Polysiloxane Coatings Market Size, Hybrid Coating Demand, and Extreme Environment Performance

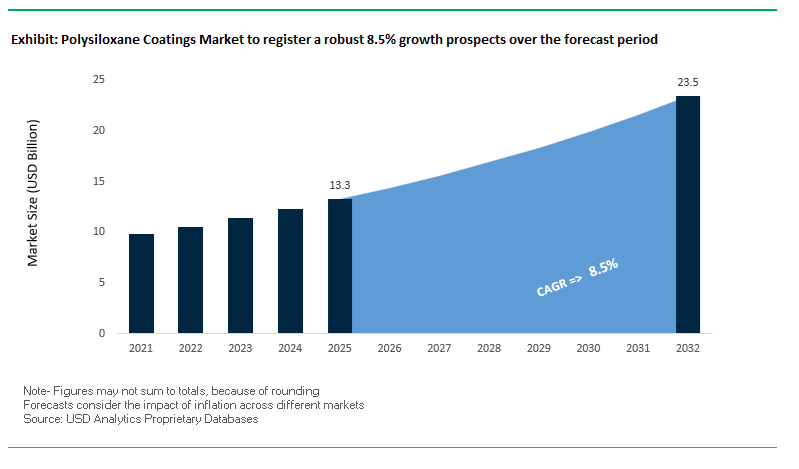

The global Polysiloxane Coatings Market was valued at $13.3 billion in 2025 and is projected to expand at a CAGR of 8.5% through 2032, reaching $23.5 billion by 2032. This strong growth reflects rising demand for high-performance, weather-resistant, and low-VOC coating systems across marine, energy, infrastructure, and industrial sectors.

Polysiloxane coatings are increasingly recognized for their ability to combine the durability of epoxy systems with the UV resistance and gloss retention of polyurethane coatings, making them ideal for extreme environmental conditions. These coatings are widely used in offshore platforms, LNG infrastructure, bridges, wind turbines, and marine vessels, where long-term performance, corrosion resistance, and reduced maintenance cycles are critical.

A major structural driver is the global expansion of energy infrastructure, including LNG terminals, pipelines, offshore oil platforms, and renewable energy installations, all of which require coatings capable of withstanding thermal cycling, chemical exposure, high salinity, and intense UV radiation. Additionally, the increasing adoption of hybrid epoxy-polysiloxane systems is enabling formulators to deliver multi-functional performance, including enhanced adhesion, chemical resistance, and aesthetic longevity.

Sustainability and regulatory compliance are also reshaping the market. The transition toward high-solids, low-VOC, and powder-based polysiloxane coatings is accelerating as manufacturers respond to stricter environmental regulations. These innovations allow for reduced emissions without compromising application performance, positioning polysiloxane coatings as a preferred solution in green infrastructure and decarbonization initiatives.

Market Analysis: Hybrid Coating Innovation, LNG Infrastructure Demand, and Regulatory-Driven Reformulation

Recent developments in the Polysiloxane Coatings Market highlight a strong convergence of advanced material innovation, infrastructure-driven demand, and sustainability compliance. In April 2026, Hempel launched Hempaguard NB, a silicone-based polysiloxane coating designed specifically for marine newbuild applications. This product enables shipyards to integrate high-performance fouling-release systems during construction, improving fuel efficiency and reducing lifecycle emissions.

Technological advancements are enhancing coating performance in extreme environments. Jotun’s next-generation hybrid epoxy-polysiloxane systems (March 2026) deliver improved chemical resistance and gloss retention, addressing the demanding conditions of offshore platforms and power plants, particularly in high-salinity and high-UV regions such as the Middle East.

Regulatory compliance is driving formulation innovation. Wacker Chemie’s SILRES® HP 2000 LV enables the development of ultra-high-solids coatings with minimal VOC content, supporting compliance with stringent environmental regulations in Europe and North America. Additionally, the implementation of EU Regulation 2024/1328 has accelerated industry-wide reformulation efforts, creating a competitive advantage for companies with compliant polysiloxane portfolios.

Infrastructure expansion is further boosting demand. Sherwin-Williams’ focus on polysiloxane coatings for LNG pipeline projects (February 2026) highlights their ability to withstand cryogenic temperatures and harsh environmental conditions, while maintaining long-term aesthetic performance. Meanwhile, Hempel’s expanded Zhangjiagang facility in China supports growing demand from LNG carrier construction and offshore wind projects, reinforcing the importance of regional manufacturing capacity.

Sustainability-driven product innovation is also gaining traction. AkzoNobel’s expansion of powder-based polysiloxane coatings (January 2026) reduces VOC emissions while maintaining high weatherability, and Evonik’s advanced wetting agents improve the performance of acrylic-polysiloxane hybrid systems, ensuring defect-free, high-gloss finishes in demanding applications.

Strategic growth initiatives are aligning with these trends. Hempel’s “Accelerate to Win” strategy (April 2026) emphasizes the expansion of its sustainable polysiloxane portfolio, particularly in Asia and the Middle East, where infrastructure investments are accelerating.

Market Trend: Epoxy-Polysiloxane Hybrid Coatings Optimizing Offshore Wind Turbine Durability and Lifecycle Economics

The polysiloxane coatings market is witnessing strong adoption of epoxy-polysiloxane hybrid systems in offshore wind infrastructure, particularly across harsh marine environments such as the North Sea and Baltic Sea. These hybrid coatings are engineered to combine the corrosion resistance of epoxy primers with the superior UV stability and gloss retention of polysiloxane topcoats, addressing the long-standing performance gap in offshore protective coating systems.

Performance durability is a primary driver. Under ISO 12944-9 C5 and CX corrosivity classifications, advanced epoxy-polysiloxane hybrid coatings demonstrate gloss retention exceeding 90% after 5,000 hours of accelerated QUV-A testing. This translates into real-world performance exceeding five years with minimal color deviation, typically maintaining ΔE values below 2.0. Such stability is critical for offshore wind towers, where coating degradation directly impacts inspection intervals and maintenance costs.

Operational efficiency gains are also significant. By transitioning from conventional three-coat systems consisting of zinc primer, epoxy intermediate, and polyurethane topcoat to streamlined two-coat systems incorporating zinc primer and polysiloxane topcoat, manufacturers are reducing application time by 30% to 40%. This reduction is particularly valuable in offshore fabrication yards, where coating throughput directly affects project timelines and installation schedules.

Lifecycle performance improvements further reinforce adoption. Offshore operators report that epoxy-polysiloxane systems extend the first major maintenance interval to beyond 15 years, reducing the frequency of costly offshore repairs. Additionally, the elimination of intermediate epoxy layers reduces total dry film thickness by 150 to 200 microns per structure, lowering overall coating weight and contributing to structural efficiency in floating wind turbine platforms. These combined benefits are positioning polysiloxane hybrid coatings as a standard specification in offshore renewable energy projects.

Market Trend: Waterborne Polysiloxane Coatings Standardizing Long-Life Bridge Preservation with Ultra-Low VOC Profiles

Infrastructure agencies are increasingly specifying waterborne polysiloxane coatings for steel bridge protection, driven by the dual requirement of long-term durability and compliance with stringent environmental regulations. These coatings provide a high-performance alternative to traditional solvent-borne polyurethane systems, particularly in regions subject to strict VOC emission limits.

Environmental compliance is a critical factor. Modern waterborne polysiloxane formulations consistently achieve VOC levels below 100 g/L, enabling their application in non-attainment zones where conventional solvent-based coatings exceeding 300 g/L are restricted. This capability allows Departments of Transportation to meet regulatory mandates without compromising on protective performance.

Service life extension is a key advantage. Field data from bridge maintenance programs indicates that polysiloxane coating systems can achieve recoat intervals of 20 to 25 years, significantly outperforming the 12 to 15 year lifecycle typical of acrylic urethane coatings. This extended durability reduces maintenance frequency and lowers total lifecycle costs for large-scale infrastructure assets.

Thermal and mechanical resilience further enhance their suitability. The inorganic Si–O backbone structure of polysiloxanes provides exceptional resistance to thermal cycling, with testing demonstrating zero cracking or delamination after 1,000 cycles between −30°C and 60°C. This makes these coatings particularly effective in continental climates with extreme seasonal temperature variations.

The convergence of ultra-low VOC compliance, extended service life, and superior environmental resistance is driving the standardization of waterborne polysiloxane coatings in bridge preservation programs across developed and emerging markets.

Market Opportunity: FHWA Long-Term Bridge Performance Program Validating Polysiloxane Coatings for 25-Year Lifecycle Optimization

The United States infrastructure sector presents a significant growth opportunity for polysiloxane coatings, supported by data-driven validation under the Federal Highway Administration’s Long-Term Bridge Performance program. The program has identified structural steel coating durability as a critical factor in extending bridge service life and reducing maintenance expenditures.

Polysiloxane coatings are emerging as a preferred solution due to their demonstrated ability to deliver long-term protection with reduced lifecycle costs. Data collected through ongoing 2026 evaluations indicates that these coatings can achieve a 25% to 30% reduction in total lifecycle cost compared to traditional alkyd and vinyl coating systems. This cost advantage is driven by extended recoat intervals and reduced maintenance interventions.

Federal funding alignment is further accelerating adoption. Under the Infrastructure Investment and Jobs Act, infrastructure spending increasingly prioritizes materials that can deliver a verified service life of 25 years or more. Polysiloxane coating systems, supported by FHWA performance data, meet these criteria and are being incorporated into procurement specifications for bridge rehabilitation projects.

This alignment between performance validation and funding criteria is creating a strong market pull for high-performance protective coatings. Manufacturers capable of providing certified long-term durability data and compliance with federal standards are gaining increased specification in public infrastructure projects across the United States.

Market Opportunity: China’s GB 30981.2-2025 Enforcement Driving Transition to Ultra-Low VOC Polysiloxane Protective Coatings

China’s regulatory framework is acting as a major catalyst for the adoption of polysiloxane coatings in industrial and infrastructure applications. The enforcement of GB 30981.2-2025 introduces stringent limits on volatile organic compounds and hazardous substances in industrial protective coatings, effectively reshaping formulation strategies across the market.

The regulation imposes strict VOC caps that significantly constrain the use of traditional solvent-borne coatings, pushing manufacturers toward high-solids and waterborne alternatives. Polysiloxane coatings, particularly hybrid systems with solids content exceeding 80%, are well-positioned to meet these requirements while maintaining high-performance corrosion protection.

In addition to VOC restrictions, the standard enforces tighter limits on hazardous substances, including lead, cadmium, hexavalent chromium, and mercury. This regulatory pressure is accelerating the transition toward cleaner, inorganic coating chemistries such as siloxanes, which inherently avoid many of the restricted substances.

The broader industrial policy context further strengthens this opportunity. Under China’s 15th Five-Year Plan for 2026 to 2030, environmentally friendly high-performance coatings are designated as a strategic priority, with a target of achieving 60% adoption of low-VOC technologies in major industrial clusters. This policy direction is expected to drive large-scale replacement of legacy coating systems across sectors such as infrastructure, energy, and heavy industry.

Polysiloxane Coatings Market Share and Segmentation Insights

By Component Configuration: Two-Component (2K) Polysiloxane Coatings Dominate with High-Solids, Low-VOC Performance

The two-component (2K) polysiloxane coatings segment accounted for a leading 78.7% market share in 2025, driven by its optimal balance of performance, environmental compliance, and lifecycle efficiency. These advanced coating systems are widely adopted across bridges, storage tanks, offshore platforms, and heavy infrastructure, where long-term durability and reduced maintenance cycles are critical. Compared to conventional polyurethane coatings, 2K polysiloxanes deliver superior UV resistance and exceptional gloss retention, ensuring prolonged aesthetic and structural integrity in harsh environments. A major advantage lies in their single-coat application capability (primer + topcoat combined), which significantly reduces labor costs and project timelines. Additionally, high-solids formulations exceeding 80% solids with VOC levels below 100 g/L make these coatings compliant with stringent environmental regulations while maintaining excellent corrosion protection and weatherability. This combination of low-VOC coatings, high-performance protection, and cost efficiency continues to strengthen the dominance of 2K polysiloxane systems in global markets.

By Sales Channel: Certified Coating Application Contractors Lead Due to Technical Precision and Compliance Requirements

The certified coating application contractors segment held a dominant 55.1% share of the polysiloxane coatings market in 2025, underscoring the importance of skilled professionals in executing complex coating systems. Polysiloxane coatings demand precise mixing ratios, controlled induction times, and strict environmental conditions such as temperature and humidity, making proper application highly technical. Certified contractors ensure accurate dry film thickness (DFT), adhesion performance, and curing consistency, which are critical for long-term coating success. Their role becomes even more vital in large-scale infrastructure projects, including bridges, dams, and offshore installations, where strict specification standards require detailed documentation of application parameters and environmental logs for project approval. Furthermore, these professionals provide compliance with warranty requirements and regulatory frameworks, enhancing trust among asset owners and project stakeholders. As demand grows for high-performance protective coatings in infrastructure and marine sectors, certified contractor-led channels are expected to remain the backbone of the polysiloxane coatings market.

Competitive Landscape of the Polysiloxane Coatings Market

AkzoNobel Leads Premium Polysiloxane Coatings with AI Integration and Sustainability Initiatives

AkzoNobel N.V. is a leading innovator in the polysiloxane coatings market, strengthening its position through its planned merger with Axalta. In 2026, the company reported improved profitability driven by pricing strategies and cost optimization. Its International® Interfine® series remains a benchmark for high-performance polysiloxane topcoats, widely used in marine and industrial environments. AkzoNobel has introduced AI-driven drone inspection tools capable of detecting degradation in polysiloxane coatings with micron-level precision. Additionally, its collaboration with BASF and Arkema focuses on integrating bio-attributed materials to reduce carbon emissions across the value chain, reinforcing its sustainability leadership.

PPG Expands Market Leadership with Advanced Epoxy-Polysiloxane Hybrid Technologies

PPG Industries, Inc. is a dominant player in the polysiloxane coatings market, particularly in offshore and infrastructure applications. Its PSX® 700 and PSX 805 coatings are industry benchmarks for C5-M marine environments, offering exceptional corrosion resistance and long service life. In 2026, PPG launched the PPG LINQ™ digital ecosystem, enabling AI-driven color matching and coating optimization for large-scale infrastructure projects. The company is also expanding its “Cool Surface” coatings to mitigate urban heat island effects. With strong growth driven by global investments in energy infrastructure, PPG continues to lead in high-performance hybrid coating systems.

Sherwin-Williams Strengthens Infrastructure Coatings with Fast-Cure Polysiloxane Systems

The Sherwin-Williams Company is a major player in the polysiloxane coatings market, leveraging its extensive distribution network and strong Protective & Marine segment. The company has introduced fast-cure polysiloxane coatings that enable return-to-service in under four hours, making them ideal for bridge and highway refurbishment projects. Its integration of the Suvinil acquisition has expanded its footprint in South America. Sherwin-Williams is also focusing on combining automotive-grade aesthetics with industrial-grade durability, aligning with its 2026 innovation initiatives. This approach strengthens its position in both infrastructure and architectural coatings markets.

Jotun Enhances Marine Coatings Leadership with Integrated Performance and Cleaning Solutions

Jotun Group is a leading player in the polysiloxane coatings market, particularly in marine and offshore applications. Its Hardtop® series is widely recognized for high-gloss retention and durability under extreme environmental conditions. Jotun has integrated its Hull Skating Solutions (HSS) technology with polysiloxane coatings, offering a complete performance system that improves vessel efficiency and reduces emissions. The company has achieved strong financial performance, driven by demand in Asia and Africa. Its focus on proactive asset protection and lifecycle optimization reinforces its leadership in the global marine coatings market.

Hempel Drives Efficiency and Sustainability with Silicone-Hybrid Polysiloxane Technologies

Hempel A/S is a key innovator in the polysiloxane coatings market, focusing on silicone-hybrid technologies and efficiency-driven solutions. Its Hempaxane Classic coating provides long-term color stability and durability for industrial applications. The company is expanding the use of biocide-free fouling-release coatings, particularly in marine newbuilding projects. Hempel’s strategic focus on energy storage and biofuel transport applications further strengthens its market position. Its ability to deliver high-performance coatings with reduced environmental impact aligns with global sustainability trends.

Carboline Advances Specialized Polysiloxane Coatings for High-Risk Industrial Applications

Carboline, part of RPM International Inc., is a specialist in high-performance polysiloxane coatings, particularly for critical infrastructure and industrial applications. Its Carboxane® series is widely used for single-coat, high-durability finishes on steel and non-ferrous substrates. In 2026, the company demonstrated that its polysiloxane topcoats maintain fire protection performance when used over intumescent coatings, marking a breakthrough in safety-critical applications. Carboline is also focusing on nuclear-grade coatings, positioning itself as a key supplier for the growing nuclear energy sector. Its digital tools for real-time environmental monitoring enhance application precision and performance reliability.

China Polysiloxane Coatings Market: Dual-Carbon Transition and UHP Coating Expansion

China remains the dominant force in the global polysiloxane coatings market, transitioning toward ultra-high purity (UHP) silicone-hybrid coatings to support advanced industries such as New Energy Vehicles (NEVs), semiconductors, and 6G electronics. Large-scale investments, including the commissioning of the Kunpeng manufacturing facility in Shandong, are strengthening domestic production capacity and addressing supply chain bottlenecks for high-performance coatings.

Regulatory frameworks such as GB 30981.1-2025 are accelerating the shift toward solvent-free, room-temperature curing polysiloxane systems, particularly across major industrial hubs. Technological innovation is also evident in the adoption of nanotechnology-enabled polysiloxane coatings for semiconductor cleanrooms, offering near-zero outgassing and resistance to plasma etching. In marine applications, silicone-modified coatings are improving fuel efficiency and extending maintenance cycles, while demand from the electronics sector is driving the adoption of high-resistivity conformal coatings for flexible OLED and 5G components.

United States Polysiloxane Coatings Market: CHIPS Act Growth and PFAS-Free Innovation

The U.S. polysiloxane coatings market is undergoing a transformation driven by regulatory changes, infrastructure investment, and advanced manufacturing growth. The transition toward PFAS-free polysiloxane formulations is accelerating as manufacturers prepare for stricter environmental regulations, ensuring compliance while maintaining high-performance characteristics such as water repellency.

Federal initiatives, including the CHIPS Act, are boosting demand for polysiloxane coatings in semiconductor facilities, particularly for ultra-pure applications and dielectric protection systems. The aerospace sector is a key growth driver, with increased adoption of polysiloxane topcoats offering significantly improved durability under extreme thermal and UV conditions. Additionally, advancements in sub-zero curing coatings are supporting cold-chain logistics infrastructure, while government mandates targeting methane emissions are driving the use of internal polysiloxane linings in pipeline systems.

India Polysiloxane Coatings Market: Smart Infrastructure and PLI-Driven Growth

India is emerging as one of the fastest-growing markets in the polysiloxane coatings industry, fueled by infrastructure expansion, government incentives, and increasing demand for high-performance coatings. Strategic developments such as the PPG–Asian Paints joint venture renewal and the reopening of advanced manufacturing facilities are strengthening local production capabilities.

The expansion of PLI schemes for specialty chemicals is promoting domestic synthesis of polysiloxane resins, reducing import dependency. Infrastructure projects, including railway modernization, are driving the adoption of high-gloss, UV-resistant coatings for rolling stock, ensuring durability in harsh climatic conditions. Additionally, growth in renewable energy is increasing demand for UV-stable polysiloxane coatings in solar applications, while coastal infrastructure projects are utilizing hybrid coatings to combat corrosion. These trends position India as a key growth engine in the global polysiloxane coatings market.

Germany Polysiloxane Coatings Market: Hydrogen Infrastructure and Circular Economy Leadership

Germany is leading the European polysiloxane coatings market, driven by sustainability goals, hydrogen infrastructure development, and advanced material innovation. The country is pioneering high-density barrier coatings that significantly reduce hydrogen permeation, enabling the safe repurposing of natural gas pipelines for hydrogen transport.

Regulatory pressure under EU frameworks is driving innovation in low-cyclic, environmentally compliant polysiloxane formulations, while research centers such as the Münster hub are advancing HiPIMS-based hybrid coatings. German manufacturers are also developing self-stratifying coatings, which improve performance while reducing material usage. Digital product passports are enhancing traceability across the supply chain, supporting circular economy initiatives. Additionally, the automotive sector is adopting self-healing polysiloxane coatings to improve durability and reduce maintenance costs.

Saudi Arabia Polysiloxane Coatings Market: Vision 2030 and Extreme Climate Performance

Saudi Arabia is emerging as a critical market for high-performance polysiloxane coatings, driven by large-scale infrastructure development under Vision 2030. Projects such as NEOM are mandating the use of UV-stable coatings capable of withstanding extreme desert conditions, including prolonged exposure to intense solar radiation.

The oil and gas sector is also a major driver, with polysiloxane coatings standardized for corrosion-under-insulation (CUI) protection in high-temperature environments. Innovations in abrasion-resistant formulations are supporting pipeline durability in desert conditions, while building regulations are increasing the adoption of waterproofing polysiloxane systems. Localization initiatives under IKTVA are strengthening domestic production of siloxane materials, enhancing supply chain resilience. Additionally, polysiloxane coatings are being widely used in desalination infrastructure to improve corrosion resistance and extend operational life.

South Korea Polysiloxane Coatings Market: Semiconductor Precision and Marine Applications

South Korea’s polysiloxane coatings market is closely aligned with its leadership in semiconductors, OLED displays, and advanced packaging technologies. The expansion of semiconductor clusters is driving demand for plasma-resistant coatings used in cleanroom environments and advanced fabrication facilities.

The country is also innovating in marine applications, developing anti-fouling coatings for LNG carriers that enhance performance while reducing environmental impact. Advances in hybrid PVD-polysiloxane coatings are supporting HBM and DRAM chip production, while low-voltage curing technologies are enabling applications on heat-sensitive substrates. Additionally, South Korea is a leader in high-barrier packaging solutions and premium cosmetic packaging, utilizing PVD-metallized polysiloxane coatings to combine aesthetics with durability and sustainability.

Japan Polysiloxane Coatings Market: Precision Coatings for 6G and Advanced Optics

Japan remains the global benchmark for high-precision polysiloxane coatings, particularly in applications related to semiconductors, advanced optics, and telecommunications. Innovations such as ULVAC’s ENTRON-EXX deposition system are enabling advanced coating processes for 2nm semiconductor fabrication, ensuring high reliability and process control.

The country is also pioneering 6G smart surface technologies, utilizing ultra-thin polysiloxane coatings to enhance signal transmission in urban environments. In the healthcare and packaging sectors, Japan is advancing biocompatible and high-barrier coatings, improving product performance and longevity. Updated standards such as JIS R 1703:2024 are ensuring global competitiveness in photocatalytic and self-cleaning coatings. Additionally, innovations in hydrophilic coatings for marine applications are improving safety and performance, reinforcing Japan’s leadership in advanced functional coatings.

Polysiloxane Coatings Market Report Scope

Polysiloxane Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$13.3 Billion

|

|

Market Size (2032)

|

$23.5 Billion

|

|

Market Growth Rate

|

8.5%

|

|

Segments

|

By Resin (Epoxy-Polysiloxane Hybrids, Acrylic-Polysiloxane Hybrids, Polyester-Modified Polysiloxane, Ethyl Silicate, Other Hybrids), By Technology (Solvent-borne Coatings, Water-borne Polysiloxane, Solvent-free, Powder Polysiloxane), By End-Use Industry (Marine, Protective, Oil and Gas, Power Generation, Infrastructure, Chemical Processing, Automotive and Transportation, Aerospace and Defense, Building and Construction), By Substrate Compatibility (Steel, Aluminum, Concrete and Masonry, Plastics and Composites), By Component Configuration (Two-Component, Three-Component, One-Component), By Functional Property (Corrosion Protection, UV and Weathering Resistance, Thermal, Chemical and Abrasion Resistance, Foul-Release), By Sales Channel (Direct Sales, Specialty Construction and Marine Distributors, Certified Coating Application Contractors)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

PPG Industries, Inc., Akzo Nobel N.V., The Sherwin-Williams Company, Jotun A/S, Hempel A/S, Carboline Company, Asian Paints Limited, Kansai Paint Co., Ltd., Tnemec Company, Inc., Sika AG, Axalta Coating Systems Ltd., Chugoku Marine Paints, Ltd., KCC Corporation, Nippon Paint Holdings Co., Ltd., Evonik Industries AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Polysiloxane Coatings Market Segmentation

By Resin

- Epoxy-Polysiloxane Hybrids

- Acrylic-Polysiloxane Hybrids

- Polyester-Modified Polysiloxane

- Ethyl Silicate

- Other Hybrids

By Technology

- Solvent-borne Coatings

- Water-borne Polysiloxane

- Solvent-free

- Powder Polysiloxane

By End-Use Industry

- Marine

- Protective

- Oil and Gas

- Power Generation

- Infrastructure

- Chemical Processing

- Automotive and Transportation

- Aerospace and Defense

- Building and Construction

By Substrate Compatibility

- Steel

- Aluminum

- Concrete and Masonry

- Plastics and Composites

By Component Configuration

- Two-Component

- Three-Component

- One-Component

By Functional Property

- Corrosion Protection

- UV and Weathering Resistance

- Thermal

- Chemical and Abrasion Resistance

- Foul-Release

By Sales Channel

- Direct Sales

- Specialty Construction and Marine Distributors

- Certified Coating Application Contractors

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Polysiloxane Coatings Industry

- PPG Industries, Inc.

- Akzo Nobel N.V.

- The Sherwin-Williams Company

- Jotun A/S

- Hempel A/S

- Carboline Company

- Asian Paints Limited

- Kansai Paint Co., Ltd.

- Tnemec Company, Inc.

- Sika AG

- Axalta Coating Systems Ltd.

- Chugoku Marine Paints, Ltd.

- KCC Corporation

- Nippon Paint Holdings Co., Ltd.

- Evonik Industries AG

*- List not Exhaustive