Plant-Based Proteins for Pets Market Outlook– Ethical Nutrition and Sustainable Innovation

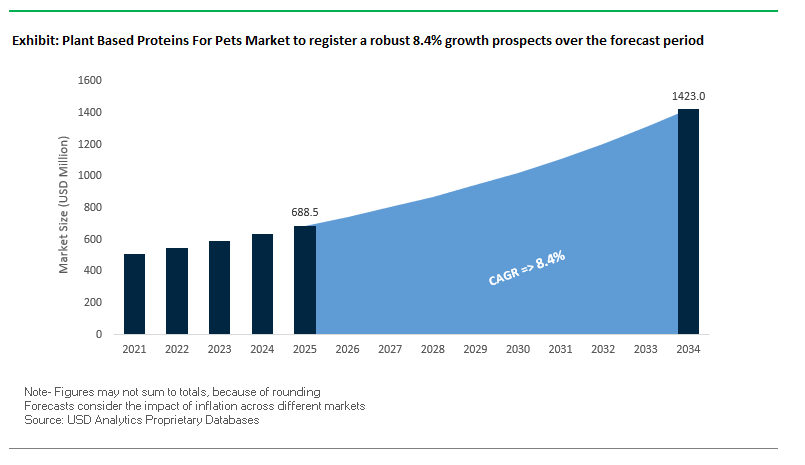

The global plant-based pet proteins market is projected to grow from USD 688.5 million in 2025 to USD 1,422.9 million in 2034 at a CAGR of 8.4%. Demand is fueled by shifting consumer values towards sustainable, ethical, and health-conscious pet food mimicking human food trends. Pet owners increasingly need clean-label, hypoallergenic, and sustainable options, with plant-based proteins a viable substitute for traditional meat-based pet food. In addition to aligning with pet humanization trends, these foods have genuine environmental benefits, reducing resource consumption and carbon emissions associated with animal protein production. Nutritional innovation via AI-powered formulation, cultured proteins, and precision fermentation is overcoming age-old issues of palatability and completeness. The European market is especially dynamic, with regulatory attitudes softening and consumer penetration speeding up.

Key Insights for Industry Professionals

- Pet Humanization Driving Demand – Owners seek plant-based diets that mirror their own health and ethical choices.

- Sustainability as a Core Differentiator – Lower carbon footprint and resource efficiency appeal to eco-conscious buyers.

- Health & Allergen Management – Plant-based formulas offer hypoallergenic alternatives for pets with protein sensitivities.

- Technology-Led Formulation – Precision fermentation and AI are improving nutrient profiles and palatability.

- European Momentum – Regulatory shifts, such as the British Veterinary Association’s acceptance of vegan dog diets, support growth.

Plant-Based Proteins for Pets Market Analysis – M&A Activity, Product Innovation, and Regional Growth

The plant-based pet proteins market is being prompted by new product development, cross-category innovation, and strategic buying. In January 2024, one of the startups founded by a former Impossible Foods executive, PawCo Foods, introduced "InstaBites," the first shelf-stable fresh plant-based dog food, and "LuxBites," a premium postbiotic- and fermented protein-based fresh food. Wild Earth launched its first nutritionally complete vegan cat food in August 2024 into the feline nutrition sector, one that has specific nutritional challenges.

The market is also consolidating. Colgate-Palmolive, through Hill's Pet Nutrition, acquired Australia's Prime100 in February 2025, which signals a market leader's foray into high-growth premium tiers. Archway Pet Food's 2025 acquisition of Bright Planet Pet complemented its climate-smart product line, reinforcing sustainability-driven brand positioning. Antos B.V. fortified its veggie dog treat line in Europe in 2024, and Benevo re-designed its plant-based cat food to include enhanced taurine supplementation, reflecting an industry-wide shift towards science-based nutritional assurance.

New technologies are also entering the scene. Bond Pet Foods successfully tested its precision-fermented protein in 2024, setting the stage for B2B incorporation into mass market pet food brands. Not necessarily plant-based, broader food-tech innovations like AR-based consumer engagement with Perfect Corp. demonstrate how much digital solutions can be used to bring next-generation pet nutrition products to consumers. Generally, the market is shifting from specialty novelty to mass market, driven by sustainability, functionality, and trust.

Trends and Opportunities in the Plant-Based Proteins for Pets Market

Precision-Fermented Taurine Unlocking True Feline Nutrition

One of the most groundbreaking trends in the plant-based pet proteins industry is using precision fermentation to produce bio-identical taurine for cats. Taurine is a critical amino acid for cats, and deficiency in the diet may result in severe health issues like dilated cardiomyopathy and retinal degeneration. While dogs can produce taurine from other amino acids, cats must obtain it directly from the diet traditionally from animal sources. Precision fermentation sidesteps this dependence by inserting specific DNA strands into microorganisms to produce taurine chemically equivalent to that of animal tissue. Studies, such as the collaboration between Bond Pet Foods and the University of Illinois, have demonstrated equal fermentation-based proteins improve digestion and gut microbiome health in pets. AI-optimized strain development now accelerates production cycles considerably, and bulk production is now economically feasible. Regulatory approvals within the EU, UK, Canada, and other regions further provide a clear path to commercialization, leading to taurine-fortified plant-based pet food that fulfills complete nutritional requirements for cats.

3D-Printed Custom Protein Blends Personalizing Pet Wellness

Integration of 3D printing technology into pet food production is making it possible to achieve unprecedented degrees of customization in plant-based pet food. By including data on breed, age, genetic predispositions, and medical history, manufacturers can formulate specific nutrients on a per-pet basis. The technology has clear benefits in the space of finicky consumers through tailored texture and shape, and through pets with medical conditions such as dysphagia through easy-to-eat softer food. 3D printing also facilitates sustainability objectives by allowing precise-portion production, minimizing food waste, and through the use of sustainable protein sources such as pea, lentil, and soy. Published research verifies the viability of using printable pastes and slurries from plant-based protein to produce customized, nutritionally complete meals. With consumer spending trending towards premiumization and "pet humanization," this capability to provide hyper-personalized, sustainable, and functional pet food positions 3D printing as a high-growth opportunity for innovative brands.

Veterinary-Prescribed Plant-Based Proteins for Clinical Nutrition

One of the largest untapped market segments is plant-based diets for veterinarian-prescribed chronic pet health diseases. Human nutrition science has established that plant-based, low-protein diets can manage chronic kidney disease (CKD), reduce acid load, and enhance gut microbiota. Applying these concepts to veterinary use may result in clinically validated pet foods for CKD, obesity, and cardiovascular disease. Studies indicate navy beans can reduce canine cholesterol, and green tea polyphenols enhance insulin sensitivity with established therapeutic benefit. Plant-based diets also minimize allergen exposure in pet animals with animal protein allergies such as beef and chicken. With proper formulation to provide complete amino acid profiles, veterinary-exclusive plant-based pet foods can be a high-margin, evidence-based segment of the total market.

Opportunity: Plant-Based, Insect-Free Aquafeed for the Pet Fish Segment

The plant-based, sustainable aquafeed market for pets is under pressure due to growing customer demand for non-traditional options for fishmeal that are not animal-derived. Plant-protein aquafeeds, which are formulated with soy, pea, canola, and fermented protein meals, yield high digestibility and nutritionally balanced diets without the use of marine-based material. Fermented proteins, in turn, yield higher nutrient assimilation and gut health benefits for aquatic animals. With twice the world's consumption of fish since 1970, the world needs sustainable feed solutions today. Government initiatives, such as India's launch of "Bio Guru 3F Pro" vegan aquafeed in 2023, are driving adoption by creating positive regulatory and consumer awareness climates. The shift presents plant-based protein manufacturers with the opportunity to enter the aquafeed market, targeting the fast-growing ornamental fish industry with insect-free, eco-friendly alternatives.

Plant-Based Proteins for Pets Market Share and Segmentation Insights

Pea Protein Leading with Superior Digestibility and Hypoallergenic Benefits

Pea protein products account for 38% of pet plant-based proteins, the highest and largest segment. Their popularity stems from their hypoallergenic nature, possibility of non-GMO sourcing, and applicability to the trend towards grain-free and gluten-free formulas. Soy proteins, at 25%, are the most cost-effective but are marred by allergen and sustainability issues, prompting brands to explore lentil, sunflower, and wheat proteins. Lentil protein is the fastest-growing source, valued for its complete amino acid profile and applicability in premium formulas. Sunflower and wheat proteins are specialty players now but are being used more and more in specialty diets and hybrid formulas. Presence of multi-source protein blends (e.g., pea-lentil blends) reflects a trend towards attaining amino acid completeness plus ingredient diversification for sustainability and product differentiation purposes.

.png)

Dry Food Dominating Due to Convenience and Shelf Stability

Dry food, 45% of plant-based pet protein market share, is propelled by demand for convenience, longer shelf life, and simplicity of storage. Plant-based proteins are being used on dry kibble as direct substitutes for animal protein meals, with palatability but with better environmental profiles. Wet food, 30%, is gaining share as consumers demand greater moisture content for hydration and gastrointestinal health. Freeze-dried formats represent a new premium segment, delivering raw-like nutrition with extended shelf stability, and functional treats and mixers used for joint health, dental health, and gut health are growing rapidly across mainstream and specialty channels. The trend toward full portfolio plant-based across staple diets to functional snacks demonstrates a maturity market where convenience, variety, and tailored functionality are equally significant purchase drivers.

Competitive Landscape – Leading Innovators in Plant-Based Pet Nutrition

Functional ingredients, sustainable proteins, and balanced formulations are plant-based pet food innovations aimed at improving pet health and sustainability. The named companies include The Every Company, Benevo, Wild Earth, The Honest Kitchen, V-Dog, Halo Pets, Yarrah Organic Pet Food, Wysong, Nature's Recipe, Evolution Diet, Vigor & Sage (Bridge PetCare), Yantai China Pet Foods Co., Ltd., Adimax, Mars Petcare, Nestlé Purina PetCare, Others.

Wild Earth, Inc. – Building the Plant-Based Frontiers

Wild Earth has established itself as a solid brand for veterinarian-developed, nutritionally balanced pet food. Sustainability and cruelty-free options remain its strategic priority, underpinned by intense R&D. Plant-based cat food in August 2024 is an example of category extension and demonstration of navigating species-specific requirements, placing the brand as a premium ethical nutrition innovator.

V-dog – Flourishing Vegan Pet Food Innovator

Established in 2005, V-dog is still one of the highest-regarded plant-based canine food brands. With kibble and treat options that address dogs with sensitivities, the company has loyal consumer bases and high-quality educational outreach to its advantage. Word-of-mouth and long-term consumer commitment allow the company to compete favorably without large amounts of advertisement expenditure.

Bond Pet Foods, Inc. – Precision Fermentation Industry Leader

Bond Pet Foods' proprietary fermentation technology produces cultured proteins genetically indistinguishable from animal meat, without animal agriculture. Its B2B business model supports integration into existing pet food brands, delivering impact at pace. Its 2024 pilot production demonstration demonstrates it can scale towards commercial.

Benevo – Leading Vegan Pet Food in Europe

UK-based Benevo pioneered vegan pet nutrition from 2005 onwards, and its products are available in over 30 countries. Its 2024 reformulation of its vegan cat food demonstrates dedication to nutritional science and continuous product enhancement. The established brand presence in the European vegan food market ensures market penetration and advocacy.

United States: Regulatory Flexibility, Fermentation Breakthroughs, and Sustainability-Led Demand

A flexible U.S. regulatory backdrop shaped by the FDA’s voluntary fortification policy and clear labeling expectations encourages rapid innovation in plant-based pet nutrition. Major pet food manufacturers are launching pea-protein dog treats and scaling purpose-built facilities (with expansions boosting capacity ~40%) to meet rising demand. Category momentum is reinforced by precision fermentation: U.S. innovators (e.g., animal-free egg proteins produced via fermentation for pet applications) are creating novel, consistent, and sustainable protein inputs.

Science-first marketing is gaining traction as veterinary positions evolve; the British Veterinary Association has eased objections to vegan dog diets, while peer-reviewed studies (e.g., at the University of Liverpool) assess health outcomes, supporting informed adoption. Formulators are also diversifying beyond soy with pea and sunflower proteins prized for digestibility and amino-acid balance aligning plant-based recipes with owner priorities around health, clean labels, and lower environmental impact.

Germany: By-Product Valorization, Cultivated Ferments, and Functionality-Driven R&D

Germany’s ecosystem blends deep research capability with sustainability. The Fraunhofer IVV advances recovery of proteins from oil press cake, spent grain, and other upcycled by-streams, cutting waste while widening the ingredient toolbox for plant-forward pet foods. Brands are commercializing fermentation-derived options e.g., a vegan, air-dried snack made from cultivated protein speaking to ethics-minded consumers. Policy and strategy work (e.g., Systemiq with GFI Europe) underline how investment in plant-based and fermentation proteins can strengthen the economy, hinting at streamlined pathways for novel foods.

German R&D doubles down on functionality and palatability: award-winning work on debittered lupin proteins improves taste and processing behavior. The result is a pipeline of high-quality, sensory-optimized plant proteins ready for extrusion, treats, toppers, and veterinary-guided formulations.

China: Scale Manufacturing, Smart Factories, and Globalized Pet-Protein Supply

China couples massive manufacturing capacity with a fast-growing domestic pet market. Leaders such as Bridge PetCare and Yantai China Pet Foods operate large, automated plants, turning out dry, wet, and treats lines for both local shelves and export markets. Capacity and quality systems enable rapid iteration on alternative-protein SKUs as pet ownership and spending rise.

Chinese champions also show global ambition with multi-country plant footprints and exports to 50+ markets positioning China as a hub for plant-based pet protein scale-up. Investment in state-of-the-art automation (e.g., factories producing hundreds of tons per hour) ensures supply resilience, consistent quality, and cost competitiveness as brands expand soy, pea, lentil, and emerging fermentation-based inputs.

India: Alternative-Protein Uptake, BIS-Anchored Trust, and D2C Acceleration

India’s pet nutrition is rapidly embracing alternative proteins from plant-based to insect-based driven by owner demand for eco-conscious and hypoallergenic choices. BIS standards anchor safety and quality, building trust as new formulations scale. Meanwhile, e-commerce and D2C routes let challenger brands educate consumers, personalize recommendations, and serve Tier-2/3 cities with efficient logistics.

With premiumization rising, local formulators tailor cost-effective plant proteins to Indian preferences, leveraging functional blends for digestibility and skin/coat health. The result is a high-growth, digitally enabled market where compliance, storytelling, and evidence-based benefits convert first-time buyers into loyal subscribers.

Brazil: Local Sourcing, Ingredient Innovation, and Capacity Expansion

Brazil’s pet sector is leaning into sustainable sourcing, favoring locally grown plant proteins and eco-friendly packaging (biodegradable/recyclable) to cut footprint and improve transparency. Formulation teams are widening beyond soy to pea and lentil proteins and superfood inclusions, aligning recipes with vegetarian and climate-aware owner values.

Industrial muscle is growing: Adimax’s $140M plant adds ~7,000 tons/month of capacity, reinforcing Brazil as a regional production powerhouse. With supply close to farms and ports, Brazil can scale affordable, plant-centric diets across dry, wet, and treats, supporting both domestic penetration and export growth.

Plant Based Proteins For Pets Market Report Scope

Plant Based Proteins For Pets Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$688.5 Million

|

|

Market Size (2034)

|

$1422.9 Million

|

|

Market Growth Rate

|

8.4%

|

|

Segments

|

By Pet Type (Dogs, Cats, Other Pets), By Protein Source (Soy-based, Pea Protein-based, Sunflower Protein-based, Wheat-based, Lentil-based), By Form (Dry Food (Kibble), Wet Food, Treats & Mixers, Freeze-Dried Food), By Application (General Health & Nutrition, Weight Management, Digestive Health, Allergy Management), By Distribution Channel (Store-based (Specialty Stores, Supermarkets), Online Retail, Veterinary Clinics)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Every Company, Benevo, Wild Earth, The Honest Kitchen, V-Dog, Halo Pets, Yarrah Organic Pet Food, Wysong, Nature's Recipe, Evolution Diet, Vigor & Sage (Bridge PetCare), Yantai China Pet Foods Co., Ltd., Adimax, Mars Petcare, Nestlé Purina PetCare, Others.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Plant Based Proteins For Pets Market Segmentation

By Pet Type

By Protein Source

- Soy-based

- Pea Protein-based

- Sunflower Protein-based

- Wheat-based

- Lentil-based

By Form

- Dry Food (Kibble)

- Wet Food

- Treats & Mixers

- Freeze-Dried Food

By Application

- General Health & Nutrition

- Weight Management

- Digestive Health

- Allergy Management

By Distribution Channel

- Store-based

- Specialty Stores

- Supermarkets

- Online Retail

- Veterinary Clinics

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Plant Based Proteins For Pets Market

- The Every Company

- Benevo

- Wild Earth

- The Honest Kitchen

- V-Dog

- Halo Pets

- Yarrah Organic Pet Food

- Wysong

- Nature's Recipe

- Evolution Diet

- Vigor & Sage (Bridge PetCare)

- Yantai China Pet Foods Co. Ltd.

- Adimax

- Mars Petcare

- Nestlé Purina PetCare

* List Not Exhaustive

Research Coverage

This report investigates the dynamic growth trajectory, emerging breakthroughs, and strategic advancements shaping the global plant-based proteins for pets market. With a focus on ethical nutrition, sustainability-led innovation, and science-backed product development, the report delivers in-depth analysis reviews, competitive benchmarking, and regulatory insights essential for decision-making. It highlights how shifting consumer preferences, technology-led formulation such as precision fermentation and AI integration, and veterinary-prescribed diets are redefining industry standards. From major M&A activity to transformative product innovations, this report by USDAnalytics is an essential resource for industry professionals seeking to capitalize on high-growth niches and global adoption trends. It also provides detailed regional analyses, company profiles, and segmentation insights, offering a complete strategic blueprint for stakeholders aiming to navigate this evolving market with confidence. Scope includes-

- Segmentation: By Pet Type (Dogs, Cats, Other Pets), By Protein Source (Soy-based, Pea Protein-based, Sunflower Protein-based, Wheat-based, Lentil-based), By Form (Dry Food, Wet Food, Treats & Mixers, Freeze-Dried Food), By Application (General Health & Nutrition, Weight Management, Digestive Health, Allergy Management), By Distribution Channel (Store-based, Online Retail, Veterinary Clinics).

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Historic Data & Forecast: Coverage from 2021 to 2024 (historic) and 2025 to 2034 (forecast).

- Companies: Profiles and strategic analysis of 15+ leading companies driving innovation in plant-based pet proteins.

Methodology

The research methodology combines primary and secondary approaches to ensure data accuracy, market relevance, and actionable insights. Primary research includes interviews with key stakeholders such as pet nutrition experts, veterinary professionals, sustainability advocates, and executives from leading manufacturers. Secondary research leverages reputable industry publications, regulatory databases, trade journals, and company filings. Quantitative data is validated through statistical modeling and cross-referenced with market trends, while qualitative insights are derived from case studies and real-world applications. The methodology ensures comprehensive coverage of market drivers, challenges, and opportunities, providing a reliable foundation for strategic planning and investment decisions.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.