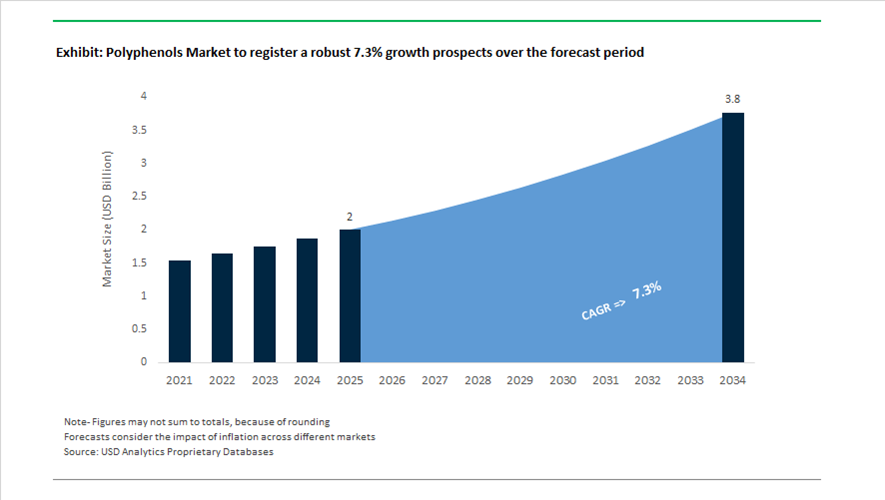

Polyphenols Market Valued at $2 Billion in 2025, Projected to Reach $3.8 Billion by 2034 at 7.3% CAGR

The global polyphenols market is valued at $2 billion in 2025 and is projected to reach $3.8 billion by 2034, registering a strong CAGR of 7.3%. Growth is driven by rising demand for plant-based antioxidants, botanical extracts, flavonoids, phenolic acids, green tea polyphenols, olive polyphenols, and cocoa-derived bioactives across nutraceuticals, functional foods, cosmetics, animal nutrition, and plant-based meat alternatives. Increasing scientific validation of oxidative stress mitigation, cellular protection, immune modulation, and microbiome interaction is accelerating commercial adoption of standardized polyphenol ingredients.

In January 2024, Novozymes and Chr. Hansen completed their merger to form Novonesis, creating the world’s largest biosolutions company. The consolidation enables advanced enzyme platforms to improve the extraction efficiency, bioavailability, and stability of plant-based phenolic compounds. Enzymatic bioprocessing is becoming critical for enhancing yield from botanical sources such as grapes, olives, tea leaves, and berries while maintaining polyphenol integrity. In April 2024, Layn Natural Ingredients released shelf-life data for its TruGro AOX+ blend of rosemary, tea, and pomegranate polyphenols, demonstrating up to one year of shelf-life extension in pet food formulations as a natural alternative to synthetic antioxidants like BHA and BHT. In June 2024, Bayer’s One A Day brand launched “Age Factor Cell Defense,” incorporating olive-derived polyphenols to target oxidative stress and cellular aging. In July 2024, ADM introduced a wellness gummy line featuring clinically studied botanical polyphenols, capitalizing on consumer preference for convenient supplement delivery formats. That same month, Unilever launched a Vaseline lotion formulated with 100% green tea extract, reinforcing demand for topical polyphenols in skin barrier protection and cosmetic antioxidant formulations. In November 2024, Groupe Berkem introduced RECELLCL’IN, a passiflora-derived cosmetic active rich in polyphenols, emphasizing localized and sustainable botanical sourcing in France.

Technological scaling and alternative production models gained traction in 2025. In January 2025, Layn Natural Ingredients unveiled water-soluble polyphenol feed additives for poultry and swine, enabling antioxidant delivery via drinking water, particularly valuable during heat stress when feed intake declines. In 2025, Givaudan expanded “The Cultured Hub” in partnership with Bühler and Migros to include plant cell culturing technology for high-value polyphenols from cocoa and coffee. This approach reduces reliance on climate-sensitive agriculture while ensuring consistent bioactive concentration. In October 2025, dsm-firmenich opened its Global Food Innovation Center in Delft, focusing on diet transformation and the integration of polyphenols into plant-based meat and dairy alternatives to improve oxidative stability and nutritional density. In December 2025, dsm-firmenich named Frosted Star Anise as its 2026 Flavor of the Year, highlighting increased consumer interest in spice-derived polyphenols with functional health positioning.

Distribution and nutraceutical penetration have expanded alongside production innovation. In July 2024, Brenntag Specialties entered into an exclusive agreement with Cargill to distribute EpiCor, a postbiotic fermentate rich in polyphenols and metabolites, strengthening global supply to immune-health supplement manufacturers. The polyphenols market is increasingly characterized by enzyme-assisted extraction technologies, plant cell culture production systems, clinically validated botanical antioxidants, polyphenol-enriched gummies, natural food preservation blends, animal feed antioxidant solutions, and topical cosmetic formulations. Scientific substantiation, sustainable sourcing models, and integration into plant-based product reformulation strategies are driving rapid value expansion across food, nutraceutical, cosmetic, and feed industries.

Trends and Opportunities in the Polyphenols Market

Strategic Sourcing and Vertical Integration for Supply Chain Purity

The polyphenols market is undergoing a structural shift toward vertically integrated, farm-to-formulation supply models as brands and regulators raise the bar on traceability, consistency, and clean-label compliance. Polyphenols are inherently sensitive to cultivar selection, harvest timing, and post-harvest handling, making raw material control a decisive competitive factor rather than a procurement detail. As a result, leading ingredient suppliers are moving upstream to secure proprietary access to high-catechin green tea varieties, anthocyanin-rich berries, and flavanol-dense cocoa and grape sources that meet pharmaceutical- and nutraceutical-grade specifications.

In 2024, several global botanical derivative producers expanded long-term cultivation contracts across the Mediterranean basin and Southeast Asia to lock in traceable, single-origin polyphenol streams. These agreements are increasingly supported by analytical profiling platforms that document polyphenol fingerprints at each stage of the value chain, reducing batch-to-batch variability and insulating suppliers from the volatility created by 2025 U.S. tariff adjustments on imported botanical intermediates. This level of control is now essential for customers seeking reproducible clinical outcomes rather than generic antioxidant positioning.

Processing technology is reinforcing this purity-led trend. In 2025, the adoption of supercritical CO₂ extraction and ultrasonic-assisted extraction accelerated sharply, driven by consumer data indicating that 68% of global buyers actively avoid solvent-intensive ingredients. These green extraction technologies preserve thermolabile polyphenols while eliminating residual solvents, enabling suppliers to meet both regulatory scrutiny and premium brand requirements. German specialty ingredient manufacturers have been particularly active in this space, leveraging advanced extraction to commercialize standardized polyphenol ingredients designed for gut, immune, and metabolic applications.

Geopolitical considerations are also influencing integration strategies. To mitigate shipping disruptions and thermal degradation risks during long transit times, North American and European companies are acquiring or partnering with regional processors. This localized production buffer ensures that high-purity polyphenols retain bioactive integrity, a critical requirement as applications move from general wellness into regulated functional foods and condition-specific nutrition.

Formulation Pivot to Functional Gummies and Fast-Release Formats

Consumer fatigue with traditional capsules and tablets has triggered a decisive pivot toward gummies, soft chews, and effervescent delivery systems, fundamentally reshaping polyphenol formulation requirements. While demand for these formats is surging, polyphenols present unique challenges due to their bitterness, oxidative instability, and sensitivity to heat and moisture during processing. Addressing these challenges has become a major innovation frontier within the market.

Between 2024 and 2025, advances in molecular grafting and macromolecular stabilization enabled polyphenols to be chemically anchored to gelatin and plant-based hydrocolloids. These eco-friendly grafting techniques have demonstrated the ability to maintain stability through gummy manufacturing while delivering near-complete bioaccessibility during digestion. This has been particularly impactful for citrus-derived flavonoids, which historically degraded under thermal processing conditions.

At the commercial level, brands are increasingly upcycling orange and lemon peel by-products into high-value polyphenol cores for gummies and chewables. These formulations concentrate hesperidin and narirutin in fast-release matrices, aligning with Gen Z and millennial demand for snackable formats that provide immediate antioxidant and immune support. The shift toward these delivery systems is expanding polyphenol consumption occasions beyond supplements into functional confectionery and hybrid food-nutrition categories.

Clinically Validated Ingredients for Cognitive and Metabolic Health

The most defensible growth opportunity in the polyphenols market lies in proprietary, clinically validated ingredients that move beyond broad antioxidant claims toward specific, regulator-recognized health benefits. Following the FDA’s 2023 Qualified Health Claim linking high-flavanol cocoa powder with reduced cardiovascular disease risk, suppliers are increasingly investing in human clinical trials to establish similar credibility in cognitive performance, metabolic health, and vascular function.

The Cocoa, Cognition, and Aging (CoCoA) Study has emerged as a reference point, demonstrating that sustained flavanol intake can measurably improve processing speed and executive function in aging populations. This evidence has catalyzed interest in cognitive-positioned polyphenols derived from cocoa, berries, and tea, particularly as global populations age and demand for non-pharmaceutical cognitive support grows.

In Europe, the EFSA Article 13.5 “new function” claim pathway represents a strategic lever for differentiation. Suppliers that secure proprietary clinical datasets benefit from data protection, allowing them to command premium pricing and long-term customer lock-in. This is especially relevant as the functional food and beverage segment, valued at over USD 2 billion, increasingly prioritizes ingredients with substantiated mechanisms of action rather than generic wellness narratives.

Regulatory developments are reinforcing this opportunity. The FDA’s April 2025 update to its “Healthy” Final Rule expanded eligibility criteria for nutrient content claims, allowing certain polyphenol-rich foods to carry the “Healthy” label provided they meet revised thresholds for sugars and saturated fats. This creates a direct commercialization pathway for polyphenol-fortified snacks, beverages, and nutrition bars positioned around heart and brain health.

Natural Food Preservation and Clean-Label Antioxidant Systems

The global move away from synthetic preservatives is opening a large-volume, formulation-driven opportunity for polyphenols as natural antioxidant systems. Food manufacturers are under increasing pressure to eliminate BHA, BHT, and sodium benzoate while maintaining shelf-life, color stability, and oxidative resistance across meat, bakery, and ready-to-eat categories.

Industry trials conducted in late 2024 demonstrated that rosemary extracts rich in rosmarinic and carnosic acids can deliver antioxidant performance three to five times stronger than synthetic BHA. In processed meat applications, these polyphenols extended shelf-life by up to 60 days, compared to approximately 25 days achieved with conventional nitrite systems. Similar synergies have been observed when rosemary is combined with green tea polyphenols, creating multi-layered oxidative protection.

To overcome sensory challenges, manufacturers are increasingly deploying microencapsulation and nanoemulsion technologies. These systems mask herbal or bitter notes and protect polyphenols at temperatures reaching 180°C, enabling their use in high-heat bakery applications where they can replace calcium propionate without altering taste or texture.

Polyphenols Market Share and Segmentation Insights

Flavonoids Lead Polyphenols Market with Broad Applications in Nutraceuticals and Functional Foods

Flavonoids accounted for 52.80% of the Polyphenols Market by product type in 2025, reflecting their widespread occurrence in fruits, vegetables, tea, cocoa, and wine and their extensive use in nutraceuticals, functional foods, and cosmetic formulations. This diverse class of polyphenols is recognized for strong antioxidant, anti-inflammatory, and cardioprotective properties, making flavonoids a key ingredient in dietary supplements and health-focused food products. Increasing consumer awareness of natural antioxidants and plant-based bioactive compounds continues to support flavonoid demand across global nutraceutical markets. In 2025, advances in flavonoid bioavailability technologies are gaining industry attention, with nanoparticle encapsulation, phytosome complexes, and co-crystallization techniques improving absorption efficiency and enabling premium functional food and supplement formulations.

Plant-Based Sources Dominate Polyphenol Extraction for Nutraceutical and Functional Ingredient Production

Plant-based sources represented the largest share of the Polyphenols Market by source in 2025, supported by the abundance of polyphenol compounds in fruits, vegetables, herbs, tea leaves, cocoa, grapes, and other botanical raw materials. These natural sources are widely used to produce polyphenol extracts for dietary supplements, functional beverages, cosmetics, and pharmaceutical ingredients. The rising demand for plant-derived antioxidants and clean label nutraceutical ingredients continues to drive large-scale extraction and processing of botanical polyphenols. In 2025, advanced extraction technologies such as supercritical CO₂ extraction and green solvent processing are improving polyphenol yield and purity, enabling manufacturers to produce standardized plant extracts that meet stringent quality requirements for global functional ingredient and nutraceutical markets.

Polyphenols Market Competitive Landscape

The global polyphenols market is entering a bio-efficacy phase, driven by clinically validated nutraceuticals, phytosome delivery systems, and precision botanical extraction. Competitive intensity is shaped by metabolic health positioning, clean-label demand, and advanced bioavailability technologies across functional foods, beverages, and supplements.

Givaudan Accelerates Botanical Integration with Naturex and Clinically Proven Polyphenol Solutions

Givaudan is strengthening its leadership in polyphenols through deep integration of its Naturex portfolio into health and active beauty segments. The company reported CHF 7.47 billion in 2025 sales with a strong 24.2% EBITDA margin, reflecting resilience despite input cost pressures. Its $110 million Mexico facility investment enhances regional supply chain agility for botanical extracts and polyphenol ingredients. Cereboost™, a clinically validated American ginseng extract, demonstrates strong cognitive performance benefits, reinforcing Givaudan’s position in functional nutraceuticals. The company is leveraging digital tools and regulatory foresight to deliver integrated, clean-label polyphenol solutions. Strategy focuses on clinical validation, botanical integration, and global supply optimization.

IFF Refocuses on High-Value Biosciences with Portfolio Streamlining and Margin Expansion

IFF is undergoing a strategic transformation by divesting lower-margin assets to prioritize high-value polyphenol and bioscience applications. The company reported $10.89 billion in 2025 revenue with a 19.2% adjusted EBITDA margin, despite a decline due to divestitures. Its Health & Biosciences segment delivered strong growth, driven by demand for proactive health ingredients and microbial stabilization technologies. IFF is aligning its R&D pipeline toward high-efficacy polyphenols and functional ingredients. The company projects stable 2026 revenues while focusing on profitability and innovation-led growth. Strategy centers on portfolio optimization, bioscience integration, and high-margin nutraceutical ingredients.

Kerry Group Enhances Functional Polyphenol Delivery with AI-Driven Taste Masking and Fermentation Capabilities

Kerry Group is positioning itself as a leader in taste and nutrition by addressing key formulation challenges of polyphenols, particularly bitterness and astringency. Its Tastesense Advanced platform uses AI-driven sensory optimization to maintain flavor integrity in polyphenol-rich functional beverages. The company achieved EBITDA margin expansion to 17.9% in 2025 and targets further improvement through its Accelerate 2.0 program. Kerry’s biotechnology investments, including its Leipzig center, support fermentation-derived polyphenol production and enzyme innovation. Emerging markets are a key growth driver, with strong expansion in Asia and Latin America. Strategy focuses on taste optimization, fermentation technology, and global nutraceutical expansion.

Indena Leads Bioavailability Innovation with Phytosome® Technology and Pharmaceutical-Grade Polyphenols

Indena is the scientific leader in polyphenol bioavailability, leveraging its proprietary Phytosome® delivery system to enhance absorption of botanical actives. The launch of CRONILIEF® demonstrates its expansion into clinically supported health solutions for chronic conditions. Its Quercefit® platform targets cellular aging and senescence, aligning with the growing "healthy aging" market. Indena’s collaboration on antibody-drug conjugates highlights its transition toward pharmaceutical-grade applications. The company is also advancing sustainability through renewable energy investments across its operations. Strategy centers on bioavailability enhancement, clinical efficacy, and high-value pharmaceutical integration.

Novonesis Integrates Microbial Science with Polyphenols for Metabolic Health Solutions

Novonesis, formed from the merger of Chr. Hansen and Novozymes, is emerging as a biosolutions powerhouse in the polyphenols market. The company achieved 7% organic growth and a high 37.1% EBITDA margin in 2025, driven by strong performance across segments. Its collaboration with Novo Nordisk focuses on metabolic health, aligning polyphenol applications with GLP-1-driven dietary trends. The integration of enzyme and probiotic technologies enables synergistic health benefits in functional nutrition. Novonesis also achieved 100% renewable electricity across its operations, reinforcing its sustainability leadership. Strategy emphasizes bioscience integration, metabolic health innovation, and sustainable production.

ADM Expands Polyphenol Portfolio with Vertical Integration and Functional Nutrition Positioning

ADM is strengthening its role in the polyphenols market by leveraging its global agricultural supply chain and focus on functional nutrition. The company reported 2025 EPS of $3.43 and expects improved performance in 2026 driven by demand for plant-based extracts. Its cost efficiency program is generating up to $750 million in savings, which is being reinvested into digitalization and ingredient innovation. ADM’s trend strategy highlights "Lifelong Vitality" and "Age Hacking," positioning polyphenols as key components for cognitive and physical performance. Its vertically integrated sourcing ensures traceability and purity for clean-label applications. Strategy focuses on scalable production, functional health positioning, and supply chain transparency.

China: Regulatory Enablement and Scaled Bio-Extraction Driving Polyphenol Leadership

China continues to consolidate its position as a global production and innovation hub for polyphenols, supported by regulatory approvals, large-scale botanical processing, and circular bioeconomy initiatives. In May 2025, the National Health Commission approved Sakura Polyphenols derived from Prunus serrulatus as a new food raw material under Announcement No. 3, formally recognizing its antioxidant efficacy for functional beverages and beauty-from-within formulations. This approval reflects a broader regulatory openness toward novel, plant-derived polyphenols with substantiated health benefits. China also maintains global leadership in tea polyphenols, with the Zhejiang province accounting for a substantial share of worldwide EGCG supply during the 2025 fiscal year, reinforcing the country’s strategic dominance in green tea catechins used across nutraceuticals, sports nutrition, and functional foods.

Sustainability and traceability are increasingly shaping China’s polyphenol value chain. In alignment with the 2025 Circular Economy Promotion Plan, manufacturers have scaled up the extraction of apple polyphenols and grape stem proanthocyanidins from pomace waste, improving resource efficiency while reducing raw material costs. Bio-manufacturing capacity has matured further, with the Guilin Layn Natural Ingredients facility reaching full operational optimization in early 2025, focusing on high-purity monk fruit and stevia-polyphenol blends for clean-label sweetening systems. Cross-border innovation is also visible through Japanese-Chinese joint ventures such as Fujicco, which are expanding Chronocare SP production, a black soybean seed coat extract containing over 58% polyphenols for functional food labeling across Asia. Mandatory QR-code based digital traceability introduced in 2025 now requires exporters to disclose polyphenol content and solvent residue levels, strengthening China’s credibility with international pharmaceutical and nutraceutical buyers.

France: Clean-Label Innovation and Premium Polyphenol Applications

France represents a high-value, innovation-led polyphenols market characterized by eco-extraction technologies, clinical research, and premium end-use integration. In April 2025, Naturex, part of Givaudan, announced a strategic expansion of its French production facility to meet rising EU demand for plant-based antioxidants aligned with the clean-label movement. The site deploys eco-extraction processes that reduce solvent usage while preserving phenolic integrity, positioning France as a benchmark for sustainable polyphenol manufacturing.

Scientific validation is reinforcing market credibility. In late 2025, ICTAN-CSIC in collaboration with French academic institutions published data demonstrating that specific phenolic metabolites can cross the blood-brain barrier, supporting neuroprotective positioning in Alzheimer’s prevention research. Product specialization is also advancing. Diana Food launched Upurin in 2025, a high-performance apple polyphenol extract derived from Brittany’s cider-apple biomass, optimized for high phenolic concentration and stability. Demand from cosmeceuticals remains strong, with luxury groups such as L'Oréal and LVMH increasing procurement of resveratrol and grape seed extracts for anti-pollution and UV-repair skincare lines. Additionally, adoption of the 2025 Biodiversity Sourcing Charter ensures certified soil-health conservation for olive and grape-derived polyphenols, reinforcing France’s leadership in ethically sourced, premium-grade antioxidants.

United States: Functional Claims, Branded Ingredients, and Biotech Pathways

The United States polyphenols market in 2025 is being reshaped by regulatory recalibration, consumer willingness to pay for clinically validated ingredients, and biotechnology-driven supply diversification. The FDA’s final rule on the “Healthy” nutrient content claim has accelerated the incorporation of polyphenols as functional markers in reduced-sugar snacks and beverages, enabling manufacturers to maintain health-forward positioning amid sugar reformulation. This regulatory clarity has coincided with strategic supply chain adjustments. Nutraceutical players such as NOW Foods and Herbalife redirected investments in 2025 toward domestic botanical sourcing, increasing reliance on North American grape, berry, and citrus polyphenols to mitigate trade-related risks.

Consumer behavior is reinforcing premiumization. Insights shared during Vitafoods 2025 indicated that over 70% of U.S. consumers are willing to pay a significant premium for supplements containing branded, clinically proven polyphenols such as Pycnogenol or advanced quercetin derivatives. Product innovation is also evident in immune health, where launches of immune-plus shots increased by 15% post-2024, combining zinc and vitamin C with citrus bioflavonoids to enhance bioavailability. On the supply side, the U.S. Department of Agriculture expanded precision fermentation grants in 2025, supporting startups producing nature-identical polyphenols like resveratrol via bioreactors. This approach reduces dependence on agricultural variability while ensuring consistent purity and scalability.

India: Export-Oriented Botanicals and Standardized Traditional Extracts

India’s polyphenols industry is transitioning from traditional herbal extraction toward standardized, export-ready nutraceutical ingredients. In 2025, the Production Linked Incentive scheme for food processing expanded to include curcumin and ginger polyphenol extractors, strengthening India’s competitiveness in high-value botanical exports to Europe. Product differentiation is advancing rapidly. Companies such as SV Agrofood launched Ginger Polyphenol 26FFC in 2025, delivering over 26% gingerols and shogaols tailored for digestive health formulations.

Regulatory modernization is reinforcing global acceptance. In late 2025, the Ministry of AYUSH standardized phenolic fingerprinting protocols for traditional extracts including amla and ashwagandha, aligning Indian herbal exports with EU Novel Food safety requirements. Infrastructure investments are supporting this shift. Sabinsa expanded its biotechnology research operations in Bengaluru in 2025, focusing on black pepper polyphenols and their function as bio-enhancers for nutrient absorption. Collectively, these initiatives position India as a scalable supplier of clinically standardized, plant-based polyphenols for global nutraceutical markets.

Germany: Bio-Derived Antioxidants and Processing Innovation

Germany’s polyphenols market is characterized by regulatory foresight, processing innovation, and integration into functional foods and industrial applications. German firms are preparing for the 2026 implementation of the New European Biotech Act, which is expected to streamline commercialization of enzymatically produced polyphenols, reducing time-to-market for innovative bio-derived antioxidants. Product innovation is already visible. HERZA Schokolade introduced high-flavanol functional chocolates in 2025 using proprietary roasting techniques that preserve significantly higher cocoa polyphenol levels compared with conventional processing.

Research-led efficiency gains are also notable. The University of Bonn, in collaboration with industry partners, presented supercritical CO2 extraction advancements at the 2025 Polyphenols Applications Congress, achieving substantially higher yields for sensitive flavonoids while minimizing solvent residues. At an industrial level, German chemical leaders including BASF are pivoting toward bio-derived antioxidant systems under the EU’s Clean Industrial Deal framework, aiming to replace synthetic phenolic preservatives in food, cosmetics, and industrial formulations. Germany’s market thus reflects a convergence of biotechnology regulation, sustainable processing, and high-performance applications.

Comparative Overview of Country-Level Dynamics in the Polyphenols Industry

Polyphenols Market County Level Snapshot

|

Country

|

Core 2025 Focus Areas

|

Implications for Polyphenols Industry

|

|

China

|

Regulatory approvals, circular extraction, digital traceability

|

Scaled, compliant supply of tea, fruit, and specialty polyphenols

|

|

France

|

Clean-label demand, clinical research, luxury cosmeceuticals

|

Premium, sustainably sourced polyphenol formulations

|

|

United States

|

Functional claims, branded ingredients, biotech production

|

High-margin demand for clinically validated polyphenols

|

|

India

|

Export-oriented botanicals, standardized traditional extracts

|

Rising global supply of compliant nutraceutical polyphenols

|

|

Germany

|

Biotech regulation, processing efficiency, industrial antioxidants

|

Growth in bio-derived and high-retention polyphenol systems

|

Polyphenols Market Report Scope

Polyphenols Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2 Billion

|

|

Market Size (2034)

|

$3.8 Billion

|

|

Market Growth Rate

|

7.3%

|

|

Segments

|

By Product Type (Flavonoids, Phenolic Acids, Stilbenes, Lignans, Other Polyphenols), By Source (Plant-Based Sources, Marine Sources, Synthetic Sources)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

DSM Nutritional Products, Indena SpA, Naturex, Givaudan, Ajinomoto Co. Inc., International Flavors & Fragrances Inc., Sabinsa Corporation, Kemin Industries Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Polyphenols Market Segmentation

By Product Type

By Source

- Plant-Based Sources

- Marine Sources

- Synthetic Sources

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Polyphenols Industry

- DSM Nutritional Products

- Indena SpA

- Naturex

- Givaudan

- Ajinomoto Co. Inc.

- International Flavors & Fragrances Inc.

- Sabinsa Corporation

- Kemin Industries Inc.

*- List not Exhaustive