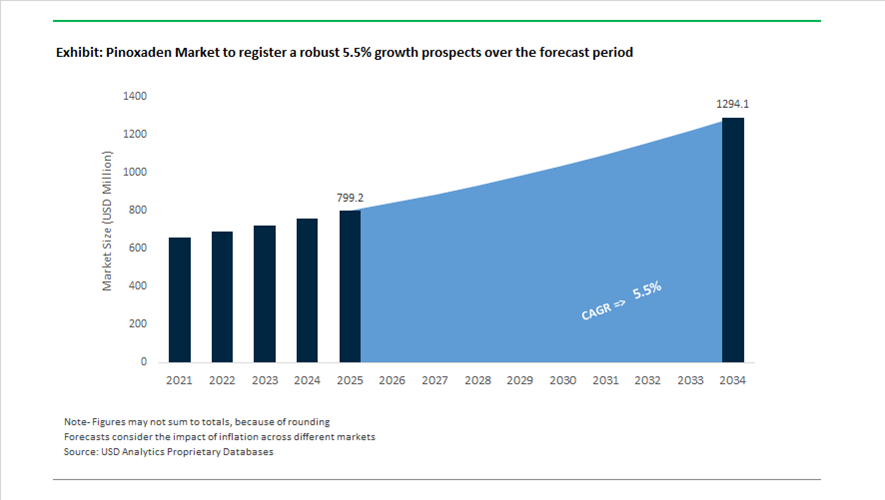

Pinoxaden Market Size 2025–2034: $799.2 Million to $1,294 Million at 5.5% CAGR Driven by Resistance Management and Smart Application Technologies

The global pinoxaden market is projected to grow from $799.2 million in 2025 to $1,294 million by 2034, registering a CAGR of 5.5%. Pinoxaden, a third-generation ACCase-inhibiting herbicide widely used in cereal crops, remains a critical tool for post-emergence grass weed control in wheat and barley. Market growth is primarily driven by escalating herbicide resistance in key weeds such as wild oats, ryegrass, and blackgrass, alongside increasing adoption of multi-mode-of-action formulations and precision agriculture technologies. As regulatory pressure tightens around older chemistries, pinoxaden-based solutions are being reformulated and integrated with complementary actives to extend efficacy and lifecycle value.

Resistance management is reshaping product innovation strategies. In November 2024, Syngenta Canada launched Axial Maxx, combining pinoxaden with fluroxypyr, bromoxynil, and bicyclopyrone to provide a multiple mode-of-action system for spring wheat and barley. Similarly, in May 2024, ADAMA introduced Edaptis in Poland, integrating pinoxaden with mesosulfuron-methyl to address resistant grass populations in European cereal systems. These combination products reflect a structural shift from single-active reliance toward diversified herbicide stacks designed to delay resistance evolution and improve spectrum control.

Generic competition and regional registrations are expanding global supply. In October 2024, Yifan Biotechnology secured Australian Pesticides and Veterinary Medicines Authority approval for Glaive 100 EC, containing 100 g/L pinoxaden with a cloquintocet-mexyl safener. This registration provides Australian grain growers with an alternative to branded formulations, intensifying price competition in mature markets. Meanwhile, Syngenta Australia promoted Axial Xtra in May 2024, emphasizing its built-in adjuvant system for improved rainfastness and weed uptake compared to standard 100 EC generics.

Corporate strategy and margin protection initiatives influenced 2025 dynamics. ADAMA reported in October 2025 that differentiated pinoxaden-based suspension concentrate formulations contributed materially to Q3 adjusted gross profit of $257 million, reflecting a pivot toward higher-value stabilized products. In early 2025, U.S. tariff adjustments on agrochemical actives prompted manufacturers to restructure portions of the pinoxaden supply chain into tariff-advantaged jurisdictions, mitigating cost pressures for North American wheat producers.

Technological advancement in herbicide classes is also emerging. In June 2025, Syngenta announced metproxybicyclone as the fourth generation ACCase inhibitor, marking the first major innovation since pinoxaden’s introduction in 2006. Although targeted initially at soybean and cotton markets, this development signals continued R&D investment in ACCase chemistry and may influence future positioning of pinoxaden within crop protection portfolios.

Precision agriculture and digitalization are enhancing application efficiency. In mid-2025, drone spraying trials in Hebei Province, China, demonstrated a 15% reduction in total herbicide volume per hectare using optimized pinoxaden blends while maintaining coverage uniformity. In January 2026, SAP and Syngenta announced a multi-year AI partnership to predict optimal application timing, reduce spray drift, and improve control of multi-resistant blackgrass in European cereal systems. Integration of AI-assisted decision tools is expected to strengthen stewardship compliance and maximize yield outcomes.

Trends and Opportunities in the Global Pinoxaden Market

Geographic Expansion and Localized Formulation Strategies Across Global Cereal Belts

The post-patent phase of the pinoxaden market has triggered an aggressive shift toward geographic expansion and formulation localization, particularly across high-growth cereal-producing regions such as India, Brazil, and parts of Eastern Europe. Rather than competing purely on price, manufacturers are differentiating through region-specific formulation engineering, balancing efficacy with local agronomic constraints such as water hardness, ambient temperature volatility, and spray-window compression driven by climate variability.

India has emerged as a focal point for volume-driven growth. In February 2025, the Government of India raised the Minimum Support Price for wheat by 6.6% to ₹2,425 per 100 kg, directly incentivizing yield-protection investments by farmers. This policy tailwind has accelerated the uptake of post-emergence grass herbicides, with pinoxaden retaining a strong agronomic position. Field trials conducted under the All India Coordinated Research Project on Wheat at JNKVV Jabalpur during 2024–2025 confirmed that pinoxaden applied at 45 g active ingredient per hectare consistently delivered superior control of grassy weeds and improved grain weight under sub-tropical growing conditions. These data points reinforce pinoxaden’s role as a yield-protection tool rather than a discretionary input.

In parallel, formulation innovation has become central to market competitiveness. Suspension Concentrate (SC) formulations have gained preference over traditional emulsifiable concentrates in 2024–2025 due to their reduced crystallization risk during storage and transport. This resilience is particularly valuable in North America and Central Asia, where rapid temperature swings and narrowing application windows have increased the penalty for formulation instability. As a result, SC-based pinoxaden products are increasingly positioned as “field-ready” solutions for large-acreage cereal producers operating under tighter operational constraints.

Integration into Multi-Mode-of-Action Resistance Management Programs

Rising resistance to ACCase inhibitors has structurally altered how pinoxaden is positioned within weed control programs. Rather than functioning as a standalone solution, pinoxaden is increasingly embedded within premium resistance-management frameworks that emphasize sequence, rotation, and complementary modes of action. This strategic repositioning is essential to extending the commercial lifespan of the molecule in key cereal markets.

In June 2025, CropLife Australia updated its resistance stewardship guidance, highlighting that repeated, exclusive use of Group 1 herbicides can result in resistant weed populations within three to four seasons. This guidance has accelerated adoption of sequential “double-knock” programs, where pinoxaden is deployed as a targeted post-emergence spray followed by a residual or alternative mode-of-action treatment to eliminate survivors. Such programs reduce selection pressure while preserving pinoxaden’s efficacy against key grass weeds.

At the commercial level, proprietary pre-mixes have gained traction as a convenience-driven response to resistance complexity. Marketed formulations combining pinoxaden with complementary active ingredients allow growers to broaden weed-spectrum control in a single pass, reducing operational time, fuel usage, and per-hectare environmental exposure. Products such as Syngenta’s Traxos and AxialXtreme exemplify this shift, positioning pinoxaden within an integrated agronomic solution rather than as a generic post-emergence herbicide.

Climate-Resilient Adjuvant and Safener System Development

One of the most underexploited value pools in the pinoxaden market lies in adjuvant and safener innovation. Pinoxaden’s dependence on the safener cloquintocet-mexyl creates a natural entry point for specialty formulation technologies that enhance crop safety and performance consistency under environmental stress. As drought frequency and heat stress increase, maintaining herbicide selectivity without yield penalty has become a priority for cereal growers.

Technical field data generated between 2021 and 2024 demonstrate that newer pinoxaden formulations incorporating built-in hard-water stability significantly reduce efficacy losses associated with calcium- and magnesium-rich spray solutions. By eliminating the need for additional water conditioners, these formulations simplify tank-mix preparation and reduce operational error risk, particularly during weather-driven spray delays.

Beyond stability, ongoing R&D into next-generation safener chemistries is targeting label expansion. There is a clear greenfield opportunity to enable pinoxaden use in more sensitive cereal cultivars and potentially adjacent crop segments where grass-weed pressure constrains yield but crop tolerance remains a limiting factor. Successful expansion would materially increase the addressable market while reinforcing pinoxaden’s position as a premium, crop-safe solution.

Precision Spot-Spraying and AI-Enabled Application Platforms

The integration of pinoxaden into AI-driven precision agriculture systems represents a structural inflection point for the market. Technologies such as computer-vision-enabled spot spraying are redefining herbicide economics by shifting from blanket application to plant-level targeting, fundamentally altering usage patterns and resistance dynamics.

During 2024–2025, John Deere’s See & Spray technology was deployed across more than one million acres globally. Operational data indicate an average reduction of nearly two-thirds in herbicide solution volume per acre by selectively targeting weeds rather than entire fields. For pinoxaden, this transition supports higher-value positioning, as reduced total volume offsets the use of more refined formulations while lowering selection pressure on weed populations.

Advanced dual-tank sprayer systems further enhance this opportunity. Platforms such as See & Spray Ultimate allow pinoxaden to be applied precisely to grass weeds while simultaneously broadcasting a different mode-of-action or fungicide. This “two-passes-in-one” capability improves operational efficiency and supports more sophisticated resistance strategies without increasing total chemical spend per hectare.

From a sustainability perspective, precision application is becoming a regulatory enabler. Smart spray control systems have demonstrated up to 93% reductions in chemical runoff and 87% reductions in airborne drift, aligning closely with EU Green Deal objectives and emerging global net-zero agriculture frameworks. These performance metrics position pinoxaden as a compatibility molecule for the next generation of low-impact, technology-enabled weed management systems.

Pinoxaden Market Share and Segmentation Insights

Emulsifiable Concentrate Formulations Lead Pinoxaden Herbicide Adoption in Cereal Crop Protection

Emulsifiable concentrates accounted for 42.80% of the Pinoxaden Market by formulation type in 2025, reflecting their widespread use in post-emergence grass weed control programs for cereal crops. These formulations provide excellent stability, efficient mixing with water, and uniform droplet distribution during spraying operations. Farmers prefer emulsifiable concentrate herbicide formulations because they enable rapid absorption by target grass weeds and deliver consistent field performance across wheat, barley, rye, and triticale production systems. In 2025, adjuvant compatibility optimization within emulsifiable concentrate herbicide formulations is improving rainfastness and leaf penetration efficiency, with integrated surfactant systems designed specifically for pinoxaden chemistry to enhance weed control performance under variable field conditions.

Post-Emergence Application Drives Pinoxaden Usage in Precision Weed Management Programs

Post-emergence application represented 72.80% of the Pinoxaden Market by application method in 2025, reflecting the herbicide’s design for controlling actively growing grass weeds after crop establishment. This approach allows growers to respond to real-time weed pressure rather than relying on pre-scheduled herbicide treatments. Pinoxaden is widely applied through foliar spraying systems that target grass weeds during their most susceptible growth stages in cereal cropping systems. In 2025, application timing optimization using digital agronomy tools and field monitoring systems is improving herbicide efficiency, enabling growers to apply pinoxaden at precise weed growth stages while reducing herbicide resistance risk and improving crop yield outcomes.

Pinoxaden Market Competitive Landscape

The global pinoxaden market is shaped by patent enforcement from innovators and rapid scale-up of generic technical producers. Competition centers on SC formulations, built-in adjuvant systems, regulatory compliance, and high-purity manufacturing for selective graminicides in wheat and barley across global cereal markets.

Syngenta Defends Axial® Franchise with Patent Enforcement and Next-Generation ACCase Innovation

Syngenta Crop Protection leads the pinoxaden market as the originator of the Axial® brand, focusing on lifecycle management and formulation protection. The February 2026 patent infringement action in China reinforces its strict defense of proprietary formulation technologies. A strategic R&D shift includes development of metproxybicyclone, a fourth-generation ACCase inhibitor targeting resistance management in key cereal markets. Advanced modeling tools are used to optimize tank-mix performance, improving selectivity and reducing surfactant load. The company integrates pinoxaden with digital agronomy platforms to provide real-time application guidance. Strategy emphasizes innovation defense, integrated weed management (IWM), and premium formulation performance.

ADAMA Expands Mid-Market Penetration with Built-In Adjuvant and SC-Based Pinoxaden Formulations

ADAMA Ltd. operates as the efficiency-driven arm of Syngenta, focusing on differentiated off-patent formulations. The launch of Bazzal (Pinoxaden 5.1% EC) in India targets Phalaris minor with rapid visible efficacy within 48 hours. Brazen All In™ technology integrates adjuvants directly into formulations, eliminating external surfactant requirements and improving application flexibility. The company is transitioning toward SC formulations across Southeast Asia and Europe to meet solvent regulations and improve rainfastness. Pricing strategy targets mid-tier cereal growers with innovator-grade performance at competitive cost levels. Portfolio development centers on formulation innovation and market accessibility.

Crystal Crop Protection Builds Integrated Pinoxaden Manufacturing with Large-Scale Capacity Expansion

Crystal Crop Protection Ltd. is expanding its presence through infrastructure investment and vertical integration in herbicide manufacturing. The February 2026 acquisition of 31.06 acres in Jhagadia supports development of a 50,000-tonne automated plant focused on pinoxaden-based products such as Topper. A ₹300 crore investment from IFC and EAF strengthens R&D capabilities and manufacturing automation for export-grade production. The launch of Saffire Crop Science introduces digital retail platforms targeting customized herbicide solutions in North India’s wheat belt. The company has completed nine acquisitions in five years, accelerating portfolio expansion and technical registrations. Strategy focuses on scale, integration, and direct farmer engagement.

Tagros Strengthens Global Supply of High-Purity Pinoxaden Technical with China-Plus-One Strategy

Tagros Chemicals India Pvt. Ltd. operates as a key global supplier of pinoxaden technical (minimum 98% purity) with strong regulatory compliance capabilities. Expansion under India’s Production Linked Incentive (PLI) scheme enhances capacity for high-purity manufacturing aligned with global demand. The company maintains ISO-certified, vertically integrated production with strict impurity profiling for EPA and EFSA regulatory submissions. Registration data expansion in Latin America and CIS markets supports global commercialization of generic pinoxaden. Product innovation includes oil-dispersion (OD) formulations improving herbicide uptake in resistant weed species. Strategy emphasizes technical-grade leadership, regulatory readiness, and export-driven growth.

Bhagiradha Advances Specialty Pinoxaden Formulations with AI-Driven Manufacturing and R&D Expansion

Bhagiradha Chemicals & Industries Ltd. is transitioning toward high-margin herbicides through process optimization and formulation innovation. The October 2025 revalidation request for technical manufacturing licenses supports scale-up at its Jhagadia facility. AI-driven process controls are being implemented to reduce cross-contamination in multi-product plants and ensure regulatory compliance for export markets. R&D efforts focus on polymeric thickeners and alcohol-based solvent systems to improve stability of pinoxaden EC formulations under high-temperature conditions. The company is increasing R&D spending by 15% to develop integrated pesticide-adjuvant solutions. Strategic direction emphasizes specialty formulation development and export-focused growth.

Luba Chemical Scales Cost-Competitive Pinoxaden Supply with Export-Focused Manufacturing Ecosystem

Weifang Luba Chemical Co., Ltd. operates as a major source manufacturer within the global pinoxaden supply chain. The company successfully completed 5-batch validation with India’s Central Insecticide Board in 2025, supporting its role as a preferred technical supplier. Operations in the Binhai Economic Development Zone provide cost advantages through shared infrastructure and optimized logistics. Export-only registration mechanisms enable production of customized high-concentration formulations tailored to international regulatory standards. Strong capabilities in triazolone and ACCase inhibitor intermediates support large-scale, cost-efficient manufacturing. Strategy focuses on export-driven production, pricing competitiveness, and global supply chain integration.

India – Yield Protection Economics Driving Domestic Pinoxaden Scale-Up

India’s Pinoxaden market in 2025 is being shaped by a clear yield-protection economics cycle anchored in government pricing policy. The 6.6% increase in the Minimum Support Price for wheat to ₹2,425 per 100 kg has materially raised the opportunity cost of yield loss, accelerating farmer adoption of premium post-emergence graminicides. With wheat output reaching approximately 113.3 million metric tons, Pinoxaden has emerged as a preferred solution for managing Phalaris minor, particularly in resistance-prone belts of the Indo-Gangetic plains. The regulatory environment has reinforced this shift, with a record 10 new agrochemical registrations in mid-2025, including advanced Pinoxaden-based pre-mixes engineered to delay resistance development and improve spectrum coverage.

On the supply side, India is transitioning from formulation dependence to integrated manufacturing. Agrochemical producers expanded domestic formulation capacity during 2025 under the Make in India framework, reducing reliance on imported technical grades. Government-backed residue studies confirming zero carryover impact on succeeding rice crops at application rates of 40 g per hectare have strengthened Pinoxaden’s positioning as a rotational-safe herbicide. Parallel investments in upstream chemical capacity are underway, with domestic producers scaling Sandmeyer reaction intermediates critical for the heterocyclic Pinoxaden core. This combination of agronomic validation and supply-chain localization is structurally embedding Pinoxaden into India’s cereal weed-management programs.

Brazil – Regulatory Velocity and Resistance Management Supporting Portfolio Expansion

Brazil represents one of the fastest-moving regulatory environments for Pinoxaden in 2025. The authorization of 725 new pesticide products in December 2025, including multiple Pinoxaden-based formulations, reflects a policy stance focused on portfolio diversification rather than chemical reduction alone. This regulatory momentum coincides with a record agricultural output of 350.2 million tons, which drove imports of 14,600 tonnes of ready-to-use herbicides between January and August 2025. Pinoxaden adoption is particularly strong in wheat and rotational cereal systems embedded within soybean–corn cycles, where grass-weed pressure has intensified.

Resistance dynamics are reinforcing this trend. The 2025 update from the Herbicide Resistance Action Committee explicitly prioritized ACCase inhibitors such as Pinoxaden for rotational use in glyphosate-resistant ryegrass zones. Despite the launch of the Pronara pesticide-reduction initiative, off-patent Pinoxaden registrations continue to rise due to its favorable resistance profile and compatibility with integrated weed management frameworks. Market consolidation is also reshaping distribution, with AgriConnection’s late-2025 acquisition of 96 pesticide registrations signaling tighter control over downstream market access and formulation branding.

United States – Precision Application and Label Optimization Enhancing Use Efficiency

In the United States, Pinoxaden adoption is increasingly defined by precision agriculture and formulation performance rather than expansion of treated acreage. In early 2025, large cereal producers integrated AI-enabled drone scouting with Pinoxaden spray programs, enabling site-specific applications that reduce chemical load while preserving efficacy against dense grass-weed patches. This precision alignment is particularly relevant in the Midwest wheat belt, where variable weather windows demand fast-acting, rainfast solutions.

Product innovation has reinforced this positioning. Syngenta updated labels for Axial-based Pinoxaden formulations in 2025, emphasizing a 30-minute rainfast window that directly addresses application risk during unstable spring conditions. Concurrently, land-grant university trials confirmed expanded tank-mix compatibility with broadleaf herbicides, allowing growers to deploy one-pass weed control programs that reduce operational costs. From a compliance standpoint, adherence to the 48-hour Restricted Entry Interval has become a focal point of EPA Worker Protection Standard audits, positioning Pinoxaden as a well-characterized and regulator-aligned option for large-scale cereal operations.

China – Technical Standardization and Export-Oriented Formulation Strategy

China’s Pinoxaden market remains selectively penetrated but strategically important. By 2025, approximately 20% of wheat growers had adopted Pinoxaden-based solutions, primarily in regions where older chemistries such as isoproturon have lost efficacy due to resistant weed biotypes. Policy emphasis has shifted toward manufacturing discipline, with the Ministry of Industry and Information Technology introducing new purity benchmarks for 97% technical Pinoxaden. These standards cap residual solvents such as toluene below 1 g per kg, directly supporting export compliance and international formulation partnerships.

Chinese producers are also repositioning Pinoxaden through formulation innovation. Suspension Concentrate formats now dominate output, accounting for over 47% of shipments in the 2024–2025 period, driven by stability, ease of handling, and distributor preference. R&D centers accelerated late-2025 trials combining Pinoxaden with biostimulants to mitigate crop stress during late post-emergence applications, signaling a gradual shift toward integrated crop-care packages. This export-oriented, formulation-led strategy is positioning China as a cost-competitive supplier rather than a purely domestic consumption market.

Comparative Snapshot – Pinoxaden Industry by Country

Pinoxaden Market County Level Snapshot

|

Country

|

Primary Adoption Driver

|

2025–2026 Strategic Focus

|

Market Positioning

|

|

India

|

MSP-linked yield protection

|

Localization and residue safety

|

Core cereal herbicide

|

|

Brazil

|

Regulatory approvals and resistance rotation

|

Portfolio expansion and consolidation

|

High-growth rotation market

|

|

United States

|

Precision agriculture efficiency

|

Label optimization and tank-mix flexibility

|

Performance-led usage

|

|

China

|

Technical purity and export compliance

|

SC formulation scaling

|

Cost-competitive supplier

|

Pinoxaden Market Report Scope

Pinoxaden Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$799.2 Million

|

|

Market Size (2034)

|

$1294 Million

|

|

Market Growth Rate

|

5.5%

|

|

Segments

|

By Formulation Type (Suspension Concentrates, Emulsifiable Concentrates, Combination Formulations, Granules & Wettable Powders), By Technical Purity (High-Purity Grades, Standard-Purity Grades), By Application Method (Post-Emergence Application, Foliar Spraying, Precision Spraying), By Crop Type (Wheat, Barley, Rye & Triticale)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Syngenta Group, BASF SE, Bayer AG, Corteva Agriscience, Adama Agricultural Solutions, Nufarm Limited, UPL Limited, FMC Corporation, Sumitomo Chemical Co. Ltd., Hebei Duoke Chemical Technology, Haihang Industry Co. Ltd., Agchem Access, Drexel Chemical Company, PI Industries

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Pinoxaden Market Segmentation

By Formulation Type

- Suspension Concentrates

- Emulsifiable Concentrates

- Combination Formulations

- Granules & Wettable Powders

By Technical Purity

- High-Purity Grades

- Standard-Purity Grades

By Application Method

- Post-Emergence Application

- Foliar Spraying

- Precision Spraying

By Crop Type

- Wheat

- Barley

- Rye & Triticale

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Pinoxaden Industry

- Syngenta Group

- BASF SE

- Bayer AG

- Corteva Agriscience

- Adama Agricultural Solutions

- Nufarm Limited

- UPL Limited

- FMC Corporation

- Sumitomo Chemical Co. Ltd.

- Hebei Duoke Chemical Technology

- Haihang Industry Co. Ltd.

- Agchem Access

- Drexel Chemical Company

- PI Industries

*- List not Exhaustive