Phosphorus and Derivatives Market Size 2025–2034: $82.5 Billion to $113.4 Billion at 3.6% CAGR Driven by Fertilizer Expansion, Circular Phosphorus Recovery, and Specialty Derivative Growth

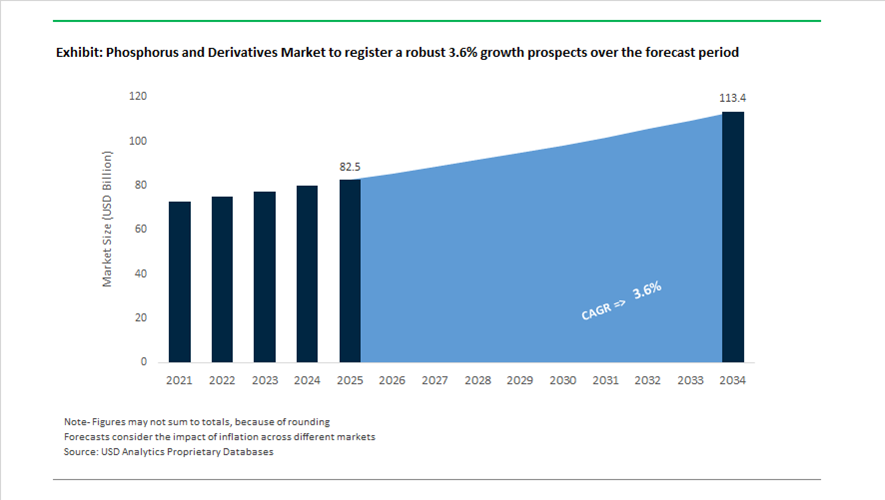

The global phosphorus and derivatives market is projected to grow from $82.5 billion in 2025 to $113.4 billion by 2034, registering a CAGR of 3.6%. The market encompasses phosphate fertilizers, phosphoric acid, yellow phosphorus (P4), phosphorus pentoxide, flame retardants, surfactants, specialty phosphates, and industrial phosphorus intermediates used across agriculture, electronics, lubricants, and advanced materials. Growth is underpinned by rising global food demand, supply security strategies in key importing nations, and structural expansion of high-margin specialty phosphorus derivatives beyond traditional fertilizer applications.

Large-scale fertilizer capacity expansion is reinforcing Middle Eastern dominance in global phosphate exports. In January 2025, the Saudi Arabian Mining Company awarded $922 million in construction contracts for its “Phosphate 3” project at Ras Al Khair and Wa’ad Al Shamal, targeting an additional 3 million tonnes per annum of phosphate fertilizer capacity. This expansion strengthens Saudi Arabia’s position as a global phosphorus supplier and supports downstream phosphoric acid and derivative manufacturing. In August 2025, Ma’aden secured a five-year agreement to supply 3.1 million metric tons of phosphate products annually to major Indian fertilizer producers, establishing a long-term export corridor aligned with India’s food security objectives. Similarly, in January 2025, Paradeep Phosphates Ltd. signed a ₹4,000 crore investment agreement with the Government of Odisha to expand phosphatic product manufacturing and port infrastructure, reinforcing India’s domestic production capabilities.

Trade enforcement and geopolitical shifts reshaped North American phosphorus markets in 2024 and 2025. Following administrative reviews in late 2024, the U.S. Department of Commerce finalized countervailing duties on phosphate fertilizers from Morocco and Russia. By 2025, the U.S. International Trade Commission reaffirmed these measures, prompting buyers to diversify sourcing toward domestic producers and alternative exporters such as Jordan and Saudi Arabia. This regulatory stance altered import flows and reinforced price discipline within the U.S. phosphate fertilizer and derivative market.

Circular economy initiatives and sustainability commitments are becoming strategic differentiators in the global phosphorus value chain. In 2025, Italmatch Chemicals advanced its role in the EU-funded FlashPhos project, reporting significant progress in recovering high-quality white phosphorus from sewage sludge. This innovation addresses Europe’s dependence on imported phosphate rock, classified as a critical raw material. In parallel, ICL Group expanded its circular fertilizer strategy through Puraloop®, a recycled phosphorus-based fertilizer launched in 2024, and in May 2025 acquired Lavie Bio to integrate biological solutions that enhance phosphorus uptake efficiency in soil. These initiatives reflect a broader transition toward sustainable phosphorus management and nutrient optimization.

China’s yellow phosphorus sector underwent structural rationalization through 2025. Facing environmental constraints and oversupply, authorities accelerated permanent closures of older, less-integrated facilities. By January 2026, industry reports indicated that these capacity reductions began stabilizing the global supply-demand balance for elemental phosphorus and its downstream derivatives. This rationalization supports more disciplined pricing for phosphorus trichloride, phosphoric acid, and flame-retardant intermediates used in electronics and polymer industries.

Specialty phosphorus derivatives are gaining momentum beyond fertilizers. In December 2025, Solvay launched an advanced portfolio of phosphorus-based chemicals targeting electronics, lubricant additives, and flame-retardant formulations. In September 2025, Arkema expanded its phosphorus intermediates offerings through global manufacturing partnerships to improve supply chain access across the Americas and Asia, particularly for surfactants and catalyst applications. Sustainability leadership is also influencing procurement decisions; in its 2024 sustainability report released in early 2025, OCP Group confirmed its pathway toward carbon neutrality by 2040 through renewable energy integration and green ammonia adoption at phosphorus processing sites.

Strategic Trends and High-Impact Opportunities in the Phosphorus and Derivatives Market

Strategic Decoupling and Regional Capacity Expansion to Safeguard Food Security

The phosphorus and derivatives market is undergoing a structural transformation driven by geopolitical risk, fertilizer price volatility, and food security imperatives. Governments and integrated producers are actively decoupling from globally concentrated phosphate rock supply chains by accelerating regional processing and derivative capacity expansion. The strategic focus has shifted from exporting raw phosphate rock to producing higher-value downstream derivatives such as di-ammonium phosphate (DAP), mono-ammonium phosphate (MAP), and purified phosphoric acid within domestic borders.

Brazil has emerged as a key example of this shift. The OECD Agricultural Policy Review released in October 2025 highlighted Brazil’s intensified push toward fertilizer self-sufficiency, with targeted investments in domestic phosphate beneficiation and conversion facilities. This policy direction mirrors India’s 2025 Union Budget allocation of approximately ₹3,850 crore for a one-time special DAP support package, aimed at stabilizing farm-gate prices and shielding the agricultural sector from global supply shocks. Together, these initiatives signal a move toward nationally anchored phosphorus value chains rather than reliance on a small group of exporting countries.

At the producer level, Morocco-based OCP Group is redefining scale and sustainability in the phosphorus derivatives market. Under its 2023–2027 investment plan, OCP is expanding plant nutrient capacity from 15 million tonnes in 2025 to 20 million tonnes by 2027. Importantly, this expansion is coupled with a decisive pivot toward high-value phosphorus derivatives for both agriculture and the energy transition, supported by a planned 5 GW clean energy platform. This positions OCP not only as a volume supplier but as a future-facing, low-carbon phosphorus integrator.

Parallel to industrial expansion, governments are also reshaping phosphorus demand patterns at the farm level. India’s National Mission on Natural Farming (NMNF), launched in late 2024 with a ₹2,481 crore allocation, seeks to reduce import dependency by promoting localized phosphorus cycling and bio-input systems. By targeting 10,000 Bio-input Resource Centres and aiming to transition nearly 1 crore farmers to ecosystem-based nutrient management by 2025–26, the program introduces a structural shift toward efficiency-driven phosphorus consumption rather than volume-led growth.

Regulatory-Driven Innovation in Lithium-Ion Battery Electrolyte Salts

Beyond agriculture, the phosphorus and derivatives market is being reshaped by electrification, with lithium-ion battery supply chains emerging as a strategic growth pillar. Lithium hexafluorophosphate (LiPF6), a phosphorus-derived electrolyte salt, has become a mission-critical material for EV batteries, forcing producers to invest in ultra-high-purity, environmentally controlled manufacturing processes.

In November 2025, Capchem announced technical upgrades through its Shilei Fluorine Materials subsidiary to raise LiPF6 capacity to 36,000 tonnes per year. This expansion is not purely volume-driven. New supply contracts signed for 2026 incorporate dynamic pricing clauses tied to raw material volatility, reflecting the increasing strategic importance and cost sensitivity of battery-grade phosphorus derivatives. Producers are moving toward closed-loop production models to control quality, emissions, and waste streams across the value chain.

North America is simultaneously accelerating reshoring efforts. In November 2025, Tinci Materials commenced construction of its first electrolyte manufacturing facility in the region. The plant is designed to comply with Inflation Reduction Act requirements, particularly Foreign Entity of Concern provisions, which mandate localized processing of phosphorus-based electrolyte salts to qualify for EV consumer tax credits. This regulatory framework is directly reshaping global investment flows within the phosphorus derivatives market.

Regulation is also influencing recycling economics. Effective August 1, 2025, China’s Ministry of Ecology and Environment implemented new standards governing recycled battery black mass, capping water-soluble fluoride levels from LiPF6 decomposition at 0.1%. These limits are forcing recyclers to invest in advanced hydrometallurgical recovery systems, elevating the technological and capital intensity of phosphorus salt recycling while improving environmental performance and asset longevity.

Semiconductor-Grade Phosphine and High-Purity Phosphorus Precursors

One of the highest-margin opportunities in the phosphorus and derivatives market is emerging from the semiconductor industry’s shift toward advanced architectures such as 3D IC packaging and gallium nitride power electronics. These technologies require ultra-high-purity phosphorus precursors, including electronic-grade phosphine, for vapor deposition, doping, and interconnect fabrication processes.

Industry data from December 2025 indicates that the global 3D semiconductor packaging market is on track to reach approximately $44 billion by 2025, driven by AI accelerators and 5G infrastructure. This directly expands demand for high-purity phosphine, which is critical for achieving the short interconnect lengths and high-density stacking required in chiplet-based designs. Even trace contamination in phosphorus precursors can lead to yield losses, making supply reliability and purity control decisive competitive factors.

Policy support is accelerating this opportunity. In March 2025, the U.S. streamlined CHIPS Act implementation under the newly formed Investment Accelerator office, which now oversees more than $100 billion in semiconductor-related projects. Among these are targeted incentives for domestic production of bottleneck materials, including electronic-grade phosphorus compounds, positioning local suppliers as strategic partners in sovereign semiconductor supply chains.

As generative AI workloads drive higher thermal densities in data centers, suppliers are also investing in ultra-clean phosphorus additives for organic substrates used in advanced packaging. These materials play a critical role in managing heat dissipation and signal integrity, elevating phosphorus derivatives from commodity chemicals to performance-critical enablers of next-generation computing infrastructure.

Organic Phosphorus Ligands for Sustainable Homogeneous Catalysis

A second high-value opportunity lies in fine chemicals and pharmaceuticals, where organic phosphorus ligands are becoming essential tools for sustainable catalysis. Under increasing regulatory pressure to reduce solvent use, waste generation, and reaction steps, pharmaceutical manufacturers are adopting advanced phosphine and phosphite ligands that enable high selectivity and atom-efficient transformations.

In March 2025, the ACS Green Chemistry Institute issued targeted research grants focused on sustainable catalysis, with organic phosphorus ligands identified as a priority area. These ligands are being designed to replace traditional, synthesis-intensive systems used in cross-coupling and carbon–heteroatom bond formation, aligning pharmaceutical process development with ESG objectives.

Recent pharmaceutical process reviews published in mid-2025 highlight that optimized phosphorus ligand systems can reduce E-factor waste by up to 40% in key API synthesis routes. This not only lowers environmental impact but also shortens production timelines and improves cost efficiency, making ligand innovation a strategic lever rather than a purely academic exercise.

The transition toward earth-abundant metal catalysis further amplifies this opportunity. As manufacturers replace palladium with iron or copper to reduce cost and supply risk, new generations of tailored phosphorus ligands are required to maintain reaction selectivity and yield. This creates a durable growth pathway for chemical companies capable of precision organic phosphorus synthesis, particularly those serving regulated pharmaceutical and fine chemical markets.

Phosphorus and Derivatives Market Share and Segmentation Insights

Phosphoric Acid Leads Phosphorus Derivatives Market as the Core Intermediate for Phosphate Production

Phosphoric acid accounted for 42.80% of the Phosphorus and Derivatives Market by derivative type in 2025, reflecting its central role as the primary intermediate in the global phosphorus value chain. This compound is used to produce fertilizers, industrial phosphates, food-grade phosphates, and specialty phosphorus chemicals that support agricultural, industrial, and consumer product applications. Global phosphoric acid production exceeds 60 million tons annually, making it the foundational product in phosphorus chemistry. In 2025, producers are focusing on wet-process phosphoric acid purification technologies, enabling removal of impurities such as cadmium, uranium, and heavy metals, allowing purified wet-process acid to replace thermal-process acid in several industrial and food processing applications.

Agrochemicals and Fertilizers Drive Phosphorus Derivative Consumption in Global Agriculture

Agrochemicals and fertilizers represented 68.40% of the Phosphorus and Derivatives Market by application in 2025, making agriculture the dominant consumer of phosphorus chemicals. Phosphorus is an essential nutrient required for plant growth, and phosphate fertilizers are critical for maintaining soil fertility and crop productivity across global agricultural systems. Major fertilizer products including monoammonium phosphate and diammonium phosphate continue to support large-scale food production. In 2025, the industry is increasingly focused on improving phosphate use efficiency through enhanced fertilizer technologies, including controlled-release fertilizers and precision nutrient application methods that optimize crop uptake while reducing environmental impacts associated with phosphate runoff.

Phosphorus and Derivatives Market Competitive Landscape

The global phosphorus and derivatives market is undergoing structural transformation toward high-purity technical-grade products for electronics, EV batteries, and pharmaceuticals. Competitive dynamics are defined by vertical integration, specialty chemical diversification, and the creation of dedicated business units targeting high-margin phosphorus derivatives.

ICL Group Refocuses on High-Purity Phosphorus Derivatives and Specialty Chemical Integration

ICL Group (Israel Chemicals Ltd.) operates as a vertically integrated specialty minerals producer with strong positioning in purified phosphoric acid (PPA) and high-value phosphorus derivatives. The company reported $7.15 billion in revenue for 2025, reflecting 5% year-on-year growth driven by its Phosphate Solutions segment. A strategic shift in early 2026 includes exiting non-core LFP cathode material expansion and prioritizing high-purity food-grade and technical phosphorus intermediates. The acquisition of Bartek Ingredients strengthens its presence in specialty additives and enhances integration with phosphate-based chemical offerings. Regional production strategies are being emphasized to reduce supply chain volatility and improve resilience. Core capabilities include backward integration and development of water-soluble phosphorus derivatives for precision agriculture and industrial cleaning.

OCP Group Establishes Dedicated Specialty Phosphorus Platform with Green Chemistry Integration

OCP Group is restructuring its operations to expand into high-value phosphorus derivatives beyond commodity fertilizers. The formation of OCP Specialty Products & Solutions S.A. (OCP SPS S.A.) centralizes activities targeting electronics, energy storage, and pharmaceutical applications. Production capacity for Purified Wet Process (PWP) phosphoric acid at Jorf Lasfar, through EMAPHOS, is being expanded to 280,000 tonnes of P2O5 annually to meet demand for technical-grade reagents. A 2026 collaboration with the International Atomic Energy Agency (IAEA) applies nuclear and isotopic techniques to optimize phosphorus utilization efficiency. Green phosphate production integrates renewable energy and desalinated water, aligning with low-carbon requirements in the EU market. Resource scale and downstream specialization support expansion into advanced phosphorus chemistry segments.

Nutrien Evaluates Strategic Repositioning of Phosphate Segment Amid Strengthening Market Conditions

Nutrien Ltd. remains the largest integrated crop input provider with significant phosphoric acid and phosphate derivative production capacity. The company initiated a strategic review of its phosphate business in late 2025, assessing restructuring, partnerships, or selective divestitures to improve long-term returns. Phosphate sales volumes are projected between 2.4 and 2.6 million tonnes in 2026, supported by stronger North American demand and improved pricing. Capital expenditure of approximately $2.0 billion is allocated toward mine automation and brownfield expansions across nitrogen and phosphate operations. Market conditions improved in early 2026 due to Chinese export restrictions and elevated input costs, supporting better margins for technical-grade derivatives. Operational scale and capital allocation continue to support phosphate production and downstream optimization.

Mosaic Expands Phosphate Processing Capacity and Advances Biological Integration Technologies

The Mosaic Company is strengthening its position in phosphorus derivatives through capacity expansion and process innovation. The proposed expansion of the New Wales facility in Florida targets up to 3 million tons of processed phosphate capacity, representing a significant increase in North American production. The company reported $541 million in net income and $2.4 billion in adjusted EBITDA for 2025 despite fluctuations in global shipment volumes. Mosaic Biosciences integrates biological catalysts with phosphorus derivatives to enhance nutrient-use efficiency and reduce environmental leaching. Operational adjustments in early 2026 included idling SSP production in Brazil to manage sulfur cost pressures and inventory levels. Production strategy focuses on high-efficiency phosphate processing and value-added derivative applications.

LANXESS Focuses on High-Performance Phosphorus Additives for Electronics and EV Applications

LANXESS AG specializes in high-performance phosphorus derivatives used in flame retardants and polymer additives for advanced industrial applications. The Levagard® 2100 product, introduced at K 2025, is a reactive phosphorus-based flame retardant that bonds chemically to polymer matrices, eliminating migration and reducing VOC emissions. The Emerald Innovation® NH 500 series targets glass-fiber reinforced plastics used in EV battery housings and electrical components. Full backward integration into phosphorus-based intermediates produced in Germany provides supply stability and insulation from global elemental phosphorus price volatility. The transition of Mesamoll® plasticizers to Scopeblue versions incorporates circular raw materials and reduces product carbon footprint by 20%. Product development emphasizes halogen-free phosphorus chemistry and high-performance material applications.

Saudi Arabia – Scale-Led Expansion Anchored in Integrated Phosphate Security

Saudi Arabia has consolidated its position as a structurally advantaged phosphorus and derivatives hub by combining scale expansion, upstream integration, and logistics efficiency. The Phosphate 3 mega-project, formally advanced in January 2025 with construction contracts worth USD 922 million, is designed to add 3 million tonnes per annum of new capacity, materially strengthening Ma’aden’s role in global phosphate rock and derivative supply. This expansion is strategically reinforced by the Kingdom’s July 2025 five-year supply agreement with India, under which 3.1 million tonnes of phosphate fertilizers will be delivered annually through 2030, effectively embedding Saudi Arabia into South Asia’s long-term food security framework.

Operational consolidation has further enhanced cost and execution discipline. The full acquisition of Mosaic’s stake in the Wa’ad Al Shamal Phosphate Company has unified upstream mining and downstream processing under a single operational umbrella, reducing coordination friction across the value chain. Export competitiveness is evident in October 2025 transactions of DAP at USD 728 per tonne CFR, enabled by low-cost energy inputs and optimized logistics. Looking ahead, Ma’aden’s confirmation during LME Week 2025 of AI-driven mine design and a tripling of exploration programs signals a data-led approach to extending reserve life and accelerating phosphate rock extraction in the Northern Borders region.

China – Policy-Driven Consolidation and High-End Phosphorus Reorientation

China’s phosphorus and derivatives industry is undergoing a state-directed transformation focused on energy efficiency, environmental compliance, and high-end application alignment. The MIIT’s April 2025 modernization mandate sets aggressive targets to cut energy use by 15 million tons and carbon emissions by 36 million tons over five years, forcing producers to re-engineer legacy phosphorus operations. Parallel growth directives under the 2025–2026 stabilization plan require more than 5% annual expansion in chemical sector value added, with explicit prioritization of electronic-grade phosphorus chemicals for semiconductor manufacturing.

Structural tightening is accelerating industry concentration. New regulations prohibit yellow phosphorus plants without integrated phosphogypsum recycling, institutionalizing closed-loop “resources-to-solid-waste” models. At the same time, demand-side pressure from the EV sector is reshaping product economics. LFP battery installations reached 105.2 GWh in Q1 2025, driving industrial-grade phosphoric acid prices to around 7,800 yuan per ton by mid-year. Capacity rationalization plans targeting the removal of roughly 30% of backward production by 2027 are expected to further strengthen the dominance of state-backed groups such as Yuntianhua and Xingfa, reshaping competitive dynamics in both domestic and export markets.

Morocco – Green Capital Deployment and Specialty Phosphate Upscaling

Morocco’s phosphorus and derivatives strategy is increasingly defined by capital-intensive decarbonization and downstream specialization. OCP Group reported USD 5.45 billion in revenues for the first half of 2025, reflecting strong export momentum in high-value phosphate rock and specialty fertilizers. This cash flow strength is being reinvested through a USD 13 billion green transformation program, supported by new financing secured in 2025 from European export credit and development agencies. The objective is full reliance on clean energy by 2027, positioning Moroccan phosphates as low-carbon inputs for global agriculture and industry.

Downstream portfolio sophistication is also advancing. Through its Specialty Products and Solutions unit, OCP increased its stake in Spain-based GlobalFeed in early 2025, expanding its footprint in phosphate-based animal nutrition additives. Capital market confidence remains strong, underscored by a USD 1.75 billion bond issuance in April 2025 to fund the 2030 investment roadmap. A core pillar of this roadmap is large-scale green ammonia production, which will progressively decouple phosphorus derivative manufacturing from fossil-based hydrogen and reinforce Morocco’s role as a sustainable phosphorus supplier.

India – Demand Stabilization and Domestic Derivative Industrialization

India’s phosphorus and derivatives landscape in 2025 is shaped by demand-side stabilization and accelerated localization of downstream manufacturing. In response to global fertilizer price volatility, the government increased DAP subsidies by 7% to INR 29,805 per tonne, maintaining a capped retail price of INR 27,000 per tonne. This buffer mechanism has insulated farmers while ensuring steady offtake of phosphorus-based inputs across the agricultural sector.

On the supply side, the Production Linked Incentive Scheme update for 2025–2026 has catalyzed over INR 1.76 lakh crore in manufacturing investments, with targeted provisions for key starting materials in phosphorus-based agrochemicals. Structural support is being reinforced through the rollout of nine plastic and chemical parks as of December 2025. These integrated hubs are designed to co-locate feedstocks, utilities, and logistics for downstream phosphorus derivatives such as flame retardants, plasticizers, and specialty intermediates, strengthening India’s position as a regional processing and consumption center rather than a purely import-reliant market.

Canada – Portfolio Rationalization Amid North American Supply Security

Canada’s phosphorus and derivatives industry is at an inflection point, balancing operational strength with strategic reassessment. In November 2025, Nutrien initiated a strategic alternatives review of its phosphate business, reflecting a potential reallocation of capital toward higher-margin nitrogen and potash segments. Despite this review, operational performance remains robust, with 2025 phosphate sales volumes projected between 2.35 and 2.55 million metric tons, supported by higher production of purified phosphoric acid for industrial and technical applications.

Geopolitical and trade considerations are influencing forward strategy. Chinese export restrictions have elevated the importance of North American supply security, prompting Canadian producers to reassess asset configuration and long-term capacity commitments. Decisions expected in early 2026 will likely determine whether Canada maintains a fully integrated phosphate value chain or pivots toward selective downstream specialization aligned with regional industrial demand.

Comparative Overview – Phosphorus and Derivatives by Country

Phosphorus and Derivatives Market County Level Snapshot

|

Country

|

Strategic Emphasis

|

Core 2025–2026 Driver

|

Structural Position

|

|

Saudi Arabia

|

Mega-scale expansion and integration

|

Long-term fertilizer supply contracts

|

Energy-advantaged global exporter

|

|

China

|

Policy-led consolidation and upgrading

|

EV batteries and semiconductors

|

Concentrated, state-backed producers

|

|

Morocco

|

Decarbonization and specialty derivatives

|

Green financing and export growth

|

Low-carbon global supplier

|

|

India

|

Demand stabilization and localization

|

Subsidies and PLI-driven manufacturing

|

High-growth consumption and processing hub

|

|

Canada

|

Portfolio optimization

|

North American supply security

|

Selective industrial supplier

|

Phosphorus and Derivatives Market Report Scope

Phosphorus and Derivatives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$82.5 Billion

|

|

Market Size (2034)

|

$113.4 Billion

|

|

Market Growth Rate

|

3.6%

|

|

Segments

|

By Derivative Type (Phosphoric Acid, Ammonium Phosphates, Industrial Phosphates, Phosphorus Precursors, Phosphorus Specialties), By Application (Agrochemicals & Fertilizers, Energy Storage, Electronics & Semiconductors, Food & Beverages, Water Treatment, Industrial & Specialty Applications)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

OCP Group, Saudi Arabian Mining Company, The Mosaic Company, Nutrien Ltd., Sinopec, Yuntianhua Group, Hubei Xingfa Chemicals Group, Israel Chemicals Ltd., Yara International ASA, EuroChem Group AG, PhosAgro, Jordan Phosphate Mines Company, UPL Limited, Solvay SA, Lanxess AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Phosphorus and Derivatives Market Segmentation

By Derivative Type

- Phosphoric Acid

- Ammonium Phosphates

- Industrial Phosphates

- Phosphorus Precursors

- Phosphorus Specialties

By Application

- Agrochemicals & Fertilizers

- Energy Storage

- Electronics & Semiconductors

- Food & Beverages

- Water Treatment

- Industrial & Specialty Applications

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Phosphorus and Derivatives Industry

- OCP Group

- Saudi Arabian Mining Company

- The Mosaic Company

- Nutrien Ltd.

- Sinopec

- Yuntianhua Group

- Hubei Xingfa Chemicals Group

- Israel Chemicals Ltd.

- Yara International ASA

- EuroChem Group AG

- PhosAgro

- Jordan Phosphate Mines Company

- UPL Limited

- Solvay SA

- Lanxess AG

*- List not Exhaustive