The global Polyurethane Foam Blowing Agents Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Type (Hydrocarbons (HC), Hydroflurocarbon (HFC), Hydrochlorofluorocarbons (HCFC), Hydrofluorocarbon (HFO)), By Application (Building, Gardening, Sound Insulation, Hutch Defends, Others).

The future of the polyurethane foam blowing agents market is influenced by key trends driving innovation and sustainability in foam insulation, packaging, and automotive applications. These trends include the increasing demand for energy-efficient building materials and lightweight automotive components, leading to the growing adoption of polyurethane foam insulation and structural foams. Manufacturers are focusing on developing next-generation blowing agents that offer improved thermal insulation properties, reduced environmental impact, and enhanced fire safety performance. Moreover, there is a growing emphasis on regulatory compliance and environmental stewardship, leading to the development of low-global-warming-potential (GWP) and zero-ozone-depletion-potential (ODP) blowing agents that meet stringent regulations and sustainability criteria. Additionally, advancements in blowing agent technology and formulation chemistry are driving the optimization of foam processing parameters, foam properties, and foam end-use performance, offering customized solutions that address the evolving needs of diverse industries and applications while minimizing environmental footprint and maximizing energy efficiency.

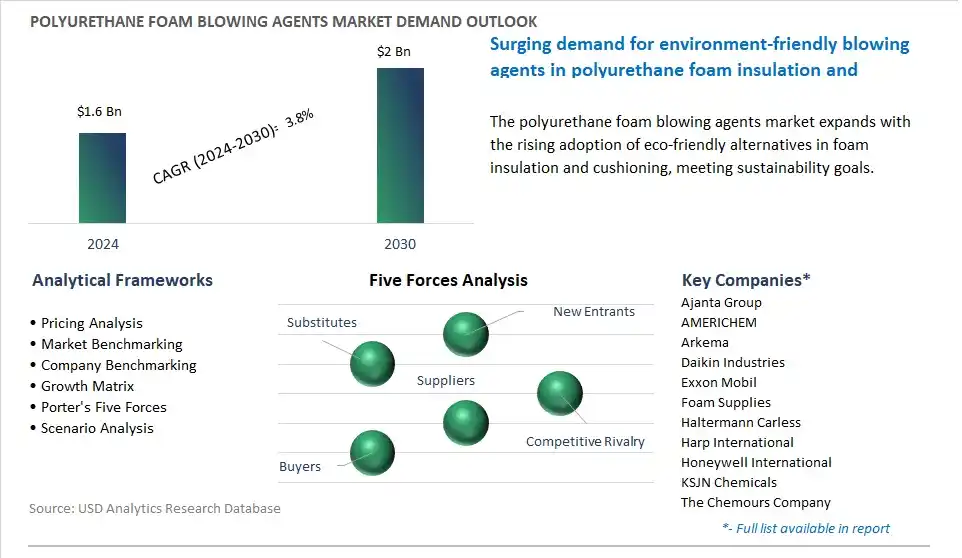

The market report analyses the leading companies in the industry including Ajanta Group, AMERICHEM, Arkema, Daikin Industries, Exxon Mobil, Foam Supplies, Haltermann Carless, Harp International, Honeywell International, KSJN Chemicals, The Chemours Company.

Polyurethane foam blowing agents are experiencing a prominent market trend driven by the transition towards environmentally friendly and low-global warming potential (GWP) formulations. With increasing regulatory restrictions and consumer demand for sustainable products, there is a growing shift away from traditional blowing agents such as hydrochlorofluorocarbons (HCFCs) and hydrofluorocarbons (HFCs) towards alternatives with lower environmental impact. Manufacturers are increasingly adopting blowing agents with reduced ozone depletion potential (ODP) and lower GWP, such as hydrocarbons (HCs), hydrofluoroolefins (HFOs), and water-based systems, to comply with regulations and meet sustainability goals. This trend is driven by the need to reduce greenhouse gas emissions, minimize ozone layer depletion, and address concerns about climate change, driving the adoption of environmentally friendly blowing agents in polyurethane foam production.

The market for polyurethane foam blowing agents is being driven by the growth in construction and automotive industries, which are significant consumers of polyurethane foam insulation and cushioning materials. With increasing construction activities, renovation projects, and energy efficiency regulations, there is a rising demand for polyurethane foam insulation materials for residential, commercial, and industrial buildings. Similarly, in the automotive sector, polyurethane foam is used for seat cushions, headrests, armrests, and interior components to enhance comfort, safety, and noise insulation in vehicles. Polyurethane foam blowing agents play a critical role in the expansion of foam materials during production, influencing foam density, thermal conductivity, and mechanical properties. The growth of construction and automotive industries drives the demand for polyurethane foam blowing agents and fosters innovation in blowing agent technologies to meet the evolving needs of end-users and regulatory requirements.

The market for polyurethane foam blowing agents presents a significant opportunity for the development of novel formulations and technologies that offer improved performance, efficiency, and sustainability. With ongoing advancements in chemistry, materials science, and process engineering, there is potential to enhance the effectiveness, stability, and processability of blowing agents to optimize foam production processes and foam properties. Opportunities exist for the development of blowing agents with enhanced compatibility with polyurethane formulations, improved foam expansion control, and reduced emissions of volatile organic compounds (VOCs) and hazardous air pollutants (HAPs). Additionally, innovations in blowing agent delivery systems, such as metering equipment, mixing technologies, and process optimization tools, offer opportunities to improve process efficiency, reduce waste, and enhance foam quality and consistency. By investing in research and development of novel blowing agent formulations and technologies, stakeholders can address emerging challenges in polyurethane foam production, differentiate their products in the market, and capitalize on the growing demand for high-performance and sustainable foam materials.

The largest segment in the Polyurethane Foam Blowing Agents Market is Hydrocarbons (HC). hydrocarbons have been widely used as blowing agents for polyurethane foam for many years due to their favorable properties such as low cost, high compatibility with polyurethane formulations, and relatively low global warming potential (GWP) compared to other types of blowing agents. Additionally, regulatory restrictions on the use of certain blowing agents like hydrochlorofluorocarbons (HCFCs) and hydrofluorocarbons (HFCs) have led to a shift towards hydrocarbons, driving their demand even further. Further, the increasing emphasis on environmental sustainability and energy efficiency has encouraged the adoption of hydrocarbon blowing agents, as they offer a more environmentally friendly alternative with reduced ozone depletion potential (ODP) and lower GWP. Consequently, the Hydrocarbons (HC) segment continues to maintain its position as the largest segment in the Polyurethane Foam Blowing Agents Market.

The fastest growing segment in the Polyurethane Foam Blowing Agents Market is the Building application segment. This segment is experiencing rapid growth. The construction industry is witnessing significant expansion globally, driven by urbanization, population growth, and infrastructure development projects. Polyurethane foam is extensively used in building applications for insulation purposes, offering excellent thermal insulation properties that help enhance energy efficiency in buildings. Additionally, the increasing awareness of sustainability and energy conservation is driving the demand for eco-friendly insulation materials, further boosting the adoption of polyurethane foam. Further, stringent building codes and regulations mandating higher energy efficiency standards are fueling the demand for advanced insulation materials like polyurethane foam, thus driving the need for efficient blowing agents. Consequently, the Building application segment is experiencing robust growth in the Polyurethane Foam Blowing Agents Market, with continued expansion expected in the foreseeable future.

By Type

Hydrocarbons (HC)

Hydroflurocarbon (HFC)

Hydrochlorofluorocarbons (HCFC)

Hydrofluorocarbon (HFO)

By Application

Building

Gardening

Sound Insulation

Hutch Defends

Others

Regions Included

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Ajanta Group

AMERICHEM

Arkema

Daikin Industries

Exxon Mobil

Foam Supplies

Haltermann Carless

Harp International

Honeywell International

KSJN Chemicals

The Chemours Company

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Polyurethane Foam Blowing Agents Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Polyurethane Foam Blowing Agents Market Size Outlook, $ Million, 2021 to 2030

3.2 Polyurethane Foam Blowing Agents Market Outlook by Type, $ Million, 2021 to 2030

3.3 Polyurethane Foam Blowing Agents Market Outlook by Product, $ Million, 2021 to 2030

3.4 Polyurethane Foam Blowing Agents Market Outlook by Application, $ Million, 2021 to 2030

3.5 Polyurethane Foam Blowing Agents Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Polyurethane Foam Blowing Agents Industry

4.2 Key Market Trends in Polyurethane Foam Blowing Agents Industry

4.3 Potential Opportunities in Polyurethane Foam Blowing Agents Industry

4.4 Key Challenges in Polyurethane Foam Blowing Agents Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Polyurethane Foam Blowing Agents Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Polyurethane Foam Blowing Agents Market Outlook by Segments

7.1 Polyurethane Foam Blowing Agents Market Outlook by Segments, $ Million, 2021- 2030

By Type

Hydrocarbons (HC)

Hydroflurocarbon (HFC)

Hydrochlorofluorocarbons (HCFC)

Hydrofluorocarbon (HFO)

By Application

Building

Gardening

Sound Insulation

Hutch Defends

Others

8 North America Polyurethane Foam Blowing Agents Market Analysis and Outlook To 2030

8.1 Introduction to North America Polyurethane Foam Blowing Agents Markets in 2024

8.2 North America Polyurethane Foam Blowing Agents Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Polyurethane Foam Blowing Agents Market size Outlook by Segments, 2021-2030

By Type

Hydrocarbons (HC)

Hydroflurocarbon (HFC)

Hydrochlorofluorocarbons (HCFC)

Hydrofluorocarbon (HFO)

By Application

Building

Gardening

Sound Insulation

Hutch Defends

Others

9 Europe Polyurethane Foam Blowing Agents Market Analysis and Outlook To 2030

9.1 Introduction to Europe Polyurethane Foam Blowing Agents Markets in 2024

9.2 Europe Polyurethane Foam Blowing Agents Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Polyurethane Foam Blowing Agents Market Size Outlook by Segments, 2021-2030

By Type

Hydrocarbons (HC)

Hydroflurocarbon (HFC)

Hydrochlorofluorocarbons (HCFC)

Hydrofluorocarbon (HFO)

By Application

Building

Gardening

Sound Insulation

Hutch Defends

Others

10 Asia Pacific Polyurethane Foam Blowing Agents Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Polyurethane Foam Blowing Agents Markets in 2024

10.2 Asia Pacific Polyurethane Foam Blowing Agents Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Polyurethane Foam Blowing Agents Market size Outlook by Segments, 2021-2030

By Type

Hydrocarbons (HC)

Hydroflurocarbon (HFC)

Hydrochlorofluorocarbons (HCFC)

Hydrofluorocarbon (HFO)

By Application

Building

Gardening

Sound Insulation

Hutch Defends

Others

11 South America Polyurethane Foam Blowing Agents Market Analysis and Outlook To 2030

11.1 Introduction to South America Polyurethane Foam Blowing Agents Markets in 2024

11.2 South America Polyurethane Foam Blowing Agents Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Polyurethane Foam Blowing Agents Market size Outlook by Segments, 2021-2030

By Type

Hydrocarbons (HC)

Hydroflurocarbon (HFC)

Hydrochlorofluorocarbons (HCFC)

Hydrofluorocarbon (HFO)

By Application

Building

Gardening

Sound Insulation

Hutch Defends

Others

12 Middle East and Africa Polyurethane Foam Blowing Agents Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Polyurethane Foam Blowing Agents Markets in 2024

12.2 Middle East and Africa Polyurethane Foam Blowing Agents Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Polyurethane Foam Blowing Agents Market size Outlook by Segments, 2021-2030

By Type

Hydrocarbons (HC)

Hydroflurocarbon (HFC)

Hydrochlorofluorocarbons (HCFC)

Hydrofluorocarbon (HFO)

By Application

Building

Gardening

Sound Insulation

Hutch Defends

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Ajanta Group

AMERICHEM

Arkema

Daikin Industries

Exxon Mobil

Foam Supplies

Haltermann Carless

Harp International

Honeywell International

KSJN Chemicals

The Chemours Company

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Type

Hydrocarbons (HC)

Hydroflurocarbon (HFC)

Hydrochlorofluorocarbons (HCFC)

Hydrofluorocarbon (HFO)

By Application

Building

Gardening

Sound Insulation

Hutch Defends

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Global Polyurethane Foam Blowing Agents is forecast to reach $2 Billion in 2030 from $1.6 Billion in 2024, registering a CAGR of 3.8%

Emerging Markets across Asia Pacific, Europe, and Americas present robust growth prospects.

Ajanta Group, AMERICHEM, Arkema, Daikin Industries, Exxon Mobil, Foam Supplies, Haltermann Carless, Harp International, Honeywell International, KSJN Chemicals, The Chemours Company

Base Year- 2023; Estimated Year- 2024; Historic Period- 2018-2023; Forecast period- 2024 to 2030; Currency: Revenue (USD); Volume