Market Analysis: Innovation, AI Integration, and Subscription Models Drive Growth in the Pet Wearable Market

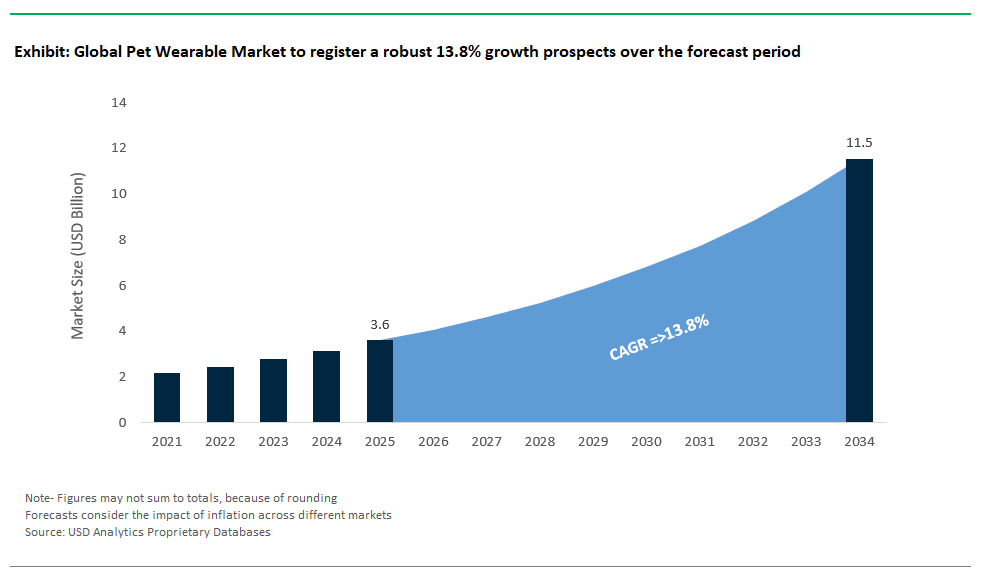

The Global Pet Wearable Market Size is estimated at $3.6 Billion in 2025 and is forecast to register an annual growth rate (CAGR) of 13.8% to reach $11.5 Billion by 2034.

The pet wearable market is seeing remarkable growth and diversification, driven by innovative brands and evolving consumer needs. In January 2024, Austrian tech leader Tractive expanded its offerings in the UK by launching pet insurance policies, cleverly integrating financial protection with its established base of pet wearable device users. This strategy demonstrates how pet tech companies are merging services such as insurance with GPS tracking and health monitoring to deliver comprehensive solutions for pet owners. At the same time, PetPace released its next-generation Health 2.0 smart dog collar in October 2023, which brings a new level of continuous health monitoring for pets. The collar uses AI to track vital signs like heart rate variability, temperature, posture, sleep quality, and more, offering early symptom detection and robust disease management empowering owners to be proactive about their pets’ well-being.

Research partnerships and ongoing technological advancements are further propelling the pet wearable industry forward. In November 2023, PetPace teamed up with the Veterinary Health Research Centers (VHRC) for the “DOGMA” initiative, using its biometric collars to study cognitive decline in aging dogs and draw parallels to human Alzheimer’s disease. This shows that pet wearables now play a vital role not just in daily monitoring but also in advanced veterinary research, unlocking insights into pet and even human health. Meanwhile, leading brands like Garmin, Tractive, and Whistle Labs are investing in constant upgrades, launching new devices and rolling out software enhancements that provide pet owners with even greater GPS accuracy and longer battery life addressing two of the most common pain points in pet tech today.

A major trend shaping the global pet wearable market is the rapid integration of artificial intelligence and the rise of subscription-based business models. Companies are embedding sophisticated AI into their wearable platforms, allowing for deeper behavioral analysis, detection of subtle emotional changes, and smarter health alerts. This enables owners to track their pets’ activity, stress, and sleep patterns more precisely than ever before. Furthermore, many pet wearable brands are introducing subscription services that unlock premium features such as advanced health analytics, virtual fencing, personalized wellness reports, and real-time alerts making high-tech pet care more accessible and tailored. As a result, the pet wearable industry is not only growing rapidly but is also setting new standards for digital, connected, and personalized pet health management.

Key Developments in the Pet Wearable Market

Trend: Multi-Sensor Early Disease Detection Collars

The pet wearable market is witnessing significant advancements with the emergence of multi-sensor early disease detection collars, fundamentally enhancing pet health monitoring capabilities. Unlike basic activity trackers, these advanced devices integrate sophisticated sensor arrays including gait analysis and temperature sensors to provide highly accurate predictions of chronic disease flare-ups, such as canine osteoarthritis. These precise insights enable pet owners and veterinarians to proactively manage pet health, significantly improving pets' quality of life. A notable example is Maven Pet Health Tracker, which utilizes multi-sensor fusion to continuously monitor vital parameters like resting respiratory rate, hydration, temperature fluctuations, and even itching behaviors, alerting pet owners to early signs of illness before they escalate into serious health issues.

Further boosting this trend, AI-powered innovations in 2024 have set new standards in pet health diagnostics. PetPace smart collars have integrated artificial intelligence to monitor an extensive range of vital signs, including temperature, pulse rate, respiration, heart rate variability, posture, and caloric expenditure. These capabilities facilitate timely veterinary intervention, reducing unnecessary clinic visits and costs associated with managing chronic conditions. Additionally, collars capable of advanced cardiovascular monitoring, detecting potentially life-threatening irregular heart rhythms like atrial fibrillation, represent a major leap forward in veterinary cardiac diagnostics. These developments highlight multi-sensor collars as a transformative technology in pet healthcare, driving growth and innovation across the pet wearable market.

Opportunity: Predator Deterrent Wearables for Rural Livestock-Guardian Dogs

Wearable technologies designed specifically for livestock-guardian dogs (LGDs) present a considerable growth opportunity within the pet wearable market, especially in rural regions vulnerable to livestock predation. GPS-enabled collars equipped with advanced vibration-based deterrent systems have shown effectiveness in deterring predators such as coyotes and wolves, providing ranchers with a modern, non-lethal alternative to traditional predator-control methods. Pilot programs employing these innovative solutions have demonstrated significant reductions in livestock losses, underscoring the substantial market potential across North American ranches.

Research consistently supports the effectiveness of LGDs as one of the most reliable non-lethal deterrent methods, significantly reducing predation by coyotes, wolves, and foxes. Emerging sensor-based detection systems utilizing GPS tracking demonstrate promising results by alerting dogs to predator threats through increased monitoring of livestock movements. Notably, innovations such as "BarkLight," which provide collar-mounted visual and auditory deterrents, have received independent validation as effective, humane alternatives to lethal predator control, gaining traction among ranchers seeking sustainable solutions. Given the growing demand for advanced protective measures for livestock and the substantial economic impact of predator-related losses, this specialized segment of predator-deterrent wearables represents a substantial and underserved market opportunity within the broader pet wearable industry.

Competitive Landscape: Pet Wearable Market

The pet wearable market is evolving rapidly, driven by rising pet humanization, demand for health monitoring, and advancements in IoT and AI technologies. Modern pet owners seek solutions that offer real-time location tracking, health analytics, and wellness insights, transforming collars into connected devices that enhance safety and preventive care. The competitive landscape is marked by companies integrating GPS, biometrics, AI-driven diagnostics, and app-based ecosystems to deliver personalized, data-driven pet care. Innovation in smart collars and trackers is complemented by growing veterinary adoption, subscription-based models, and expansion into new markets, reinforcing the role of wearables in proactive pet health management.

FitBark (Mars Inc.) – AI-Driven GPS and Health Monitoring Leader

FitBark, a Kinship Partners brand under Mars Inc., leads in pet GPS tracking and health analytics, offering lightweight, waterproof devices designed as collar attachments for dogs and cats. Its flagship solutions provide real-time GPS tracking, location history, customizable “Safe Place” alerts, and comprehensive health monitoring, including activity levels, calorie expenditure, sleep patterns, and mobility trends. FitBark’s app ecosystem, available across iOS, Android, web, and smartwatches, delivers intuitive insights for owners and veterinarians. The brand stands out with its AI-based data analysis, enabling comparisons across global pet datasets, and is widely adopted in veterinary research, being used by over 100 vet schools. Recent advancements include the launch of FitBark GPS 2nd Generation, improved nationwide coverage, and Apple Watch integration for seamless access to pet health metrics. Strategic partnerships with Fitbit and Elanco amplify its role in promoting human-pet fitness and preventive healthcare. With availability in 150+ countries, FitBark combines consumer convenience with professional-grade analytics, cementing its leadership in health-focused pet wearables.

Whistle (Mars Petcare) – Smart Collars for Location and Wellness Insights

Whistle, another Mars Petcare brand, offers smart collars integrating GPS tracking, activity monitoring, and wellness alerts to provide owners with peace of mind and actionable health data. These devices leverage cellular connectivity for real-time location tracking, alongside features like virtual fences, customizable alerts, and caloric expenditure insights. Whistle continues to innovate with improved battery performance and expanding health intelligence capabilities, aligning with the trend toward connected ecosystems in pet care. Backed by Mars Petcare’s extensive resources, Whistle benefits from integration opportunities with Mars’ nutrition and veterinary services, enhancing its positioning as part of a holistic pet wellness platform. By prioritizing pet safety, activity tracking, and behavioral monitoring, Whistle addresses key consumer concerns while reinforcing Mars’ dominance in the connected pet technology space.

PetPace – Veterinary-Grade Health Monitoring and AI Analytics

PetPace differentiates itself as a clinical-grade smart collar provider, offering advanced multi-parameter monitoring that goes beyond activity tracking to include heart rate, respiratory rate, body temperature, heart rate variability (HRV), stress indicators, posture, and caloric burn. Its AI-powered platform transforms raw data into actionable insights through wellness scores and pain indicators, positioning it as a tool for proactive health management and chronic disease monitoring. Designed for veterinary integration, PetPace supports post-operative recovery tracking, pregnancy monitoring, and outpatient care, reinforcing its role in tele-veterinary solutions. The recent launch of PetPace 2.0 brings enhanced sensors, improved GPS accuracy, and deeper AI-driven insights. Recognized as a Top Pet Tech 2025 innovator, PetPace continues to lead in clinical adoption, supported by the world’s largest pet health data repository. With applications extending to behavioral analysis and specialized breeding programs, PetPace is redefining the future of preventive and predictive pet care.

Tractive – GPS and Health Insights with Insurance Integration

Tractive is a Europe-based leader specializing in GPS-enabled pet trackers with integrated health monitoring, serving both dogs and cats. Its products offer live location tracking, activity and sleep analytics, virtual fencing, and escape alerts, while advanced models monitor resting heart and respiratory rates, signaling early health concerns. Recent innovations include bark detection for separation anxiety and community-driven danger reports, enhancing pet safety. Tractive’s strategic move into pet insurance (2024) represents a game-changing model that leverages its health data capabilities to deliver risk-based policies, deepening its engagement in the pet care ecosystem. With a user-friendly app, durable waterproof design, and feature-rich subscription services, Tractive continues to expand globally, driven by strong funding rounds and diversification into feline-specific devices. Its emphasis on real-time safety, preventive health, and insurance integration makes Tractive a formidable player in the smart pet wearables space.

Invoxia – Pioneering Biometric Tracking for Heart Health

Invoxia brings innovation to the pet wearable market through its Minitailz Biotracker GPS, combining real-time GPS tracking with advanced biometric monitoring for cardiac health. This device monitors resting heart rate, respiratory rate, activity, sleep, and behavioral indicators, providing a holistic picture of pet well-being. Using patent-pending sensor technology and AI-driven algorithms, Minitailz identifies health baselines and detects early signs of conditions like congestive heart failure, addressing a critical gap in preventive veterinary care. Recognized at CES 2024 for innovation, Invoxia’s focus on heart health differentiates it in a crowded marketplace. The device also offers features like LED-based location assistance, virtual fences, and subscription-based analytics. By aligning IoT innovation with medical-grade monitoring, Invoxia positions itself at the intersection of consumer convenience and clinical relevance, appealing to both tech-savvy pet owners and veterinary professionals.

Market Share and Segmentation Insights: Pet Wearable Market

By Product Type: Smart Collars Lead, Smart Harnesses/Vests Grow Fastest

In 2025, smart collars hold the largest share of the pet wearable market at 56.1%, making them the most widely adopted solution for GPS tracking, activity monitoring, and real-time health metrics such as heart rate and body temperature. Their affordability and multifunctionality have made them essential for pet owners seeking safety and fitness tracking solutions. Meanwhile, smart harnesses and vests are projected to grow at the fastest CAGR of 15.3% through 2034, fueled by rising demand for advanced biometric features like stress and anxiety detection, posture analysis, and performance monitoring for working dogs in military, law enforcement, and service applications. Additionally, smart cameras are gaining significant traction as owners prioritize remote monitoring and AI-powered behavior analysis for real-time pet engagement, while other tracking devices like RFID tags and microchip implants remain important for permanent identification and security.

.png)

By Animal: Dogs Dominate, Cat Segment Accelerates Rapidly

Dogs account for the dominant share of the market, representing 70.4% in 2025, largely due to their higher ownership rates and the widespread use of wearables for training, activity monitoring, and security purposes. Pet owners increasingly adopt wearable technology for real-time health tracking and geofencing capabilities, ensuring safety during outdoor activities. On the other hand, cats are emerging as the fastest-growing segment, with a CAGR of 14.9%, as innovative lightweight GPS-enabled collars and AI-driven behavior trackers become more popular among cat owners. These devices address growing concerns over outdoor exploration and indoor health monitoring for felines. Additionally, other animals, including livestock, birds, and exotic pets, account for a niche yet growing segment driven by precision farming needs and specialty applications in veterinary health monitoring.

United States Pet Wearable Market Surges with Veterinary Partnerships and Advanced Health Monitoring

The United States stands at the forefront of the global pet wearable market, propelled by a wave of veterinary integration and cutting-edge product innovation. Companies such as PetPace have deepened their collaboration with veterinary clinics, deploying smart collars nationwide that monitor vital signs and behavior, enabling early detection of health issues and supporting clinical decision-making. This medical-grade adoption is complemented by leading brands like Whistle Labs, which enhanced their offerings in 2024 with real-time GPS tracking and the rollout of advanced features such as AI-powered digestive health insights. Meanwhile, FitBark has prioritized holistic health monitoring, providing American pet owners with detailed data on sleep, activity, and behavioral changes, while also facilitating direct collaboration with veterinarians through shared health analytics.

The surge in AI-powered behavior analysis further distinguishes the U.S. market, with startups introducing devices capable of interpreting barking patterns and stress levels, as highlighted during CES 2025. This innovation ecosystem is nurtured by active venture capital investment, with funds like Ani.vc targeting disruptive startups in pet longevity and wearable tech. These dynamics, combined with a mature digital infrastructure and high pet ownership rates, drive rapid adoption of pet wearables for health, safety, and peace of mind reinforcing the U.S. as the global leader in this fast-evolving sector.

China’s Pet Wearable Market Grows Rapidly with Smart Tech Integration and Urban Demand

China’s pet wearable market is experiencing robust growth, underpinned by soaring pet ownership, urbanization, and a strong focus on smart technology. Chinese manufacturers and investors are heavily engaged in launching new smart pet devices, with wearables featuring prominently among consumer electronics offerings. The market is fueled by an urban middle class seeking convenience pet owners increasingly purchase smart collars, cameras, and monitors for remote surveillance and interaction, all of which easily integrate with mobile apps and smart home ecosystems. These solutions address the needs of busy lifestyles in major Chinese cities, enabling owners to monitor and care for their pets from afar.

Technological sophistication is a hallmark of Chinese pet wearables, with manufacturers rapidly adopting AI for automated feeding schedules, health tracking, and behavioral analysis. RFID-enabled collars are gaining momentum for pet identification and tracking, supported by municipal policies and rising concerns over lost pets. As AI and digital infrastructure continue to advance, Chinese consumers are expected to drive further innovation in wearable tech for pets, making China one of the fastest-growing and most dynamic markets in the global pet wearable landscape.

Germany Pet Wearable Market Driven by GPS Adoption and Health-Focused Consumers

Germany’s pet wearable market is characterized by high engagement with GPS tracking technologies and a discerning, health-focused pet owner base. With many German pet owners leading active outdoor lifestyles, there is strong demand for GPS-enabled collars and trackers to ensure pet safety and real-time location awareness. Leading brands like Tractive, which reported a 45% revenue increase to €87 million in 2023, continue to grow rapidly in Germany, confirming widespread consumer adoption of smart tracking solutions.

Alongside GPS, German consumers show strong interest in advanced health monitoring wearables that track heart rate, sleep quality, calorie expenditure, and other wellness indicators. The integration of wearable-generated data into veterinary care is increasingly common, as German veterinarians recommend these tools for early disease detection and personalized health management. There is also a robust premium segment, with pet owners seeking reliable, high-quality devices. Together, these trends create a sophisticated and steadily expanding German pet wearable market where innovation and user trust are closely linked.

Japan’s Pet Wearable Market Expands with Precision, Health Monitoring, and Disaster Preparedness

Japan’s pet wearable market is shaped by its aging pet population and a cultural emphasis on precision engineering and safety. The demand for health-monitoring devices is growing, especially those capable of tracking vital signs and identifying early illness in senior pets. Japanese manufacturers excel in miniaturization, delivering compact, comfortable, and highly accurate wearables that cater to small-breed dogs and cats prevalent in urban areas.

Disaster preparedness is another critical factor in Japan, with a strong focus on reliable identification and tracking technologies to reunite pets and owners during emergencies. Integration with smart home ecosystems is increasing, with wearables feeding data to automated feeders and home management apps. Japanese universities and research centers are active in AI-driven pet tech, working on solutions that interpret animal emotions and personalize health recommendations. This multifaceted approach ensures Japan remains at the cutting edge of pet wearable innovation, balancing health, convenience, and safety.

United Kingdom Pet Wearable Market Thrives on Increased Pet Ownership and Ethical Innovation

The United Kingdom’s pet wearable market is expanding rapidly, propelled by a post-pandemic boom in pet ownership and a growing emphasis on health, activity, and lost pet prevention. UK pet owners widely adopt activity and behavioral monitors, tracking everything from exercise levels to sleep and mood changes. Real-time GPS trackers and smart collars equipped with virtual fences are highly sought after, addressing strong consumer concerns over lost pets in both urban and rural environments.

The UK’s vibrant pet tech startup ecosystem brings continual innovation, introducing new wearables focused on specialized health monitoring and unique design features. Ethical consumerism plays a central role, with buyers seeking wearables made by brands with transparent supply chains and responsible manufacturing practices. The UK’s market thus combines technological sophistication, consumer consciousness, and entrepreneurial energy, solidifying its place as a European leader in pet wearables.

Canada Pet Wearable Market Benefits from Outdoor Culture and Veterinary Integration

Canada’s vast natural landscapes and active lifestyles create strong demand for durable GPS and activity trackers suitable for outdoor adventures with pets. Canadian pet owners value wearables that provide reliable health and activity data, helping monitor their pets’ wellness whether hiking, camping, or navigating city life. E-commerce channels are essential for pet wearable sales, offering broad access and fast delivery across the country.

The Canadian veterinary sector is increasingly open to integrating data from pet wearables into routine care, utilizing health insights to inform diagnostics and personalized treatment plans. As adoption rises, collaboration between tech developers and veterinarians continues to grow, helping ensure that pet wearables address real clinical needs as well as consumer preferences.

Australia Pet Wearable Market Grows with High Pet Ownership and Outdoor Activity Demand

Australia boasts one of the world’s highest pet ownership rates, fueling a vibrant market for pet wearables. With 69% of households owning pets, demand is high for robust GPS trackers and health monitors that support an active, outdoor lifestyle. Rural and semi-rural pet owners particularly value wearables for their ability to prevent pet loss and ensure safety across vast properties.

Australians are also keen adopters of smart home technology, increasingly integrating pet wearables with other connected devices for seamless remote monitoring and control. Health and safety remain top priorities, driving growth in the use of data-driven pet health trackers and wellness monitors.

France Pet Wearable Market Grows on Health, Comfort, and Regulatory Standards

French pet owners are deeply invested in products that enhance their pets’ quality of life, with a growing market for smart wearables that monitor health and ensure comfort. There is significant demand for devices that track wellness indicators and support proactive healthcare, echoing trends in Germany and other leading European markets.

Urbanization has increased the need for tracking and monitoring solutions, especially for pets living in apartments or frequently visiting public parks. France’s adherence to EU data privacy and safety regulations shapes product development, ensuring high standards in both device functionality and user protection. As the French pet wearable market evolves, it is defined by a blend of innovation, consumer care, and regulatory compliance.

Pet Wearable Market Report Scope

Pet Wearable Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.6 Billion

|

|

Market Size (2034)

|

$11.5 Billion

|

|

Market Growth Rate

|

13.8%

|

|

Segments

|

By Product Type (Smart Collars, Smart Cameras, Smart Harnesses/Vests, Other Tracking Devices), By Technology (GPS (Global Positioning System), RFID (Radio-Frequency Identification), Sensors, Bluetooth, Wi-Fi Integration, Cellular Connectivity), By Application (Identification & Tracking, Monitoring & Control, Medical Diagnosis & Treatment, Safety & Security, Communication & Entertainment), By Animal (Dogs, Cats, Other Animals), By Sales Channel (Online, Offline)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Whistle Labs (a subsidiary of Mars Petcare), Tractive GmbH, Garmin Ltd., FitBark Inc., PetPace Ltd., Link AKC, Motorola, Datamars, GoPro Inc., Felcana, Scollar, Kyon, Loc8tor Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Pet Wearable Market Segmentation

By Product Type

- Smart Collars

- Smart Cameras

- Smart Harnesses/Vests

- Other Tracking Devices

By Technology

- GPS (Global Positioning System)

- RFID (Radio-Frequency Identification)

- Sensors

- Bluetooth

- Wi-Fi Integration

- Cellular Connectivity

By Application

- Identification & Tracking

- Monitoring & Control

- Activity Monitoring

- Behavioral Monitoring

- Training/Bark Control

- Medical Diagnosis & Treatment

- Health Monitoring

- Therapeutic Devices

- Safety & Security

- Communication & Entertainment

By Animal

By Sales Channel

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Pet Wearable Market

- Whistle Labs (a subsidiary of Mars Petcare)

- Tractive GmbH

- Garmin Ltd.

- FitBark Inc.

- PetPace Ltd.

- Link AKC

- Motorola

- Datamars

- GoPro Inc.

- Felcana

- Scollar

- Kyon

- Loc8tor Ltd.

* List Not Exhaustive

Research Coverage

This USDAnalytics report provides an in-depth analysis of the global pet wearable market, presenting historic data from 2021 to 2024 and market forecasts from 2025 to 2034. The study examines key metrics such as market size, CAGR, and value growth, alongside transformative trends including AI-powered early disease detection, the proliferation of GPS and biometric innovation, and the evolution of subscription-based pet care models.

Comprehensive segmentation is included by:

- Product Type: Smart collars, smart cameras, smart harnesses/vests, other tracking devices

- Technology: GPS, RFID, sensors, Bluetooth, Wi-Fi integration, cellular connectivity

- Application: Identification & tracking, monitoring & control (activity, behavioral, training), medical diagnosis & treatment (health monitoring, therapeutic devices), safety & security, communication & entertainment

- Animal Type: Dogs, cats, other animals

- Sales Channel: Online and offline

Geographic coverage spans North America, Europe, Asia Pacific, South America, and Middle East & Africa, with country-level insights for the United States, China, Germany, Japan, United Kingdom, Canada, Australia, and France. The report contextualizes regional dynamics such as the U.S.’s leadership in advanced veterinary adoption, China’s surge in smart tech integration, and Europe’s rapid embrace of pet tech innovation.

Competitive landscape analysis profiles leading players including Whistle Labs (Mars Petcare), Tractive GmbH, Garmin Ltd., FitBark Inc., PetPace Ltd., and others, emphasizing R&D priorities, AI integration, and the growing ecosystem of pet health monitoring solutions.

The USDAnalytics report is designed to provide manufacturers, technology providers, investors, and market stakeholders with actionable insights, helping to capitalize on evolving opportunities in the global pet wearable sector through both historic perspective and forward-looking intelligence.

Deliverables:

- Full Market Research Report (PDF, Excel): Complete data tables, market charts, and visual insights.

- Country-Level Forecasts & Analysis.

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis.

- Recent Developments & News Tracker

- Executive Summary & Analyst Insights.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.