Pet Repellent Collar Supplies Market Outlook – Smart, Sustainable, and Safety-Driven Solutions

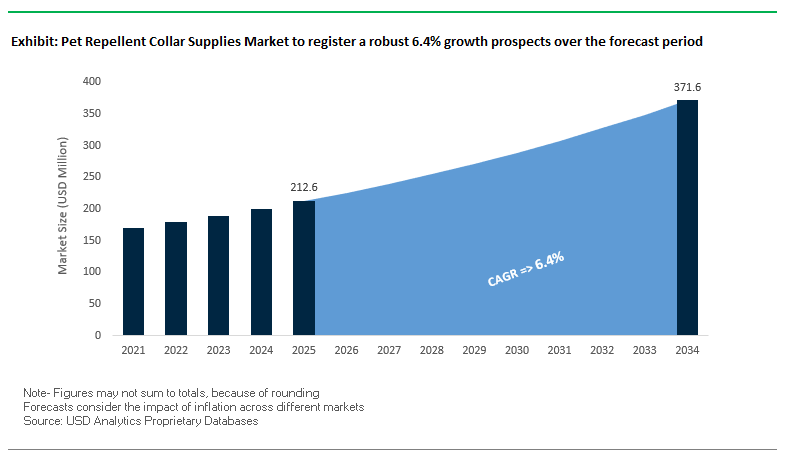

The global pet repellent collar supplies market is projected to grow from USD 212.6 million in 2025 to USD 371.6 million by 2034, at a CAGR of 6.4%. This growth is fueled by increasing consumer awareness regarding pet safety, effectiveness in pest control, and use of innovative technologies in pet accessories. The market is moving away from conventional chemical-based collars towards smart-enabled, multi-functional, and eco-friendly products that not only repel pests but also aid in overall pet health and behavioral control. Increasing demand for natural ingredients, ergonomically designed products, and longer protection periods is forcing companies to innovate. At the same time, e-commerce channel growth is improving access, enabling consumers to compare specifications and make informed buying decisions. Increasing usage of smart collars with GPS tracking, health monitoring, and app-supported features reflects the trend in the market towards comprehensive pet well-being solutions.

Key Insights for Industry Professionals

- Shift Toward Natural Formulations – Plant-based and essential oil-infused collars are meeting consumer demand for chemical-free pest control.

- Technology Integration – Ultrasonic deterrents, GPS tracking, and app-based controls are enhancing functionality.

- Extended Protection Cycles – Products offering 6–8 months of continuous pest prevention are gaining traction.

- E-commerce-Driven Growth – Online retail platforms are accelerating global product availability and brand reach.

- Holistic Wellness Approach – Collars are evolving into multipurpose devices, integrating pest control with health and safety features.

Pet Repellent Collar Supplies Market Analysis – Recent Developments and Strategic Shifts

The market is experiencing an age of rapid innovation and customer interest in safer, more efficient, and multi-functional pet care products. In June 2025, major companies launched new-generation inflatable pet collars developed from eco-friendly materials that provide comfort and mobility with greater ease of recovery after surgery. Government policies are also impacting the industry; in February 2025, the U.S. Environmental Protection Agency's Office of Inspector General expressed concerns regarding some pesticide-based collars such as Seresto, and the companies were forced to re-examine and update their safety standards.

The direction is toward health-focused and environmentally friendly products. Wild Earth launched its plant-based feline food in August 2024, riding the trend of pet humanization and the link between nutrition and health. Marketing, too, is evolving Eggland's Best's May 2024 ASMR campaign demonstrated how brands are leveraging sensory-led digital content to appeal to younger pet owners. Convergence is on the horizon, as Samsung's April 2024 launch of Bespoke AI Home Appliances previewed possible smart home-pet tech convergences, and WiTricity's July 2023 wireless charge initiative set the stage for wirelessly charged smart collars to come.

The Competitive Landscape is also affected by product diversification and acquisitions. Companies like PawCo Foods are introducing convenience-focused, plant-based nutrition foods, indirectly boosting the pest resilience of animals by way of improved health. On a general note, the market is moving toward premium, multifunctional, and science- and consumer-based safety-verified solutions.

Breakthrough Trends and High-Value Opportunities in the Pet Repellent Collar Supplies Market

Quantum Dot Tattoo Markers: Invisible, Durable Identifiers to Trigger Targeted Repellents

Biocompatible quantum dots delivered by dissolvable microneedle patches create UV/near-infrared-readable "tattoos" that are imperceptible beneath a pet's skin an elegant way to marry permanent identification with selective repellent activation. Peer-reviewed evidence shows near-infrared quantum-dot patterns remained brightly readable for 9 months in vivo and withstood ≥5 years of simulated sunlight in human cadaver skin models, highlighting robustness. The patch degrades in minutes to a painless, non-invasive mark; patterns are readable by a smartphone or scanner for decentralized data storage (ID, medical notes) and conditional logic (e.g., trigger coyote-specific deterrents while excluding harmless wildlife). For high-end pet safety ecosystems, this offers privacy-preserving identification, tamper resistance, and hands-free control of repellents.

AI-Powered Predator Recognition: On-Collar Sensing That Responds Only to Real Threats

Next-gen AI collars integrate on-board sensors (accelerometer, mic, camera), edge ML, and cloud models to detect predators vs. non-predators and only use humane deterrents when needed. Commercial baselines already exist: SATELLAI collars track behavior, energy, rest, and geofencing; Fi Series 3+ alerts for scratching/licking/eating/drinking; PetPuls infers emotion from more than 10,000 labeled barks; PetPace 2.0 provides vet-grade vital-sign analysis. Sharing these datasets with species/vocalization/motion signatures (e.g., coyote yips, raptor silhouettes) enables predictive analytics pre-emptive light/sound/odor pulses before a predator comes within range. Integrated with smart-home hubs, collars can sequence yard lights, sirens, or drone deterrents, making perimeter security more effective while minimizing false alarms.

Opportunity: Military K-9 Electronic Countermeasures (ECM) for Field Protection

Defense-grade ECM in K-9 collars/harnesses could spoof or jam adversary RF links (e.g., drone C2, remote initiators) using solid-state, low-SWaP modules. Leveraging airborne jammer roadmaps and handheld drone jammers, K-9 ECM would expand RF threat libraries, geofenced safe modes, and mission-profile presets (patrol, EOD support). The value case: force-multiplying K-9 survivability, handler risk reduction, and creating a new premium segment where repellent-class products overlap tactical counter-UAS and EW requirements.

Opportunity: Urban Wildlife Coexistence Tech for Humane, Automated Deterrence

With urbanization, automatic, non-lethal deterrents are required to control human-wildlife conflict (e.g., raccoons, coyotes) and protect pets. Research shows reactive hazing is often ineffective; best practice is humane, proactive exclusion. Auto-detecting collars that trigger directional ultrasound, strobe light, or species-specific scent can exclude "problem individuals" from gathering. Combined with public-education triggers (night-mode cat alarm, leash reminders), manufacturers can deliver turn-key coexistence systems following animal-welfare guidelines and municipal regulations.

Pet Repellent Collar Supplies Market Share Insights Revenue Drivers by Repellent Type and Technology

Chemical-Based Collars Lead, While Natural & Plant-Based Repellents Accelerate on Safety and Regulation

Chemically based repellent collars (55% share) remain the category leader for fleas/ticks/mosquitoes on the basis of broad-spectrum performance and extended wear-duration. Natural & plant-based solutions (citronella, neem, geraniol) are taking off at a rapid pace as pet parents Gen Z/Millennials are looking for green and non-toxic protection. Hybrid stacks (low-dose synthetics + botanicals) will gain momentum as companies balance strength with label positioning and meet EU/North America regulatory requirements. Messaging that balances efficacy data, residue transparency, and allergen guidance will win premium shelf space and DTC conversion.

Traditional Collars Remain Mainstream as Smart and Ultrasonic Systems Expand Multi-Function Protection

Legacy slow-release collars (60% market share) dominate on price, ubiquity, and simplicity, but smart collars (25%) are expanding most rapidly, with Bluetooth/app control, GPS, activity/health telemetry, and repellent capability for full protection. Ultrasonic collars occupy a chemical-free niche, a favorite with clients who value most toxin avoidance or wildlife-friendly deterrence; GPS + repellent combinations are expanding for work and outdoor dogs. What separates now is multi-modal stacks location + health AI + adaptive deterrents powered through subscription software (threat maps, battery health, firmware) to fuel ARPU and retention.

.png)

Competitive Landscape – Market Leaders and Innovation Pioneers in Pet Repellent Collar Supplies Industry

The pet repellent collar supplies market is controlled by a combination of multinational pet care companies and specialty entrepreneurs competing on product safety, durability, and multifunctionality. Large established brands rely on scientific logic and regulatory alliances to ensure trust, while small companies differentiate on natural ingredients and direct-to-consumer channels. As there is growing regulatory interference and consumer demand for safer, more environmentally friendly products, the competitive edge is in the integration of established pest control with innovative tech and renewable materials. Key players included are Zoetis Inc., Elanco Animal Health, Bayer AG (part of Elanco), Seresto (brand), Frontline (brand), Adams Pet Care, PetIQ, Wondercide, NiteRider, Bio-Groom, PetSafe, Hartz, Radio Systems Corporation, Yantai China Pet Foods Co., Ltd., Bridge PetCare, Others.

Bayer AG (Seresto Flea and Tick Collar)

Bayer's Seresto collar offers eight consecutive months of flea and tick protection using a polymer matrix slow-release technology. Even after EPA reviews, Bayer has committed additional safety validation and close collaboration with veterinarians, further enhancing long-duration pest control technology leadership.

Radio Systems Corporation (PetSafe)

PetSafe provides ultrasonic, static, and vibration collars of humane behavioral control, now supplemented with GPS tracking capabilities. Its product portfolio consists of waterproof models, rechargeable batteries, and more than one correction mode, appealing to pet owners who want both training and safety features in a single product.

Zoetis Inc.

A veterinary animal health giant, Zoetis has a wide portfolio of flea and tick protection outside of collars, including oral chews and topical treatments. Not in the collar game, but with the existing veterinary relationship and R&D focus, it is a big player in the larger pest control market.

Wondercide LLC

Wondercide centers on chemical-free, plant-based collars that contain essential oils such as peppermint. Its products are presented as complementary protection as a part of a larger natural pest control system, appealing to nature-oriented consumers who are looking for toxin-free pet care.

United States: Smart Connectivity, Humane Deterrents, and Natural Formulations

The U.S. market is at the forefront of tech-enabled pet repellency, integrating GPS tracking, health monitoring, and AI-driven behavioral analytics into multi-functional collars. These devices often employ biosensors to detect early health risks while incorporating humane deterrent methods such as ultrasonic signals, vibration, or gentle air sprays to redirect behavior without causing distress. A notable example is Coastal Pet Products’ air-spray collar, which reinforces the shift away from shock-based training.

The "humanization of pets" trend is also shaping product development, with growing demand for plant-based repellents featuring essential oils like neem, geraniol, and lavandin as alternatives to synthetic chemicals. Regulatory oversight from the FDA promotes product safety, accurate labeling, and evidence-backed efficacy claims, supporting consumer trust. Meanwhile, e-commerce channels dominate distribution, enabling broad SKU variety, user-generated reviews, and easy comparison shopping that influence brand selection.

China: Scale Manufacturing, Rapid Domestic Uptake, and Export Leadership

China’s role as a global manufacturing powerhouse in pet supplies gives it unmatched scalability, with companies like Yantai China Pet Foods producing collars and accessories for both domestic and international markets. Urban pet ownership growth, combined with rising disposable incomes, is fueling domestic demand for affordable, innovative repellency solutions.

Chinese firms are expanding global exports to over 50 countries, leveraging advanced automation, strict quality controls, and cost-efficient production models to remain competitive. Increasing technological investment including sensor integration and improved materials ensures compliance with international safety standards while appealing to both value-conscious and premium buyers.

European Union: Natural Formulations, Rigorous Safety Standards, and Consumer Transparency

The EU market is defined by stringent chemical-use regulations (e.g., REACH compliance), pushing manufacturers toward non-toxic, plant-based formulations to meet both safety and environmental benchmarks. The region’s emphasis on animal welfare and sustainability fosters innovation in humane deterrent technologies, avoiding harmful stimuli while maintaining efficacy.

Active research and development networks are driving ingredient testing, efficacy studies, and advanced repellency methods. Consumer protection laws mandate clear labeling of ingredients, usage guidelines, and potential side effects, enhancing brand credibility. EU buyers increasingly favor companies that demonstrate environmental stewardship alongside product safety.

India: Safety-Driven Standards, Digital Reach, and Rising Hygiene Awareness

India’s Bureau of Indian Standards (BIS) underpins product safety and quality, ensuring that collars meet essential performance and health benchmarks. E-commerce growth particularly via D2C brands is expanding availability beyond metro areas, allowing smaller-city pet owners to access advanced repellency solutions.

Rising awareness of flea, tick, and parasite risks among Indian pet owners is spurring demand for collars that offer both effectiveness and comfort. Local and international brands are responding with affordable, BIS-compliant products, often paired with digital campaigns that educate consumers about preventive pet care.

Pet Repellent Collar Supplies Market Report Scope

Pet Repellent Collar Supplies Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$212.6 Million

|

|

Market Size (2034)

|

$371.6 Million

|

|

Market Growth Rate

|

6.4%

|

|

Segments

|

By Pet Type (Dogs, Cats), By Repellent Type (Chemical-Based (Fipronil, Imidacloprid), Natural & Plant-Based (Essential Oils)), By Technology (Traditional Repellent Collars, Smart Collars (GPS, Health Monitoring), Ultrasonic Collars), By Duration (Short-Term (30-60 days), Long-Term (3-8 months)), By Distribution Channel (Store-based (Pet Stores, Veterinary Clinics, Supermarkets), Online Retail)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Zoetis Inc., Elanco Animal Health, Bayer AG (part of Elanco), Seresto (brand), Frontline (brand), Adams Pet Care, PetIQ, Wondercide, NiteRider, Bio-Groom, PetSafe, Hartz, Radio Systems Corporation, Yantai China Pet Foods Co., Ltd., Bridge PetCare, Others.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Pet Repellent Collar Supplies Market Segmentation

By Pet Type

By Repellent Type

- Chemical-Based

- Natural & Plant-Based (Essential Oils)

By Technology

- Traditional Repellent Collars

- Smart Collars (GPS, Health Monitoring)

- Ultrasonic Collars

By Duration

- Short-Term (30-60 days)

- Long-Term (3-8 months)

By Distribution Channel

- Store-based

- Pet Stores

- Veterinary Clinics

- Supermarkets

- Online Retail

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Pet Repellent Collar Supplies Market

- Zoetis Inc.

- Elanco Animal Health

- Bayer AG (part of Elanco)

- Seresto (brand)

- Frontline (brand)

- Adams Pet Care

- PetIQ

- Wondercide

- NiteRider

- Bio-Groom

- PetSafe

- Hartz

- Radio Systems Corporation

- Yantai China Pet Foods Co. Ltd.

- Bridge PetCare

* List Not Exhaustive

Research Coverage

This report investigates the global Pet Repellent Collar Supplies landscape, mapping demand shifts from chemical-centric solutions to smart, plant-based, and ultrasonic deterrents. It synthesizes breakthroughs in GPS- and health-enabled collars, humane ultrasonic systems, and safety-led designs, while our analysis reviews regulatory actions, e-commerce acceleration, and multi-function product stacks that merge location, health AI, and adaptive repellency. The study highlights revenue trajectories by repellent type and technology, vendor playbooks across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa, and the strategies of leading brands in long-duration and natural formulations. Produced by USDAnalytics, this report is an essential resource for industry professionals evaluating innovation pipelines, partnership opportunities, and go-to-market priorities in a safety- and sustainability-driven collar market. Scope includes-

- Segmentation: By Pet Type (Dogs, Cats); By Repellent Type (Chemical-Based, Natural & Plant-Based); By Technology (Traditional, Smart/GPS & Health Monitoring, Ultrasonic); By Duration (Short-Term 30–60 days, Long-Term 3–8 months); By Distribution Channel (Store-based, Online Retail).

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Time Horizon: Historic data from 2021–2024 and forecasts for 2025–2034.

- Companies: Analysis/profiles of 15+ manufacturers and brands shaping product safety, efficacy, and connectivity.

Methodology

Our approach blends primary interviews (product managers, veterinarians, regulatory experts, channel partners) with secondary intelligence (company filings, patent activity, recall databases, customs/shipment trackers, and retail SKU analytics). We triangulate market sizing through bottom-up model builds (unit shipments × ASP × renewal cycles) cross-checked against top-down spends in pest prevention and connected-pet categories. Cohort analysis separates chemical, botanical, ultrasonic, and smart stacks, while pricing waterfalls capture subscription and accessory attach rates. Scenario modeling quantifies regulatory impact, e-commerce penetration, and technology adoption curves, with sensitivity tests on repellent duration, efficacy claims, and component costs to deliver decision-ready, defensible forecasts.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.