability is a strong differentiator, with demand for biodegradable waste bags, organic grooming kits, and eco-friendly packaging significantly outpacing global averages. This has created opportunities for brands to innovate in plant-based and low-impact formulations.

European Union: Regulatory Leadership, Sustainability Standards, and Veterinary Integration

The EU market is defined by stringent safety regulations, particularly regarding chemical composition in grooming and hygiene products, which encourages the use of natural, plant-based ingredients. Compliance with these rules is a selling point, as it reassures consumers about product safety and quality.

Sustainability is central to market growth, with manufacturers adopting biodegradable packaging, eco-friendly production methods, and traceable supply chains. Veterinary integration is also strong in the EU, with clinics and animal hospitals increasingly offering curated hygiene and care products alongside dietary advice, rehabilitation services, and preventive healthcare solutions. This integration strengthens consumer trust and reinforces the link between hygiene products and overall pet wellness.

Pet Hygiene and Care Products Market Report Scope

Pet Hygiene and Care Products Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$189.5 Billion

|

|

Market Size (2034)

|

$304.2 Billion

|

|

Market Growth Rate

|

5.4%

|

|

Segments

|

By Product Type (Grooming Products (Shampoos, Conditioners, Brushes), Waste Management (Litter, Waste Bags), Dental Care (Toothpaste, Brushes), Flea & Tick Control (Collars, Sprays, Shampoos), Eye & Ear Care, Paw & Skin Care), By Pet Type (Dogs, Cats, Other Pets), By Ingredient (Natural & Organic, Chemical-Based, Plant-Based), By Distribution Channel (Store-based (Specialty Pet Stores, Veterinary Clinics, Supermarkets), Online Retail), By Price Point (Mass Market, Premium)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Mars Petcare, Nestlé Purina PetCare, The J.M. Smucker Company, Colgate-Palmolive Company (Hill's Pet Nutrition), Zoetis Inc., Elanco Animal Health, Hartz, Central Garden & Pet Company, Wahl Clipper Corporation, PetIQ, Virbac, Beaphar, Suprtails, Heads Up for Tails, Royal Canin, Others.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Pet Hygiene and Care Products Market Segmentation

By Product

- Grooming Products

- Shampoos

- Conditioners

- Brushes

- Waste Management

- Dental Care

- Flea & Tick Control

- Eye & Ear Care

- Paw & Skin Care

By Pet Type

By Ingredient

- Natural & Organic

- Chemical-Based

- Plant-Based

By Distribution Channel

- Specialty Pet Stores

- Veterinary Clinics

- Supermarkets

- Online Retail

By Price Point

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Pet Hygiene and Care Products Market

- Mars Petcare

- Nestlé Purina PetCare

- The J.M. Smucker Company

- Colgate-Palmolive Company (Hill's Pet Nutrition)

- Zoetis Inc.

- Elanco Animal Health

- Hartz

- Central Garden & Pet Company

- Wahl Clipper Corporation

- PetIQ

- Virbac

- Beaphar

- Suprtails

- Heads Up for Tails

- Royal Canin

* List Not Exhaustive

Research Coverage

This report investigates the global Pet Hygiene & Care Products opportunity across premiumization, sustainability, and tech-enabled wellness, combining demand mapping with regulatory and channel intelligence. It explains breakthroughs in microbiome-safe skincare, at-home ultrasonic oral care, pet-safe disinfectants, and functional topicals, while our analysis reviews pricing ladders, refill/subscription models, and e-commerce acceleration. The study highlights regional dynamics in the U.S., EU, China, India, and Latin America, vendor strategies in grooming, dental, flea & tick, waste, eye/ear, and paw/skin care, and how veterinary integration is reshaping preventive routines. Produced by USDAnalytics, this report is an essential resource for product leaders, strategy teams, and investors prioritizing margin-accretive innovation and compliant growth. Scope includes-

- Segmentation: By Product (Grooming, Waste Management, Dental Care, Flea & Tick Control, Eye & Ear Care, Paw & Skin Care); By Pet Type (Dogs, Cats, Other Pets); By Ingredient (Natural & Organic, Chemical-Based, Plant-Based); By Distribution Channel (Specialty Stores, Veterinary Clinics, Supermarkets, Online Retail); By Price Point (Mass, Premium).

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Time Horizon: Historic data 2021–2024 and forecasts 2025–2034.

- Companies: Analysis/profiles of 15+ companies active across pet hygiene, veterinary, and omnichannel retail ecosystems.

Methodology

USDAnalytics applies a mixed-methods design: executive interviews (brand owners, veterinarians, clinic buyers, digital marketplaces, contract manufacturers) are merged with secondary evidence (company disclosures, regulatory actions, patent and clinical databases, retail SKU panels, web-scraped PDPs/reviews). A bottom-up build models category units, ASPs, and replenishment cycles by channel and ingredient class; a top-down lens reconciles with pet population, spend per pet, and veterinary procedure incidence. Elasticities are stress-tested for green-premium pricing, tariff shifts, private-label entry, and subscription attach. Forecasts use adoption S-curves for tech devices, cohort curves for natural/plant-based migration, and Monte Carlo ranges around regulation, raw-material costs, and e-commerce share.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.