Accelerating Growth in Polyethylene Terephthalate Market: Strong Valuation and Outlook

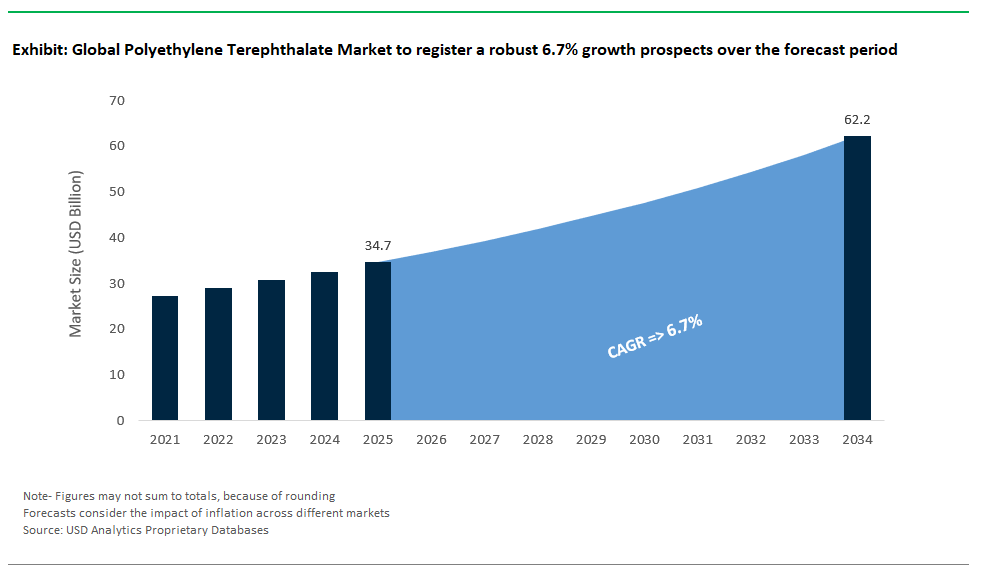

The global Polyethylene Terephthalate (PET) market is projected to grow to over $34.7 billion in 2025, and will achieve $62.2 billion by 2034, growing with a CAGR of 6.7% during the forecast period 2025-2034. This growth is fuelled by a surge in demand for light weight, durable, and fully recyclable plastics in packaging, textile as well as speciality engineering applications. PET’s status as the leading material for beverage bottles, food packaging and high-performance fibers reinforces its position as a bedrock of the changing plastics and circular economy landscape.

Polyethylene Terephthalate – the stalwart of the world plastics industry and celebrated for its versatility, cost-effectiveness and excellent barrier performance. PET is a thermoplastic polymer that provides a rigid package with excellent clarity and fast, easy conversion for shapes that perform well for today’s fast-paced packaging needs such as bottles, films, and containers. Outside of packaging, PET has seen widespread use in the textile and carpet fiber industry, as well as the engineering plastic market for electronic and automotive parts. The growing demand of recycled PET (rPET) and advances in both chemical and mechanical recycling highlight the relevance of PET in sustainability and circularity. Brands and government around the world are stepping up to increase recycled content while minimizing environmental impact, making PET an essential part of the effort for greener packaging and consumer goods.

Dynamic Developments and Strategic Advances Transforming the PET Market

The Polyethylene Terephthalate (PET) market is currently marked by sweeping innovation, global partnerships, and an intensified push for circularity. In July 2025, an agreement was reached between Indorama Ventures Public Company Limited (IVL) and a leading beverage brand to significantly increase rPET availability, facilitating the transition to sustainable PET packaging. Its competitor Alpek S.A.B. de C.V. also materialized in June 2025 with its plans to add 100,000 metric tons per year of North American rPET capacity, which it plans to bring online toward the end of 2026, to meet spiking demand from beverage and consumer industries.

Innovations in recycling technologies are changing the industry. (“SK geo centric”) announced that together with its global commercialization partner, Loop Industries, Inc. (“Loop Industries”) it has made substantial process in the construction of its Polyethylene Terephthalate (“PET”) depolymerization plant in Ulsan, South Korea, capable of recycling otherwise unrecyclable PET waste into virgin-quality PET resin for use in a variety of end-market applications. Also, Eastman Chemical Company said late April 2025 that several of the world's biggest brands have agreed to adopt PET from its leading-edge molecular recycling methods designed to produce high-quality resin from difficult-to-recycle plastics such as colored PET for use in new packaging. Announcement on The Coca-Cola system’s actions in March 2025 shine are a testament to an industry shift globally to 100% rPET bottles, with investments in collection, infrastructure and with recyclers to ensure bottle-to-bottle PET recycling at scale.

This momentum continued with Reliance Industries Limited (RIL) in January 2025 announced move to circular polyester solutions and further expansion of rPET in both fiber and packaging. Our internal sector-wise data also showed that demand for food-grade rPET is on a clear growth path, driven by EU regulatory requirements and brand sustainability commitments. Policy remains key to PE and PP recycling —At the same time, European plastics converters in November 2024 urged for strong frameworks for PET recycling infrastructure, notably for food-grade applications. It is also boosted by a string of new developments such as mono-material PET film for flexible packaging in September 2024 and Carbon Lite Recycling’s US rPET operations expansion in August 2024, all of which are designed to meet increasingly ambitious recycled content commitments.

Trends and Opportunities Reshaping the Polyethylene Terephthalate (PET) Industry

Surging Demand for Recycled PET (rPET) Accelerates Circular Economy

A defining trend in the PET market is the explosive global demand for recycled PET (rPET), reshaping the entire PET value chain and reinforcing sustainability as a core market driver. Regulatory frameworks, such as the European Union’s Single-Use Plastics Directive, are mandating minimum recycled content levels in PET packaging 27.8% by 2025 and 32.1% by 2034. Leading beverage and consumer brands have responded with voluntary pledges to integrate 50% or more rPET into their packaging portfolios. High-profile examples include Coca-Cola’s commitment to 100% rPET bottles in several European markets, and Alpek’s substantial capacity expansion to meet demand for food-grade rPET. Technological advances, such as Loop Industries’ and Eastman’s chemical recycling, are enabling previously non-recyclable PET streams colored bottles, multi-layer packaging, and even textiles to be converted into virgin-quality rPET, dramatically expanding feedstock availability. Investments from organizations like Closed Loop Partners are improving collection and sorting infrastructure, ensuring a reliable supply of high-quality recyclable PET. These developments are generating upward pricing pressure for rPET and incentivizing new business models across the plastics recycling value chain, fundamentally advancing the circular economy for PET packaging.

Expanding High-Performance PET Applications Beyond Traditional Packaging

Significant opportunities are emerging from the diversification and innovation of high-performance PET applications in sectors beyond packaging. PET’s inherent properties lightweight strength, chemical resistance, and thermal stability are spurring its adoption in advanced textiles, engineering plastics, and technical films. In the textile sector, polyester fibers (derived from PET) are increasingly favored for performance apparel, industrial fabrics, and home furnishings due to their durability and versatility. Technical textiles for automotive, geotextiles, and composites benefit from PET’s resilience and adaptability. The electronics and solar industries are embracing advanced PET films for their dimensional stability and optical clarity, while the automotive and consumer electronics sectors are specifying PET-based engineering plastics for demanding, weight-sensitive applications. Companies like Teijin are leading innovation in PET fiber for automotive and industrial use, while packaging converters are developing mono-material PET films to improve recyclability. The rise of rPET-based fibers and components is aligning these high-performance segments with sustainability goals, driving new growth avenues and reinforcing PET’s resilience against evolving market risks.

Competitive Landscape: Market Leaders and Innovators Powering the PET Industry

The global Polyethylene Terephthalate (PET) market features a competitive ecosystem led by multinational petrochemical giants and cutting-edge recycling specialists, each leveraging technology, integration, and sustainability to drive growth.

Indorama Ventures Strengthens Leadership in Global rPET Supply

Indorama Ventures Public Company Limited (IVL), headquartered in Thailand, is the world’s largest PET and rPET producer, offering unmatched vertical integration from PTA/MEG to finished PET products. IVL’s comprehensive product portfolio spans resins for bottles, films, and containers, and polyester fibers for textiles, complemented by aggressive investment in rPET production. The July 2025 strategic collaboration with a global beverage brand to scale rPET supply underscores IVL’s focus on circularity. Continuous global expansion particularly in rPET enables IVL to meet growing demand from major consumer brands and support the industry’s shift toward closed-loop packaging.

Alpek Expands rPET Capacity to Meet Sustainability Demands in the Americas

Alpek S.A.B. de C.V., based in Mexico, is a leading PET and polyester fiber producer with strong backward integration into raw materials, ensuring cost stability and secure supply. In June 2025, Alpek unveiled plans to expand rPET production by 100,000 metric tons per year in North America by Q4 2026, directly targeting the rising demand for sustainable packaging. Alpek’s comprehensive offering of high-quality PET resins, specialty fibers, and growing rPET capacity positions the company as a key partner for North American packaging and consumer goods sectors seeking circular solutions.

Reliance Industries Drives Circular Economy in Indian PET and Polyester Markets

Reliance Industries Limited (RIL), a diversified Indian conglomerate, is a global force in PET and polyester fiber production. With integrated operations from petrochemicals to final products, RIL is focused on expanding its use of recycled polyester (rPET) for both fibers and packaging, in line with India’s growing sustainability ambitions. The company’s January 2025 announcement to scale up rPET applications underscores a strategic commitment to the circular economy, leveraging vast production capacity and technological expertise.

Eastman Chemical Company Scales Advanced Molecular Recycling

Eastman Chemical Company of the United States stands out for its pioneering molecular recycling technology, enabling chemical breakdown of complex plastics into virgin-quality PET. Eastman’s April 2025 announcement of new brand partnerships for its advanced recycling output validates the market’s appetite for circular solutions. The company operates one of the world’s largest molecular recycling facilities, focusing on high-purity rPET for premium packaging, textiles, and consumer durables. Eastman’s emphasis on technology licensing and global collaboration amplifies the reach of its circular PET solutions.

Loop Industries Accelerates PET Chemical Recycling Globally

Loop Industries, Inc. specializes in proprietary depolymerization technology to chemically recycle PET waste especially colored and hard-to-recycle material into food-grade resin. The May 2025 milestone with SK geo centric to develop a PET depolymerization plant in South Korea marks a major step in global expansion. Loop’s model of technology licensing and regional partnerships aims to establish a distributed network for high-purity, circular PET production, empowering brand owners to reach aggressive recycled content targets and supporting the plastics circular economy.

Polyethylene Terephthalate (PET) Market Share Analysis: Segment Insights for 2025

Virgin PET Dominates, but Recycled PET Surges with Sustainability Mandates

Virgin PET resin remains the clear leader, capturing 65% of the global PET market share in 2025. Its dominance is rooted in cost efficiency, high clarity, and compliance with stringent food safety standards, making it the top choice for water, soft drink, and food packaging worldwide. However, the rapid rise of recycled PET (rPET) is reshaping the market. Major beverage brands are aggressively targeting 30% rPET content in bottles by 2025, spurred by regulations such as the EU Single-Use Plastics Directive and U.S. EPA circularity goals. Post-consumer rPET driven by bottle collection and recycling programs forms the bulk of supply, while post-industrial rPET leverages factory scrap for pre-consumer circularity. Virgin PET continues to be preferred in pharmaceutical and medical packaging where ultimate safety is non-negotiable. A key industry focus is on narrowing the cost gap between rPET and virgin PET, as recycling scale and supply chain efficiencies improve globally.

Packaging Leads by a Wide Margin, with Fibers and Engineering Plastics Growing

Packaging applications account for a commanding 75% of global PET demand in 2025, with beverage bottles representing the largest sub-segment (60%), followed by trays and films (15%). The market is powered by strong demand for lightweight, transparent, and shatter-resistant packaging in food, beverage, household, and personal care products. Fibers contribute 15% of the PET market, particularly in polyester textiles for apparel, fast fashion, home furnishings, and carpets. The growth in rPET use by leading apparel brands (such as Adidas and H&M) is boosting the recycled fibers segment. Engineering plastics represent a smaller but important niche, where PET’s strength, chemical resistance, and lightweighting advantages benefit automotive, electronics, and other industrial uses. Other emerging applications such as 3D printing filaments and medical devices highlight PET’s versatility as technology and end-user requirements evolve.

.png)

China: Global PET Production and Recycling Powerhouse

China stands as the world’s foremost PET producer and consumer, underpinned by massive investments in new polymerization lines, integrated petrochemical complexes, and a booming recycling sector. The country’s dominant position is fueled by extraordinary demand for beverage bottles, food packaging, and polyester fibers for the colossal textile industry. Regulatory tightening mandating minimum rPET content in packaging has triggered a surge in domestic recycling infrastructure, including pioneering investments in chemical recycling. China’s “Green Manufacturing” policies and rapid technological upgrades have enabled the integration of more rPET into consumer and industrial products, making China a key supplier for both domestic and export markets seeking circularity and compliance with global sustainability standards.

China’s PET value chain is also innovating in high-performance films, engineering plastics, and specialty applications. With rising focus on environmental goals, Chinese producers are investing heavily in advanced sorting, depolymerization, and closed-loop recycling systems. International partnerships and continued R&D place China at the epicenter of both traditional and next-generation PET solutions, as the nation looks to maintain its market leadership while accelerating the transition toward sustainable plastics.

United States: Leader in PET Innovation and Circular Economy

The United States is a trailblazer in PET resin and recycling technology, with major players like Eastman Chemical and Alpek driving high-performance PET grades and advanced molecular recycling solutions. U.S. government policies, such as the EPA’s support for recycled content and circularity, are stimulating demand for rPET and investment in new recycling facilities. American companies are also innovating in high-clarity, food-safe packaging and engineering plastics for automotive and electronics. Partnerships across the supply chain from bottle collection to rPET pelletization support a robust circular economy for PET.

Recent developments, such as Alpek’s planned 100,000 MT/year rPET expansion in North America, reflect the scale of commitment to meet brand and regulatory targets. The U.S. is also a major consumer of PET for beverage, food, and non-food containers, as well as polyester fibers for both industrial and apparel use. With a strategic focus on closing the loop, the U.S. remains a global benchmark for PET recycling technology and sustainable packaging leadership.

India: Rapid Market Expansion and Localized PET Circularity

India’s PET market is experiencing rapid growth, driven by surging demand in packaging, bottled water, soft drinks, edible oils, and textiles. Major players like Reliance Industries are ramping up polyester production and investing in new capacities for both virgin PET and rPET. The government’s “Make in India” campaign, coupled with increasing consumer awareness of plastic waste, is accelerating the domestic recycling ecosystem and adoption of sustainable packaging solutions.

India is quickly becoming a strategic growth market for PET, not only for food and beverage packaging but also as a supplier of polyester fiber for global textile and apparel brands. Investments in local PET recycling infrastructure and public-private initiatives are positioning India as a regional leader in circular economy plastics. The focus is increasingly on improving collection rates, developing efficient recycling technologies, and scaling up rPET usage to align with evolving global and domestic sustainability goals.

Germany: European Leader in PET Recycling and Circular Packaging

Germany is a pioneer in advanced PET recycling, lightweight packaging design, and sustainable materials. Stringent EU waste management regulations, such as deposit-return systems, have made high rPET content bottles the norm, with many German producers exceeding regulatory targets. The country is also a hub for R&D in chemical depolymerization, enabling higher quality recycled PET for food and beverage use. German innovation in lightweight, recyclable PET packaging and eco-friendly design supports a mature and highly circular PET value chain.

The packaging sector dominates PET demand in Germany, with a strong focus on beverage bottles, food containers, and high-performance films. German companies are also driving the adoption of bottle-to-bottle recycling and closed-loop supply models, influencing PET markets across Europe and beyond. Investments in infrastructure, public awareness, and continuous regulatory evolution ensure Germany’s ongoing leadership in sustainable PET solutions.

Japan: Technology Pioneer in PET and High-Value Recycling

Japan’s PET market is defined by technological excellence, high collection rates, and advanced recycling systems. The country is a leader in molecular recycling, efficient bottle collection, and producing high-purity rPET for both packaging and industrial applications. Japanese companies like Teijin and Sumitomo Chemical are developing breakthrough recycling technologies to maximize circularity and resource efficiency. The government’s proactive recycling policies and resource stewardship have established Japan as a global reference for closed-loop PET management.

Beyond beverage bottles and food packaging, Japan is at the forefront of developing high-performance PET films for electronics, LCDs, and engineering plastics for industrial use. The focus on innovation and stringent quality standards ensures that Japanese PET products are synonymous with reliability, safety, and sustainability.

South Korea: Advanced Recycling Hub and Exporter of PET Innovation

South Korea is a regional leader in PET resin production, recycling technology, and advanced materials innovation. Major investments are flowing into both virgin PET manufacturing and rPET processing, as companies pursue global market share and sustainable solutions. South Korea’s policies supporting plastic circularity and waste reduction are driving new developments in chemical recycling, particularly depolymerization.

Joint ventures like Loop Industries and SK geo centric’s Ulsan plant reflect a strong commitment to technological leadership in PET recycling. The packaging and electronics sectors are the primary consumers, with increasing focus on sustainable textiles and polyester fibers. As a hub for PET innovation and an exporter of advanced recycling solutions, South Korea is shaping the future of sustainable plastics in Asia and beyond.

Brazil: Expanding PET Packaging and Recycling Capacities

Brazil’s PET market is growing steadily, propelled by a large food and beverage sector, rising consumer demand for packaged products, and investment in recycling infrastructure. Beverage bottles for water, soft drinks, and juices are the dominant application, while food containers and cleaning product packaging also represent significant segments. The Brazilian government’s growing awareness of plastic waste and emerging regulations are boosting PET collection and recycling rates.

Mechanical recycling remains the primary technology, but there is increasing interest in chemical recycling and higher-value applications for rPET. Brazilian companies are focused on expanding both virgin and recycled PET capacities, aligning with global trends toward sustainable packaging and circular economy plastics.

Mexico: North American Hub for PET Production and Exports

Mexico plays a critical role in the North American PET market, with robust manufacturing capabilities for beverages and consumer goods driving substantial PET packaging demand. Companies like Alpek have major operations in Mexico, supplying both domestic and export markets with virgin PET and rPET. The country is investing in advanced resin production and expanding rPET facilities to serve the region’s growing need for sustainable packaging.

High consumption in beverage and food bottles is complemented by a strategic focus on export competitiveness and integration with U.S. and Canadian supply chains. Mexico’s rising rPET capacity, underpinned by local innovation and international investment, supports its emergence as a production and recycling hub for the Americas.

Polyethylene Terephthalate Market Report Scope

Polyethylene Terephthalate Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$34.7 Billion

|

|

Market Size (2034)

|

$62.2 Billion

|

|

Market Growth Rate

|

6.7%

|

|

Segments

|

By Type (Virgin PET Resin, Recycled PET (rPET) Resin (Flakes, Pellets - Post-Consumer, Post-Industrial))

By Application (Packaging, Bottles - Water, CSD, Edible Oil, Films - Flexible Packaging, Industrial Films, Graphic Arts, Sheets & Trays - Food Containers, Blister Packaging, Fibers, Polyester Staple Fiber – PSF, Filament Yarn - POY, DTY, FDY, Industrial Yarns - Tire Cords, Seatbelts, Engineering Plastics, Automotive Components, Electrical & Electronic Parts, Industrial Applications, Other Applications)

By End-Use Industry (Food & Beverage, Textile, Automotive, Electrical & Electronics, Consumer Goods, Healthcare, Other Industrial Applications

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Indorama Ventures Public Company Limited, Alpek S.A.B. de C.V., Reliance Industries Limited, Eastman Chemical Company, Loop Industries, Inc., Sinopec Corporation, DuPont de Nemours, Inc., Lotte Chemical Corporation, SK geo centric Co., Ltd., Formosa Plastics Corporation, Far Eastern New Century Corporation, Zhejiang Wankai New Materials Co., Ltd., Daicel Corporation, Carbon Lite Recycling LLC, Evergreen Plastics, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Polyethylene Terephthalate Market Segmentation

By Type

Virgin PET Resin

Recycled PET (rPET) Resin (Flakes, Pellets - Post-Consumer, Post-Industrial)

By Application

- Packaging

- Bottles - Water, CSD, Edible Oil

- Films - Flexible Packaging, Industrial Films, Graphic Arts

- Sheets & Trays - Food Containers, Blister Packaging

- Fibers

- Polyester Staple Fiber – PSF

- Filament Yarn - POY, DTY, FDY

- Industrial Yarns - Tire Cords, Seatbelts

- Engineering Plastics

- Automotive Components

- Electrical & Electronic Parts

- Industrial Applications

- Other Applications

By End-Use Industry

- Food & Beverage

- Textile

- Automotive

- Electrical & Electronics

- Consumer Goods

- Healthcare

- Other Industrial Applications

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Polyethylene Terephthalate Market

- Indorama Ventures Public Company Limited

- Alpek S.A.B. de C.V.

- Reliance Industries Limited

- Eastman Chemical Company

- Loop Industries, Inc.

- Sinopec Corporation

- DuPont de Nemours, Inc.

- Lotte Chemical Corporation

- SK geo centric Co., Ltd.

- Formosa Plastics Corporation

- Far Eastern New Century Corporation

- Zhejiang Wankai New Materials Co., Ltd.

- Daicel Corporation

- Carbon Lite Recycling LLC

- Evergreen Plastics, Inc.

* List Not Exhaustive

Research Coverage

This report from USDAnalytics provides a dynamic, data-driven investigation of the Polyethylene Terephthalate (PET) Market, covering industry breakthroughs, sustainability initiatives, and end-use trends. It delivers in-depth segmentation by type, application, and end-use industry, and reviews market drivers, regulatory impacts, recycling advancements, and supply chain developments. With coverage of historic data (2021–2024) and forecasts (2025–2034), this report is an essential resource for packaging manufacturers, brand owners, recyclers, investors, and policymakers navigating the evolving PET landscape.

By Type: Virgin PET Resin, Recycled PET (rPET) Resin Post-Consumer, Post-Industrial

By Application: Packaging (Bottles, Films, Trays), Fibers, Engineering Plastics, Other Applications

By End-Use Industry: Food & Beverage, Textile, Automotive, Electrical & Electronics, Consumer Goods, Healthcare, Other Industries

Geographic Scope: 25+ countries across North America, Europe, Asia Pacific, South America, and Middle East & Africa

Historic Data: 2021–2024 and Forecast Data: 2025–2034

Companies Covered: Indorama Ventures, Alpek, Reliance Industries, Eastman Chemical, Loop Industries, Sinopec, DuPont, Lotte Chemical, SK geo centric, Formosa Plastics, Far Eastern New Century, Zhejiang Wankai, Daicel, Carbon Lite Recycling, Evergreen Plastics

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.