Polyurethane Coatings Market Size, High-Performance Coating Demand, and Energy-Linked Applications

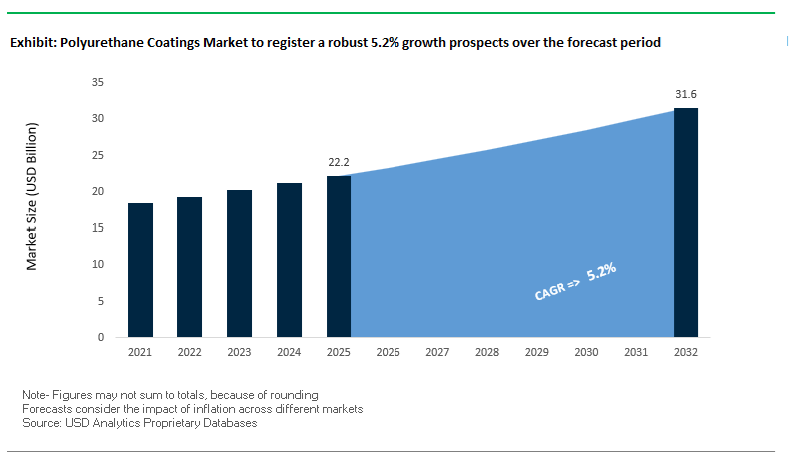

The global Polyurethane (PU) Coatings Market was valued at $22.2 billion in 2025 and is projected to grow at a CAGR of 5.2% through 2032, reaching $31.7 billion by 2032. This expansion reflects sustained demand across marine, automotive, construction, aerospace, and industrial sectors, where polyurethane coatings are preferred for their superior durability, chemical resistance, flexibility, and high-gloss aesthetic performance.

Polyurethane coatings serve as critical topcoat systems in multi-layer coating architectures, providing UV resistance, color retention, abrasion protection, and long-term weatherability. Their versatility across substrates—including metals, plastics, and composites—makes them indispensable in applications ranging from shipbuilding and offshore platforms to automotive finishes and architectural coatings.

A major structural driver is the expansion of global infrastructure and energy projects, particularly in marine, LNG, and industrial sectors, where coatings must withstand harsh environmental exposure, thermal cycling, and corrosive conditions. Additionally, the rise of electric vehicles, renewable energy systems, and advanced construction technologies is increasing demand for coatings with enhanced performance characteristics and extended service life.

Sustainability is also reshaping the PU coatings landscape. Manufacturers are increasingly developing low-VOC, waterborne, and bio-based polyurethane systems, alongside innovations that reduce the carbon footprint of coating production and application processes. The integration of energy-efficient curing technologies and mass-balance raw materials is further aligning the market with global decarbonization goals.

Market Analysis: Global Standardization of PU Systems, Capacity Expansion, and Low-Carbon Innovation Driving Market Evolution

Recent developments in the Polyurethane Coatings Market highlight a strong convergence of standardization, capacity expansion, and sustainability-driven innovation. In March 2025, Sherwin-Williams launched its expanded “Global Core” polyurethane topcoats, engineered to deliver consistent chemistry and performance across all manufacturing regions. This addresses a critical challenge in multinational infrastructure projects, ensuring compliance with ISO 12944:2018 C5 standards regardless of geographic location.

Capacity expansion is accelerating in response to rising demand. Jotun’s COSCO Qingdao facility reached a production milestone of 100 million liters in 2025, supported by a major expansion focused on high-performance marine polyurethane coatings. The company has also initiated a Phase II expansion, further increasing capacity to serve the growing shipbuilding and industrial markets in Asia.

Strategic positioning is shifting toward high-margin applications. Hempel’s “Accelerate to Win” strategy (January 2026) prioritizes polyurethane-based systems for marine and energy sectors, where performance requirements are stringent and margins are higher. The company reported strong growth in its marine segment, driven largely by PU-based fouling control and topcoat technologies.

Innovation is expanding the functional scope of polyurethane coatings. AkzoNobel’s partnership on solar-absorbing wall technology (October 2025) introduces PU coatings as active components in energy-efficient building systems, while BASF’s “Driving the Proxy” automotive trends initiative is guiding the development of next-generation PU finishes with enhanced aesthetic and durability characteristics.

Sustainability initiatives are becoming central to competitive differentiation. The AkzoNobel–BASF collaboration (May 2025) focuses on integrating bio-based PU precursors to reduce embedded carbon, while AkzoNobel’s hydrogen-powered spray booth technology demonstrates innovation in reducing emissions during the curing process of automotive PU coatings.

Market Trend: Ultra-High-Solids Polyurethane Clearcoats Redefining Automotive OEM Finishing Efficiency and Durability

The polyurethane coatings market is undergoing a significant transformation as automotive OEMs transition toward ultra-high-solids polyurethane clearcoats to meet tightening VOC regulations and elevate surface performance standards. This shift is particularly pronounced in premium vehicle segments, including electric vehicles, where high-gloss, defect-free finishes are a critical differentiator.

Emission compliance is a primary catalyst. Modern ultra-high-solids polyurethane coatings consistently achieve VOC levels below 150 g/L, representing a substantial reduction compared to legacy solventborne clearcoats operating in the 400 to 500 g/L range. This enables OEM paint shops to comply with stringent global air quality regulations while reducing reliance on costly emission control infrastructure.

Surface durability advancements are equally impactful. The integration of nano-silica reinforcement and core-shell resin architectures has significantly enhanced scratch and mar resistance. Current 2026 benchmarks show these coatings maintaining over 90% gloss retention after 2,000 cycles of steel wool abrasion testing, whereas conventional acrylic clearcoats typically experience a 40% to 60% loss in gloss under similar conditions. This improvement directly supports long-term aesthetic retention and reduced warranty claims.

Process efficiency gains further strengthen adoption. With volume solids content reaching 80% to 85%, ultra-high-solids polyurethane systems enable single-pass application to achieve target dry film thicknesses of 40 to 50 microns. This reduces overspray losses and lowers curing energy consumption by approximately 15%, improving both operational efficiency and sustainability metrics in automotive manufacturing facilities.

Market Trend: Bio-Based and Non-Isocyanate Polyurethane Coatings Advancing Sustainable Industrial Coating Technologies

Industrial equipment manufacturers are increasingly integrating bio-based polyurethane coatings to align with sustainability targets and reduce lifecycle carbon emissions. This transition is particularly evident in sectors such as agriculture, construction, and renewable energy, where coatings must deliver high mechanical performance under demanding operating conditions.

Material innovation is centered on bio-polyol integration. Modern polyurethane coatings incorporate renewable feedstocks such as castor oil, soybean derivatives, and lignin, achieving bio-based carbon content levels between 20% and 35% as verified through ASTM D6866 analysis. This enables manufacturers to reduce Scope 3 emissions without compromising coating performance.

Performance parity with conventional systems has been achieved. Bio-based polyurethane coatings demonstrate excellent adhesion characteristics, achieving 5B ratings in cross-hatch testing, and reach 2H pencil hardness within 24 hours of ambient curing. These metrics match or exceed those of traditional petroleum-based polyurethane coatings, ensuring suitability for heavy-duty industrial applications.

A parallel innovation pathway is the development of non-isocyanate polyurethane technologies. These systems utilize cyclic carbonate chemistry to eliminate the use of diisocyanates, addressing occupational health concerns related to respiratory sensitization. This shift is particularly relevant in industrial environments where worker safety regulations are becoming more stringent.

The convergence of sustainability, regulatory compliance, and high-performance characteristics is driving widespread adoption of bio-based and non-isocyanate polyurethane coatings across industrial end-use sectors.

Market Opportunity: US EPA NESHAP Subpart PPPP Driving Rapid Adoption of Low-VOC Polyurethane Coating Systems

Regulatory enforcement under the United States Environmental Protection Agency’s NESHAP Subpart PPPP is creating a strong market opportunity for advanced polyurethane coatings, particularly in applications involving plastic substrates. The updated regulatory framework imposes stricter emission limits and operational compliance requirements for coating facilities.

Facilities utilizing polyurethane coatings must meet updated emission standards by February 23, 2026, with mandatory monitoring protocols including semi-annual inspections and continuous pressure drop tracking across emission control systems. The removal of startup, shutdown, and malfunction exemptions further intensifies compliance requirements, as facilities must maintain emission limits under all operating conditions.

This regulatory environment is accelerating the transition toward high-solids and waterborne polyurethane coatings, which inherently produce lower VOC and hazardous air pollutant emissions. Manufacturers adopting these technologies can reduce regulatory risk, minimize reporting complexity, and avoid capital-intensive upgrades to emission control equipment such as regenerative thermal oxidizers.

The compliance-driven shift is expected to generate sustained demand for low-emission polyurethane coating systems, particularly among Tier 1 and Tier 2 suppliers serving automotive and consumer goods industries.

Market Opportunity: China VOCs Phase 4 Action Plan Accelerating Market Shift Toward Low-Emission Polyurethane Coatings

China’s VOCs Phase 4 Action Plan for 2026 to 2030 is emerging as a major growth driver for polyurethane coatings, particularly in high-volume manufacturing sectors. The policy introduces stringent emission limits and environmental taxation mechanisms that directly impact coating formulation and application practices.

The plan mandates the phase-out of high-emission processes and materials, including the use of HCFC-based blowing agents in related polyurethane applications, while promoting the adoption of waterborne and high-solids polyurethane systems. Coatings exceeding the newly defined VOC thresholds are subject to environmental taxes, increasing their cost competitiveness relative to compliant alternatives.

The scope of the regulation is extensive, covering 62 industrial sectors including automotive, electronics, and footwear manufacturing. This broad applicability ensures that polyurethane coatings meeting ultra-low VOC criteria will see accelerated adoption across multiple end-use industries.

In addition to emission controls, the policy framework emphasizes the development of localized, environmentally compliant coating technologies. This is expected to drive investment in domestic production capabilities for advanced polyurethane chemistries, including waterborne dispersions and high-solids formulations.

The combination of regulatory enforcement, economic incentives, and industrial policy support is creating a substantial market expansion opportunity for polyurethane coating manufacturers capable of delivering compliant, high-performance solutions.

Polyurethane Coatings Market Share and Segmentation Insights

By Product Type: Two-Component (2K) Polyurethane Coatings Dominate with Industrial-Grade Performance

The two-component (2K) polyurethane coatings segment held a leading 48.1% market share in 2025, driven by its unmatched durability, chemical resistance, and long-term performance across demanding environments. Formulated using isocyanate and polyol chemistry, 2K polyurethane coatings deliver excellent abrasion resistance, solvent resistance, and UV stability, making them the industry standard for industrial flooring, marine topside coatings, aerospace applications, and heavy equipment protection. These coatings are widely used in tank linings, pipeline coatings, and structural steel protection, where high-performance protective coatings are critical. Additionally, modern formulations feature high solids content ranging from 60% to 80%, significantly reducing volatile organic compound (VOC) emissions while maintaining superior film build and protective properties. This aligns with global environmental regulations and sustainability goals, further accelerating adoption. The combination of low-VOC polyurethane coatings, high durability, and industrial versatility ensures the continued dominance of 2K systems in the global polyurethane coatings market.

By Sales Channel: Professional Contractors Lead with Technical Expertise and Warranty Assurance

The professional contractor segment accounted for a dominant 47.6% share of the polyurethane coatings market in 2025, reflecting the essential role of skilled applicators in achieving optimal coating performance. The application of 2K polyurethane systems involves precise mixing ratios, controlled induction times, and strict humidity and temperature management, making professional expertise critical for ensuring proper curing, adhesion, and film integrity. Contractors provide advanced surface preparation and application techniques that are vital for industrial, marine, and infrastructure coating projects. Moreover, asset owners increasingly demand contractor-backed warranties ranging from 5 to 10 years, covering issues such as coating failure, delamination, and environmental degradation. This shifts performance liability away from manufacturers and distributors while enhancing buyer confidence in long-term asset protection. As demand rises for high-performance protective coatings and durable industrial finishes, the contractor-driven sales channel is expected to remain a key growth engine in the polyurethane coatings market.

Competitive Landscape of the Polyurethane Coatings Market

AkzoNobel Strengthens Market Leadership with Profit-Driven Strategy and Digital Innovation

AkzoNobel N.V. remains a cornerstone of the polyurethane coatings market, supported by strong financial performance and operational efficiency. The company reported a 27% surge in operating profit in 2025 and maintained a robust EBITDA margin of 14.2% heading into 2026. Its proposed merger with Axalta is expected to further consolidate its leadership in performance coatings and automotive refinish segments. AkzoNobel is also advancing AI-driven color matching and drone-based inspection technologies, enabling more efficient maintenance of large-scale industrial assets. Its “Winning Ways” strategy has significantly reduced operating costs while enhancing profitability, reinforcing its competitive position.

PPG Drives Innovation with Waterborne Polyurethane Coatings and EV Integration

PPG Industries, Inc. is a leading player in the polyurethane coatings market, particularly in automotive and aerospace applications. The company holds a strong share in the automotive segment, which accounts for over 30% of market demand. In 2026, PPG expanded its waterborne polyurethane coatings portfolio to comply with global environmental regulations, reducing VOC emissions. Its coatings provide superior scratch resistance and gloss retention, making them ideal for high-performance applications. PPG is also deeply integrated into the EV supply chain, offering dielectric polyurethane coatings for battery systems that enhance thermal management and safety.

Sherwin-Williams Expands Global Presence with High-Performance and Sustainable PU Coatings

The Sherwin-Williams Company is a dominant force in the polyurethane coatings market, particularly in construction and industrial applications. The company reported record sales of $23.57 billion in 2025, supported by strong growth in its Performance Coatings Group. Its EnviroLastic® and Pipeclad® polyurethane coatings are industry benchmarks for fast-curing, high-durability applications, enabling same-day return-to-service in high-traffic environments. Sherwin-Williams is also transitioning toward bio-circular polyurethane resins, aiming to capture growth in the green building sector, which is expanding at 20% annually.

BASF Leads Raw Material Innovation with Integrated Polyurethane Value Chain

BASF SE plays a critical role in the polyurethane coatings market, leveraging its integrated chemical production capabilities. The company supplies key raw materials such as MDI and TDI, ensuring cost efficiency and supply stability. In 2026, BASF introduced advanced polyurethane-based color technologies featuring interference pigments for multidimensional visual effects. Its expansion of the Zhanjiang Verbund site in China has significantly increased production capacity for polyurethane raw materials. BASF’s focus on sustainability and circular economy solutions, including its VALERAS® portfolio, strengthens its leadership in next-generation coating materials.

Axalta Strengthens Mobility Coatings Leadership with High-Efficiency Polyurethane Systems

Axalta Coating Systems is a key player in the polyurethane coatings market, particularly in automotive OEM and refinish segments. The company reported record financial performance with a 22.0% EBITDA margin, reflecting strong operational efficiency. Its Cromax® and Standox® product lines are widely recognized for fast-curing polyurethane coatings that reduce energy consumption in spray booths by up to 35%. Axalta’s strategic focus on mobility coatings and its potential merger with AkzoNobel position it as a major force in the global coatings industry.

Jotun Expands Global Leadership with High-Durability Polyurethane Coatings for Harsh Environments

Jotun Group is a leading player in the polyurethane coatings market, particularly in marine and energy sectors. Its Hardtop® series provides long-lasting protection and superior gloss retention, with coatings designed to withstand extreme environmental conditions. Jotun has integrated advanced technologies such as Hull Skating Solutions to enhance coating performance and reduce fuel consumption. The company’s strong global presence, with production facilities in over 120 countries, ensures rapid delivery and localized support. Its focus on high-performance coatings and lifecycle optimization reinforces its competitive position in the global market.

China Polyurethane (PU) Coatings Market: Dual-Carbon Strategy and Smart Cabin Innovation

China remains the global leader in the polyurethane (PU) coatings market, transitioning from high-volume production to ultra-high purity (UHP) and functional coatings aligned with advanced industries such as New Energy Vehicles (NEVs), semiconductors, and 6G electronics. The implementation of GB 30981.1-2025 has driven a rapid shift toward water-borne UV PU coatings, significantly reducing VOC emissions across key industrial clusters.

Technological advancements include the adoption of PU-based dielectric coatings for semiconductor components, supporting domestic 5nm fabrication with ultra-low contamination levels. In the automotive sector, the rise of “Smart Cabins” is fueling demand for haptic PU coatings on recycled plastics, enabling seamless touch-sensitive surfaces. Infrastructure expansion projects, including the Meishan Industrial Base, are boosting production of fast-curing polyaspartic PU systems, while innovations in IR-reflective pigments are enhancing thermal management in coastal and urban environments.

Germany Polyurethane Coatings Market: Circular Economy and Hydrogen-Ready Solutions

Germany leads the European PU coatings market through its strong focus on sustainability, circular economy principles, and advanced material innovation. The phase-out of traditional chrome plating under EU REACH Annex XIV has accelerated the adoption of PVD-on-PU systems for automotive exterior components, offering improved durability and environmental compliance.

German research is pioneering high-density PU barrier coatings that reduce hydrogen permeation by up to 99.9%, enabling safe repurposing of gas pipelines for hydrogen transport. Innovations such as self-healing PU coatings are enhancing durability in offshore wind applications, while digital traceability technologies embedded within coatings are supporting recycling and lifecycle management. Additionally, the development of high-solids dispersing agents is reducing reliance on solvent-heavy formulations, aligning with EU Green Deal objectives.

United States Polyurethane Coatings Market: Aerospace Innovation and PFAS-Free Transition

The U.S. PU coatings market is undergoing a structural transformation driven by aerospace modernization, healthcare applications, and environmental regulations. The transition toward PFAS-free PU coatings is accelerating as manufacturers prepare for upcoming regulatory mandates, ensuring compliance without compromising performance.

Aerospace manufacturers are increasingly adopting PU-coated CFRP components, achieving significant weight reductions while maintaining structural integrity. The healthcare sector is also driving growth, with widespread use of biocompatible PU coatings for medical devices. Technological advancements such as UV-LED curing systems are improving energy efficiency in automotive and industrial applications. Additionally, the adoption of sub-zero curing PU systems is expanding applications in cold-chain logistics, reinforcing the U.S. position in advanced coating technologies.

Japan Polyurethane Coatings Market: Precision Coatings and 6G Infrastructure

Japan continues to set global benchmarks in the PU coatings market, particularly in precision applications related to semiconductors, optics, and next-generation telecommunications. Innovations such as in-mold coating (IMC) technology are reducing VOC emissions and improving manufacturing efficiency for large thermoplastic components.

The country is also advancing ultra-thin PU coatings for 6G smart surfaces, enabling building facades to function as signal reflectors in future urban networks. In packaging, PVD-coated PU barrier films are extending product shelf life without additional preservatives. Updated standards like JIS R 1703:2024 are enhancing performance benchmarks for coatings on recycled plastics, while innovations in hydrophilic coatings are improving safety and functionality in marine applications.

India Polyurethane Coatings Market: Infrastructure Growth and PLI-Driven Manufacturing

India is emerging as one of the fastest-growing markets in the PU coatings industry, supported by infrastructure expansion, manufacturing localization, and government incentives. Strategic developments such as the PPG–Asian Paints joint venture renewal are strengthening domestic production capabilities for high-performance coatings.

Government support through PLI scheme expansion is encouraging local synthesis of polyols and isocyanates, reducing import dependency. Infrastructure projects under the Smart Cities Mission are driving demand for PU-coated architectural steel designed to withstand harsh environmental conditions. The growth of consumer electronics manufacturing is also increasing demand for high-volume PU coating systems, while innovations in agritech are expanding applications into sensor protection and smart farming technologies.

Saudi Arabia Polyurethane Coatings Market: Vision 2030 and Extreme Climate Applications

Saudi Arabia is emerging as a major market for high-performance PU coatings, driven by large-scale infrastructure development under Vision 2030. Projects such as NEOM are mandating the use of UV-stable PU coatings to withstand extreme desert conditions and prevent degradation over time.

The oil and gas sector is also a key driver, with PU coatings standardized for chemical-resistant flooring and pipeline protection in downstream facilities. Innovations such as IR-reflective “Cool-Poly” coatings are improving thermal management in high-temperature environments. Localization initiatives under IKTVA are strengthening domestic production of PU raw materials, enhancing supply chain resilience. Additionally, PU-coated infrastructure is being widely adopted in desalination and water management projects to improve corrosion resistance and durability.

South Korea Polyurethane Coatings Market: Semiconductor Precision and OLED Applications

South Korea’s PU coatings market is closely aligned with its leadership in semiconductors, OLED displays, and advanced electronics. The expansion of semiconductor clusters is driving demand for plasma-resistant PU coatings used in cleanroom environments and fabrication facilities.

The country is also leading in Thin-Film Encapsulation (TFE) technologies, utilizing PU-based layers to protect flexible OLED displays from moisture ingress. Innovations in marine applications include PU-infused anti-fouling coatings for LNG carriers, while advancements in packaging are driving the adoption of high-barrier PU coatings. Additionally, the K-beauty sector is increasing demand for PVD-metallized PU coatings on recycled plastic packaging, combining premium aesthetics with sustainability.

Polyurethane Coatings Market Report Scope

Polyurethane Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$22.2 Billion

|

|

Market Size (2032)

|

$31.7 Billion

|

|

Market Growth Rate

|

5.2%

|

|

Segments

|

By Technology (Solvent-borne Coatings, Water-borne Coatings, Powder Coatings, Radiation-Cured, High-Power Impulse Magnetron Sputtering), By Product Type (One-Component, Two-Component, Urethane Alkyds, Polyurethane Dispersions), By Raw Material (Isocyanates, Polyols), By Substrate Material (Metals, Wood and Timber, Plastics and Polymers, Concrete and Masonry, Textiles and Leather, Glass), By End-Use Industry (Automotive and Transportation, Building and Construction, Wood and Furniture, Aerospace and Defense, Electrical and Electronics, Marine, Industrial Manufacturing), By Functional Property (Corrosion and Chemical Resistance, Scratch and Abrasion Resistance, UV Stability and Weathering, Aesthetic, Specialty Functional), By Sales Channel (Direct Sales, Specialty Chemical and Coating Distributors, Professional Contractor)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

PPG Industries, Inc., The Sherwin-Williams Company, Akzo Nobel N.V., Axalta Coating Systems Ltd., BASF SE, Kansai Paint Co., Ltd., Nippon Paint Holdings Co., Ltd., Jotun A/S, Hempel A/S, Covestro AG, RPM International Inc., Asian Paints Limited, Stahl Holdings B.V., Sika AG, Huntsman Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Polyurethane Coatings Market Segmentation

By Technology

- Solvent-borne Coatings

- Water-borne Coatings

- Powder Coatings

- Radiation-Cured

- High-Power Impulse Magnetron Sputtering

By Product Type

- One-Component

- Two-Component

- Urethane Alkyds

- Polyurethane Dispersions

By Raw Material

By Substrate Material

- Metals

- Wood and Timber

- Plastics and Polymers

- Concrete and Masonry

- Textiles and Leather

- Glass

By End-Use Industry

- Automotive and Transportation

- Building and Construction

- Wood and Furniture

- Aerospace and Defense

- Electrical and Electronics

- Marine

- Industrial Manufacturing

By Functional Property

- Corrosion and Chemical Resistance

- Scratch and Abrasion Resistance

- UV Stability and Weathering

- Aesthetic

- Specialty Functional

By Sales Channel

- Direct Sales

- Specialty Chemical and Coating Distributors

- Professional Contractor

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Polyurethane Coatings Industry

- PPG Industries, Inc.

- The Sherwin-Williams Company

- Akzo Nobel N.V.

- Axalta Coating Systems Ltd.

- BASF SE

- Kansai Paint Co., Ltd.

- Nippon Paint Holdings Co., Ltd.

- Jotun A/S

- Hempel A/S

- Covestro AG

- RPM International Inc.

- Asian Paints Limited

- Stahl Holdings B.V.

- Sika AG

- Huntsman Corporation

*- List not Exhaustive