Phosphate Conversion Coatings for Oil and Gas Market Size, Corrosion Protection Demand, and Energy Infrastructure Expansion

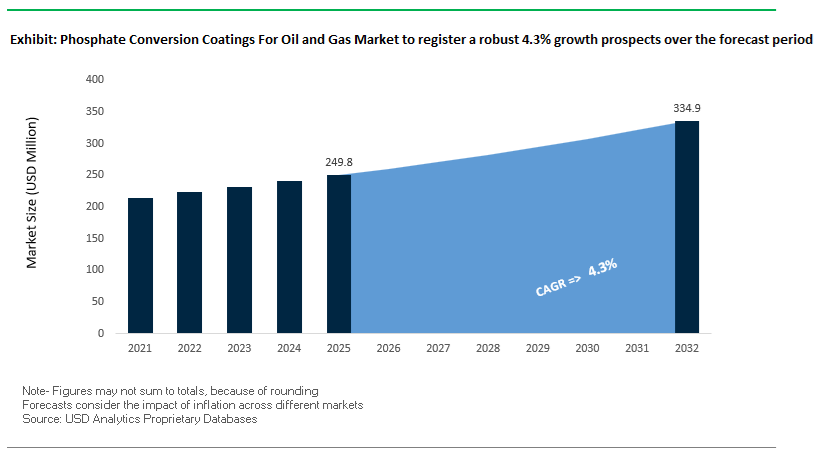

The global Phosphate Conversion Coatings for Oil and Gas Market was valued at $249.8 million in 2025 and is projected to grow at a CAGR of 4.3% through 2032, reaching $335.4 million by 2032. This growth is driven by the increasing need for robust corrosion protection, enhanced surface adhesion, and wear resistance in upstream, midstream, and downstream oil and gas operations.

Phosphate conversion coatings play a critical role as pre-treatment layers that improve the adhesion of subsequent coatings such as epoxies and polyurethanes, while also providing lubrication, anti-galling properties, and baseline corrosion resistance. In oil and gas applications, these coatings are essential for oil-country tubular goods (OCTG), drill pipes, subsea components, valves, and pipeline systems, where exposure to harsh chemicals, high pressures, and extreme temperatures is constant.

A key growth driver is the expansion of global energy infrastructure, particularly in the Middle East, North America, and Asia-Pacific, where investments in offshore platforms, LNG terminals, and pipeline networks are increasing. Additionally, the rising complexity of oil extraction methods, including deepwater drilling and unconventional resources, is intensifying the demand for high-performance surface treatments capable of withstanding aggressive operating environments.

The market is also evolving under the influence of environmental regulations and sustainability goals, prompting a transition toward chrome-free, low-sludge, and energy-efficient phosphating technologies. Innovations in nanostructured coatings, hybrid coating systems, and cold-process phosphating are improving performance while reducing environmental impact, positioning phosphate conversion coatings as a critical component of modern oilfield materials engineering.

Market Analysis: Regional Expansion, Eco-Phosphating Technologies, and Hybrid Coating Systems Driving Market Evolution

Recent developments in the Phosphate Conversion Coatings for Oil and Gas Market reflect a strong focus on regional expansion, environmental innovation, and advanced performance engineering. In March 2026, Master Builders Solutions completed the acquisition of Arkaz Al Sharq, strengthening its presence in Saudi Arabia and enabling localized production of high-performance conversion coatings for large-scale infrastructure initiatives such as Vision 2030. This move underscores the importance of regional manufacturing and supply chain proximity in serving major energy projects.

Technological advancements are enhancing both performance and sustainability. Henkel’s expansion of its Bonderite portfolio (February 2026) introduces cold-process manganese phosphating, reducing energy consumption while maintaining the high load-bearing and wear resistance required for subsea equipment. Similarly, Chemetall’s Viant® eco-phosphating technology (November 2025) addresses environmental concerns by reducing sludge formation, a major challenge in traditional phosphating processes.

Product innovation is also targeting increasingly demanding operating conditions. Nihon Parkerizing’s nanostructured manganese phosphate coatings (October 2025) improve wear resistance and oil retention, extending maintenance intervals for drilling equipment. Meanwhile, AkzoNobel’s offshore-optimized conversion systems enhance adhesion for high-build epoxy coatings, supporting long service life requirements in corrosive marine environments.

Regulatory compliance is reshaping formulation strategies. PPG’s transition toward chrome-free conversion coatings (February 2026) aligns with tightening REACH and EPA regulations, reducing reliance on hazardous hexavalent chromium. In parallel, Sherwin-Williams’ integrated pre-treatment solutions (January 2026) focus on manganese phosphate coatings for OCTG applications, improving assembly efficiency and reducing equipment wear.

Emerging hybrid technologies are further expanding performance boundaries. Ionbond’s hybrid PVD/phosphate coating initiative (September 2025) combines the lubricating properties of phosphate layers with the hardness of PVD coatings, enabling tools to withstand extreme pressures in horizontal drilling operations. Additionally, Hempel’s expansion into pipeline pre-treatment solutions (March 2025) highlights growing demand in the midstream sector for integrated corrosion protection systems.

Market Trend: Manganese Phosphate Coatings Enhancing Anti-Galling Performance in Ultra-Deepwater HPHT Applications

The phosphate conversion coatings market in the oil and gas industry is evolving with a clear shift toward manganese phosphate systems for ultra-deepwater and high-pressure/high-temperature environments. As drilling operations extend into harsher subsea conditions, the mechanical integrity of threaded connections and wellhead components has become a critical reliability factor. Manganese phosphate coatings are increasingly specified to address severe wear, friction, and galling challenges during repeated makeup and breakout cycles.

Manganese phosphate coatings provide significantly thicker crystalline layers, typically ranging from 10 to 40 microns, compared to the 1 to 5 microns associated with zinc phosphate systems. This increased coating thickness enhances lubricant retention capacity, allowing the porous structure to act as a reservoir for synthetic lubricants. As a result, wear life of critical components such as couplings and threaded connections improves by approximately 35% to 50%, reducing maintenance frequency and operational risk in subsea environments.

Anti-galling performance is a key differentiator. The higher surface hardness of manganese phosphate coatings minimizes friction-induced surface damage on high-alloy steels, ensuring consistent torque application during assembly and disassembly of wellhead systems. This is particularly important in deepwater installations where mechanical failure can lead to costly downtime and safety hazards.

Friction control is further optimized through the coating’s microcrystalline structure, which maintains a stable coefficient of friction in the range of 0.12 to 0.15 under load. This consistency is essential for maintaining seal integrity and preventing leakage in high-pressure subsea systems. These combined performance benefits are driving the widespread adoption of manganese phosphate coatings in advanced offshore drilling operations.

Market Trend: Zinc Phosphate Hybrid Systems Improving Corrosion Resistance in Sour Service Environments

In sour service environments characterized by the presence of hydrogen sulfide and carbon dioxide, zinc phosphate coatings integrated with corrosion inhibitors are gaining traction as a critical protective solution. These hybrid systems are specifically engineered to mitigate risks associated with hydrogen-induced cracking and sulfide stress cracking in downhole tubulars and pipelines.

Advanced zinc phosphate coatings provide a stable conversion layer that enhances adhesion for organic corrosion inhibitors, creating a synergistic protection mechanism. Laboratory testing demonstrates that these integrated systems can reduce corrosion rates in seawater and brine environments from approximately 119 mils per year to as low as 1.77 mils per year, representing a reduction efficiency of around 98.5%. This significant improvement in corrosion resistance extends the service life of carbon steel components operating in aggressive chemical conditions.

The incorporation of hydrogen sulfide scavengers further enhances protection. Modern formulations achieve scavenging efficiencies exceeding 90%, neutralizing reactive sulfur species before they can penetrate the substrate and initiate cracking mechanisms. This proactive chemical control is critical in maintaining structural integrity in sour crude and gas production systems.

The phosphate conversion layer also plays a vital role in extending barrier longevity. By providing a stable and anchored surface for inhibitor films, these coatings extend the effective protection window by three to four times compared to standalone liquid inhibitor treatments. This reduces the frequency of maintenance interventions and improves operational reliability in downhole environments. These performance characteristics are positioning zinc phosphate hybrid systems as a key solution for corrosion management in sour service applications.

Market Opportunity: BSEE 2026 Well Control Regulations Driving Demand for High-Reliability Phosphate-Coated Components

The proposed revisions to the Well Control Rule by the Bureau of Safety and Environmental Enforcement are creating a significant opportunity for phosphate conversion coatings in offshore oil and gas operations. The updated regulatory framework places increased emphasis on the reliability and performance validation of critical subsea equipment, particularly blowout preventer systems.

The requirement for third-party verification and detailed material performance data is driving demand for coatings that can demonstrate consistent reliability under extreme operational conditions. Phosphate conversion coatings, particularly those designed for anti-galling and wear resistance, are well positioned to meet these requirements by enhancing the durability and functionality of critical components.

The regulatory shift toward real-time monitoring of equipment performance is also influencing maintenance strategies. Operators are increasingly focused on preventing mechanical failures such as seizing or sticking in subsea intervention systems, where failure can result in significant financial and environmental consequences. Phosphate-coated components that improve actuation reliability and reduce friction-related failures are becoming a preferred choice in both new installations and retrofit projects.

This evolving regulatory environment is expected to accelerate the adoption of advanced conversion coatings as operators seek to meet compliance requirements while minimizing operational risk.

Market Opportunity: China Hazardous Chemicals Safety Law Accelerating Adoption of Phosphate Coatings for Safety-Critical Equipment

China’s enforcement of the Hazardous Chemicals Safety Law is creating a substantial opportunity for phosphate conversion coatings in the oil and gas and chemical processing sectors. The regulation mandates comprehensive safety assessments for equipment handling hazardous substances, with a strong focus on operational reliability and lifecycle performance.

Under the new framework, enterprises are required to conduct safety evaluations at regular intervals, increasing scrutiny on the materials and coatings used in valves, pressure vessels, and pipeline systems. Phosphate conversion coatings are gaining importance as they enhance wear resistance, reduce friction, and improve the fail-safe performance of mechanical components operating under high stress.

The introduction of lifecycle tracking systems further reinforces the need for durable and verifiable coating solutions. Equipment coated with high-performance phosphate systems can leverage documented durability and performance data to streamline compliance with regulatory requirements and facilitate faster approval within national safety registries.

The scale of industrial activity in China, combined with stricter enforcement of safety standards, is driving increased demand for advanced phosphate coatings across both onshore and offshore applications. Manufacturers capable of delivering high-reliability, compliance-ready coating solutions are well positioned to benefit from this regulatory-driven market expansion.

Phosphate Conversion Coatings Market Share and Segmentation Insights

Upstream Segment Captures 48.7% Share Driven by Drill Pipe Protection and Sour Service Requirements

The phosphate conversion coatings for oil and gas market by sector is led by the upstream segment, accounting for 48.7% of market share in 2025, primarily due to intensive drilling and exploration activities. In upstream operations, manganese and zinc phosphate coatings are extensively applied to drill pipes, tool joints, casing, and downhole tools, where they provide critical lubricity, wear resistance, and corrosion protection under high torque and pressure conditions. These coatings also play a vital role in H₂S sour service environments, acting as a protective base layer to mitigate sulfide stress cracking (SSC)—a major failure risk in sour gas wells. As global energy demand sustains exploration in both conventional and unconventional reserves, the upstream sector continues to drive strong demand for oilfield corrosion protection coatings and phosphate surface treatments, reinforcing its leadership in the oil and gas coatings market.

Onshore Segment Holds 52.5% Share Supported by Large-Scale Well Deployment and Economic Efficiency

In the phosphate conversion coatings market by environment, onshore operations dominate with a 52.5% market share in 2025, driven by the sheer volume of global oil and gas wells. Onshore wells—spanning conventional drilling, shale extraction, and unconventional resources—outnumber offshore installations by approximately 20:1, significantly increasing demand for phosphate coatings used on tubing, sucker rods, and downhole accessories. A key factor supporting this dominance is cost sensitivity, as onshore operators prioritize economical corrosion protection solutions. Compared to more expensive alternatives like nickel plating or electroless coatings, phosphate conversion coatings provide a cost-effective balance of performance and durability. With continued expansion of onshore exploration and production activities, especially in North America, the Middle East, and Asia-Pacific, this segment remains the primary driver of growth in the oilfield surface treatment and corrosion protection market.

Competitive Landscape of the Phosphate Conversion Coatings for Oil and Gas Market

Henkel Leads Oil & Gas Phosphate Coatings with Advanced BONDERITE® Technologies

Henkel AG & Co. KGaA dominates the phosphate conversion coatings market, with its BONDERITE® brand recognized as the industry benchmark for tri-cationic phosphate technologies. In 2026, the company reported strong financial performance with €20.5 billion in sales and robust margins in its Adhesive Technologies division. Henkel is advancing sustainable pre-treatment solutions, including nickel-free and low-temperature phosphating systems that reduce energy consumption by up to 30%. Its BONDERITE® M-PP coatings are widely used for oilfield tools, providing a strong base for advanced finishes like fusion-bonded epoxy. Additionally, its innovative 2-step Flex Process enables efficient phosphating of multi-metal assemblies, enhancing performance in offshore applications.

Nihon Parkerizing Expands High-Performance Phosphate Coatings for Mechanical Components

Nihon Parkerizing Co., Ltd. is a global leader in manganese phosphate coatings, particularly for high-friction oil and gas components. Its PALBOND® series is widely used in drill string components and threaded connectors, offering superior oil retention and anti-galling properties under extreme torque conditions. In 2026, the company expanded its presence in South Asia through automated manufacturing systems, supporting regional oil and gas growth. Its integration of plasma electrolytic oxidation (PEO) with phosphating enhances surface hardness for lightweight alloys, surpassing traditional anodizing methods. Nihon Parkerizing’s multiplex surface treatments further improve wear resistance and corrosion protection, strengthening its position in advanced industrial coatings.

PPG Strengthens Integrated Coating Systems with Advanced Zinc Phosphate Technologies

PPG Industries, Inc. is a key player in the oil and gas protective coatings market, offering integrated phosphate and paint systems for large-scale infrastructure. In 2026, the company reported strong growth in its protective coatings segment, driven by demand in hazardous environments. PPG specializes in micro-crystalline zinc phosphate coatings, which serve as a primary corrosion barrier for refinery assets and storage tanks. Its cross-industry innovation includes the development of PVC-free and BPA-NI compliant coatings, enhancing safety standards. With continuous R&D investment, PPG is optimizing application efficiency and coating performance, reinforcing its leadership in corrosion protection and asset integrity solutions.

Sherwin-Williams Enhances Asset Integrity with Phosphate-Based Coating Systems

The Sherwin-Williams Company is a dominant force in phosphate conversion coatings for oil and gas, focusing on long-term asset integrity and corrosion protection. In 2026, the company leveraged its “Success by Design” digital platform to deliver automated, code-compliant coating specifications for energy infrastructure. Its Pipeclad® and Macropoxy® systems utilize phosphate conversion layers to improve adhesion of heavy-duty epoxy coatings on pipelines and subsea structures. Sherwin-Williams reported strong growth in its Performance Coatings Group, driven by increasing maintenance and repair activities in aging infrastructure. Its global technical service network ensures compliance with ASTM and NACE standards, strengthening its reputation in high-performance coatings.

Chemetall Leads Eco-Friendly Phosphate Alternatives with Zirconium-Based Technologies

Chemetall, a BASF Group company, is a leader in eco-friendly phosphate conversion coatings, particularly in zirconium-based pre-treatment solutions. These advanced coatings offer comparable corrosion resistance to traditional phosphates while reducing sludge generation by up to 90%, significantly lowering environmental impact. In 2026, Chemetall expanded its production capabilities in India to meet growing demand in Asia-Pacific. Its Gardobond® product line features thin-film conversion technologies that reduce chemical usage and wastewater treatment costs. By integrating ChemCycling principles and circular economy practices, Chemetall is positioning itself as a key innovator in sustainable surface treatment technologies for the oil and gas industry.

United States: Shale Leadership and Ultra-High Purity Coating Innovation

The United States remains the global leader in phosphate conversion coatings for oil and gas, driven by advanced shale exploration and high-performance infrastructure requirements. Expansion of domestic manufacturing, including Parker Hannifin’s new facility (2025), is strengthening supply chains and reducing lead times for drilling operators.

Operational demands in regions like the Permian Basin are driving adoption of heavy zinc phosphate coatings (>7 g/m²) to combat corrosion and hydrogen embrittlement in structural steel and fasteners. Additionally, the integration of ultra-high purity (UHP) phosphating techniques, adapted from semiconductor processes, is enhancing protection for sensitive downhole sensor housings.

Efficiency improvements are also shaping the market, with manganese phosphate coatings being widely used in hydraulic fracturing pumps to reduce friction and extend service life by approximately 22%. Environmental compliance is accelerating the shift toward nickel-free and chrome-free sealers, while strategic stockpiling of pre-treated OCTG is helping mitigate supply chain volatility.

China: Offshore Expansion and Green Manufacturing Transition

China is rapidly scaling its phosphate coatings market, driven by deep-sea exploration, infrastructure expansion, and dual-carbon sustainability goals. Government mandates are encouraging the integration of phosphating lines with passive fire protection (PFP) systems for offshore platforms in the South China Sea.

Regulatory frameworks such as GB 30981.1-2025 are pushing manufacturers toward low-sludge zinc-calcium phosphate systems, reducing environmental impact and waste disposal costs. Investments in industrial hubs like Zhejiang are supporting automated manganese phosphating lines for high-pressure valves in cross-border gas pipelines.

Technological advancements include nanostructured phosphate coatings, improving adhesion for fluoropolymer topcoats in subsea assemblies. Additionally, China is integrating photocatalytic-ready coatings into storage infrastructure, combining corrosion protection with energy efficiency. These developments position China as a leader in high-volume, environmentally optimized phosphate coating technologies.

Germany: Sustainable Chemistry and Hydrogen Infrastructure Readiness

Germany leads Europe in phosphate coating innovation, focusing on sustainability, circular economy practices, and advanced industrial applications. Companies such as BASF have introduced eco-friendly phosphate coatings designed to minimize toxic runoff in offshore environments.

The country is also advancing hydrogen-ready infrastructure, with R&D efforts targeting conductive phosphate coatings that can withstand high-pressure hydrogen transport conditions. Industrial adoption of accelerator-free phosphating processes is reducing sludge generation by up to 40%, aligning with EU zero-pollution goals.

Infrastructure investments, including the Münster Waterborne Excellence Center, are accelerating the transition toward aqueous-based phosphating systems. Germany is also integrating digital traceability technologies into coatings, ensuring lifecycle monitoring of offshore assets for up to 25 years, reinforcing its leadership in sustainable and high-performance coatings.

India: Infrastructure Expansion and Domestic Manufacturing Growth

India is emerging as a high-growth market for phosphate conversion coatings, driven by regulatory reforms and large-scale infrastructure projects. The Petroleum and Natural Gas Rules (2025) have simplified exploration policies, triggering increased demand for localized coating services.

Major consolidation, including the JSW Paints–Akzo Nobel India deal, is strengthening domestic supply chains for industrial coatings. Infrastructure expansion, particularly in pipeline development exceeding 10,000 km, is driving demand for field-applied phosphating solutions for corrosion protection.

Government incentives under the PLI scheme are boosting domestic production of manganese phosphate materials, reducing import dependency. Growth in refining capacity, such as the HPCL Rajasthan project, is further increasing demand for phosphated pump components and valves, positioning India as a key emerging market.

Norway: Subsea Excellence and Decarbonized Coating Systems

Norway remains a global benchmark for subsea corrosion protection, driven by its leadership in offshore oil and gas and transition toward decarbonized production systems. Electrification of offshore platforms is increasing demand for non-conductive phosphate coatings to prevent galvanic corrosion in high-voltage environments.

Technological advancements include modified zinc phosphate coatings capable of maintaining adhesion at temperatures as low as -40°C, ensuring reliability in Arctic conditions. Projects such as Northern Lights CCS are driving the development of CO₂-resistant phosphate linings for injection wells.

Innovation is also evident in digital twin integration, with embedded microsensors enabling real-time corrosion monitoring. Norway’s strict environmental regulations have led to the adoption of closed-loop phosphating systems, ensuring zero discharge and reinforcing sustainability leadership.

Brazil: Deep-Water Exploration and Bio-Based Innovation

Brazil’s phosphate coatings market is driven by pre-salt deep-water exploration, requiring high-performance coatings for extreme conditions. Activity in fields such as Buzios is increasing demand for thick-film manganese phosphate coatings for drill string components.

The country is leveraging its bio-based economy, utilizing ethanol-based cleaning agents and carnauba wax-modified sealers to improve sustainability and performance in tropical environments. Cross-industry innovation from the automotive sector is enhancing coating adhesion and durability in oil and gas equipment.

Local content regulations are driving the development of domestic phosphating hubs, particularly in Rio de Janeiro, strengthening supply chain resilience. Additionally, Brazil’s position as a bio-chemical exporter is enabling the global supply of sustainable phosphate additives, reinforcing its role in green coating technologies.

Saudi Arabia: Localization Strategy and Extreme Environment Coatings

Saudi Arabia is rapidly advancing its phosphate coatings market through localization initiatives under the IKTVA program and large-scale infrastructure projects. The development of major gas fields, such as Jafurah, is driving demand for locally produced phosphating solutions.

Extreme environmental conditions are shaping innovation, with phosphate-ceramic hybrid coatings being deployed to withstand temperatures above 450°C in refinery operations. R&D efforts are also focusing on abrasion-resistant coatings with carbide reinforcement to mitigate sand erosion in pipelines.

The expansion of desalination infrastructure is creating demand for potable-water-grade phosphate linings, while mega-projects like NEOM are boosting demand for high-performance coatings in structural steel. Growth in logistics hubs is further increasing the need for long-term anti-corrosion coatings, reinforcing Saudi Arabia’s position as a strategic regional market.

Phosphate Conversion Coatings For Oil and Gas Market Report Scope

Phosphate Conversion Coatings For Oil and Gas Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$249.8 Million

|

|

Market Size (2032)

|

$335.4 Million

|

|

Market Growth Rate

|

4.3%

|

|

Segments

|

By Product (Zinc Phosphate, Manganese Phosphate, Iron Phosphate, Amorphous and Hybrid Phosphates), By Sector (Upstream, Midstream, Downstream), By Substrate Material (Carbon Steel, Low-Alloy Steel, Cast Iron, Stainless Steel and Specialty Alloys), By Application (OCTG, Threaded Components and Fasteners, Valves, Pumps, and Actuators, Wellhead and Christmas Tree Equipment, Downhole Tools and Completion Equipment, Subsea Hardware), By Application Method (Immersion, Spray Application, In-situ), By Environment (Onshore Operations, Offshore and Subsea Operations, HPHT)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG and Co. KGaA, PPG Industries, Inc., BASF SE, The Sherwin-Williams Company, Axalta Coating Systems Ltd., Nihon Parkerizing Co., Ltd., 3M Company, Hubbard-Hall Inc., DuBois Chemicals, Crest Chemicals, Keystone Corporation, Freiborne Industries, Inc., Argosy Control Engineering Ltd., Westchem Technologies Inc., SurTec International GmbH

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Phosphate Conversion Coatings For Oil and Gas Market Segmentation

By Product

- Zinc Phosphate

- Manganese Phosphate

- Iron Phosphate

- Amorphous and Hybrid Phosphates

By Sector

- Upstream

- Midstream

- Downstream

By Substrate Material

- Carbon Steel

- Low-Alloy Steel

- Cast Iron

- Stainless Steel and Specialty Alloys

By Application

- OCTG

- Threaded Components and Fasteners

- Valves, Pumps, and Actuators

- Wellhead and Christmas Tree Equipment

- Downhole Tools and Completion Equipment

- Subsea Hardware

By Application Method

- Immersion

- Spray Application

- In-situ

By Environment

- Onshore Operations

- Offshore and Subsea Operations

- HPHT

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Phosphate Conversion Coatings For Oil and Gas Industry

- Henkel AG & Co. KGaA

- PPG Industries, Inc.

- BASF SE

- The Sherwin-Williams Company

- Axalta Coating Systems Ltd.

- Nihon Parkerizing Co., Ltd.

- 3M Company

- Hubbard-Hall Inc.

- DuBois Chemicals

- Crest Chemicals

- Keystone Corporation

- Freiborne Industries

- Argosy Control Engineering Ltd.

- Westchem Technologies Inc.

- SurTec International GmbH

*- List not Exhaustive